Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Philippines home finance market reached approximately USD ~ billion in outstanding housing loans, driven by rapid urban housing demand, expanding mortgage lending by universal and thrift banks, and government-backed housing finance programs reported by the Bangko Sentral ng Pilipinas and the Home Development Mutual Fund. Rising condominium development, overseas remittance-supported home purchases, and longer loan tenors have strengthened mortgage origination volumes across both primary residential buyers and property investors nationwide.

Metro Manila dominates the Philippines home finance market due to concentration of real estate development, higher property values, and strong banking presence supporting mortgage origination and refinancing activity. Cebu and Davao also show substantial home finance demand as regional economic centers with expanding residential projects and middle-income homeownership growth. Overseas Filipino household investment in housing across these cities further reinforces mortgage uptake through bank and government housing finance channels.

Market Segmentation

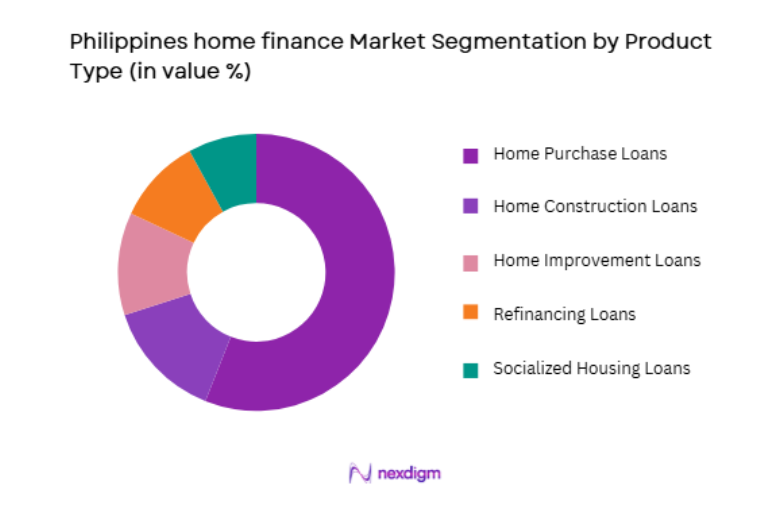

By Product Type

Philippines home finance market is segmented by product type into home purchase loans, home construction loans, home improvement loans, refinancing loans, and socialized housing loans. Recently, home purchase loans have a dominant market share due to factors such as strong residential demand, developer-bank tie-ups, and primary homeownership financing needs among middle-income households. Banks prioritize purchase mortgages through pre-approved project financing partnerships with developers, enabling faster loan approval and higher origination volumes.

By Lender Type

Philippines home finance market is segmented by lender type into universal banks, thrift banks, government housing institutions, rural banks, and non-bank financial institutions. Recently, universal banks have a dominant market share due to factors such as large balance sheets, nationwide branch networks, and integrated mortgage products aligned with developer projects and salaried borrowers. Universal banks leverage payroll-linked lending, competitive interest rates, and longer tenors to attract middle- and upper-income borrowers, while digital mortgage processing improves customer acquisition. Their strong capital base and property valuation capabilities reinforce leadership in housing finance origination and portfolio growth nationwide.

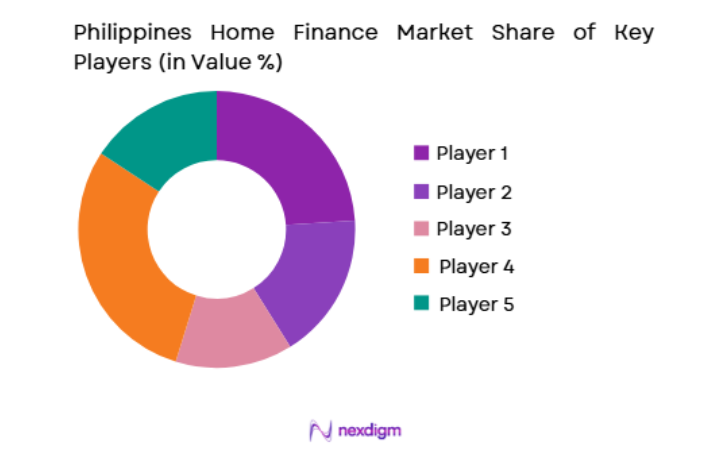

Competitive Landscape

The Philippines home finance market is led by universal banks and government housing institutions providing mortgage lending through developer partnerships and salaried borrower channels. Market concentration reflects the capital intensity and long-tenor nature of housing loans, favoring large banks with strong funding bases. Government programs expand affordability segments, while thrift banks and specialized lenders compete in niche housing finance and regional markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio |

| BDO Unibank | 1968 | Makati | ~ | ~ | ~ | ~ | ~ |

| BPI | 1851 | Makati | ~ | ~ | ~ | ~ | ~ |

| Metrobank | 1962 | Makati | ~ | ~ | ~ | ~ | ~ |

| Pag-IBIG Fund | 1978 | Makati | ~ | ~ | ~ | ~ | ~ |

| Security Bank | 1951 | Makati | ~ | ~ | ~ | ~ | ~ |

Philippines Home Finance Market Analysis

Growth Drivers

Urbanization and residential real estate expansion driving mortgage demand

The Philippines continues to experience sustained urban population growth and internal migration toward metropolitan and regional economic centers, creating structural demand for residential housing that directly translates into rising mortgage origination volumes across banks and housing finance institutions. Rapid condominium and subdivision development by large real estate developers in urban corridors increases the supply of mortgage-eligible housing units aligned with bank financing programs and pre-approved loan structures. Middle-income household formation and income growth enable more families to transition from renting to ownership, stimulating purchase loan uptake supported by salaried employment-based credit assessment models used by lenders. Overseas Filipino remittances provide additional equity funding for home purchases, improving borrower affordability and down payment capacity for financed residential property acquisition.

Expansion of bank-led housing finance accessibility and longer-tenor lending

Philippine banks have progressively expanded housing finance accessibility through product innovation, extended loan tenors, and digital mortgage processing systems that reduce barriers to homeownership financing for middle- and upper-income borrowers across urban and regional markets. Longer loan maturities improve affordability by lowering monthly amortization requirements, enabling households to qualify for larger mortgage amounts aligned with rising property prices. Banks increasingly offer flexible repayment structures, fixed-rate periods, and refinancing options that enhance borrower confidence and encourage mortgage adoption. Integration of payroll accounts and credit scoring data allows lenders to streamline underwriting and reduce default risk, supporting portfolio expansion. Digital loan application platforms and automated documentation workflows shorten approval timelines and improve customer experience in mortgage origination. Competitive interest rate pricing driven by bank competition further stimulates borrower demand for housing finance.

Market Challenges

Housing affordability constraints and property price escalation

The Philippines home finance market faces persistent affordability challenges arising from rapid residential property price increases in major urban centers that outpace household income growth, limiting the proportion of families capable of qualifying for mortgage financing despite expanding lender accessibility. High land costs and construction expenses elevate property values, requiring larger loan amounts and down payments that exclude lower-income households from formal housing finance. Mortgage affordability ratios become strained as borrowers allocate higher income shares toward housing repayments, increasing credit risk sensitivity for lenders. Affordable housing supply remains insufficient relative to urban population growth, intensifying price pressure and reducing accessible mortgage inventory. Borrowers with informal or variable income face additional qualification barriers due to stringent documentation requirements imposed by lenders. Interest rate sensitivity also affects affordability, as mortgage payments increase during tightening cycles, discouraging new borrowing.

Land titling, collateral documentation, and legal complexity in housing finance

The Philippines housing finance system encounters structural inefficiencies related to land titling, property registration, and collateral verification processes that complicate mortgage origination and increase transaction timelines and costs for both lenders and borrowers. Incomplete or disputed land titles and fragmented property records create legal uncertainty in collateral valuation and enforceability, discouraging lenders from financing certain properties or geographic areas. Lengthy documentation requirements and manual verification procedures delay loan approval and disbursement, reducing efficiency compared with other retail lending segments. Borrowers may face additional administrative costs and delays in securing property titles and permits necessary for mortgage qualification. Informal settlements and unregistered land ownership further limit eligibility for formal housing finance among lower-income populations. Lenders must invest significant resources in legal due diligence and property appraisal to mitigate collateral risk, increasing operational costs.

Opportunities

Expansion of affordable housing finance and public–private partnership programs

The Philippines presents significant opportunity for expansion of affordable housing finance through strengthened collaboration between government housing institutions, banks, and real estate developers to increase supply and financing accessibility for low- and middle-income households underserved by traditional mortgage markets. Public–private partnership housing projects can integrate subsidized financing structures, longer tenors, and lower down payment requirements to improve borrower qualification and affordability. Government guarantees and risk-sharing mechanisms encourage private lenders to extend mortgages to emerging borrower segments. Digital mortgage platforms and standardized documentation can reduce origination costs for affordable housing loans, improving scalability.

Digital mortgage ecosystems and property transaction integration

The digitization of property transactions and mortgage processes in the Philippines creates substantial opportunity to modernize housing finance through integrated digital ecosystems connecting lenders, developers, brokers, registries, and borrowers within streamlined platforms that accelerate approval timelines and reduce transaction friction. Online property listing portals and digital broker networks can integrate pre-approved mortgage offers, enabling buyers to secure financing simultaneously with property selection. Automated credit scoring, document upload, and e-signature systems reduce manual processing and improve efficiency in loan origination. Integration with digital land registry systems and property databases enhances collateral verification and title validation accuracy. Borrowers benefit from transparent loan comparisons, faster approvals, and simplified documentation, improving mortgage accessibility and customer experience. Lenders gain operational efficiency and expanded reach across geographically dispersed markets.

Future Outlook

The Philippines home finance market is expected to expand steadily as urban housing demand, mortgage accessibility, and affordable housing initiatives strengthen loan origination across metropolitan and regional markets. Banks and government housing institutions will continue expanding digital mortgage platforms and developer partnerships to reach broader borrower segments. Affordable housing finance and refinancing demand will deepen portfolio growth. Regulatory and land registry modernization efforts will further support housing finance scalability nationwide.

Major Players

- BDO Unibank

- Bank of the Philippine Islands

- Metrobank

- Pag-IBIG Fund

- Security Bank

- Philippine National Bank

- EastWest Bank

- China Banking Corporation

- RCBC

- UnionBank of the Philippines

- Land Bank of the Philippines

- Development Bank of the Philippines

- PS Bank

- Maybank Philippines

- Sterling Bank of Asia

Key Target Audience

- Mortgage lenders

- Real estate developers

- Housing finance institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- Property brokers

- Construction companies

- Housing cooperatives

Research Methodology

Step 1: Identification of Key Variables

Key variables including housing loan volumes, borrower segments, property types, lender categories, and regulatory housing programs were identified through banking and housing finance statistics. Market scope focused on outstanding residential mortgage portfolios and housing loan origination. Demographic and real estate indicators were mapped to mortgage demand patterns.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using central bank housing loan data, lender disclosures, and housing institution reports. Product and lender distribution patterns were triangulated across sources. Competitive structure and financing channels were analyzed to define market composition.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with mortgage lenders, housing developers, and property finance specialists regarding borrower behavior, affordability trends, and financing structures. Assumptions on segment dominance and lender roles were refined. Market shares were cross-checked with industry insights.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were synthesized into a comprehensive analysis of market size, segmentation, drivers, challenges, and opportunities. Strategic outlook and growth implications were derived from housing demand and financing trends. Final outputs were reviewed for consistency and analytical accuracy.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Urban housing demand driven by population growth and migration to cities

Government affordable housing and subsidy programs expanding access

Bank competition increasing availability of mortgage products - Market Challenges

High property prices relative to household incomes limiting affordability

Lengthy land titling and property registration processes

Credit risk concerns for informal income borrowers - Market Opportunities

Digital mortgage origination and approval platforms

Green and climate-resilient housing finance products

Expansion of micro-housing finance in underserved regions - Trends

Rising developer–bank tie-ups for project-based mortgage sales

Growth of OFW-targeted remote home loan origination - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential Mortgage Loans

Housing Microfinance

Home Equity Loans

Construction and Self-build Financing

Refinancing and Balance Transfer Loans - By Platform Type (In Value%)

Bank Branch-based Lending

Digital Mortgage Platforms

Developer-linked Financing Channels

Cooperative and Rural Bank Platforms

Government Housing Finance Platforms - By Fitment Type (In Value%)

Fixed Rate Home Loans

Variable Rate Home Loans

Subsidized Housing Loans

Hybrid Rate Home Loans - By End User Segment (In Value%)

Salaried Urban Households

Informal and Self-employed Borrowers

Low-income Social Housing Beneficiaries

- Market Share Analysis

- Cross Comparison Parameters (Loan Type, Interest Rate Structure, Distribution Channel, Borrower Segment Focus, Approval Turnaround Time, Loan Tenure Flexibility, Down Payment Requirement, Digital Application Capability, Government Subsidy Integration, Property Type Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BDO Unibank Home Loans

Bank of the Philippine Islands Housing Loans

Metrobank Home Loan

Security Bank Home Loan

RCBC Home Loan

UnionBank Home Loan

Philippine National Bank Housing Loan

China Banking Corporation HomePlus Loan

EastWest Bank Home Loan

Land Bank of the Philippines Housing Loan

Development Bank of the Philippines Housing Loan

Pag-IBIG Fund Housing Loan

Maybank Philippines Home Loan

PSBank Home Loan

Sterling Bank of Asia Home Loan

- Urban middle-class households upgrading from rental to ownership housing

- Informal workers accessing micro-housing loans through rural institutions

- Low-income families relying on subsidized social housing credit

- Overseas workers financing homes for families in provincial regions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now