Download PDF

Download PDFMarket Overview

The Philippines echocardiography equipment market is valued at approximately USD ~ million in 2024, driven by increasing cases of cardiovascular diseases and rising awareness regarding early diagnosis and preventive care. The demand for advanced echocardiography systems, particularly 3D/4D and portable units, is surging due to improvements in healthcare infrastructure, growing urbanization, and governmental healthcare initiatives aimed at tackling heart disease. The market growth is also accelerated by the adoption of point-of-care diagnostic solutions, as well as advancements in artificial intelligence integration within echocardiography devices.

Metro Manila, particularly Quezon City, Makati, and Pasig, is the dominant region for echocardiography equipment adoption, driven by the concentration of top-tier hospitals, diagnostic clinics, and specialized heart centers. Furthermore, Cebu and Davao are emerging as key markets due to improvements in regional healthcare facilities and the expansion of diagnostic services in these areas. The increased healthcare spending by both public and private sectors in urban and suburban centers is significantly contributing to the growth of the echocardiography equipment market in these areas.

Market Segmentation

By Product Type

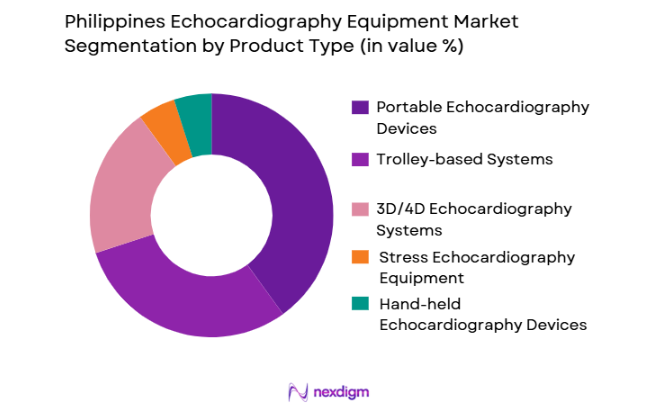

The Philippines echocardiography equipment market is segmented by product type, primarily into portable echocardiography devices, trolley-based systems, and advanced 3D/4D echocardiography systems. Among these, the portable echocardiography devices dominate the market due to their flexibility and ability to perform quick diagnostics in various settings, including remote and rural areas. The increasing demand for portability and cost-efficiency in diagnostic services has made portable echocardiography devices a preferred choice for healthcare providers in hospitals and clinics. Their compact nature allows for better mobility and convenience, which is essential in emergency and critical care situations. The trend towards miniaturized and handheld devices also contributes to their market dominance.

By Application

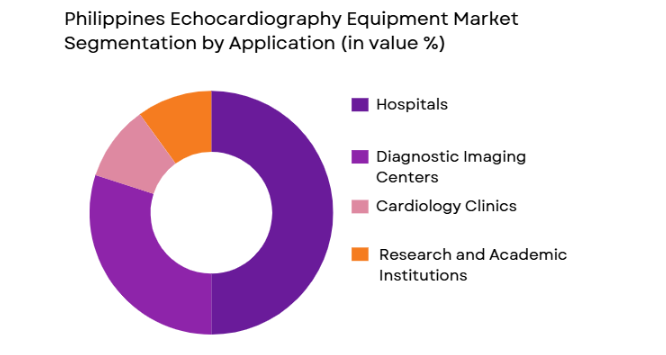

The market is also segmented by application, which includes cardiology clinics, hospitals (ICU, ER, and cardiology departments), diagnostic imaging centers, and research institutions. The hospital segment dominates due to the increasing number of cardiac care departments and specialized heart centers that require advanced echocardiography systems for continuous monitoring of heart conditions. Hospitals invest heavily in advanced and high-performance echocardiography systems, especially for high-risk patients and those undergoing surgery. Moreover, the shift towards non-invasive diagnostic tools to monitor heart conditions in emergency and critical care settings has led to the dominance of this segment in the market.

Competitive Landscape

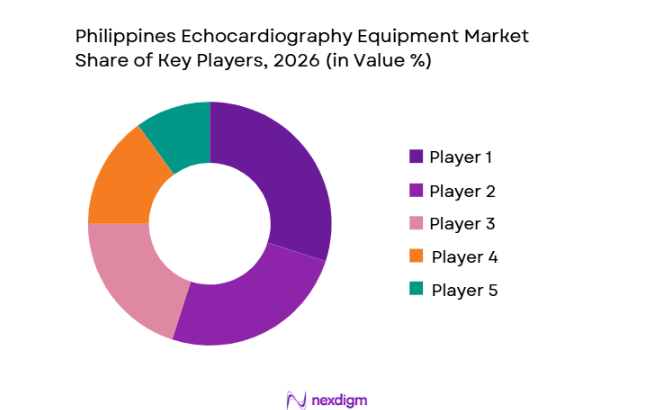

The Philippines echocardiography equipment market is dominated by a few major international and regional players. Global players such as GE Healthcare, Philips Healthcare, and Siemens Healthineers lead the market due to their advanced technology, comprehensive product portfolios, and strong distribution networks. These companies leverage their technological innovations and offer solutions like 3D/4D echocardiography systems and portable models, which are driving market expansion. Local players like Mindray and Edan Instruments are also gaining market share by offering cost-effective solutions that cater to the growing demand for affordable diagnostic equipment in hospitals and clinics across the country.

| Company | Establishment Year | Headquarters | Key Market Parameter 1 | Key Market Parameter 2 | Key Market Parameter 3 | Key Market Parameter 4 | Key Market Parameter 5 | Key Market Parameter 6 |

| GE Healthcare | 1892 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Mindray | 1991 | China | ~ | ~ | ~ | ~ | ~ | ~ |

| Edan Instruments | 1995 | China | ~ | ~ | ~ | ~ | ~ | ~ |

Philippines Echocardiography Equipment Market Analysis

Growth Drivers

Urbanization

The rapid pace of urbanization in the Philippines is a significant driver for the adoption of echocardiography equipment. As of 2025, over ~% of the country’s population resides in urban areas, primarily in Metro Manila, Cebu, and Davao, with urban areas expected to account for ~% of the total population by 2025 (World Bank). This trend has led to an increased demand for advanced medical technologies, including echocardiography, as healthcare infrastructure expands to meet the needs of urban populations. The rise in health-conscious urbanites, coupled with accessible healthcare facilities in these areas, has driven the demand for diagnostic devices, especially in cardiology departments.

Industrialization

The Philippines’ industrialization, especially in the manufacturing and energy sectors, has resulted in the growth of industrial zones, often leading to increased pollution and a higher incidence of cardiovascular diseases. Industrial activity contributes significantly to environmental changes and lifestyle diseases, particularly heart disease. The increasing urban workforce exposed to air pollution and high-stress environments has increased the demand for healthcare services, leading to a higher need for diagnostic equipment like echocardiography systems. As industries grow, the healthcare infrastructure follows suit to support the rise in medical cases, including heart-related diseases.

Restraints

High Initial Costs

One of the significant barriers to the widespread adoption of echocardiography equipment in the Philippines is the high initial cost of advanced echocardiography machines. As of 2025, the cost of high-end echocardiography systems, such as 3D/4D models, can range from USD ~ to USD ~. This high upfront investment can be a major hurdle for smaller healthcare facilities, especially in rural and remote areas, where budgets are constrained. The high cost of maintenance and the need for specialized training for operators further adds to the financial burden, limiting the accessibility of advanced echocardiography equipment.

Technical Challenges

Technical challenges related to the installation, calibration, and maintenance of echocardiography systems pose a significant barrier to market growth. Many healthcare providers, particularly in less urbanized regions, struggle to implement and maintain these high-tech devices due to the lack of technical expertise. The complexity of modern echocardiography systems, including the integration of AI and 3D imaging, requires highly skilled personnel to operate and troubleshoot, and this remains a challenge in the Philippines, where there is a shortage of trained echocardiography technicians and medical professionals.

Opportunities

Technological Advancements

There are significant opportunities for the Philippines echocardiography equipment market due to ongoing technological advancements in medical imaging systems. The shift toward portable, handheld, and AI-integrated echocardiography devices has opened up new markets, especially for rural clinics and emergency medical services. These devices are not only more affordable but also offer real-time diagnostic capabilities, improving the accessibility of heart disease diagnosis. The integration of telemedicine with echocardiography allows for remote monitoring and consultation, presenting a major opportunity to expand healthcare coverage in underserved regions.

International Collaborations

International collaborations between the Philippines government and global medical technology companies present substantial growth prospects for the echocardiography equipment market. Partnerships aimed at enhancing healthcare infrastructure, including the deployment of advanced diagnostic devices, are expected to boost the adoption of echocardiography equipment in both private and public healthcare settings. The Philippines’ healthcare sector is expected to benefit from foreign investments, which will enable the modernization of diagnostic facilities and the incorporation of cutting-edge technologies in hospitals and clinics across the country.

Future Outlook

Over the next five years, the Philippines echocardiography equipment market is expected to show robust growth driven by continuous technological advancements, the rising demand for preventive healthcare, and increasing cardiovascular disease prevalence. Key drivers include the growing adoption of portable echocardiography devices in both urban and rural areas, expanding access to advanced diagnostic technologies, and government initiatives aimed at improving healthcare infrastructure. The market is also expected to witness increased integration of AI and telemedicine solutions, which will enhance diagnostic accuracy and remote monitoring capabilities.

Major Players in the Philippines Echocardiography Equipment Market

- GE Healthcare

- Philips Healthcare

- Siemens Healthineers

- Mindray

- Fujifilm Holdings

- Canon Medical Systems

- Hitachi Medical Corporation

- Esaote S.p.A.

- Edan Instruments

- Toshiba Medical Systems Corporation

- Schiller AG

- Nihon Kohden Corporation

- SonoSite, Inc.

- Samsung Medison

- Aloka Co. Ltd

Key Target Audience

- Healthcare Providers (Hospitals and Clinics)

- Diagnostic Imaging Centers

- Medical Device Manufacturers

- Distributors and Dealers of Medical Equipment

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies (Department of Health, Philippine FDA)

- Medical Research Institutes

- Healthcare Technology Innovators

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key market variables affecting the Philippines echocardiography equipment market. This is achieved by collecting industry-level data through secondary research and analyzing variables like product demand, technological adoption, and regional healthcare infrastructure.

Step 2: Market Analysis and Construction

This phase includes the compilation and analysis of historical data, assessing factors such as market penetration, healthcare infrastructure, and technological trends. Data is segmented by equipment type, application, and end-users to provide a comprehensive market understanding.

Step 3: Hypothesis Validation and Expert Consultation

The market hypothesis is validated through expert consultations with industry leaders and practitioners. Interviews with medical professionals, hospital administrators, and government bodies provide valuable insights into the market’s growth drivers and challenges.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data gathered through both bottom-up and top-down approaches. Insights from manufacturers, distributors, and end-users are integrated to ensure the accuracy and reliability of market projections.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Philippines-Specific Terminologies, Abbreviations, Market Sizing Logic, Bottom-Up & Top-Down Validation, Triangulation Framework, Primary Interviews Across Healthcare Providers, Diagnostic Centers, Government Agencies, and Industry Experts, Demand-Side & Supply-Side Weightage, Data Reliability Index, Limitations & Forward-Looking Assumptions)

- Definition and Scope

- Market Genesis and Evolution Pathway

- Philippines Echocardiography Equipment Industry Timeline

- Echocardiography Equipment Business Cycle

- Supply Chain & Value Chain Analysis

- Market Trends Shaping the Echocardiography Landscape

- Regulatory Landscape Impacting Echocardiography Systems

- Key Growth Drivers

Rising Incidence of Cardiovascular Diseases

Technological Advancements in Echocardiography Equipment

Increased Government and Healthcare Investments

Growing Awareness of Preventive Healthcare - Market Challenges

High Initial Equipment Costs

Lack of Skilled Professionals

Regulatory and Compliance Barrier - Market Opportunities

Emerging Demand for Point-of-Care Devices

Technological Innovations in Mobile and Portable Devices

Expanding Healthcare Facilities in Rural Areas - Key Trends

Integration with Artificial Intelligence and Machine Learning

Remote Monitoring and Telemedicine Adoption

Advancements in Mobile Echocardiography Devices - Regulatory & Policy Landscape

Philippine FDA Regulations on Medical Devices

Quality Assurance and Standards for Echocardiography Equipment

Government Healthcare Initiatives and Funding - SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces Analysis

- Competition Ecosystem

- By Value, 2019-2025

- By Volume, 2019-2025

- By Average Price, 2019-2025

- By Product Type (In Value %)

Portable Echocardiography Devices

Trolley-based Echocardiography Systems

3D/4D Echocardiography Systems

Stress Echocardiography Equipment

Hand-held Echocardiography Device - By Application (In Value %)

Cardiology Clinics

Hospitals (ICU, ER, Cardiology Departments)

Diagnostic Imaging Centers

Research and Academic Institutions - By End-User (In Value %)

Hospitals

Diagnostic Laboratories

Private Cardiology Practices

Medical Research Institutes - By Region (In Value %)

Luzon

Visayas

Mindanao - By Technology (In Value %)

2D Echocardiography

3D/4D Echocardiography

Doppler Echocardiography

Color Flow Doppler

Tissue Doppler Imaging - By Testing Mode (In Value %)

Manual Testing

Automated Testing

- Market Share Analysis

Market Share by Product Type

Market Share by Region - Cross Comparison Parameters (Product Portfolio Breadth, Technology Integration, Distribution Footprint, Regulatory Approvals, R&D Investment & Technological Advancements, Strategic Partnerships & Collaborations, Customer Reach, Testing Accuracy & Reliability, Cost-Effectiveness)

- SWOT Analysis of Key Players

- Competitive Benchmarking of Key Players

- Pricing Analysis (Price Trends for Different Equipment Models)

- Comparison of Prices Across Major Providers

- Detailed Company Profiles

GE Healthcare

Philips Healthcare

Siemens Healthineers

Canon Medical Systems

Mindray

Fujifilm Holdings

Samsung Medison

Esaote S.p.A.

Toshiba Medical Systems Corporation

Edan Instruments, Inc.

Schiller AG

Nihon Kohden Corporation

Aleo Medical

SonoSite, Inc.

Hitachi Medical Corporation

- Demand Pattern and Utilization Metrics

- Procurement Models and Purchasing Cycles for Echocardiography Equipment

- Compliance and Certification Requirements

- Consumer Needs, Desires, and Pain-Point Mapping

- Decision-Making Framework for Healthcare Providers and Suppliers

- Cost vs. Security Prioritization in Equipment Selection

- By Value, 2026-2030

- By Volume, 2026-2030

- By Average Price, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now