Download PDF

Download PDFMarket Overview

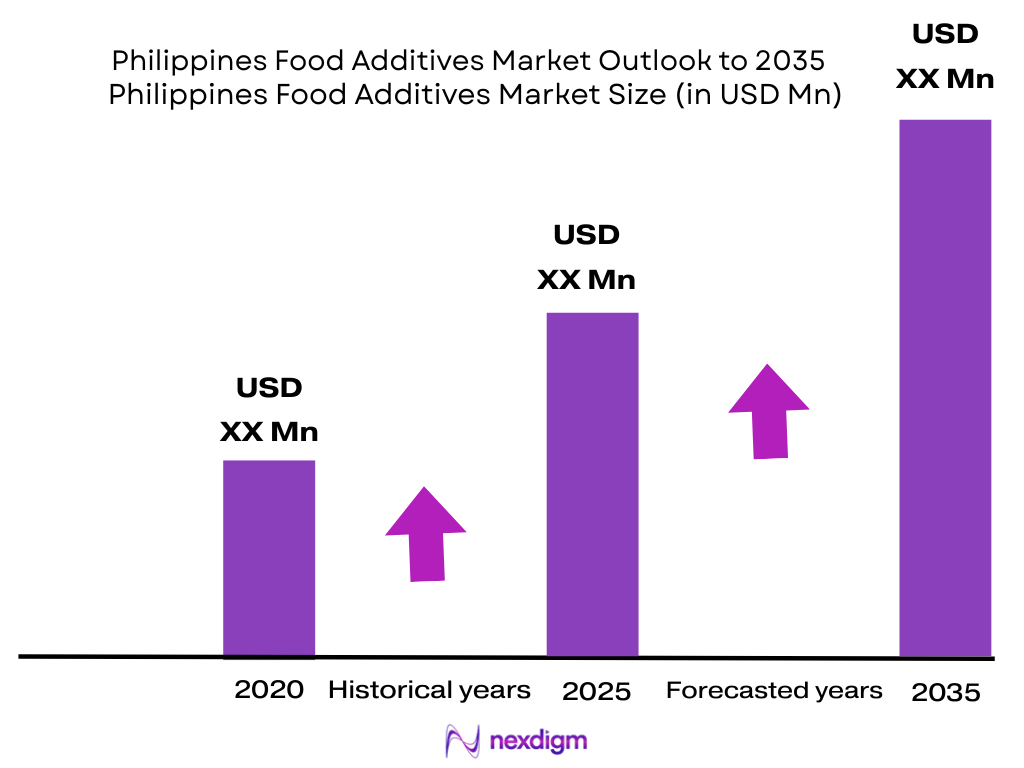

The Philippines food additives market is valued at approximately USD ~ million, supported by the expansion of packaged foods, beverages, processed meat, bakery products, sauces and convenience meals. Food-manufacturing production recorded numerical index growth of 3.9 in the latest comparable period versus 8.5 for overall manufacturing in the preceding period, while household consumption growth moved from 5.6 to 4.8. Rising formulation complexity, shelf-life requirements and product standardization sustain additive procurement. Metro Manila, CALABARZON, Central Luzon, Cebu and Davao form the principal demand centres because they combine food-processing plants, ports, warehouses, modern retail networks and large consumer markets. The national market must serve more than 7,600 islands, increasing the need for preservatives, stabilizers and shelf-life systems. The country’s gross national income per capita reached USD 4,470, while the economic reporting framework covers 82 provinces and 33 highly urbanized cities, supporting increasingly dispersed food-additive demand.

Market Segmentation

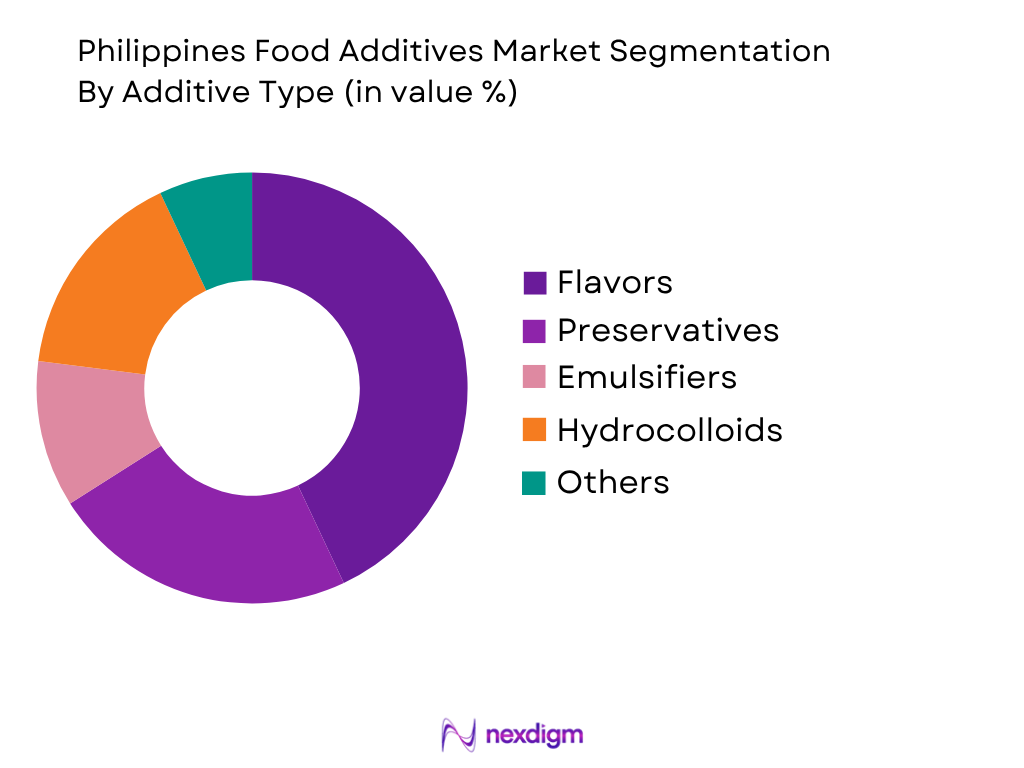

By Additive Type

The Philippines food additives market is segmented by additive type into flavors and flavor enhancers, preservatives, emulsifiers and stabilizers, sweeteners, colors, acidulants, enzymes, and nutritional additives. Flavors and flavor enhancers hold the dominant market share because taste differentiation is central to beverages, instant noodles, snacks, sauces, meat products and bakery items. Philippine manufacturers frequently adapt formulations to sweet, savory, tropical-fruit and umami-oriented taste preferences. Large processors also require standardized flavor delivery across plants and production batches. The segment benefits from frequent product launches and reformulation, since flavor systems can refresh an existing product without major capital investment. Local preferences for calamansi, mango, coconut, pandan, ube, cheese, barbecue and seafood profiles further expand demand for customized systems. Flavor suppliers also provide masking, mouthfeel and sodium-reduction technologies, allowing them to participate in health-oriented reformulation beyond basic taste creation. Global suppliers increasingly position themselves as co-development partners rather than commodity vendors.

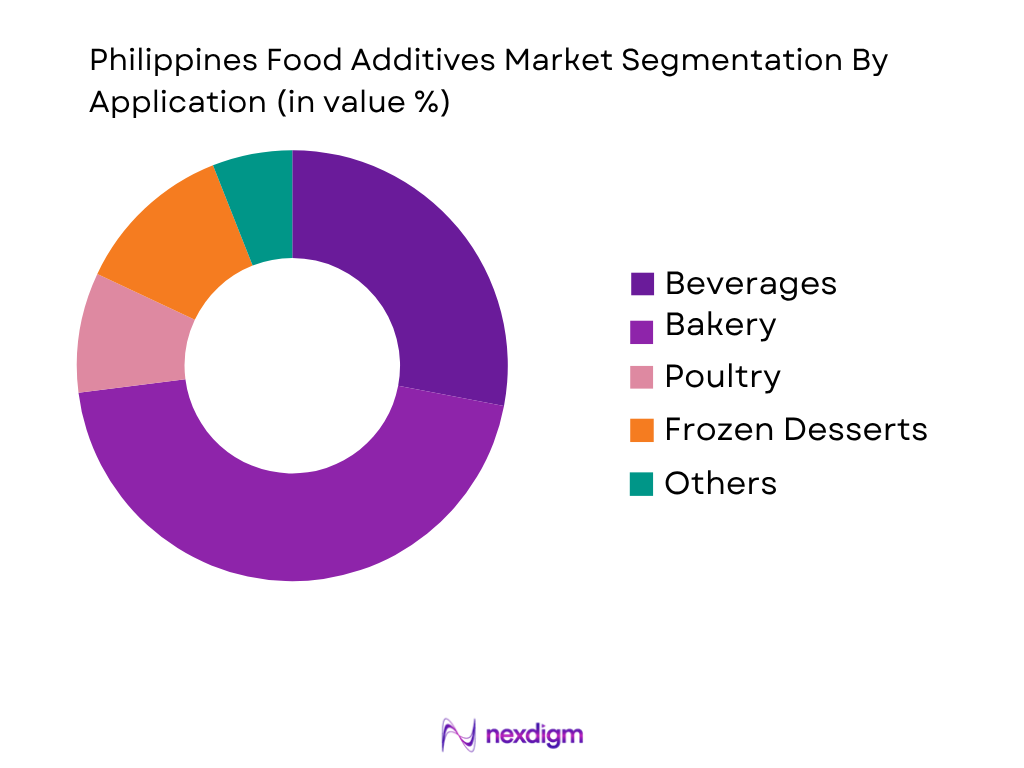

By Application

The Philippines food additives market is segmented by application into beverages, bakery products, processed meat and poultry, snacks and instant noodles, dairy products, sauces and condiments, confectionery, and functional nutrition. Beverages hold the dominant market share because a typical commercial formulation may require flavors, sweeteners, colors, acidulants, preservatives, stabilizers, clouding agents and micronutrient premixes. The category covers carbonated drinks, juices, powdered beverages, energy drinks, flavored water, milk-based drinks and ready-to-drink coffee or tea. Beverage manufacturers operate high-volume production lines and require precise ingredient consistency because minor formulation variations can affect taste, appearance, sedimentation and shelf life. Demand is also stimulated by frequent flavor extensions, smaller packaging formats and functional claims. Tropical conditions increase the importance of microbial control and emulsion stability. Powdered drink manufacturers further support demand for encapsulated flavors, anti-caking agents, sweetener blends and color systems that remain stable during storage and reconstitution.

Competitive Landscape

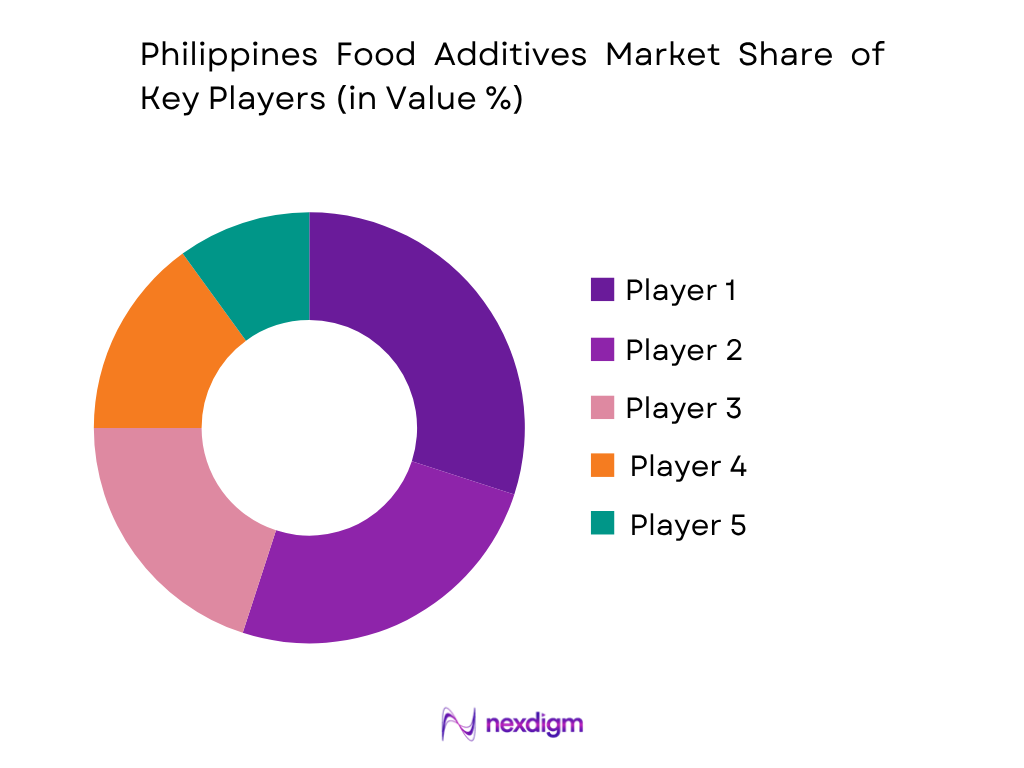

The Philippines food additives market includes global taste and nutrition companies, multinational agricultural ingredient groups, international specialty distributors, domestic ingredient traders and local formulation houses. Competition is moderately fragmented, but large accounts are concentrated among suppliers capable of providing complete regulatory files, stable imported supply, application testing and customized formulation support. Kerry’s investment in a customer co-creation centre in Taguig illustrates the growing importance of local technical collaboration, while Brenntag maintains an established Philippine ingredients-distribution presence.

| Company | Establishment year | Headquarters | Core additive portfolio | Philippine operating model | Major applications | Technical capability | Clean-label capability | Distribution strength |

| Kerry Group | 1972 | Tralee, Ireland | ~ | ~ | ~ | ~ | ~ | ~ |

| Cargill | 1865 | Minneapolis, United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Brenntag | 1874 | Essen, Germany | Food ingredients, preservatives, acidulants, sweeteners, hydrocolloids and specialty additives | ~ | ~ | ~ | ~ | ~ |

| Brenntag | 1874 | Essen, Germany | Food ingredients, preservatives, acidulants, sweeteners, hydrocolloids and specialty additives | ~ | ~ | ~ | ~ | ~ |

| Azelis | 2001 | Antwerp, Belgium | Specialty ingredients, hydrocolloids, emulsifiers, flavors and nutritional systems | ~ | ~ | ~ | ~ | ~ |

Philippines Food Additives Market Analysis

Growth Drivers

Expansion of Processed-Food Production and Consumer Demand

The expansion of Philippine food manufacturing is increasing the addressable demand for preservatives, flavors, emulsifiers, stabilizers, sweeteners, colors, enzymes, acidulants and nutritional premixes. The Philippine Statistics Authority reported that the production index for food manufacturing increased by 5.2% in November 2024, compared with 1.4% in October 2024, indicating higher activity across food-processing facilities. This matters because additive consumption is tied directly to production batches: greater output of beverages, bakery goods, processed meat, noodles, sauces and dairy products requires proportionately more functional ingredients. Household final consumption expenditure increased by 4.8% in 2024, while spending on food and non-alcoholic beverages reached PHP 2.531 trillion, compared with PHP 2.237 trillion in 2023. Food and non-alcoholic beverages remained the largest component of household expenditure, providing a broad demand base for packaged-food manufacturers. The Philippines also had a population of approximately 115.84 million people in 2024, while its urban population reached 56.32 million, creating a large concentration of consumers who rely increasingly on manufactured, packaged and convenience-oriented foods. The country’s GDP amounted to USD 461.62 billion in 2024, with GDP per capita reaching USD 3,984.8, supporting continued development of modern retail, quick-service restaurants, convenience stores and institutional foodservice. For additive suppliers, the important effect is not simply higher food consumption, but the increasing industrialization of food preparation. Commercial manufacturers require repeatable flavor profiles, controlled texture, microbial stability and predictable shelf life across large production volumes. The need to transport finished foods between Luzon, Visayas and Mindanao further strengthens the use of preservation and stabilization systems. Beverage producers require combinations of flavors, acidulants, sweeteners, colors and stabilizers, while industrial bakeries use mold inhibitors, enzymes, emulsifiers and humectants. Processed-meat manufacturers depend on phosphates, antioxidants, hydrocolloids and flavor systems. Consequently, expansion in food output and household demand generates multi-category growth rather than demand for a single additive class.

Regulatory Formalization and Product Standardization

The continuing formalization of food regulation is driving demand for documented, standardized and technically validated food additives. Philippine FDA Administrative Order No. 2024-0015 established updated rules, requirements and procedures governing License-to-Operate applications for FDA-regulated establishments. These requirements increase the importance of traceability, compliant sourcing, specifications, certificates of analysis and consistent manufacturing controls across importers, distributors and food processors. The Philippine FDA also applies the Codex General Standard for Food Additives food-category system, which links permitted additives to specific technological functions, food applications and maximum use conditions. Proposed updates to the country’s additive framework consolidate permitted food additives and processing aids used in both locally manufactured and imported products. This regulatory direction benefits suppliers capable of providing complete technical files, additive identity details, purity specifications, allergen declarations, safety documentation and internationally recognized additive numbers. The Philippine economy contained 82 provinces and 33 highly urbanized cities in the latest government economic reporting framework, making consistent compliance and product quality important for manufacturers distributing food nationally. The country also recorded USD 200.87 billion in total merchandise trade during 2024, including USD 73.27 billion in exports. Food manufacturers participating in international supply chains must meet both domestic requirements and importing-country standards, reinforcing demand for additives with reliable documentation and controlled performance. Regulatory harmonization additionally encourages processors to replace undocumented or inconsistently supplied ingredients with products sourced from established manufacturers and authorized distributors. Food companies developing beverages, bakery products, meat products, nutrition products and processed foods must verify whether every additive is permitted for the relevant food category and whether its use remains within applicable limits. This makes regulatory support an integral component of supplier selection. Global ingredient companies and specialized distributors can differentiate themselves through compliance reviews, formulation guidance and assistance with product-registration documentation. Local blenders are similarly encouraged to strengthen quality-control systems and batch traceability. Rather than acting solely as a constraint, formal regulation supports market development by increasing confidence in legally compliant food technologies and reducing uncertainty around additive identity, quality and use.

Market Challenges

Import Dependence and Raw-Material Supply Volatility

The Philippines food additives market remains exposed to imported active ingredients, agricultural feedstocks and intermediate materials. The Philippine Statistics Authority reported agricultural imports of USD 19.46 billion in 2024, demonstrating the scale of the country’s dependence on external agricultural supply. Agricultural trade reached USD 27.22 billion, while fourth-quarter agricultural imports amounted to USD 5.18 billion, compared with USD 4.65 billion in the corresponding 2023 period. This dependence affects additives derived from corn, sugar, starch, seaweed, fruits, fermentation substrates, oils and botanical extracts. Domestic agricultural output also faced material constraints. Crop production totaled 80.41 million metric tons in 2024, compared with 85.83 million metric tons in 2023. Sugarcane output declined by 13.5%, while palay production decreased by 4.8%. These reductions are relevant to food-additive manufacturers because sugar, starch and carbohydrate feedstocks support sweetener systems, fermentation-derived ingredients, carriers, modified starches and encapsulated flavors. Fisheries production during the fourth quarter reached 1.07 million metric tons, down from 1.17 million metric tons in the corresponding period, while crop production in the same quarter fell from 27.46 million metric tons to 24.94 million metric tons. Volatility in local raw-material availability can limit the feasibility of domestic extraction and additive production, maintaining reliance on imported concentrates and functional ingredients. Importers also operate within a national trade system that handled USD 200.87 billion in merchandise flows in 2024, exposing food ingredients to port congestion, documentation requirements and competition for logistics capacity. Additives are frequently purchased in foreign currency and transported in bags, drums or intermediate bulk containers. Delays can therefore result in stock shortages, emergency sourcing and production interruptions. The challenge is particularly acute for specialized enzymes, natural colors, cultures, high-intensity sweeteners and proprietary flavor systems that cannot be substituted immediately. Food manufacturers must conduct laboratory testing, sensory assessment and shelf-life validation before changing suppliers. Market participants consequently need safety inventories, alternative approved sources, regional procurement arrangements and stronger local blending capacity to reduce the operational impact of imported-input volatility.

Regulatory Complexity and Technical Qualification Requirements

Food-additive commercialization requires manufacturers and suppliers to address detailed regulatory and technical requirements before an ingredient can be used at production scale. Philippine FDA rules require covered establishments to hold appropriate operating authorization, while processed-food registrations must rely on additives permitted under the latest Codex General Standard for Food Additives, the applicable FDA listing or other recognized permitted-use frameworks. The FDA’s updated licensing order, Administrative Order No. 2024-0015, affects regulated establishments handling food products and ingredients. In addition, the agency adopted Codex technical regulations for specialized product categories in 2025, including standards covering ready-to-use therapeutic foods and products for older infants and young children. These regulations address additive use together with quality factors, purity requirements, contaminants, hygiene, labeling and analytical methods. For market participants, this means additive acceptance depends on more than commercial availability. Suppliers must demonstrate identity, purity, technological need, appropriate dosage, food-category compatibility and labeling compliance. A flavor system may contain carriers, solvents, preservatives or colors that must each be assessed. A stabilizer blend can combine several hydrocolloids and emulsifiers requiring accurate declaration. Imported products may also need certificates of analysis, manufacturing information, allergen statements, safety data and evidence of compliance with relevant microbiological or contaminant limits. Technical qualification adds another layer of complexity. Beverage producers must test sedimentation, pH stability, flavor interaction and microbial control. Bakeries evaluate dough handling, crumb structure, moisture retention and mold development. Meat processors assess yield, water binding, texture, color and storage stability. These trials can require laboratory screening, pilot runs, plant-scale validation and shelf-life observation before approval. The challenge is greater for small and medium-sized food processors that may lack dedicated regulatory teams, application laboratories or experienced food technologists. Suppliers must therefore provide intensive technical assistance while managing relatively small order volumes. Regulatory changes can also force processors to review formulas, labels and product registrations. Companies without robust documentation or local technical personnel face longer commercialization cycles and a higher risk of rejected formulations, delayed launches or non-compliant declarations.

Market Opportunities

Local Blending, Formulation and Import Substitution

The country’s high dependence on imported agricultural and ingredient inputs creates a significant opportunity for domestic blending, compounding, repacking and application-specific formulation. Agricultural imports reached USD 19.46 billion in 2024, while total agricultural trade amounted to USD 27.22 billion. Imports from ASEAN suppliers alone reached USD 1.97 billion in the third quarter of 2024, with Vietnam supplying USD 636.34 million of agricultural products during that period. These figures indicate that Philippine food manufacturing already operates within a large regional supply network that can support local value addition. Instead of importing every additive as a finished formulation, domestic businesses can import active ingredients or concentrates and convert them into flavor blends, bakery improver systems, beverage stabilizers, seasoning preparations, micronutrient premixes and preservation systems tailored to local applications. Government investment activity provides an enabling industrial context. The Board of Investments reported PHP 1.15 trillion in approved investments by July 2024, compared with PHP 699 billion in the corresponding prior period. Its Green Lane initiative covered 176 projects by December 2024, including 23 food-security projects valued at PHP 14.37 billion and 4 manufacturing projects valued at PHP 36.91 billion. Separately, BOI and Department of Agriculture collaboration supported PHP 9.59 billion in approved agriculture-related projects. These investments can improve the broader availability of processing facilities, utilities, logistics and food-industry inputs required for ingredient localization. Local blending can reduce shipment lead times, enable smaller minimum order quantities and allow formulas to be adjusted for Philippine taste preferences, production equipment and climatic conditions. It also permits suppliers to serve medium-sized processors that cannot import full containers or hold large inventories. Priority opportunities include seasoning systems, customized flavor blends, bakery improvers, hydrocolloid systems, vitamin and mineral premixes, natural preservation blends and beverage bases. The strongest market position will belong to companies that combine local stockholding with quality assurance, batch traceability, application testing and Philippine FDA compliance.

Clean-Label, Fortification and Functional Formulation Solutions

Changing product-development priorities create an opportunity for suppliers of natural, multifunctional and nutrition-oriented additive systems. The Philippines had approximately 115.84 million residents in 2024, including an urban population of 56.32 million, providing a substantial consumer base for packaged beverages, bakery goods, snacks, dairy products and convenience meals. Household spending on food and non-alcoholic beverages reached PHP 2.531 trillion, up from PHP 2.237 trillion in 2023, while food remained the largest household-consumption category. These conditions support continued product launches and reformulation by food manufacturers seeking differentiation through nutrition, natural positioning, reduced sugar, reduced sodium or simplified ingredient declarations. The economic environment also provides a platform for premium and functional product development: national GDP reached USD 461.62 billion, and GDP per capita reached USD 3,984.8 in 2024. Market opportunities extend beyond replacing synthetic ingredients individually. Manufacturers increasingly require complete systems that maintain taste, color, texture and shelf life after reformulation. Removing an artificial preservative may require a combination of acidity control, cultured ingredients, natural extracts, packaging changes and improved manufacturing hygiene. Reducing sugar can require high-intensity sweeteners, bulking agents, flavor modulators and mouthfeel enhancers. Sodium reduction may combine yeast extracts, nucleotides, savory flavors and mineral salts. Fortified products require vitamin and mineral premixes that remain stable through processing and storage. The Philippine FDA’s adoption of Codex-based food categories and its 2025 technical regulations for therapeutic foods and young-child products reinforce the need for precisely formulated nutrition systems with controlled additive use, purity and labeling. Current food-production momentum also supports commercialization: food-manufacturing output increased by 5.2% in November 2024, providing a wider industrial platform for specialty formulations. Suppliers that offer local sensory testing, pilot trials, shelf-life assessment and regulatory assistance can capture greater value than commodity traders. High-potential solutions include natural colors stable under tropical conditions, fermented preservatives, clean-label starches, encapsulated flavors, sugar-reduction blends, sodium-reduction systems and micronutrient premixes designed for beverages, bakery goods and nutrition products.

Future Outlook

The Philippines food additives market is expected to expand at a forecast CAGR of approximately % during the forecast period. Growth will be supported by packaged-food production, urban convenience consumption, quick-service restaurant expansion and demand for products capable of withstanding longer distribution cycles. Product reformulation will create additional demand for natural preservation, sugar reduction, sodium reduction and clean-label texture systems. Beverage, bakery, processed meat, snacks and condiments will remain the core volume-generating applications. Higher-value growth is expected in functional beverages, fortified foods, plant-based products, natural colors, fermentation-derived ingredients and integrated functional blends. Rather than purchasing individual additives, manufacturers are expected to increase procurement of combined systems designed to solve several formulation requirements simultaneously.

Major Players

- Kerry Ingredients Philippines

- Cargill Philippines

- Brenntag Ingredients Philippines

- DKSH Philippines

- Azelis Philippines

- Caldic Philippines

- dsm-firmenich Philippines

- International Flavors & Fragrances Philippines

- Givaudan Philippines

- Symrise Philippines

- BNC Ingredients Corporation

- New Flavor House

- SBS Philippines Corporation

- TNC Chemicals Philippines

- Philippine Aminosan Corporation

Key Target Audience

- Global food additive and specialty ingredient manufacturers

- Philippine food and beverage manufacturers

- Food ingredient importers, distributors and compounders

- Industrial bakery, beverage, dairy, meat and snack producers

- Investments and venture capitalist firms

- Private-equity firms and strategic corporate investors

- Logistics, warehousing and ingredient supply-chain operators

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase constructs the Philippines food additives ecosystem covering global principals, local manufacturers, importers, distributors, blenders and food processors. Secondary research is used to identify additive categories, application sectors, import dependency, pricing variables and regulatory requirements that materially influence demand.

Step 2: Market Analysis and Construction

Historical demand is assessed through food-manufacturing output, import flows, supplier revenues, application production and additive-consumption coefficients. The top-down model applies additive-intensity ratios to bakery, beverage, meat, dairy, snack and condiment production.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary hypotheses are validated through computer-assisted telephone interviews with additive suppliers, food technologists, procurement managers, quality-assurance teams and regulatory specialists. Interviews examine dosage rates, supplier selection, average prices, import lead times, customer qualification and switching behavior.

Step 4: Research Synthesis and Final Output

The final phase triangulates top-down and bottom-up findings to develop the market size, segmentation and forecast. Differences between import values, distributor revenue and end-use consumption are adjusted for inventory movement, inactive product registrations, re-exports and intermediary margins.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Food Additive Classification Framework, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Import-Based Supply Assessment, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry and Regulatory Developments

- Food Additives Industry Value Chain Analysis

- Supply Chain Analysis

- Import Dependency and Local Formulation Landscape

- Growth Drivers (Expansion of Packaged Food Manufacturing, Rising Demand for Shelf-Stable Foods, Growth of Beverage and Bakery Production, Expansion of Quick-Service Restaurants, Increasing Demand for Product Consistency, Growth of Fortified Foods, Urbanization and Convenience Food Consumption)

- Market Challenges (Dependence on Imported Active Ingredients, Foreign-Exchange Volatility, International Freight Cost Fluctuations, Food Additive Approval Requirements, Cost Sensitivity of Small Manufacturers, Limited Domestic Production Capacity, Long Product Qualification Cycles)

- Market Opportunities (Natural Preservatives, Clean-Label Ingredients, Sugar-Reduction Systems, Sodium-Reduction Solutions, Natural Food Colors, Customized Functional Blends, Local Flavor Development, Shelf-Life Extension Systems, Domestic Additive Blending and Import Substitution)

- Market Trends (Clean-Label Formulation, Natural Flavor and Color Adoption, Fermentation-Derived Additives, Integrated Functional Systems, Encapsulation Technologies, Reduced-Sugar Product Reformulation, Localized Filipino Flavor Profiles, Halal-Certified Ingredient Demand)

- Government Regulations (Philippine FDA Food Additive Requirements, Codex General Standard for Food Additives, Permitted Additive Use Levels, Food Category Classification, Product Registration Requirements, Importer Licensing, Ingredient Labeling, INS Number Declaration, Food Fortification Requirements, Halal Compliance)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- By Market Value (2020-2025)

- By Consumption Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Additive Type (In Value %)

Flavors and Flavoring Preparations

Flavor Enhancers

Preservatives and Antimicrobials

Sweeteners and Sugar-Reduction Systems

Food Colors and Coloring Preparations

Emulsifiers - By Application (In Value %)

Bakery and Baked Goods

Beverages and Drink Mixes

Processed Meat and Poultry

Processed Seafood

Dairy Products and Frozen Desserts - By Distribution Channel (In Value %)

Direct Sales by Global Ingredient Manufacturers

Exclusive Food Ingredient Distributors

Multi-Principal Specialty Distributors

General Chemical and Ingredient Traders - By Geographic Demand Cluster (In Value %)

National Capital Region

CALABARZON

Central Luzon

Central and Western Visayas

Northern Mindanao

- Market Share of Major Players (By Market Value, Consumption Volume, Additive Category, Food Application and Distribution Channel)

- Cross Comparison Parameters (Philippines Food Additive Portfolio Breadth, Number of Food Additive SKUs, Local Application Laboratory Capability, FDA and Codex Regulatory Support Capability, Imported versus Locally Blended Product Mix, Food-Processing Application Coverage, Warehouse and Inter-Island Distribution Reach, Clean-Label and Natural Additive Portfolio)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Kerry Ingredients Philippines

Cargill Philippines

Brenntag Ingredients Philippines

DKSH Philippines

Azelis Philippines

Caldic Philippines

dsm-firmenich Philippines

International Flavors & Fragrances Philippines

Givaudan Philippines

Symrise Philippines

BNC Ingredients Corporation

New Flavor House

SBS Philippines Corporation

TNC Chemicals Philippines

Philippine Aminosan Corporation

- Additive Consumption and Utilization Assessment

- Food Manufacturer Procurement Behavior

- Supplier Selection Criteria

- Purchasing Power and Ingredient Budget Allocation

- Product Qualification and Vendor Approval Process

- By Market Value (2026-2035)

- By Consumption Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now