Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Gearboxes Market demonstrates steady expansion with a recorded valuation of USD ~ billion based on a recent historical assessment, driven by increasing automotive production, industrial automation, and infrastructure investments across key sectors. Rising demand for fuel-efficient transmission systems, coupled with growth in construction and logistics equipment, supports consistent gearbox adoption. Additionally, industrial machinery upgrades and expanding manufacturing output further contribute to market expansion, supported by government-led infrastructure programs and private sector capital expenditure.

Metro Manila, Cebu, and Davao emerge as dominant regions due to concentrated industrial clusters, automotive assembly facilities, and logistics hubs supporting gearbox demand. The presence of manufacturing zones and port infrastructure strengthens supply chain efficiency, enabling faster distribution of gearbox systems. Industrial corridors near Luzon drive higher demand due to construction and heavy equipment usage, while Visayas and Mindanao regions benefit from agricultural mechanization and marine applications, reinforcing regional demand patterns across diverse end-use industries.

Market Segmentation

By Product Type

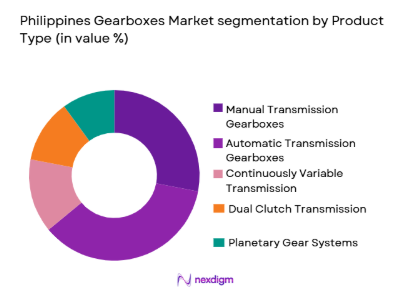

Philippines Gearboxes market is segmented by product type into manual transmission gearboxes, automatic transmission gearboxes, continuously variable transmission gearboxes, dual clutch transmission gearboxes, and planetary gear systems. Recently, automatic transmission gearboxes has a dominant market share due to increasing consumer preference for convenience, growing urban congestion, and rising adoption in passenger vehicles. Expanding middle-class income levels and preference for advanced vehicle features also contribute to the dominance of automatic systems. Furthermore, automotive manufacturers are prioritizing automatic transmission integration to align with global vehicle trends, enhancing efficiency and driving market leadership of this segment.

By End-User

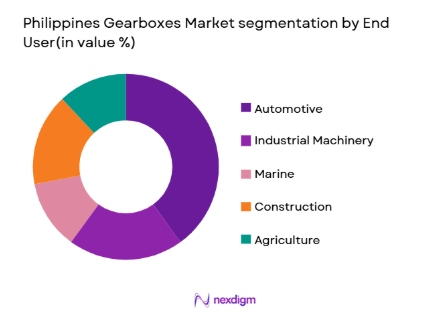

Philippines Gearboxes market is segmented by end-user into automotive, industrial machinery, marine, construction, and agriculture. Recently, automotive has a dominant market share due to sustained vehicle demand, expansion of assembly operations, and increasing urban mobility requirements. Growth in passenger cars and light commercial vehicles significantly drives gearbox installations. Additionally, rising aftermarket demand for gearbox replacement and maintenance supports the segment’s leadership. Government infrastructure development also indirectly fuels automotive logistics demand, strengthening the automotive segment’s position as the primary revenue contributor.

Competitive Landscape

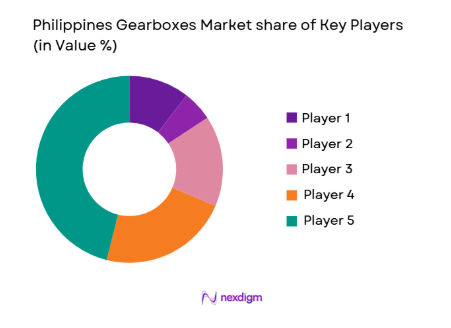

The Philippines Gearboxes Market is moderately consolidated, with a mix of global automotive component manufacturers and regional industrial equipment suppliers competing for market share. Major players leverage technological expertise, strong distribution networks, and OEM partnerships to maintain competitive positioning. International firms dominate high-end gearbox technologies, while local players focus on aftermarket services and cost-effective solutions, creating a balanced competitive environment with moderate entry barriers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Customization Capability |

| Toyota Motor Philippines | 1988 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Motors Philippines | 1963 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Aisin Philippines | 1969 | Japan | ~ | ~ | ~ | ~ | ~ |

| ZF Philippines | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Bosch Philippines | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

Philippines Gearboxes Market Analysis

Growth Drivers

Rising Automotive Production and Vehicle Ownership Expansion:

The Philippines Gearboxes Market benefits significantly from the continuous increase in automotive production and vehicle ownership across urban and semi-urban regions. The expansion of middle-income households and improving financing accessibility have enabled more consumers to purchase vehicles, driving demand for transmission systems. Increasing urbanization has also led to higher commuting needs, further accelerating vehicle sales and consequently gearbox installations. Automotive manufacturers are expanding local assembly operations, strengthening domestic supply chains and boosting gearbox demand. Additionally, the growing preference for automatic and hybrid vehicles has increased the complexity and value of gearbox systems, enhancing revenue generation. Fleet expansion in logistics and ride-hailing services has also contributed to sustained demand for durable and efficient gearbox systems. Furthermore, the automotive aftermarket sector is expanding as vehicles age, creating consistent demand for replacement gearboxes. Government initiatives supporting transportation infrastructure indirectly stimulate vehicle usage and maintenance cycles. Overall, these factors collectively reinforce strong growth momentum in gearbox demand.

Industrial Automation and Infrastructure Development Growth:

The Philippines Gearboxes Market is further propelled by rapid industrialization and increasing adoption of automation technologies across manufacturing and processing sectors. Industrial facilities are upgrading machinery to improve productivity and operational efficiency, driving demand for advanced gearbox systems. Infrastructure projects such as highways, ports, and urban development programs require heavy machinery, which depends heavily on robust gearbox solutions. Construction equipment usage has increased significantly, boosting demand for high-performance gear systems capable of handling heavy loads. Additionally, expansion in sectors such as mining, energy, and food processing has led to higher adoption of industrial gearboxes. Automation in factories requires precision gear systems, further elevating demand for technologically advanced gearboxes. The government’s emphasis on industrial growth and economic diversification supports increased machinery imports and installations. Furthermore, maintenance and retrofitting of older industrial equipment create additional demand in the aftermarket segment. These combined factors contribute to sustained industrial gearbox market growth.

Market Challenges

Dependence on Imported Components and Supply Chain Vulnerabilities:

The Philippines Gearboxes Market faces a significant challenge due to its reliance on imported gearbox components and technologies from international suppliers. Limited domestic manufacturing capabilities restrict local production, increasing dependence on global supply chains. This reliance exposes the market to fluctuations in international trade conditions, shipping delays, and currency volatility, which can impact pricing and availability. Disruptions in global logistics networks can lead to extended lead times, affecting industrial and automotive production schedules. Additionally, import tariffs and regulatory requirements add cost burdens for distributors and manufacturers. The lack of localized component manufacturing limits the ability to rapidly respond to demand fluctuations. Smaller businesses often struggle to manage inventory efficiently due to unpredictable supply timelines. Furthermore, geopolitical uncertainties can further complicate import dependencies. Addressing this challenge requires investment in domestic production capabilities and supply chain diversification.

High Maintenance Costs and Technical Complexity of Advanced Gear Systems:

The increasing adoption of technologically advanced gearbox systems introduces challenges related to maintenance complexity and operational costs. Modern gearboxes, particularly those integrated with sensors and automation technologies, require specialized skills for installation and servicing. Limited availability of skilled technicians in certain regions creates service bottlenecks and increases downtime risks. Maintenance costs for advanced transmission systems are significantly higher compared to conventional gearboxes, impacting total cost of ownership for end users. Additionally, the need for periodic calibration and monitoring adds to operational expenses. Industrial users often face challenges in maintaining optimal performance due to insufficient technical expertise. Spare parts for high-end systems are also expensive and sometimes difficult to source locally. This complexity discourages smaller enterprises from adopting advanced gearbox technologies. Overcoming this challenge requires investment in workforce training and service infrastructure development.

Opportunities

Expansion of Electric and Hybrid Vehicle Transmission Systems:

The Philippines Gearboxes Market presents strong opportunities through the growing adoption of electric and hybrid vehicles, which require specialized transmission systems. As environmental regulations become more stringent and fuel efficiency gains importance, automakers are introducing electric drivetrains that utilize innovative gearbox designs. This shift creates demand for lightweight, high-efficiency gear systems tailored for electric mobility. Government incentives promoting clean energy transportation further support adoption rates. Additionally, global automotive manufacturers are expanding their electric vehicle portfolios in emerging markets, including the Philippines. This trend opens opportunities for suppliers to introduce advanced gearbox technologies optimized for electric powertrains. The transition also encourages research and development investments in compact and efficient gear mechanisms. Local assembly and manufacturing of electric vehicle components can further strengthen domestic market capabilities. These developments collectively create a favorable environment for gearbox market expansion.

Growth in Local Manufacturing and Aftermarket Service Ecosystem:

The Philippines Gearboxes Market has significant potential in developing a localized manufacturing base and strengthening aftermarket services. Increasing focus on domestic industrialization provides opportunities for establishing gearbox assembly units within the country. Local production can reduce dependency on imports, improve supply chain resilience, and lower overall costs. Additionally, expanding the aftermarket service network enhances accessibility to maintenance and replacement components, supporting long-term demand. Rising vehicle ownership ensures consistent aftermarket activity, creating stable revenue streams for service providers. Industrial sectors also require regular maintenance and component replacement, further boosting aftermarket opportunities. Government support for small and medium enterprises encourages local participation in component manufacturing and servicing. Furthermore, partnerships between global manufacturers and local firms can facilitate technology transfer and skill development. These factors collectively position local manufacturing and services as a key growth opportunity.

Future Outlook

The Philippines Gearboxes Market is expected to experience steady growth driven by increasing automotive demand, industrial expansion, and infrastructure development. Technological advancements in transmission efficiency and smart gearbox systems will play a significant role in shaping market evolution. Regulatory support for energy efficiency and industrial modernization is likely to encourage adoption of advanced systems. Additionally, rising demand for electric mobility and localized manufacturing will contribute to sustained long-term market expansion.

Major Players

- Toyota Motor Philippines Corporation

- Mitsubishi Motors Philippines Corporation

- Isuzu Philippines Corporation

- Honda Cars Philippines Inc

- Nissan Philippines Inc

- Suzuki Philippines Incorporated

- Aisin Philippines Corporation

- ZF Philippines Inc

- Bosch Philippines

- Dana Philippines Inc

- BorgWarner Philippines

- GKN Driveline Philippines

- Hyundai Motor Philippines Inc

- Caterpillar Philippines Inc

- Komatsu Philippines Corporation

Key Target Audience

- Automotive manufacturers

- Industrial equipment manufacturers

- Marine operators

- Construction companies

- Agricultural equipment companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Logistics and fleet operators

Research Methodology

Step 1: Identification of Key Variables

The study identifies critical variables including production volume, demand drivers, technological adoption, and supply chain factors. These variables are validated using industry databases, trade statistics, and sector-specific indicators to ensure accuracy.

Step 2: Market Analysis and Construction

Market sizing is developed through a combination of bottom-up and top-down approaches, integrating industry data, company revenues, and sector demand trends to construct a reliable market framework.

Step 3: Hypothesis Validation and Expert Consultation

Initial findings are validated through consultations with industry experts, manufacturers, and distributors. Feedback ensures alignment with real-world market conditions and enhances analytical precision.

Step 4: Research Synthesis and Final Output

All validated data is synthesized into structured insights, ensuring consistency, accuracy, and relevance. Final outputs are reviewed to meet quality standards and provide actionable intelligence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising automotive production and vehicle parc expansion

Growth in infrastructure and construction equipment demand

Increasing industrial automation across manufacturing sectors

Expansion of marine and logistics industries

Technological advancements in fuel efficient transmission systems - Market Challenges

High dependency on imported gearbox components

Fluctuating raw material prices affecting production costs

Limited domestic manufacturing capabilities

Complex maintenance requirements for advanced gearbox systems

Supply chain disruptions impacting component availability - Market Opportunities

Expansion of electric and hybrid vehicle transmission solutions

Growth in localized manufacturing and assembly facilities

Rising demand for energy efficient industrial gearbox systems - Trends

Adoption of lightweight gearbox materials for fuel efficiency

Integration of smart sensors for predictive maintenance

Shift towards automated and semi automatic transmissions

Increasing customization in industrial gearbox applications

Growth in electric drivetrain compatible gearbox technologies - Government Regulations & Defense Policy

Implementation of automotive safety and emission standards

Policies promoting local manufacturing and industrialization

Regulations governing marine and heavy equipment performance - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Manual Transmission Gearboxes

Automatic Transmission Gearboxes

Continuously Variable Transmission Gearboxes

Dual Clutch Transmission Gearboxes

Planetary Gear Systems - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Industrial Machinery

Marine Applications

Agricultural Equipment - By Fitment Type (In Value%)

OEM Fitments

Aftermarket Replacement

Retrofit Installations

Heavy Duty Custom Fitments

Modular Assembly Fitments - By EndUser Segment (In Value%)

Automotive Manufacturers

Industrial Equipment Producers

Marine Operators

Construction Sector Companies

Agricultural Enterprises - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Distributors

Independent Aftermarket Suppliers

Online Industrial Marketplaces

Government and Fleet Tenders - By Material / Technology (in Value %)

Steel Alloy Gear Systems

Aluminum Lightweight Gearboxes

Composite Material Gear Units

Precision CNC Machined Systems

Smart Sensor Integrated Gearboxes

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Diversity, Transmission Efficiency, Pricing Strategy, Distribution Network Strength, Technological Innovation, Aftermarket Support, Manufacturing Capability, Regional Presence, Customization Capability, Supply Chain Integration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Toyota Motor Philippines Corporation

Mitsubishi Motors Philippines Corporation

Isuzu Philippines Corporation

Honda Cars Philippines Inc

Nissan Philippines Inc

Suzuki Philippines Incorporated

Aisin Philippines Corporation

ZF Philippines Inc

Bosch Philippines

Dana Philippines Inc

BorgWarner Philippines

GKN Driveline Philippines

Hyundai Motor Philippines Inc

Caterpillar Philippines Inc

Komatsu Philippines Corporation

- Automotive manufacturers increasingly adopting advanced transmission systems

- Industrial sector focusing on durable and high efficiency gear solutions

- Marine operators requiring corrosion resistant gearbox technologies

- Construction and agriculture sectors demanding heavy duty gearbox systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now