Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines manual transmissions market is valued at approximately USD ~ billion based on a recent historical assessment, driven by sustained demand for cost-efficient vehicle systems and the continued reliance on internal combustion engine vehicles across urban and rural mobility segments. The affordability of manual transmission vehicles, combined with lower maintenance requirements and fuel efficiency advantages, supports strong demand among price-sensitive consumers and commercial fleet operators, particularly in logistics, agriculture, and public transportation sectors.

Metro Manila, Cebu, and Davao emerge as dominant urban centers, supported by dense vehicle ownership and strong automotive aftermarket ecosystems. Regional provinces also contribute significantly due to reliance on durable, low-cost vehicles suited for rugged terrain and long-distance usage. The Philippines benefits from strong import networks and assembly operations linked to Japan and Thailand, ensuring steady supply of manual transmission systems and components, while local workshops and service centers sustain aftermarket demand.

Market Segmentation

By Product Type

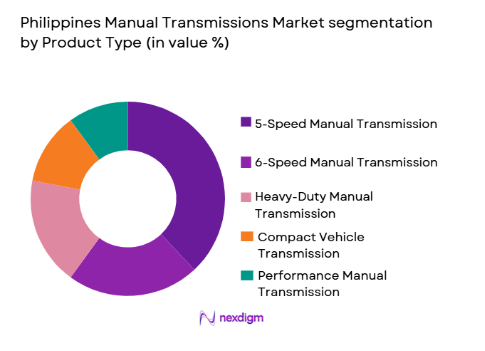

Philippines Manual Transmissions market is segmented by product type into 5-speed manual transmission, 6-speed manual transmission, heavy-duty manual transmission, compact vehicle transmission, and performance manual transmission. Recently, 5-speed manual transmission has a dominant market share due to its widespread adoption in entry-level passenger vehicles and light commercial fleets. Its lower cost, ease of maintenance, and compatibility with small displacement engines make it highly preferred across urban and rural users. Additionally, the Philippines automotive landscape continues to favor affordable mobility solutions, reinforcing demand for simpler transmission configurations. Availability of spare parts and technician familiarity further strengthens its position, particularly in provincial areas where servicing infrastructure remains limited compared to advanced transmission technologies.

By Platform Type

Philippines Manual Transmissions market is segmented by platform type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, agricultural vehicles, and off-road vehicles. Recently, passenger vehicles have a dominant market share due to their high volume of ownership and continued consumer preference for affordable transportation solutions. The Philippines market is heavily driven by compact sedans and hatchbacks equipped with manual transmissions, especially among middle-income households. Additionally, ride-hailing drivers and private users prioritize fuel efficiency and lower acquisition costs, which manual systems support effectively. Strong dealership networks and financing options for entry-level vehicles further accelerate demand, making passenger vehicles the leading platform segment within the market landscape.

Competitive Landscape

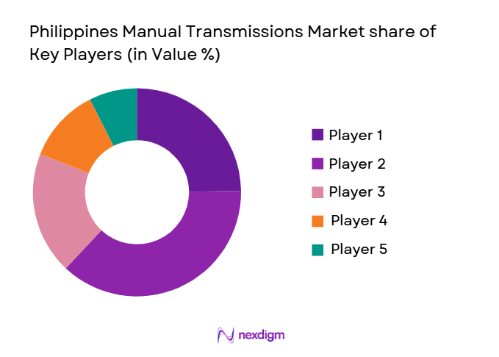

The Philippines manual transmissions market exhibits moderate consolidation, with a mix of global transmission manufacturers and regional suppliers dominating supply chains. Major players leverage strong OEM partnerships, technological capabilities, and established distribution networks to maintain market positioning. Japanese and European manufacturers play a significant role due to long-standing automotive ties with the Philippines, while aftermarket suppliers remain critical in servicing aging vehicle fleets. Competitive dynamics are shaped by cost efficiency, durability, and supply chain reliability.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Production Capacity |

| Aisin Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Eaton Corporation | 1911 | Ireland | ~ | ~ | ~ | ~ | ~ |

| BorgWarner Inc | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

| Hyundai Transys | 1994 | South Korea | ~ | ~ | ~ | ~ | ~ |

Philippines Manual Transmissions Market Analysis

Growth Drivers

Rising Demand for Cost-Efficient Mobility Solutions:

The Philippines manual transmissions market is significantly driven by the increasing demand for affordable transportation options among middle- and lower-income populations. Consumers prioritize vehicles that offer lower upfront costs, reduced maintenance expenses, and better fuel economy, all of which are characteristics of manual transmission systems. The expanding urban population and growing need for daily commuting further amplify this demand. Manual vehicles remain more accessible through financing schemes, encouraging ownership among first-time buyers. Fleet operators in logistics and ride-hailing services also favor manual systems to optimize operating costs. Additionally, the prevalence of congested traffic conditions makes fuel efficiency a critical factor in vehicle selection. The durability of manual transmissions ensures longer vehicle life, reducing replacement frequency. These economic considerations collectively reinforce the sustained adoption of manual transmission vehicles. The market continues to benefit from a strong preference for practicality over convenience-driven automatic systems.

Expansion of Commercial Vehicle and Logistics Sector:

rapid growth of the logistics and transportation sector in the Philippines is a major driver for manual transmission adoption, particularly in light and heavy commercial vehicles. The rise of e-commerce and supply chain networks has increased demand for delivery vehicles that are cost-efficient and reliable. Manual transmissions are preferred in commercial applications due to their robustness and lower repair costs under heavy usage conditions. Fleet operators prioritize total cost of ownership, making manual systems an economically viable choice. Rural logistics operations further support this trend, as manual vehicles perform better in uneven terrains. Additionally, public transportation systems such as jeepneys and utility vehicles rely heavily on manual transmissions. Continuous infrastructure development and road connectivity projects also stimulate demand for transport vehicles. These factors collectively strengthen the role of manual transmissions in the commercial vehicle ecosystem. The segment continues to expand as logistics networks penetrate deeper into regional areas.

Market Challenges

Shift Toward Automatic and Electrified Vehicle Technologies:

The Philippines manual transmissions market faces increasing pressure from the growing adoption of automatic transmissions and electric vehicles, which offer enhanced driving convenience and reduced operational complexity. Consumers in urban areas are gradually shifting toward automatic vehicles due to traffic congestion and ease of driving. Automakers are also prioritizing the development of automatic and hybrid systems, limiting innovation in manual transmission technologies. Government initiatives promoting cleaner mobility solutions indirectly support electric vehicle adoption, reducing reliance on traditional manual systems. Additionally, younger consumers demonstrate a preference for modern driving experiences, further impacting manual transmission demand. The availability of affordable automatic variants has narrowed the cost gap between the two systems. This transition is particularly evident in metropolitan areas where convenience outweighs cost considerations. As technology evolves, manual transmissions risk becoming less relevant in future vehicle platforms. The industry must adapt to changing consumer preferences to remain competitive.

Limited Technological Advancements and Investment Focus:

manual transmissions segment faces challenges due to limited technological advancements compared to automatic and hybrid systems. Automotive manufacturers are increasingly investing in advanced transmission technologies such as dual-clutch systems and continuously variable transmissions. This shift reduces research and development focus on manual systems, slowing innovation. As a result, manual transmissions may struggle to meet evolving efficiency and performance standards. The lack of technological differentiation makes it difficult to attract premium segment buyers. Additionally, global automotive trends are shifting toward automation and electrification, leaving manual systems with reduced strategic importance. Supply chain investments are also directed toward newer technologies, impacting availability and development of manual components. The market may face stagnation if innovation gaps continue to widen. Manufacturers must balance cost advantages with technological improvements to sustain demand. Without adequate investment, manual transmissions risk declining relevance in the long term.

Opportunities

Growth in Aftermarket Replacement and Servicing Demand:

The Philippines manual transmissions market presents strong opportunities in the aftermarket segment, driven by the aging vehicle fleet and high usage of manual vehicles. As vehicles age, demand for replacement parts and servicing increases significantly. Manual transmissions, due to their mechanical complexity, require periodic maintenance and component replacement. Local workshops and independent service providers play a crucial role in supporting this demand. The availability of affordable spare parts enhances aftermarket growth potential. Additionally, consumers often prefer repairing existing vehicles rather than purchasing new ones, particularly in cost-sensitive segments. The expansion of automotive service networks across regional areas further supports this opportunity. Manufacturers and suppliers can leverage this trend by strengthening distribution channels and offering cost-effective solutions. The aftermarket segment ensures sustained revenue streams even as new vehicle sales fluctuate. This opportunity remains critical for long-term market stability.

Expansion of Rural Mobility and Utility Vehicle Demand:

Rural and semi-urban regions in the Philippines offer significant growth opportunities for manual transmission vehicles due to their reliance on durable and cost-effective transportation solutions. Manual systems are better suited for rugged terrains and long-distance travel, making them ideal for agricultural and utility applications. The growing need for rural connectivity and transport services supports demand for manual vehicles. Government infrastructure initiatives aimed at improving road networks further enhance accessibility. Additionally, agricultural activities require reliable vehicles capable of handling heavy loads, reinforcing the importance of manual transmissions. Consumers in these regions prioritize functionality and affordability over advanced features. The expansion of small businesses and local logistics operations also contributes to demand growth. Manufacturers can capitalize on this opportunity by targeting rural markets with tailored products. The segment remains resilient despite urban shifts toward automation.

Future Outlook

The Philippines manual transmissions market is expected to witness gradual stabilization over the next five years, supported by sustained demand from cost-sensitive consumers and commercial operators. While urban areas may shift toward automatic systems, rural and logistics-driven demand will remain strong. Technological improvements focusing on durability and efficiency are anticipated. Government infrastructure development and continued reliance on internal combustion vehicles will further sustain demand. However, long-term growth will depend on balancing affordability with evolving mobility trends.

Major Players

- Aisin Corporation

- ZF Friedrichshafen AG

- Eaton Corporation

- BorgWarner Inc

- Hyundai Transys

- Schaeffler Group

- Magna International

- GKN Automotive

- Dana Incorporated

- Jatco Ltd

- Allison Transmission

- Ricardo plc

- Xtrac Limited

- Hewland Engineering

- AVL List GmbH

Key Target Audience

- Automotive OEM manufacturers

- Automotivecomponent suppliers

- Logistics and fleet operators

- Automotive aftermarket distributors

- Transportation service providers

- Agricultural equipment operators

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables such as vehicle sales, transmission adoption rates, and aftermarket demand are identified. These variables form the foundation for assessing market dynamics and segmentation structures across the Philippines automotive ecosystem.

Step 2: Market Analysis and Construction

Comprehensive analysis is conducted using primary and secondary data sources. Market models are developed to estimate size, segmentation, and competitive positioning based on industry benchmarks and regional trends.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through consultations with industry experts, manufacturers, and distributors. This ensures accuracy and alignment with real-world market conditions and operational insights.

Step 4: Research Synthesis and Final Output

All validated data is synthesized into a structured report. Insights are refined to present actionable conclusions, ensuring clarity, accuracy, and relevance for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing demand for cost-efficient vehicle systems in emerging economies

High preference for fuel-efficient transmission systems in urban mobility

Growth in commercial vehicle fleet expansion across logistics sector

Lower maintenance cost compared to automatic transmission systems

Rising demand for durable transmissions in rural and semi-urban regions - Market Challenges

Shift toward automatic and electric vehicle technologies reducing demand

Limited innovation investment in manual transmission technologies

Rising consumer preference for convenience-driven driving systems

Supply chain disruptions impacting transmission component availability

Declining adoption in premium and urban passenger vehicle segments - Market Opportunities

Expansion in rural mobility solutions requiring low-cost transmission systems

Growth in aftermarket servicing and replacement demand

Opportunities in commercial vehicle and fleet retrofitting segments - Trends

Gradual integration of lightweight materials in transmission manufacturing

Increased focus on fuel efficiency optimization in manual systems

Growth in hybrid manual transmission configurations

Shift toward precision engineering and durability improvements

Rising aftermarket demand for performance-enhanced manual systems - Government Regulations & Defense Policy

Implementation of vehicle emission and fuel efficiency standards

Import regulations impacting transmission component sourcing

Safety compliance requirements for commercial vehicle systems - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

5-Speed Manual Transmission

6-Speed Manual Transmission

Heavy Duty Manual Transmission

Compact Vehicle Manual Transmission

Performance Oriented Manual Transmission - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Agricultural Vehicles

Off-Road and Construction Vehicles - By Fitment Type (In Value%)

OEM Installed Systems

Aftermarket Replacement Systems

Refurbished Transmission Systems

Performance Upgrade Fitments

Fleet Retrofit Installations - By EndUser Segment (In Value%)

Individual Vehicle Owners

Commercial Fleet Operators

Logistics and Transportation Firms

Agriculture and Construction Operators

Automotive Repair Workshops - By Procurement Channel (In Value%)

Direct OEM Procurement

Authorized Dealer Networks

Independent Aftermarket Suppliers

Online Automotive Platforms

Fleet Contract Procurement - By Material / Technology (in Value %)

Cast Iron Transmission Systems

Aluminum Alloy Transmission Systems

Hybrid Lightweight Materials

Synchromesh Technology Systems

Advanced Gear Precision Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Diversity, Transmission Efficiency, Cost Competitiveness, Aftermarket Support Strength, OEM Partnerships, Manufacturing Capacity, Technology Integration Level, Regional Distribution Network, Durability Performance, Supply Chain Integration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Aisin Corporation

ZF Friedrichshafen AG

Getrag Transmission Systems

Eaton Corporation

BorgWarner Inc

Hyundai Transys

Schaeffler Group

GKN Automotive

Magna International Inc

Jatco Ltd

Dana Incorporated

Ricardo plc

Allison Transmission Holdings

Hewland Engineering Ltd

Xtrac Limited

- Commercial fleet operators prioritizing cost efficiency and durability

- Rural consumers maintaining strong preference for manual systems

- Automotive workshops driving aftermarket demand growth

- Logistics firms focusing on maintenance optimization and lifecycle cost reduction

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now