Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines edge computing market is closely linked to the country’s data center and digital infrastructure ecosystem, which reached approximately USD ~ billion based on a recent historical assessment. Rapid enterprise digitalization, telecom edge deployments, and cloud-to-edge integration initiatives are expanding localized processing capacity across industries such as manufacturing, telecom, retail, and public services. Strong investment in hyperscale and edge-enabled data facilities is accelerating adoption of low-latency computing architectures supporting real-time analytics, IoT platforms, and AI-driven applications.

Within Southeast Asia, Metro Manila remains the primary edge infrastructure hub due to dense enterprise clusters, telecom interconnection nodes, and proximity to major submarine cable landing stations enabling regional data exchange. Cebu and Davao are emerging secondary edge locations supported by government digital corridor programs, growing IT-BPM presence, and regional cloud deployment needs. The Philippines benefits from regional hyperscaler expansion across Singapore and Indonesia, creating cross-border edge traffic flows and positioning the country as an emerging distributed computing node in ASEAN digital infrastructure networks.

Market Segmentation

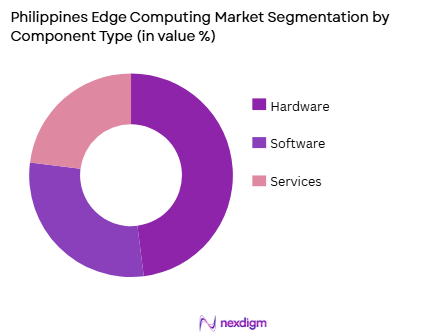

By Component

Philippines Edge Computing market is segmented by component into hardware, software, and services. Recently, hardware has a dominant market share due to factors such as telecom edge node deployment, micro data center rollout, and enterprise on-premise edge infrastructure investment. Telecom operators and hyperscale providers prioritize physical edge equipment including servers, gateways, and localized storage to enable low-latency applications and 5G traffic offloading. Enterprise sectors including manufacturing, logistics, and retail also invest in ruggedized edge hardware for real-time analytics and automation use cases. Software and services adoption is growing but remains dependent on installed hardware base expansion and operational integration maturity.

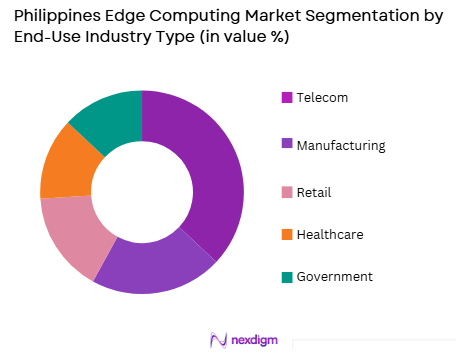

By End-Use Industry

Philippines Edge Computing market is segmented by end-use industry into telecom, manufacturing, retail, healthcare, and government. Recently, telecom has a dominant market share due to factors such as 5G rollout acceleration, mobile data traffic growth, and multi-access edge computing deployment strategies. Telecom providers deploy distributed edge nodes to reduce latency, manage network congestion, and enable new services including AR/VR streaming, IoT connectivity, and real-time analytics platforms. Enterprise sectors increasingly adopt edge capabilities, but telecom infrastructure ownership and nationwide network coverage position it as the primary enabler and largest investor in edge computing architecture across the Philippines digital ecosystem.

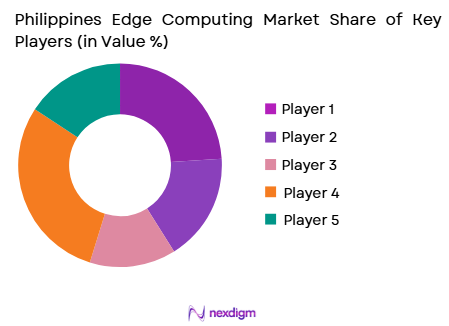

Competitive Landscape

The Philippines edge computing market shows moderate consolidation with telecom operators, global cloud providers, and data center specialists shaping infrastructure deployment and platform ecosystems. International hyperscalers influence architecture standards and enterprise adoption through regional cloud-edge integration, while domestic telecom firms control last-mile connectivity and distributed node rollout. Strategic partnerships between telecom operators and data center providers are expanding micro-edge facilities nationwide. Competition centers on latency performance, edge coverage density, and hybrid cloud compatibility rather than pure hardware differentiation.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Strategy |

| PLDT | 1928 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Globe Telecom | 1935 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Converge ICT | 2007 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Equinix | 1998 | USA | ~ | ~ | ~ | ~ | ~ |

| NTT Ltd. | 1999 | Japan | ~ | ~ | ~ | ~ | ~ |

Philippines Edge Computing Market Analysis

Growth Drivers

5G-Enabled Distributed Computing Infrastructure Expansion

The nationwide rollout of fifth-generation mobile networks is fundamentally reshaping digital traffic patterns in the Philippines, creating structural demand for distributed computing architectures positioned closer to users and devices. Telecom operators are deploying multi-access edge computing nodes within base station networks to reduce latency and support bandwidth-intensive applications including video analytics, immersive media, and industrial IoT. Edge computing enables localized processing of massive mobile data volumes generated by urban populations and connected devices, preventing congestion in centralized data centers. Enterprises adopting automation, smart retail, and logistics optimization require millisecond-level processing responsiveness that centralized cloud infrastructure cannot consistently deliver across archipelagic geography. Government digital transformation programs and smart city initiatives further accelerate localized infrastructure deployment, particularly in urban corridors. Hyperscale cloud providers are integrating regional edge zones with national telecom networks to extend hybrid cloud services to enterprise clients. Industrial sectors including manufacturing and energy increasingly rely on real-time monitoring and predictive analytics systems deployed at edge sites. The Philippines’ high mobile penetration and data consumption rates amplify the economic value of low-latency computing capabilities. Continuous telecom capital expenditure toward fiber backhaul and 5G coverage expansion sustains long-term infrastructure demand for edge computing ecosystems.

Enterprise Digitalization and Real-Time Data Processing Requirements

The acceleration of enterprise digital transformation across Philippine industries is driving demand for localized computing architectures capable of processing data streams at source rather than distant centralized facilities. Manufacturing plants deploying automation, robotics, and sensor-based monitoring require immediate analytics processing to maintain operational continuity and quality control. Retail and logistics networks depend on edge-enabled inventory tracking, computer vision, and predictive demand systems that function with minimal latency. Financial services institutions increasingly utilize edge computing for fraud detection, transaction monitoring, and customer analytics executed near transaction endpoints. Healthcare providers adopt edge-based diagnostics and medical imaging processing to support telemedicine and distributed care networks across islands. Enterprises face regulatory and data sovereignty considerations encouraging localized processing and storage within national boundaries. Edge infrastructure improves reliability and resilience in regions with variable connectivity by enabling autonomous operation independent of central cloud access. Hybrid cloud architectures integrating enterprise data centers with edge nodes allow scalable deployment of AI workloads and analytics platforms. Digital services growth across e-commerce, streaming, and online platforms generates continuous real-time data streams requiring local processing capacity. As enterprises prioritize operational intelligence and automation, edge computing becomes a foundational layer of modern Philippine digital infrastructure ecosystems.

Market Challenges

Fragmented Infrastructure and Geographic Deployment Complexity

The Philippines’ archipelagic geography presents significant logistical and economic challenges for uniform edge computing deployment, requiring distributed infrastructure across multiple islands with varying connectivity maturity. Telecom backhaul capacity, power reliability, and fiber availability differ substantially between metropolitan and provincial regions, complicating consistent edge node performance. Deploying micro data centers and edge facilities in remote or secondary cities involves high transportation, installation, and maintenance costs relative to concentrated urban deployments. Environmental exposure risks including typhoons, flooding, and humidity require specialized ruggedized infrastructure design increasing capital expenditure. Network latency optimization across islands requires redundant routing and submarine cable connectivity, adding engineering complexity. Enterprises outside major cities often lack localized connectivity and data center ecosystems needed to support edge adoption. Skilled workforce availability for managing distributed infrastructure remains concentrated in urban technology hubs. Power grid reliability variations across regions affect operational continuity of localized computing nodes. Land acquisition and facility construction for distributed sites increase deployment timelines. These structural geographic and infrastructure constraints slow nationwide edge computing penetration despite strong demand drivers.

High Capital Intensity and Integration Complexity of Edge Architectures

Edge computing deployment requires substantial upfront investment in hardware nodes, localized data facilities, fiber connectivity, and software orchestration platforms, creating financial barriers for many Philippine enterprises. Telecom operators and hyperscale providers bear significant capital expenditure in nationwide node rollout before realizing service revenue. Integrating edge systems with legacy enterprise IT infrastructure and centralized cloud platforms requires complex orchestration frameworks and interoperability engineering. Enterprises face uncertainty in selecting scalable edge architectures compatible with evolving standards and vendor ecosystems. Return on investment depends on application maturity and real-time analytics adoption, which varies across sectors. Operational management of distributed nodes increases maintenance and monitoring costs compared to centralized computing models. Cybersecurity risks expand with distributed processing endpoints requiring advanced protection systems. Talent shortages in edge computing architecture and distributed systems engineering raise implementation costs. Smaller enterprises often lack financial capacity and technical expertise to deploy dedicated edge infrastructure. These economic and technical integration challenges constrain broader market adoption despite clear performance benefits.

Opportunities

Expansion of Regional Edge Data Centers Beyond Metro Manila

Secondary Philippine cities including Cebu, Davao, Iloilo, and Clark present significant growth potential for localized edge infrastructure supporting regional enterprises and telecom networks. Government regional development programs and digital corridor initiatives are encouraging data infrastructure investment outside the capital region. IT-BPM sector expansion in provincial cities generates enterprise demand for low-latency computing and data processing capabilities. Regional logistics hubs and manufacturing zones require localized analytics and automation platforms enabling operational efficiency. Telecom operators extending 5G coverage into secondary urban centers necessitate distributed edge nodes for traffic management and service delivery. Real estate development of technology parks and economic zones supports micro data center deployment opportunities. Regional hospitals and public services digitalization initiatives require localized processing capacity for healthcare and administrative systems. Submarine cable landing diversification across islands enhances inter-regional connectivity supporting distributed computing architecture. Energy and utilities modernization programs in provincial areas create industrial edge deployment opportunities. As regional economies grow and digital adoption spreads, secondary city edge infrastructure becomes a major expansion frontier for providers.

Integration of Edge Computing with AI and IoT Ecosystems

The convergence of artificial intelligence, Internet of Things, and edge computing technologies creates substantial innovation opportunities in Philippine industrial and urban sectors. Smart manufacturing systems combining sensors, robotics, and AI analytics require edge-based processing for real-time decision making and automation control. Smart city initiatives deploying surveillance, traffic monitoring, and environmental sensors depend on localized analytics platforms to process data streams efficiently. Agriculture modernization programs integrating IoT monitoring and predictive analytics benefit from distributed computing near farms and rural facilities. Energy grid management and renewable integration systems rely on edge-enabled control and monitoring across distributed assets. Retail analytics using computer vision and customer behavior tracking require local processing to minimize latency and bandwidth consumption. Healthcare diagnostics and wearable monitoring solutions benefit from edge AI inference capabilities at patient proximity. Autonomous systems and drones deployed in logistics and infrastructure inspection depend on localized processing. Telecom providers monetizing 5G services through edge-enabled applications create new enterprise service markets. The fusion of AI, IoT, and edge computing positions the Philippines for advanced digital infrastructure adoption across sectors.

Future Outlook

The Philippines edge computing market is expected to expand rapidly over the next five years as 5G coverage deepens and enterprise digitalization accelerates nationwide. Telecom and hyperscale providers will continue deploying distributed edge nodes across metropolitan and regional cities. AI-enabled real-time applications and IoT ecosystems will increase demand for localized processing capacity. Government digital infrastructure programs and regional economic development initiatives will support broader edge adoption. Hybrid cloud-edge architectures will become standard enterprise IT models across Philippine industries.

Major Players

- PLDT

- Globe Telecom

- Converge ICT

- Equinix

- NTT Ltd.

- Digital Realty

- Huawei

- Cisco Systems

- Dell Technologies

- Microsoft

- Amazon Web Services

- Alibaba Cloud

- Vertiv

- Schneider Electric

- EdgeConneX

Key Target Audience

- Telecom operators

- Cloud service providers

- Data center operators

- Enterprise IT infrastructure firms

- Manufacturing companies

- Healthcare networks

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including telecom edge deployment, enterprise digitalization intensity, data center capacity, and regional infrastructure distribution were identified through secondary data review. Technology adoption drivers and sector-specific edge use cases were mapped across industries. Supply-side capabilities and demand-side requirements were aligned.

Step 2: Market Analysis and Construction

Market structure was constructed by analyzing telecom infrastructure expansion, enterprise IT spending patterns, and regional digitalization indicators. Edge computing value chain components including hardware, software, and services were evaluated. End-use sector adoption dynamics were modeled.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions regarding deployment patterns, adoption barriers, and growth drivers were validated through expert interviews and technology ecosystem analysis. Telecom, cloud, and enterprise infrastructure perspectives were incorporated. Regional infrastructure feasibility assessments refined projections.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative findings were synthesized into a structured market model describing segmentation, competition, and growth dynamics. Strategic trends and opportunity zones were identified. Final analysis integrated infrastructure, technology, and industry demand factors shaping the Philippines edge computing market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising 5G network rollout requiring distributed compute infrastructure

Expansion of digital services and latency-sensitive applications across enterprises

Growth of smart city and IoT deployments in urban Philippines regions - Market Challenges

Limited domestic data center capacity outside major metropolitan areas

Power and connectivity reliability constraints in secondary islands

Shortage of specialized edge infrastructure engineering skills - Market Opportunities

Edge-enabled AI analytics for retail, transport, and public safety use cases

Localization of content delivery and cloud gaming infrastructure

Industrial automation and predictive maintenance in export manufacturing zones - Trends

Convergence of telecom and enterprise edge platforms

Adoption of micro modular data center architectures

Integration of edge AI accelerators in distributed sites - Government regulations

National broadband and connectivity expansion policies

Data privacy and localization compliance requirements

Smart city and digital infrastructure funding programs - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Data Centers

Micro Edge Nodes

On-Premise Edge Appliances

Edge AI Accelerators

Ruggedized Edge Gateways - By Platform Type (In Value%)

Telecom Network Edge

Enterprise Campus Edge

Industrial Edge Platforms

Smart City Edge Infrastructure

Content Delivery Edge - By Fitment Type (In Value%)

New Deployment Installations

Retrofit Edge Enablement

Integrated OEM Edge Systems

Modular Add-on Edge Units

Cloud-managed Edge Integration - By End User Segment (In Value%)

Telecommunications Providers

Manufacturing and Industrial Firms

Retail and E-commerce Operators

Transport and Logistics Operators

Government and Smart City Agencies - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Operator Contracts

System Integrator Deployment

Cloud Service Provider Bundling

Public Sector Tenders

- Market Share Analysis

- Cross Comparison Parameters (Deployment Scale, Latency Performance, Power Efficiency, Edge AI Capability, Integration Ecosystem, Network Proximity, Scalability Architecture, Management Orchestration, Security Compliance, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

PLDT

Globe Telecom

DITO Telecommunity

ePLDT

ST Telemedia Global Data Centres Philippines

Converge ICT Solutions

Schneider Electric Philippines

Vertiv Philippines

Huawei Technologies Philippines

Nokia Philippines

ZTE Philippines

Dell Technologies Philippines

Hewlett Packard Enterprise Philippines

Cisco Systems Philippines

Fujitsu Philippines

- Telecom operators deploying edge nodes to support 5G and content delivery demand

- Manufacturers adopting edge analytics for production efficiency and monitoring

- Retail and logistics firms using edge for real-time inventory and tracking

- Government agencies implementing edge for surveillance and urban services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now