Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Philippines Freight Aggregator Market reached approximately USD ~ billion based on a recent historical assessment, driven by rapid digitalization of domestic logistics and expansion of e-commerce distribution networks across the archipelago. Aggregator platforms enable consolidation of fragmented trucking capacity and optimize inter-island cargo flows, improving utilization and lowering transport costs. Government logistics modernization programs and private investment in platform-based freight matching have accelerated adoption among SMEs and large shippers seeking scalable and transparent freight procurement solutions.

Metro Manila, Cebu, and Davao serve as dominant logistics hubs in the Philippines Freight Aggregator Market due to dense economic activity, port connectivity, and concentration of distribution infrastructure. These cities host major seaports, fulfillment centers, and trucking fleets that enable high transaction volumes for digital freight platforms. Regional manufacturing and e-commerce growth corridors further strengthen demand for aggregation services linking urban consumption centers with provincial production zones, reinforcing hub-and-spoke freight orchestration across the country’s island geography.

Market Segmentation

By Service Type

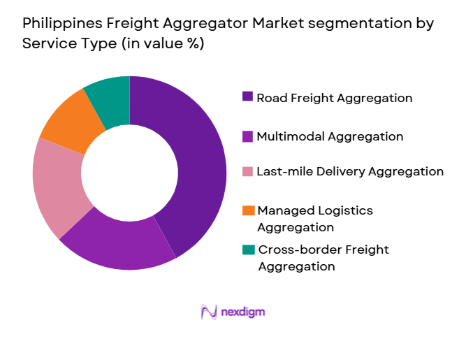

Philippines Freight Aggregator Market is segmented by service type into road freight aggregation, multimodal aggregation, last-mile delivery aggregation, cross-border freight aggregation, and managed logistics aggregation. Recently, road freight aggregation has a dominant market share due to factors such as extensive domestic trucking dependence, fragmented fleet ownership, and high intercity cargo demand between metropolitan hubs and provincial regions. The archipelagic geography necessitates frequent road-port-road cargo transfers, increasing reliance on digitally matched trucking capacity. Platform penetration among small truck operators is highest in road-based services because onboarding barriers are lower than multimodal orchestration. E-commerce fulfillment expansion has further intensified demand for domestic trucking aggregation, reinforcing its leading position within digital freight marketplaces.

By End User

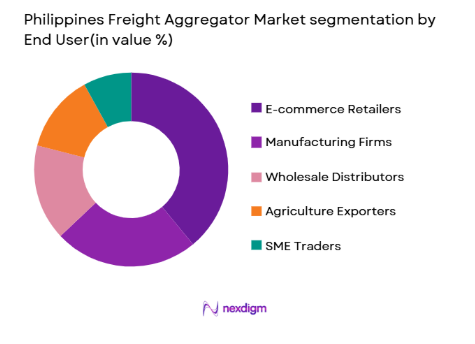

Philippines Freight Aggregator Market is segmented by end user into e-commerce retailers, manufacturing firms, agriculture exporters, wholesale distributors, and SME traders. Recently, e-commerce retailers have a dominant market share due to factors such as high shipment frequency, nationwide fulfillment requirements, and demand for scalable last-mile orchestration across islands. Online retail growth has created continuous small-lot shipments requiring flexible capacity matching and route optimization. Aggregator platforms provide real-time booking, tracking, and cost visibility essential for omnichannel delivery commitments. Retailers also drive adoption of managed aggregation services integrating warehousing and transport, consolidating logistics spend within digital freight ecosystems.

Competitive Landscape

The Philippines Freight Aggregator Market exhibits moderate consolidation with a mix of domestic digital logistics startups and global express providers expanding platform-based aggregation capabilities. Major players leverage technology integration, fleet partnerships, and fulfillment infrastructure to scale nationwide coverage, while local specialists focus on urban trucking density and last-mile optimization.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Partner Network |

| Transportify Philippines | 2016 | Manila | ~ | ~ | ~ | ~ | ~ |

| Mober Technology | 2015 | Manila | ~ | ~ | ~ | ~ | ~ |

| Ninja Van Philippines | 2014 | Taguig | ~ | ~ | ~ | ~ | ~ |

| Lalamove Philippines | 2013 | Manila | ~ | ~ | ~ | ~ | ~ |

| 2GO Group | 1949 | Pasay | ~ | ~ | ~ | ~ | ~ |

Philippines Freight Aggregator Market Analysis

Growth Drivers

Expansion of E-commerce Fulfillment and Omnichannel Distribution Networks:

The rapid expansion of online retail and omnichannel commerce ecosystems has significantly increased shipment frequency, geographic dispersion, and last-mile delivery complexity across the Philippines Freight Aggregator Market. Retailers require scalable logistics capacity capable of handling high-volume small consignments across urban and provincial destinations. Freight aggregators enable real-time matching of fragmented trucking supply with dynamic e-commerce demand, improving delivery reliability and speed. Platform-based aggregation also reduces logistics procurement friction by providing instant pricing and booking visibility. As retailers expand nationwide fulfillment footprints, aggregator platforms become critical orchestration layers connecting warehouses, ports, and delivery nodes. The growth of same-day and next-day delivery expectations further amplifies demand for flexible trucking capacity pools. Digital freight platforms integrate route optimization and tracking analytics that enhance service performance and customer experience. This structural shift toward distributed commerce logistics continues to reinforce aggregator adoption among major retailers and marketplace sellers.

Digitalization of Fragmented Trucking and Inter-Island Logistics Networks:

The Philippines Freight Aggregator Market is strongly driven by the digital transformation of a highly fragmented trucking sector characterized by small fleet ownership and low asset utilization. Aggregator platforms consolidate scattered vehicle capacity into searchable digital marketplaces, improving matching efficiency and load factors. Inter-island supply chains depend on coordinated road-port-road movements that require synchronized scheduling across carriers and terminals. Freight aggregation technology enables standardized documentation, tracking, and pricing across these multimodal transfers. Digital onboarding tools allow small operators to access national demand pools without direct contracting relationships. Improved visibility and payment assurance encourage fleet participation in platforms. As infrastructure modernization expands port and road connectivity, digitally orchestrated freight flows become increasingly viable. The ongoing shift from broker-based contracting to platform-based aggregation is structurally increasing market penetration.

Market Challenges

Infrastructure Bottlenecks and Inter-Island Connectivity Constraints:

The Philippines Freight Aggregator Market faces persistent operational limitations arising from congested ports, uneven road quality, and capacity gaps across secondary island corridors. Freight aggregators depend on reliable multimodal transfer points, yet delays at ferry terminals and urban congestion reduce scheduling predictability. Limited cold-chain and container handling infrastructure further complicate integrated logistics orchestration. These structural inefficiencies raise transit variability that digital platforms alone cannot eliminate. Aggregators must incorporate buffer times and dynamic rerouting, increasing operational complexity. Inconsistent infrastructure across provinces restricts nationwide service standardization. Fleet operators in remote regions often lack digital connectivity and equipment compatibility. Such constraints slow platform scaling outside major corridors. Addressing physical logistics bottlenecks remains critical for sustained aggregation efficiency improvements.

Low Digital Adoption Among Small Fleet Operators and SMEs:

A significant share of trucking capacity in the Philippines Freight Aggregator Market is owned by micro and small operators with limited technology familiarity and financial resources. Platform onboarding requires smartphone usage, digital documentation, and standardized service compliance that many operators initially resist. SMEs also exhibit price sensitivity and preference for traditional broker relationships based on trust. Aggregators must invest in training, incentives, and support infrastructure to integrate these participants. Payment digitization and documentation formalization can create perceived administrative burdens. Limited access to financing restricts fleet modernization needed for platform standards. Without broad operator inclusion, network density and matching efficiency are constrained. Bridging the digital readiness gap across thousands of small carriers remains a persistent structural challenge. Market growth depends on sustained ecosystem education and inclusion initiatives.

Opportunities

Development of Integrated Inter-Island Multimodal Freight Platforms:

The Philippines Freight Aggregator Market presents substantial opportunity in building unified digital platforms that seamlessly coordinate road, sea, and port logistics across islands. Integrated multimodal aggregation reduces transit fragmentation and improves shipment visibility across entire journeys. Shippers increasingly demand single-interface booking and tracking spanning trucking and maritime segments. Platforms that integrate ferry schedules, port handling, and inland transport can capture higher-value logistics orchestration roles. Such solutions also enable optimized route selection balancing cost and transit time. As domestic trade corridors expand, multimodal aggregation can significantly improve supply chain efficiency. Government logistics modernization initiatives support data integration and documentation digitization. Companies investing in inter-island orchestration technology can establish defensible network advantages. This opportunity aligns strongly with the country’s geographic logistics structure.

AI-Driven Dynamic Pricing and Capacity Optimization Solutions:

Advanced analytics and artificial intelligence offer transformative opportunity within the Philippines Freight Aggregator Market by enabling predictive demand forecasting and real-time capacity pricing. Freight platforms can analyze historical shipment patterns, seasonal flows, and route congestion to dynamically match loads and vehicles. Such optimization increases fleet utilization and reduces empty backhaul movements across islands. Shippers benefit from transparent market-based pricing reflecting real-time supply conditions. AI-driven route planning also improves delivery reliability in congested urban corridors. As platform transaction volumes grow, data advantages compound competitive differentiation. Integration of predictive ETA and risk modeling further enhances service value. These capabilities elevate aggregators from booking marketplaces to intelligent logistics orchestration providers. Adoption of advanced analytics will shape next-generation competitive positioning.

Future Outlook

The Philippines Freight Aggregator Market is expected to expand steadily as digital logistics adoption deepens across domestic trade networks and e-commerce fulfillment systems. Platform integration with multimodal transport infrastructure will enhance nationwide coverage and reliability. Technology-driven optimization, including AI-enabled routing and pricing, will improve efficiency and transparency. Continued government logistics modernization and infrastructure investment will support scalable aggregation ecosystems. Rising demand for integrated and real-time freight orchestration across islands will sustain long-term market growth.

Major Players

- TransportifyPhilippines

- Mober Technology Philippines

- Ninja Van Philippines

- Lalamove Philippines

- 2GO Group

- AP Cargo Logistics

- FAST Logistics Group

- J&T Express Philippines

- Entrego Philippines

- DHL Philippines

- GrabExpress Philippines

- Xend Business Solutions

- QuadX

- Shiptek Solutions

- Mober Fleet Solutions

Key Target Audience

- Logistics service providers

- E-commerce retailers

- Manufacturing companies

- Wholesale distributors

- Agriculture exporters

- Transportation fleet operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Primary variables including platform transaction volume, fleet participation levels, shipment frequency, and digital adoption rates across freight modes were defined. Market boundaries and service categories were standardized to ensure consistent aggregation measurement across providers.

Step 2: Market Analysis and Construction

Supply-side capacity mapping and demand-side shipment analysis were combined to construct market sizing models. Platform revenues, logistics spending flows, and service penetration across end-user sectors were integrated into bottom-up market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Industry executives, fleet operators, and logistics specialists were consulted to validate assumptions on adoption drivers, pricing structures, and operational constraints. Cross-verification ensured realistic representation of platform economics and growth dynamics.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into segmentation, competitive, and strategic analysis. Market estimates and structural trends were aligned to produce the final Philippines Freight Aggregator Market report framework.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid expansion of e-commerce and omnichannel retail logistics demand

Fragmented trucking sector seeking digital load optimization

Government logistics modernization and port connectivity initiatives

Rising SME participation in inter-island trade

Increasing demand for real-time shipment visibility and cost efficiency - Market Challenges

Limited digital adoption among small fleet operators

Infrastructure bottlenecks across islands and rural routes

Data integration complexity across multimodal carriers

Price sensitivity in fragmented shipper base

Regulatory variability across transport modes and regions - Market Opportunities

Expansion of inter-island multimodal aggregation platforms

AI-driven dynamic pricing and route optimization services

Integration with cross-border ASEAN freight networks - Trends

Shift toward mobile-based booking and fleet onboarding

Growth of managed marketplace freight models

Integration of warehousing and fulfillment aggregation

Real-time tracking and predictive ETA adoption

Platform consolidation through partnerships and acquisitions - Government Regulations & Defense Policy

National logistics and supply chain digitalization programs

Cabotage and inter-island shipping regulatory reforms

Data governance and electronic documentation compliance - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Matching Platforms

Managed Transportation Services

On-demand Truck Aggregation Systems

Multimodal Freight Aggregators

Last-mile Delivery Aggregation Platforms - By Platform Type (In Value%)

Road Freight Platforms

Sea Freight Integration Platforms

Air Cargo Aggregation Platforms

Intermodal Coordination Platforms

Urban Delivery Platforms - By Fitment Type (In Value%)

Standalone Aggregator Platforms

API-integrated Logistics Platforms

Enterprise-integrated Aggregation Suites

Marketplace-based Freight Platforms

White-label Aggregation Solutions - By EndUser Segment (In Value%)

E-commerce Retailers

Manufacturing and Industrial Firms

Agriculture and Fisheries Producers

Wholesale and Distribution Companies

SME Shippers and Traders - By Procurement Channel (In Value%)

Direct Enterprise Contracts

Platform Subscription Models

Transaction-based Spot Booking

Third-party Logistics Partnerships

Government and Institutional Tenders - By Material / Technology (in Value %)

AI-based Load Matching Algorithms

Cloud-native Logistics Platforms

Mobile-first Freight Applications

IoT-enabled Fleet Tracking Integration

Blockchain-based Shipment Documentation

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Coverage, Carrier Network Size, Pricing Model Flexibility, Multimodal Integration, Technology Stack Maturity, Geographic Reach, Value-added Services, SME Accessibility, Real-time Visibility Capability, Partnership Ecosystem)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Transportify Philippines

Mober Technology PTE Ltd Philippines

Ninja Van Philippines

Lalamove Philippines

2GO Group Inc

AP Cargo Logistics Network

QuadX Inc

DHL Philippines

J&T Express Philippines

Xend Business Solutions

GrabExpress Philippines

Shiptek Solutions Philippines

FAST Logistics Group

Entrego Philippines

Mober Fleet Solutions

- E-commerce shippers prioritizing scalable last-mile aggregation

- Manufacturers adopting multimodal cost optimization platforms

- SMEs leveraging spot freight marketplaces for flexibility

- Agriculture exporters requiring cold-chain integrated aggregation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now