Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Dual-Clutch Transmissions market demonstrates steady expansion, supported by rising automotive demand and gradual transmission technology upgrades. Based on a recent historical assessment, the market size is valued at approximately USD ~ billion, driven by increasing adoption of automatic transmission systems, urban traffic conditions requiring smoother driving, and growing consumer preference for performance-oriented vehicles. Automotive OEMs are integrating dual-clutch systems to enhance fuel efficiency and driving experience.

Metro Manila, Cebu, and Davao emerge as dominant regions due to higher vehicle density, stronger dealership networks, and greater consumer purchasing power. These urban centers benefit from developed automotive infrastructure and increased exposure to premium vehicle segments. Additionally, regional automotive assembly hubs and import distribution channels support market concentration. The presence of multinational OEMs and aftermarket service providers further reinforces demand in these locations, enabling sustained adoption of advanced transmission technologies.

Market Segmentation

By Product Type

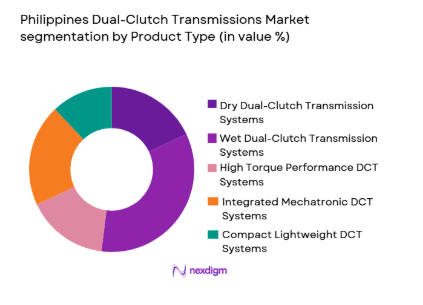

Philippines Dual-Clutch Transmissions market is segmented by product type into Dry Dual-Clutch Transmission Systems, Wet Dual-Clutch Transmission Systems, High Torque Performance DCT Systems, Integrated Mechatronic DCT Systems, and Compact Lightweight DCT Systems. Recently, Wet Dual-Clutch Transmission Systems has a dominant market share due to factors such as superior heat management, higher durability in stop-and-go traffic, and increasing deployment in premium vehicles. The Philippine driving environment, characterized by congestion and variable road conditions, favors wet systems for reliability and performance, strengthening their dominance.

By Platform Type

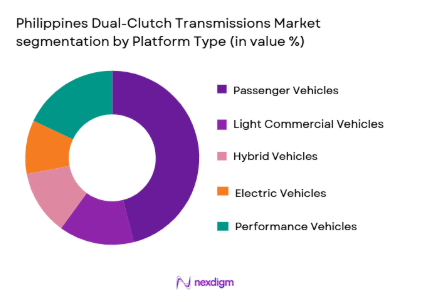

Philippines Dual-Clutch Transmissions market is segmented by platform type into Passenger Vehicles, Light Commercial Vehicles, Hybrid Vehicles, Electric Vehicles, and Performance Vehicles. Recently, Passenger Vehicles has a dominant market share due to factors such as rising urbanization, increasing middle-class income, and higher demand for comfort-oriented vehicles. Passenger vehicles dominate usage of dual-clutch systems due to consumer preference for automatic transmissions and smooth driving performance, particularly in congested metropolitan environments.

Competitive Landscape

The Philippines Dual-Clutch Transmissions market is moderately consolidated, with global transmission manufacturers maintaining strong influence through OEM partnerships and technology leadership. Major players leverage economies of scale, advanced mechatronics capabilities, and long-term supply contracts with automotive brands. Market competition is shaped by product reliability, cost optimization, and aftermarket service capabilities, while regional distributors and service providers support localized penetration and maintenance networks.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Partnership Strength |

| Aisin Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| BorgWarner Inc. | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Magna International Inc. | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

| Schaeffler AG | 1946 | Germany | ~ | ~ | ~ | ~ | ~ |

Philippines Dual-Clutch Transmissions Market Analysis

Growth Drivers

Rising Consumer Preference for Automatic and Performance Vehicles:

The Philippines automotive market is witnessing a structural shift toward automatic transmissions, driven by increasing urbanization and traffic congestion. Consumers are prioritizing convenience, reduced driver fatigue, and smoother gear transitions, making dual-clutch transmissions an attractive option. The demand for premium driving experiences is expanding beyond luxury vehicles into mid-range segments. OEMs are actively incorporating DCT systems to differentiate product offerings. Increased disposable income supports vehicle upgrades. Younger consumers show higher inclination toward technologically advanced vehicles. Improved financing options further boost vehicle sales. The integration of DCT technology enhances fuel efficiency and performance balance. As awareness increases, adoption rates are expected to rise steadily.

Expansion of Automotive Manufacturing and Regional Supply Chains:

The Philippines benefits from growing integration into Southeast Asia’s automotive supply chain, encouraging adoption of advanced transmission technologies. Regional trade agreements facilitate component imports and assembly operations. OEMs are expanding local assembly capabilities to reduce costs and improve responsiveness. Supply chain improvements enable better availability of DCT components. Increased foreign direct investment supports technology transfer. Government incentives for automotive manufacturing strengthen production capacity. Collaboration between global suppliers and local partners enhances ecosystem efficiency. This expansion drives cost competitiveness of DCT systems. Improved logistics infrastructure supports distribution and aftermarket services. The strengthening supply chain directly contributes to sustained market growth.

Market Challenges

High Cost and Maintenance Complexity of Dual-Clutch Systems:

Dual-clutch transmission systems remain significantly more expensive than conventional manual or automatic transmissions, limiting their penetration in cost-sensitive markets. Consumers in the Philippines often prioritize affordability, making adoption slower in entry-level vehicle segments. Maintenance complexity adds to the total cost of ownership, discouraging long-term usage. Specialized service requirements increase dependency on authorized service centers. Limited availability of trained technicians further exacerbates maintenance challenges. Replacement parts are relatively expensive and sometimes imported. Consumer perception of high repair costs affects purchasing decisions. Warranty limitations also influence buyer confidence. These factors collectively restrain widespread adoption despite performance benefits.

Limited Compatibility with Low-Power and Budget Vehicle Segments:

Dual-clutch transmissions are typically optimized for higher torque and performance applications, creating limitations in small-engine vehicles common in the Philippines. Budget vehicles dominate the market, reducing immediate applicability of DCT systems. Manufacturers face challenges in cost-effective integration for entry-level models. Lower engine displacement vehicles may not fully utilize DCT advantages. Engineering adjustments increase production costs. Consumer awareness regarding benefits remains limited in this segment. OEMs prioritize traditional transmissions for cost efficiency. Market education efforts are still evolving. Infrastructure limitations for servicing further hinder adoption. This restricts DCT penetration primarily to mid and high-end vehicles.

Opportunities

Growing Adoption in Hybrid and Electrified Vehicle Platforms:

The transition toward electrified mobility creates significant opportunities for dual-clutch transmission integration, particularly in hybrid vehicles. Hybrid powertrains benefit from efficient gear shifting and torque management offered by DCT systems. Automotive manufacturers are developing advanced transmission solutions compatible with hybrid architectures. Government incentives supporting cleaner mobility indirectly promote advanced transmission technologies. Rising environmental awareness influences consumer preferences. DCT systems contribute to improved fuel efficiency and reduced emissions. Collaboration between transmission manufacturers and EV developers is increasing. Technological advancements enable lightweight and compact designs. The hybrid segment is expected to serve as a major growth avenue. This evolution opens new revenue streams for market participants.

Expansion of Aftermarket Retrofit and Upgrade Solutions:

The aftermarket segment presents a growing opportunity as vehicle owners seek performance enhancements and transmission upgrades. Increasing vehicle lifespan encourages investment in retrofitting advanced systems. Automotive enthusiasts drive demand for performance-oriented modifications. Service providers are expanding capabilities to install and maintain DCT systems. Availability of retrofit kits is improving gradually. Digital platforms enable easier access to aftermarket products. Growing awareness of DCT benefits supports adoption. Fleet operators may also explore upgrades for efficiency improvements. Competitive pricing strategies enhance accessibility. This segment offers long-term growth potential beyond OEM sales channels.

Future Outlook

The Philippines Dual-Clutch Transmissions market is expected to experience gradual expansion over the next five years, supported by increasing vehicle electrification, evolving consumer preferences, and technological advancements in transmission systems. OEMs are likely to expand DCT integration into broader vehicle categories, including hybrids and premium compact cars. Regulatory focus on fuel efficiency and emissions reduction will further support adoption. Additionally, improvements in cost optimization and service infrastructure are anticipated to enhance market accessibility.

Major Players

- Aisin Corporation

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Magna International Inc.

- Schaeffler AG

- Getrag Transmission Systems

- Hyundai Transys

- Jatco Ltd.

- Ricardo plc

- GKN Automotive

- Punch Powertrain

- Valeo SA

- Continental AG

- Eaton Corporation

- Dana Incorporated

Key Target Audience

- Automotive OEM manufacturers

- Automotivecomponent suppliers

- Fleet operators and logistics companies

- Automotive dealerships

- Aftermarket service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive technology developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including vehicle sales trends, transmission adoption rates, consumer preferences, and OEM strategies were identified to establish a foundational understanding of the Philippines Dual-Clutch Transmissions market dynamics.

Step 2: Market Analysis and Construction

Comprehensive data collection from automotive industry databases, trade statistics, and manufacturer reports enabled construction of market sizing models and segmentation frameworks for accurate analysis.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, automotive engineers, and supply chain stakeholders were consulted to validate assumptions, refine projections, and ensure alignment with real-world market conditions.

Step 4: Research Synthesis and Final Output

All findings were synthesized into structured insights, ensuring consistency, accuracy, and actionable intelligence tailored to stakeholders evaluating the Philippines Dual-Clutch Transmissions market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing demand for fuel efficient and high performance vehicles

Growing penetration of automatic and semi automatic transmissions

Expansion of automotive manufacturing and assembly in Southeast Asia

Rising consumer preference for smoother gear shifting technologies

Technological advancements in mechatronics and transmission control - Market Challenges

High cost of dual clutch systems compared to manual transmissions

Maintenance complexity and higher repair costs

Limited awareness among budget vehicle buyers

Compatibility challenges with low power engine vehicles

Supply chain constraints for specialized transmission components - Market Opportunities

Expansion of DCT adoption in hybrid and electric vehicles

Growth in premium and performance vehicle segment demand

Aftermarket retrofit opportunities for automatic transmission upgrades - Trends

Integration of AI based adaptive shifting technologies

Shift towards lightweight and compact transmission designs

Increasing use of wet clutch systems for durability improvement

Rising demand for seamless driving experience in urban traffic conditions

Development of energy efficient transmission systems for EV platforms - Government Regulations & Defense Policy

Emission norms encouraging efficient transmission technologies

Automotive import and localization policies in the Philippines

Safety and vehicle performance compliance regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Dry Dual-Clutch Transmission Systems

Wet Dual-Clutch Transmission Systems

Integrated Mechatronic DCT Systems

High Torque Performance DCT Systems

Compact Lightweight DCT Systems - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Electric Vehicles

Hybrid Vehicles

Performance and Sports Vehicles - By Fitment Type (In Value%)

OEM Factory Fitments

Aftermarket Replacement Systems

Retrofit Conversion Systems

Performance Upgrade Installations

Fleet Maintenance Installations - By EndUser Segment (In Value%)

Automotive OEM Manufacturers

Fleet Operators and Logistics Providers

Individual Vehicle Owners

Performance Tuning and Motorsport Firms

Automotive Service and Repair Centers - By Procurement Channel (In Value%)

Direct OEM Procurement

Authorized Dealer Networks

Aftermarket Distributors

Online Automotive Platforms

Third Party Component Suppliers - By Material / Technology (in Value %)

Electro Hydraulic Control Systems

Advanced Friction Materials

Lightweight Alloy Gear Assemblies

Electronic Control Units Integration

AI Enabled Transmission Control Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio, Technology Integration, Pricing Strategy, Regional Presence, Production Capacity, OEM Partnerships, Aftermarket Reach, Innovation Capability, Supply Chain Strength, Customer Base Diversity)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Aisin Corporation

BorgWarner Inc.

ZF Friedrichshafen AG

Magna International Inc.

Schaeffler AG

Getrag Transmission Systems

Hyundai Transys

Jatco Ltd.

Ricardo plc

GKN Automotive

Punch Powertrain

Valeo SA

Continental AG

Eaton Corporation

Dana Incorporated

- OEMs focusing on integrating advanced transmission systems for competitive differentiation

- Fleet operators prioritizing fuel efficiency and reduced downtime

- Consumers shifting toward automatic transmission comfort in urban driving

- Service providers expanding capabilities for complex transmission maintenance

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now