Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Philippines online insurance market reached approximately USD ~ billion in gross written premiums, driven by rapid mobile internet adoption, rising digital payment penetration, and strong bancassurance-to-digital channel migration reported by the Insurance Commission and Bangko Sentral ng Pilipinas. Embedded microinsurance offerings through e-wallet ecosystems and online aggregators expanded reach among first-time policyholders, while simplified underwriting and instant issuance models reduced acquisition costs and accelerated digital policy distribution across life, health, and non-life categories nationwide.

Metro Manila remains the dominant hub for the Philippines online insurance market due to its concentration of insurers, digital platforms, fintech partnerships, and higher digital literacy levels, supported by strong broadband and mobile wallet usage. Cebu and Davao also show strong uptake as regional economic centers with expanding middle-income populations and growing insurtech distribution networks. Urban employment formalization, OFW remittance flows, and SME digitization across these cities sustain online policy adoption through employer-linked and consumer-direct digital insurance channels.

Market Segmentation

By Product Type

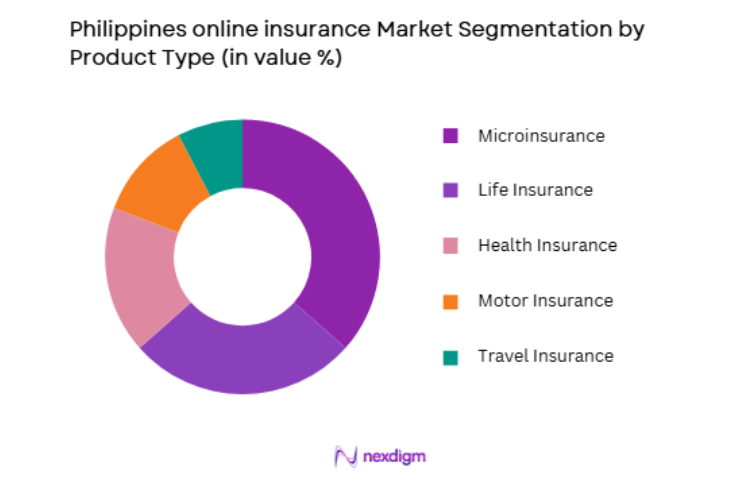

Philippines online insurance market is segmented by product type into life insurance, health insurance, motor insurance, travel insurance, and microinsurance. Recently, microinsurance has a dominant market share due to factors such as affordability, mobile wallet integration, strong insurer-fintech partnerships, and regulatory promotion of inclusive insurance. Insurers leverage e-commerce and e-wallet ecosystems to distribute low-ticket policies at scale, attracting first-time policyholders and informal-sector consumers.

By Distribution Channel

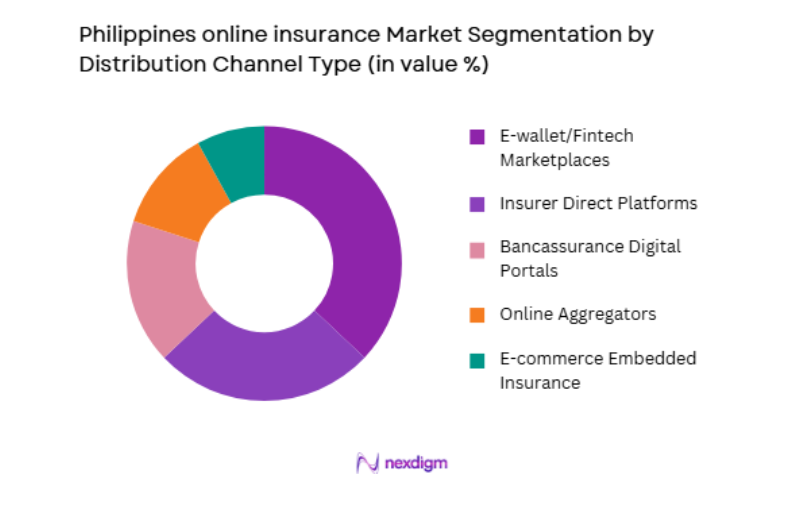

Philippines online insurance market is segmented by distribution channel into insurer direct platforms, bancassurance digital portals, e-wallet/fintech marketplaces, online aggregators, and e-commerce embedded insurance. Recently, e-wallet/fintech marketplaces have a dominant market share due to factors such as massive user bases, integrated payments, and frictionless purchase journeys embedded within daily financial transactions. Insurers gain access to millions of verified digital users, enabling micro-premium collection and automated renewals.

Competitive Landscape

The Philippines online insurance market shows moderate consolidation with a mix of established insurers and insurtech-enabled distributors leveraging digital platforms and fintech ecosystems. Large life insurers dominate through bancassurance and mobile integrations, while agile insurtech firms expand microinsurance and embedded coverage. Strategic partnerships with e-wallet providers and digital banks shape distribution leadership, and regulatory support for inclusive insurance encourages innovation among both incumbents and digital-first entrants.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Distribution Partnerships |

| Pru Life UK Philippines | 1996 | Taguig | ~ | ~ | ~ | ~ | ~ |

| Sun Life Philippines | 1895 | Taguig | ~ | ~ | ~ | ~ | ~ |

| Manulife Philippines | 1907 | Makati | ~ | ~ | ~ | ~ | ~ |

| FWD Philippines | 2014 | Taguig | ~ | ~ | ~ | ~ | ~ |

| Pioneer Insurance | 1954 | Makati | ~ | ~ | ~ | ~ | ~ |

Philippines Online Insurance Market Analysis

Growth Drivers

Expansion of mobile financial ecosystems enabling embedded insurance distribution

Digital wallets and super-apps in the Philippines have evolved into comprehensive financial ecosystems that integrate payments, lending, savings, and insurance within a single user journey, dramatically expanding the accessibility of online insurance products to previously uninsured populations across urban and rural regions. The large installed base of verified mobile wallet users allows insurers to distribute micro-premium policies with minimal onboarding friction, leveraging existing KYC data and payment rails to enable instant policy issuance and automated renewals through recurring deductions. Insurers increasingly embed contextual insurance offers within everyday transactions such as remittances, travel bookings, e-commerce purchases, and utility payments, aligning coverage with real-time consumer needs and improving conversion rates compared with traditional advisory channels. The widespread use of QR payments and peer-to-peer transfers reinforces habitual digital financial engagement, making insurance purchasing a natural extension of daily digital behavior rather than a standalone decision requiring agent interaction. Partnerships between insurers and fintech platforms also enable behavioral data analytics to refine product targeting and pricing segmentation, allowing insurers to tailor coverage amounts, durations, and premium levels to specific consumer risk profiles and spending patterns observed within wallet ecosystems. Regulatory encouragement of inclusive insurance and digital onboarding frameworks further legitimizes mobile-first distribution models and accelerates insurer investment in API-driven integration with financial platforms.

Rising middle-income digital adoption and urban workforce formalization

The Philippines has experienced sustained growth in digitally connected middle-income households concentrated in major metropolitan areas, where formal employment, stable income flows, and employer-linked financial services increase awareness and affordability of insurance products delivered through online channels. Urban professionals increasingly manage financial planning, savings, and investments through mobile banking and digital wealth platforms, creating natural adjacency for life and health insurance offerings distributed via the same digital interfaces. Employer-provided group insurance schemes are also transitioning toward digital enrollment and self-service policy management portals, familiarizing employees with online insurance processes and encouraging voluntary top-up purchases through direct digital channels. Remittance-receiving households supported by overseas Filipino worker income streams show heightened demand for protection products, particularly health and life coverage, and digital purchasing mechanisms enable geographically dispersed families to secure policies conveniently without branch visits. Education levels and financial literacy improvements in urban centers strengthen trust in regulated financial services, reducing perceived risk associated with online policy purchase and digital claims submission. Insurers respond by simplifying product language and policy structures for digital comprehension, using interactive calculators and chat-based advisory tools to guide consumers through coverage selection within online environments.

Market Challenges

Consumer trust deficits and perceived complexity in digital insurance purchasing

Despite rapid digital adoption in financial services, a significant segment of Filipino consumers remains cautious about purchasing insurance entirely online due to concerns regarding policy transparency, claims reliability, and long-term insurer credibility, particularly among first-time policyholders with limited experience in formal financial products. Insurance inherently involves deferred benefits and contractual obligations that are less tangible than transactional financial services, making digital-only interactions insufficient for some consumers who prefer human advisory reassurance before committing to coverage. Online product descriptions and policy wording often remain complex, and consumers may struggle to interpret exclusions, coverage limits, and claims procedures without personalized explanation, increasing hesitation in completing digital purchases. Negative anecdotal experiences related to claims disputes or perceived insurer inaccessibility can spread rapidly through social media, amplifying distrust and discouraging broader adoption of online insurance channels. Additionally, low historical insurance penetration in the Philippines means many consumers lack baseline understanding of risk pooling and policy value, making them more vulnerable to misconceptions about digital insurance legitimacy or utility. Insurers attempt to mitigate these concerns through simplified products and chat-based support, yet fully replacing agent-led trust-building remains challenging, especially in life and health categories involving higher premiums and long durations.

Fragmented regulatory interpretation and integration complexity across insurers and fintech platforms

The Philippines insurance sector operates within a regulated framework that continues adapting to digital distribution models, yet variations in compliance interpretation and operational requirements across insurers and fintech partners create integration challenges that slow online insurance scaling and innovation. Insurers must align digital onboarding, electronic signatures, KYC validation, and policy documentation with regulatory expectations while simultaneously integrating with multiple fintech ecosystems, each with distinct technical standards, data governance protocols, and consumer interface requirements. These integration efforts demand significant IT investment and ongoing maintenance, particularly when insurers partner with several e-wallets, digital banks, and e-commerce platforms to maximize reach, increasing operational complexity and costs. Regulatory safeguards for consumer protection and product approval also require insurers to adapt policy structures for microinsurance and embedded formats, which may involve additional review cycles before deployment on digital marketplaces.

Opportunities

Expansion of parametric and usage-based digital insurance models

The Philippines faces frequent climate-related risks such as typhoons, floods, and earthquakes, creating a strong opportunity for digitally distributed parametric insurance products that provide predefined payouts triggered by measurable events rather than traditional claims assessments, enabling faster settlement and improved consumer trust in online insurance mechanisms. Digital platforms can integrate weather data, geolocation, and satellite monitoring to automate eligibility verification and claims activation, significantly reducing administrative complexity and enhancing transparency for policyholders who receive payouts without manual documentation. Usage-based insurance models, particularly in motor and travel segments, can leverage telematics, mobility apps, and booking platforms to align premiums with actual behavior and exposure, making coverage more affordable and personalized for digitally active consumers. Parametric crop and disaster microinsurance delivered through mobile wallets can extend protection to rural populations and small businesses that remain underserved by traditional insurance channels, advancing inclusive insurance goals while expanding market size. Government climate resilience initiatives and disaster risk financing programs also create potential partnerships between insurers and public agencies to distribute subsidized parametric policies through digital channels, increasing adoption scale.

Integration of digital insurance within digital banking and lending ecosystems

The rapid expansion of digital banking and online lending platforms in the Philippines creates substantial opportunity to embed insurance products directly within credit, savings, and payments journeys, transforming insurance from a standalone purchase into an integrated financial protection layer attached to core financial services used daily by consumers and small enterprises. Digital banks increasingly provide personal loans, SME financing, and savings products through app-based interfaces, enabling insurers to bundle life, health, or credit protection coverage seamlessly during loan origination or account opening processes without requiring separate enrollment steps. Borrowers perceive insurance as a natural risk-mitigation component of financial obligations, particularly for income protection or loan repayment assurance, increasing acceptance of bundled digital policies compared with voluntary standalone insurance offers. Insurers benefit from access to verified customer financial data, enabling more accurate risk assessment and pricing personalization within digital credit ecosystems while reducing fraud and underwriting uncertainty. The integration also supports automated premium deduction and policy servicing through existing banking channels, enhancing retention and persistency rates for online insurance products. SME borrowers using digital lending platforms present opportunities for business interruption and asset protection policies distributed online, expanding commercial insurance penetration among small enterprises historically underserved by traditional insurers.

Future Outlook

The Philippines online insurance market is expected to expand steadily as mobile financial ecosystems deepen and insurers accelerate digital product innovation across life, health, and microinsurance categories. Embedded insurance within e-wallets, digital banks, and e-commerce platforms will remain the primary growth channel, supported by regulatory emphasis on inclusive insurance and consumer protection. Parametric and usage-based models are likely to gain traction in climate and mobility segments. Rising digital literacy and urban income growth will further strengthen online insurance adoption nationwide.

Major Players

- Pru Life UK Philippines

- Sun Life Philippines

- Manulife Philippines

- FWD Philippines

- AXA Philippines

- Allianz PNB Life

- Pioneer Insurance

- Malayan Insurance

- Insular Life

- Etiqa Philippines

- BPI AIA Life Assurance

- Generali Philippines

- Pacific Cross Philippines

- Philam Life

- Cocogen Insurance

Key Target Audience

- Insurance companies

- Insurtech startups

- Digital banks

- E-wallet and fintech platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Bancassurance partners

- E-commerce platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables including digital distribution channels, product types, premium volumes, regulatory frameworks, and consumer adoption drivers were identified through secondary research and insurer disclosures. Market boundaries were defined to isolate online-originated policies and embedded digital insurance transactions. Relevant macroeconomic and digital finance indicators were mapped to insurance adoption patterns.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using insurer reports, regulatory statistics, and digital platform adoption metrics. Channel-level distribution and product penetration patterns were triangulated across multiple data sources. Competitive positioning and ecosystem partnerships were analyzed to determine structural market dynamics and concentration.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with insurance executives, fintech specialists, and regulatory observers to confirm digital distribution trends and adoption drivers. Assumptions regarding consumer behavior and ecosystem integration were refined based on expert insights. Market share allocations were cross-checked against industry perspectives.

Step 4: Research Synthesis and Final Output

All validated data and qualitative insights were synthesized into a coherent analytical framework covering market size, segmentation, drivers, challenges, and opportunities. Forecast outlook and strategic implications were derived from structural trends and ecosystem developments. Final outputs were reviewed for consistency, accuracy, and market relevance.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising smartphone and mobile internet penetration enabling digital policy purchase

Expansion of e-wallet and super app ecosystems integrating insurance offerings

Regulatory push toward financial inclusion and digital insurance distribution - Market Challenges

Low insurance literacy and trust barriers in fully digital channels

Legacy insurer systems limiting seamless online integration

Fraud risks and cybersecurity concerns in online transactions - Market Opportunities

Embedded microinsurance across e-commerce and mobility platforms

Data-driven underwriting using digital behavior and alternative data

Expansion of low-ticket policies for underserved populations - Trends

Super app–based insurance distribution partnerships

Instant policy issuance and digital claims automation - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Life Insurance

Online Health Insurance

Online Motor Insurance

Online Travel Insurance

Online Microinsurance - By Platform Type (In Value%)

Mobile Insurance Applications

Web Insurance Portals

Super App Insurance Integrations

Bancassurance Digital Platforms

Aggregator and Marketplace Platforms - By Fitment Type (In Value%)

Direct-to-Consumer Online

Embedded Insurance

Digital Bancassurance

Aggregator-based Distribution - By End User Segment (In Value%)

Individual Consumers

Small and Medium Enterprises

Gig Economy Workers

- Market Share Analysis

- Cross Comparison Parameters (Product Type, Distribution Channel, Digital Platform Capability, Customer Segment Focus, Pricing Model, Underwriting Approach, Claims Automation Level, Partnership Ecosystem, Data Analytics Maturity, Customer Experience Design)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

AIA Philippines

Sun Life Philippines

Pru Life UK Philippines

Manulife Philippines

AXA Philippines

FWD Philippines

BPI AIA Life Assurance

Insular Life

Allianz PNB Life

Etiqa Philippines

Singlife Philippines

Pioneer Insurance

Malayan Insurance

Standard Insurance

Cocogen Insurance

- Growing preference for mobile-first insurance journeys among young consumers

- SME demand for simple, low-cost digital protection products

- Gig workers adopting flexible and short-duration coverage

- Overseas workers purchasing remote policies for family protection

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now