Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Fuel Injection Systems market is valued at approximately USD ~ billion, based on a recent historical assessment, driven by increasing vehicle production, rising demand for fuel-efficient engines, and regulatory emphasis on emission reduction technologies. The market growth is supported by expanding automotive manufacturing activities and the transition from carburetor-based systems to advanced electronic fuel injection technologies, which enhance engine performance, reduce fuel consumption, and comply with tightening environmental standards.

Metro Manila, Cebu, and Calabarzon regions dominate the Philippines Fuel Injection Systems market due to their strong automotive assembly presence, dense transportation networks, and higher vehicle ownership levels. These regions benefit from better infrastructure, skilled labor availability, and proximity to major OEMs and suppliers, enabling efficient production and distribution. Additionally, urbanization and increasing logistics activities in these areas continue to support the sustained demand for advanced fuel injection systems across both passenger and commercial vehicles.

Market Segmentation

By Product Type

Philippines Fuel Injection Systems market is segmented by product type into gasoline port fuel injection systems, gasoline direct injection systems, diesel common rail injection systems, throttle body injection systems, and electronic unit injection systems. Recently, gasoline direct injection systems have a dominant market share due to factors such as increasing demand for fuel efficiency, growing adoption in passenger vehicles, and improved combustion performance. The ability of these systems to deliver precise fuel metering and lower emissions aligns with regulatory requirements and consumer preferences for cost-effective mobility solutions.

By Platform Type

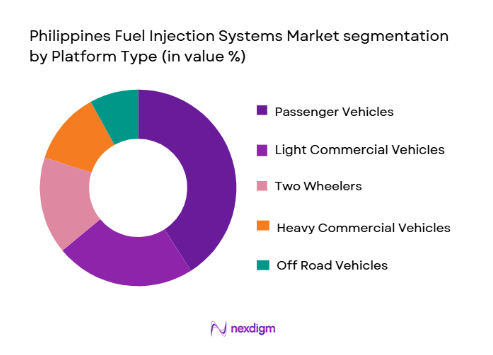

Philippines Fuel Injection Systems market is segmented by platform type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, two wheelers, and off-road vehicles. Recently, passenger vehicles have a dominant market share due to increasing urban mobility needs, rising disposable income, and growing preference for personal transportation. The expansion of compact and mid-sized vehicle segments, combined with technological advancements in fuel systems, has significantly boosted the demand for fuel injection systems in passenger vehicle platforms.

Competitive Landscape

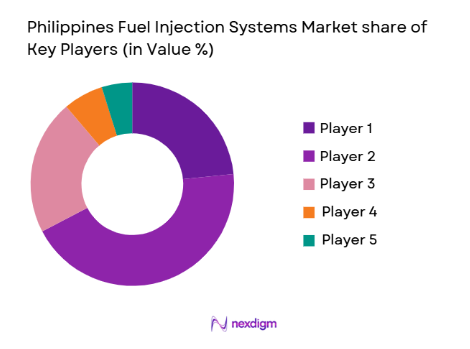

The Philippines Fuel Injection Systems market exhibits moderate consolidation with a mix of global automotive component manufacturers and regional suppliers competing for OEM contracts and aftermarket distribution. Major players leverage technological innovation, strong supply chain networks, and partnerships with automotive manufacturers to strengthen their market position, while local firms focus on cost competitiveness and service accessibility.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Partnerships |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Bosch | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Hitachi Astemo | 2021 | Japan | ~ | ~ | ~ | ~ | ~ |

| Magneti Marelli | 1919 | Italy | ~ | ~ | ~ | ~ | ~ |

Philippines Fuel Injection Systems Market Analysis

Growth Drivers

Rising Demand for Fuel Efficient Vehicles:

The increasing awareness among consumers regarding fuel efficiency and cost savings has significantly driven the demand for advanced fuel injection systems in the Philippines automotive market. Consumers are actively seeking vehicles that offer better mileage and reduced fuel consumption, particularly in urban areas where fuel prices impact daily commuting costs. Fuel injection systems, especially electronic and direct injection technologies, provide optimized fuel-air mixtures that enhance combustion efficiency and reduce wastage. This demand is further reinforced by the expansion of ride-hailing services and logistics operators that prioritize fuel-efficient fleets to maintain operational profitability. Automotive manufacturers are also focusing on integrating high-performance injection systems into entry-level and mid-range vehicles, making these technologies more accessible. Additionally, increasing traffic congestion in metropolitan regions has led to higher idling times, necessitating efficient fuel management systems to minimize consumption. The shift from carburetor systems to injection-based systems has accelerated due to their superior performance and reliability. Technological advancements in sensor integration and real-time engine monitoring have further improved fuel efficiency outcomes. This trend is expected to continue as consumers and fleet operators prioritize long-term cost benefits.

Stringent Emission Norms and Regulatory Compliance:

Government regulations aimed at reducing vehicle emissions have become a major driver for the adoption of fuel injection systems in the Philippines market. Regulatory authorities are enforcing stricter emission standards aligned with global environmental frameworks, compelling automotive manufacturers to adopt cleaner technologies. Fuel injection systems play a critical role in achieving lower emission levels by ensuring precise fuel delivery and improved combustion efficiency. These systems significantly reduce harmful emissions such as carbon monoxide and nitrogen oxides, making them essential for compliance. Automotive companies are investing in research and development to produce advanced injection systems that meet regulatory requirements without compromising engine performance. The introduction of emission testing and certification processes has further accelerated the adoption of these systems. Public awareness regarding environmental sustainability is also influencing purchasing decisions, pushing manufacturers to integrate eco-friendly technologies. Additionally, government incentives and policy support for cleaner vehicles are encouraging the use of advanced fuel injection systems. The combined effect of regulatory pressure and environmental consciousness is creating sustained demand across both passenger and commercial vehicle segments.

Market Challenges

High Cost of Advanced Fuel Injection Technologies:

The adoption of advanced fuel injection systems in the Philippines market is constrained by the relatively high cost associated with these technologies. Modern systems such as gasoline direct injection and common rail diesel injection require sophisticated components, including sensors, electronic control units, and high-pressure pumps, which increase manufacturing costs. These costs are often passed on to consumers, making vehicles equipped with advanced systems more expensive. In a price-sensitive market, this limits adoption, particularly in entry-level vehicle segments. Additionally, the cost of maintenance and repair for advanced systems is higher due to the need for specialized tools and skilled technicians. This creates reluctance among consumers and fleet operators to transition from traditional systems. Import dependency for critical components further adds to the overall cost structure, exposing manufacturers to currency fluctuations and supply chain disruptions. Local production capabilities for high-end components remain limited, restricting cost optimization. The lack of widespread service infrastructure also affects consumer confidence in adopting these systems. Overall, cost-related barriers continue to pose a significant challenge to market expansion.

Limited Technical Expertise and Service Infrastructure:

The Philippines Fuel Injection Systems market faces challenges related to limited availability of skilled technicians and specialized service infrastructure. Advanced fuel injection systems require precise calibration, diagnostics, and maintenance, which necessitate trained professionals and advanced equipment. However, the current workforce in many regions lacks the required technical expertise to handle complex systems, leading to service inefficiencies. This gap in technical capability affects both OEM service networks and independent aftermarket workshops. Vehicle owners often experience higher downtime and maintenance costs due to inadequate servicing capabilities. Additionally, the lack of standardized training programs and certification frameworks for technicians further exacerbates the issue. Rural and semi-urban areas face even greater challenges due to limited access to service centers equipped with modern diagnostic tools. This uneven distribution of service infrastructure restricts the adoption of advanced fuel injection technologies. Automotive manufacturers are attempting to address this challenge through training initiatives and partnerships with service providers. However, the pace of skill development remains slower compared to technological advancements in fuel injection systems.

Opportunities

Expansion of Hybrid and Low Emission Vehicle Segment:

The growing interest in hybrid and low emission vehicles presents a significant opportunity for the Philippines Fuel Injection Systems market. Hybrid vehicles require advanced fuel management systems to optimize engine performance alongside electric propulsion, increasing the demand for sophisticated injection technologies. As environmental concerns and fuel efficiency requirements gain importance, consumers are gradually shifting toward vehicles that offer reduced emissions and improved fuel economy. Government policies supporting cleaner transportation solutions are also encouraging the adoption of hybrid vehicles. Automotive manufacturers are introducing hybrid models across various price segments, expanding market accessibility. Fuel injection systems designed for hybrid applications provide enhanced precision and adaptability, making them critical components. Additionally, the integration of electronic control systems in hybrid vehicles aligns with advancements in injection technologies. The rising awareness of long-term cost savings associated with hybrid vehicles is further driving adoption. This trend is expected to create sustained demand for high-performance fuel injection systems tailored for hybrid applications.

Growth in Aftermarket Replacement and Upgrade Services:

The increasing vehicle parc in the Philippines is creating substantial opportunities in the aftermarket segment for fuel injection systems. As vehicles age, the need for replacement and upgrade of fuel injection components becomes more prominent. Consumers are seeking cost-effective solutions to maintain vehicle performance and fuel efficiency, driving demand for aftermarket products. The availability of a wide range of replacement components through authorized dealers and independent distributors supports market growth. Additionally, advancements in retrofit technologies enable older vehicles to upgrade to more efficient injection systems, extending their operational life. Fleet operators are particularly investing in upgrades to improve fuel efficiency and reduce operating costs. The expansion of e-commerce platforms for automotive parts is further enhancing accessibility and convenience for consumers. Local distributors are also strengthening their networks to cater to increasing demand. This growing aftermarket ecosystem is expected to contribute significantly to the overall market expansion.

Future Outlook

The Philippines Fuel Injection Systems market is expected to witness steady growth over the next five years, driven by increasing vehicle demand and technological advancements in fuel efficiency. The shift toward electronic and hybrid-compatible injection systems will accelerate adoption. Regulatory support for emission reduction will further strengthen market expansion. Additionally, rising investments in automotive infrastructure and aftermarket services will contribute to sustained demand across both passenger and commercial vehicle segments.

Major Players

- Denso Philippines Corporation

- Bosch Philippines Inc

- Continental Automotive Philippines

- Hitachi Astemo Philippines

- Magneti Marelli Philippines

- Delphi Technologies Philippines

- Keihin Philippines Corporation

- Mikuni Corporation Philippines

- Stanadyne Philippines

- Woodward Philippines

- AISIN Philippines Corporation

- Valeo Philippines Inc

- Eaton Philippines Automotive

- Schaeffler Philippines Automotive

- Hyundai Kefico Philippines

Key Target Audience

- Automotive manufacturers

- Fleet operators

- Automotive component distributors

- Aftermarket service providers

- Logistics and transportation companies

- E-commerce automotive parts platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables such as vehicle production, fuel efficiency trends, regulatory standards, and technology adoption rates were identified to establish the research framework and define market boundaries.

Step 2: Market Analysis and Construction

Data from industry databases, automotive associations, and company reports were analyzed to construct market size, segmentation, and competitive landscape using validated analytical models.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert consultations with industry professionals, OEM representatives, and aftermarket distributors to ensure accuracy and reliability of market insights.

Step 4: Research Synthesis and Final Output

All data points and insights were synthesized into a structured format, ensuring consistency, accuracy, and alignment with market dynamics to produce the final comprehensive report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising vehicle production and ownership across urban and semi urban regions

Stringent emission norms driving adoption of advanced fuel injection technologies

Growing demand for fuel efficient and low emission engines in the automotive sector

Increasing penetration of electronic control units in modern vehicles

Expansion of logistics and transportation sectors boosting commercial vehicle demand - Market Challenges

High cost of advanced fuel injection systems impacting adoption in low cost vehicles

Limited technical expertise in maintenance and calibration of modern systems

Fluctuations in raw material prices affecting system manufacturing costs

Dependency on imported components and technologies

Compatibility issues in retrofitting older vehicles with new systems - Market Opportunities

Increasing demand for hybrid and fuel efficient vehicles in the domestic market

Expansion of aftermarket services for replacement and upgrades

Government initiatives promoting cleaner automotive technologies - Trends

Shift toward gasoline direct injection systems for enhanced efficiency

Integration of smart sensors and electronic control in fuel systems

Growing adoption of common rail diesel injection in commercial fleets

Rise in aftermarket demand for high performance injection systems

Development of compact and lightweight injection components - Government Regulations & Defense Policy

Implementation of stricter vehicle emission standards aligned with global norms

Government incentives for fuel efficient and low emission vehicle technologies

Regulatory push for modernization of public transport vehicle systems - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Gasoline Port Fuel Injection Systems

Gasoline Direct Injection Systems

Diesel Common Rail Injection Systems

Throttle Body Injection Systems

Electronic Unit Injection Systems - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Two Wheelers

Off Road Vehicles - By Fitment Type (In Value%)

OEM Fitment Systems

Aftermarket Replacement Systems

Retrofitted Injection Systems

Performance Upgrade Systems

Emission Compliance Retrofit Systems - By EndUser Segment (In Value%)

Automotive Manufacturers

Fleet Operators

Individual Vehicle Owners

Public Transport Operators

Industrial Vehicle Operators - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Dealer Networks

Independent Aftermarket Distributors

Online Automotive Parts Platforms

Government Procurement Programs - By Material / Technology (in Value %)

Electronic Fuel Injection Technology

Mechanical Fuel Injection Systems

High Pressure Common Rail Technology

Multi Point Fuel Injection Technology

Single Point Injection Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Technology Type, System Efficiency, Pricing Strategy, Product Portfolio, Distribution Network, OEM Partnerships, Aftermarket Presence, Innovation Capability, Regional Presence, Compliance Standards)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Denso Philippines Corporation

Bosch Philippines Inc

Delphi Technologies Philippines

Continental Automotive Philippines

Magneti Marelli Philippines

Hitachi Automotive Systems Philippines

Keihin Philippines Corporation

Mikuni Corporation Philippines

Stanadyne Philippines Inc

Woodward Philippines

Schaeffler Philippines Automotive

Valeo Philippines Inc

AISIN Philippines Corporation

Eaton Philippines Automotive

Hyundai Kefico Philippines

- Automotive manufacturers focusing on integrating advanced injection systems for compliance and efficiency

- Fleet operators prioritizing cost effective and durable fuel systems for high utilization vehicles

- Individual vehicle owners showing growing preference for fuel efficient and low maintenance systems

- Public transport operators upgrading systems to meet emission regulations and operational efficiency

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now