Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Driveshafts market demonstrates a valuation of approximately USD ~ billion based on a recent historical assessment, supported by steady automotive production, rising vehicle ownership, and expanding logistics operations. Demand is primarily driven by increased utilization of commercial vehicles, infrastructure development activities, and aftermarket replacement cycles. Growth is further influenced by the integration of lightweight materials and improved drivetrain efficiency, which enhance performance and fuel economy across both passenger and commercial vehicle categories.

Metro Manila, Cebu, and Calabarzon dominate the Philippines Driveshafts market due to strong automotive assembly presence, dense transportation networks, and high vehicle concentration. These regions benefit from established industrial ecosystems, including OEM facilities, distribution hubs, and aftermarket service providers. Additionally, proximity to ports and logistics infrastructure enhances supply chain efficiency, while growing urbanization and industrialization sustain consistent demand for both original equipment and replacement driveshaft systems across diverse vehicle platforms.

Market Segmentation

By Product Type

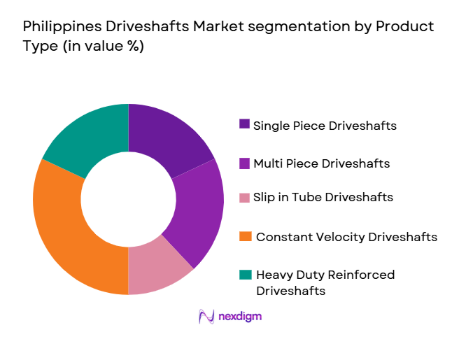

Philippines Driveshafts market is segmented by product type into single piece driveshafts, multi piece driveshafts, slip in tube driveshafts, constant velocity driveshafts, and heavy duty reinforced driveshafts. Recently, constant velocity driveshafts has a dominant market share due to increasing demand for smoother power transmission, especially in passenger and electric vehicles. Their ability to reduce vibration, enhance driving comfort, and support compact vehicle architectures has made them widely preferred among OEMs. Additionally, rising urban driving conditions and stop and go traffic patterns further support their adoption. The compatibility of CV driveshafts with modern drivetrain technologies and front wheel drive systems has reinforced their dominance across both new vehicle production and aftermarket replacements.

By Vehicle Type

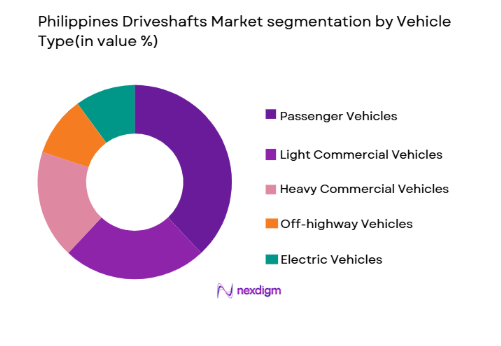

Philippines Driveshafts market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, off highway vehicles, and electric vehicles. Recently, passenger vehicles has a dominant market share due to high vehicle ownership rates and increasing urban mobility requirements. The expansion of ride hailing services and personal transportation demand has significantly boosted passenger vehicle production and usage. Additionally, frequent maintenance cycles and replacement needs in this segment contribute to strong aftermarket demand. The presence of compact and mid sized vehicles with advanced drivetrain systems further drives driveshaft consumption. This segment continues to lead due to consistent demand patterns and expanding middle class vehicle adoption.

Competitive Landscape

The Philippines Driveshafts market exhibits a moderately consolidated structure with a mix of global automotive component manufacturers and regional suppliers competing across OEM and aftermarket segments. Major players leverage technological expertise, extensive distribution networks, and strong OEM relationships to maintain competitive positioning. The market is influenced by product innovation, cost efficiency, and supply chain integration, with leading firms focusing on lightweight materials and durability enhancements to differentiate their offerings.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Driveshaft Specialization |

| GKN Automotive | 1759 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

| American Axle | 1994 | USA | ~ | ~ | ~ | ~ | ~ |

| NTN Corporation | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

| JTEKT Corporation | 2006 | Japan | ~ | ~ | ~ | ~ | ~ |

Philippines Driveshafts Market Analysis

Growth Drivers

Increasing Commercial Vehicle Demand from Logistics Expansion:

The rapid growth of logistics and e-commerce sectors has significantly increased the demand for commercial vehicles, thereby driving the Philippines Driveshafts market. With rising online retail penetration, delivery networks are expanding across urban and rural areas, requiring a larger fleet of light and heavy commercial vehicles. This expansion directly increases the need for durable and high performance driveshaft systems capable of handling continuous operations. Additionally, infrastructure projects such as road construction and urban development further boost heavy vehicle usage. Fleet operators are increasingly investing in reliable drivetrain components to minimize downtime and maintenance costs. The need for efficient power transmission in loaded vehicles enhances driveshaft demand. Moreover, replacement cycles in commercial fleets are shorter due to intensive usage, strengthening aftermarket growth. Technological advancements in driveshaft materials and design also support better efficiency and longevity. Overall, the commercial vehicle ecosystem remains a key contributor to sustained market expansion.

Rising Passenger Vehicle Ownership and Urban Mobility Trends:

Increasing disposable income and urbanization have led to higher passenger vehicle ownership, significantly contributing to the Philippines Driveshafts market growth. Consumers are increasingly opting for personal mobility solutions due to convenience and time efficiency. Urban congestion and daily commuting requirements further drive the use of compact and mid sized vehicles. These vehicles require advanced driveshaft systems for smoother and quieter performance. Automotive manufacturers are incorporating improved driveline technologies to enhance driving comfort and fuel efficiency. Additionally, ride hailing and shared mobility platforms contribute to higher vehicle utilization rates, increasing wear and tear of driveshaft components. This results in frequent replacement demand in the aftermarket segment. The shift towards automatic and front wheel drive vehicles also boosts the adoption of constant velocity driveshafts. Continuous innovation in lightweight materials further supports performance improvements. This evolving mobility landscape continues to sustain long term demand.

Market Challenges

Dependence on Imported Raw Materials and Components:

The Philippines Driveshafts market faces significant challenges due to its reliance on imported raw materials such as steel alloys and advanced composites. Fluctuations in global commodity prices directly impact manufacturing costs and profit margins for local suppliers. Additionally, supply chain disruptions can delay production timelines and affect product availability in both OEM and aftermarket segments. Import tariffs and regulatory requirements further increase procurement complexity and costs. Limited domestic production capabilities for specialized materials restrict the development of high performance driveshaft systems locally. Manufacturers often face currency exchange risks, which add to financial uncertainty. This dependency also reduces competitiveness compared to countries with strong domestic supply chains. The lack of localized innovation ecosystems limits technological advancement. As a result, companies must adopt strategic sourcing and cost optimization measures to remain competitive. Addressing these challenges requires investment in local manufacturing infrastructure and supply chain resilience.

Technical Integration Challenges with Electric and Hybrid Vehicles:

The transition towards electric and hybrid vehicles presents integration challenges for traditional driveshaft systems in the Philippines Driveshafts market. Electric vehicles require different drivetrain configurations, often reducing or modifying the role of conventional driveshafts. Manufacturers must redesign components to accommodate new powertrain architectures and performance requirements. This involves significant research and development investments and technical expertise. Additionally, compatibility with electric motors and battery systems introduces design complexities. The shift towards lightweight and compact driveline systems further intensifies engineering challenges. Limited local expertise in advanced EV driveline technologies slows adoption. Furthermore, lower maintenance requirements in electric vehicles may reduce aftermarket demand for certain driveshaft components. Market players must adapt to evolving technology trends to remain relevant. Continuous innovation and collaboration with OEMs are essential to overcome these integration barriers. The transition phase poses both operational and strategic challenges for industry participants.

Opportunities

Localization of Manufacturing and Supply Chain Development:

The growing emphasis on reducing import dependency presents a major opportunity for local manufacturing expansion in the Philippines Driveshafts market. Establishing domestic production facilities can significantly reduce costs associated with imports and logistics. It also enhances supply chain efficiency and responsiveness to market demand. Government support for industrial development and automotive manufacturing further strengthens this opportunity. Local production enables customization of driveshaft systems based on regional requirements and operating conditions. It also creates employment opportunities and strengthens the industrial ecosystem. Companies can benefit from reduced currency risk and improved pricing competitiveness. Collaboration with global technology providers can accelerate capability development. Investments in advanced manufacturing technologies can enhance product quality and innovation. This shift towards localization can drive long term sustainability and growth in the market.

Growing Demand for Lightweight and High Performance Driveshaft Systems:

Increasing focus on fuel efficiency and vehicle performance is driving demand for lightweight and advanced driveshaft systems in the Philippines Driveshafts market. Automakers are adopting materials such as aluminum and carbon fiber to reduce vehicle weight and improve efficiency. These materials offer better strength to weight ratios and enhanced durability. The trend is particularly strong in passenger vehicles and electric vehicles, where efficiency is critical. High performance driveshafts also improve acceleration and reduce vibration, enhancing driving experience. This creates opportunities for manufacturers to develop innovative product solutions. Additionally, performance oriented aftermarket segments are expanding, driven by consumer interest in vehicle upgrades. Technological advancements in material science support continuous product improvement. Companies investing in research and development can gain competitive advantage. This opportunity aligns with global trends towards sustainable and efficient mobility solutions.

Future Outlook

The Philippines Driveshafts market is expected to witness steady expansion driven by rising automotive production, infrastructure growth, and increasing vehicle ownership. Technological advancements in lightweight materials and driveline efficiency will shape product innovation. Regulatory support for local manufacturing and automotive sector development will enhance domestic capabilities. Demand from logistics, construction, and urban mobility sectors will remain strong, while electrification trends will gradually influence product design and market dynamics.

Major Players

- GKN Automotive

- Dana Incorporated

- American Axle and Manufacturing

- NTN Corporation

- JTEKT Corporation

- Schaeffler Group

- ZF Friedrichshafen AG

- Hyundai Wia Corporation

- Nexteer Automotive

- Meritor Inc

- IFA Rotorion

- Neapco Holdings

- Wanxiang Group

- Showa Corporation

- Xuchang Yuandong Drive Shaft

Key Target Audience

- Automotive OEM manufacturers

- Automotive component suppliers

- Fleet operators and logistics companies

- Government and regulatory bodies

- Investment firms and venture capitalists

- Automotive aftermarket distributors

- Construction and mining companies

- Electric vehicle manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as production volume, vehicle parc, replacement cycles, and material trends were identified. Demand drivers and supply constraints were mapped to establish market dynamics.

Step 2: Market Analysis and Construction

Data was collected from industry databases, company reports, and trade statistics. Market sizing was constructed using bottom up and top down approaches.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with industry experts, manufacturers, and distributors. Assumptions were refined based on real market feedback.

Step 4: Research Synthesis and Final Output

All data points were synthesized into a structured framework. Final insights were derived to ensure accuracy, consistency, and actionable intelligence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of automotive production and assembly operations in the Philippines

Increasing demand for commercial vehicles driven by logistics and e-commerce growth

Rising vehicle parc leading to higher aftermarket replacement demand

Growth in infrastructure and construction activities boosting heavy vehicle usage

Adoption of lightweight materials to improve fuel efficiency and performance - Market Challenges

High dependency on imported raw materials and components

Fluctuating steel and alloy prices impacting production costs

Limited domestic manufacturing capabilities for advanced driveshaft systems

Supply chain disruptions affecting timely delivery and availability

Technical complexities in integrating driveshafts with electric vehicle architectures - Market Opportunities

Localization of driveshaft manufacturing to reduce import dependency

Growing demand for high performance and lightweight driveshaft systems

Expansion of aftermarket distribution networks across regional cities - Trends

Shift towards lightweight composite driveshaft materials

Integration of advanced balancing and vibration control technologies

Increasing adoption of electric and hybrid vehicle compatible driveshafts

Digitalization in supply chain and procurement channels

Rising focus on durability and corrosion resistance in tropical environments - Government Regulations & Defense Policy

Implementation of vehicle safety and emission standards influencing component design

Policies supporting local automotive manufacturing and assembly operations

Import regulations and tariffs impacting driveshaft supply chain dynamics - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Single Piece Driveshafts

Multi Piece Driveshafts

Slip in Tube Driveshafts

Constant Velocity Driveshafts

Heavy Duty Reinforced Driveshafts - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off Highway Vehicles

Electric Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

Retrofit Installations

Performance Upgrade Fitments

Fleet Maintenance Installations - By EndUser Segment (In Value%)

Automotive OEM Manufacturers

Fleet Operators and Logistics Companies

Independent Automotive Workshops

Construction and Mining Companies

Agricultural Equipment Operators - By Procurement Channel (In Value%)

Direct OEM Supply Contracts

Authorized Distributor Networks

Online Automotive Parts Platforms

Local Spare Parts Retailers

Bulk Procurement by Fleet Owners - By Material / Technology (in Value %)

Steel Driveshaft Systems

Aluminum Driveshaft Systems

Carbon Fiber Driveshaft Systems

Hybrid Composite Driveshafts

Advanced Coated Corrosion Resistant Driveshafts

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Diversity, Material Technology Capability, Manufacturing Capacity, Pricing Strategy, Distribution Network Strength, OEM Partnerships, Aftermarket Presence, R&D Investment, Supply Chain Integration, Regional Market Reach)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

GKN Automotive

Dana Incorporated

American Axle and Manufacturing

JTEKT Corporation

NTN Corporation

Neapco Holdings

Hyundai Wia Corporation

Nexteer Automotive

Meritor Inc

Schaeffler Group

ZF Friedrichshafen AG

Showa Corporation

IFA Rotorion

Xuchang Yuandong Drive Shaft

Wanxiang Group

- Automotive OEMs focusing on cost efficient and durable driveshaft integration

- Fleet operators prioritizing reliability and reduced maintenance downtime

- Aftermarket service providers driving replacement demand across aging vehicle base

- Industrial and construction sectors requiring heavy duty and customized driveshaft solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now