Download PDF

Download PDFMarket Overview

The Philippines Outdoor Apparel market, is valued at USD ~ million in 2025, based on Nexdigm’s industry analysis covering performance apparel, footwear, and outdoor gear purchased by consumers and speciality retailers. This growth stems from rising participation in adventure sports and recreational outdoor activities, coupled with expanding health and fitness awareness among younger demographics and rising disposable incomes across urban centres. These factors have driven demand for breathable, moisture‑wicking, and UV‑protective outdoor clothing designed for hiking, cycling, water sports, and camping, with apparel revenues tracking alongside overall outdoor gear adoption.

Metro Manila, Cebu, and Davao function as the dominant hubs for outdoor apparel demand and distribution in the Philippines, supported by high population concentrations, concentrated retail infrastructure, and vibrant outdoor lifestyle communities. Metro Manila’s large urban population and dense network of specialty sports retailers and e‑commerce fulfillment centres create substantial market pull, while Cebu and Davao benefit from rapidly growing participation in adventure tourism, beach and mountain activities, and regional brand engagement. These urban and regional centres also act as logistical and distribution anchors for both domestic and imported outdoor apparel lines, reinforcing their leadership role in the market.

Market Segmentation

By Product Category

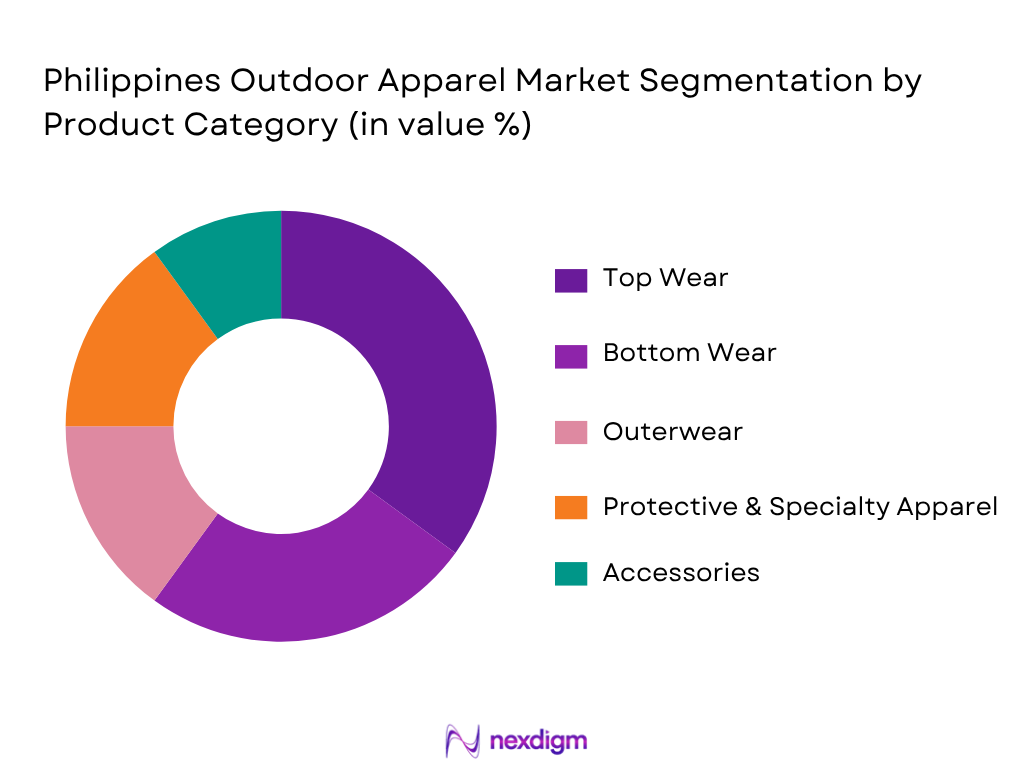

The outdoor apparel market in the Philippines is segmented by product category into top wear, bottom wear, outerwear, protective apparel and accessories. Top wear dominates share, largely because performance tops are the most frequently replaced and season‑agnostic items, appealing to hikers, cyclists, and water sports participants across most seasons. These products are also among the most visible apparel types in outdoor retail channels and e‑commerce listings, fuelling awareness and sales. In addition, strong participation in day hiking and trail running means consumers frequently purchase lightweight technical shirts that balance comfort, UV protection, and moisture management. Bottom wear follows due to its essential role in outdoor activity apparel, particularly in beach‑to‑mountain adventure itineraries common among domestic travellers. Outerwear and protective apparel, while smaller in share, are growing due to demand for waterproof and wind‑resistant gear tailored for sudden tropical weather changes. Accessories complete the mix, driven by fashion and activity functional requirements.

By Distribution Channel

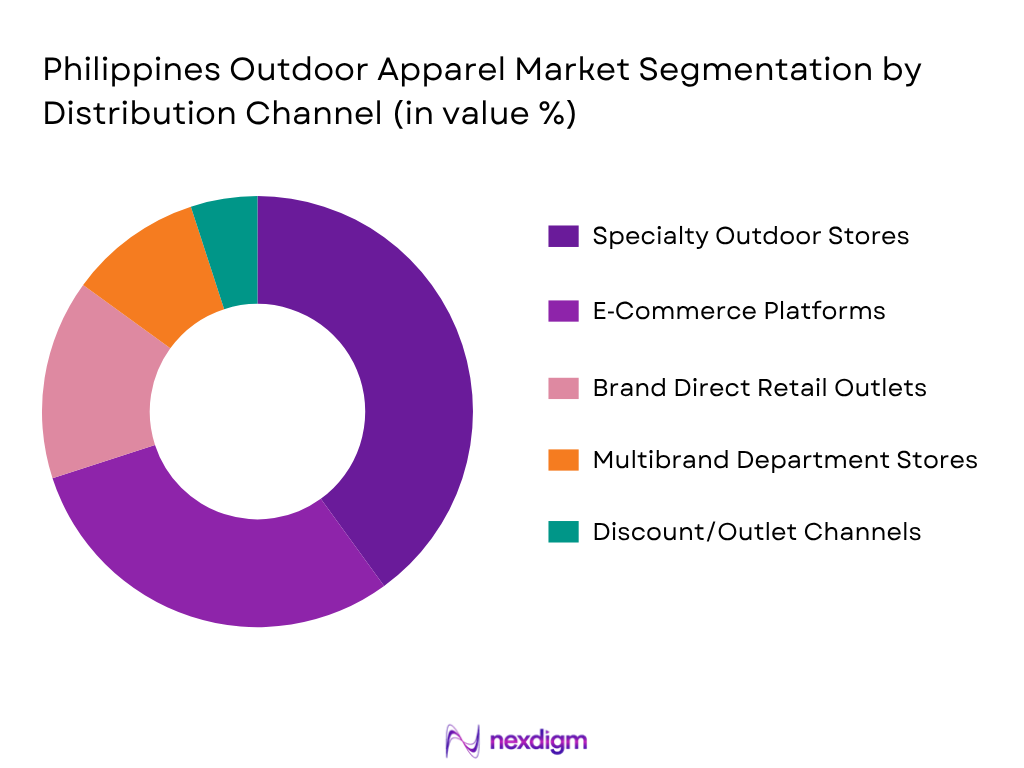

Under distribution channel segmentation, the Philippines outdoor apparel market is categorised into speciality outdoor stores, e‑commerce platforms, brand direct outlets, department stores, and discount/outlet channels. Specialty outdoor stores hold the largest share as they offer curated selections of technical apparel tailored to specific activities, coupled with expert staff guidance, a valuable factor for consumers investing in performance clothing. These stores also anchor experiential engagement, where fit, fabric technology, and activity‑specific performance can be assessed prior to purchase. E‑commerce platforms follow closely, reflecting rapid growth in online shopping for outdoor apparel driven by convenience, broader SKU availability, and expanding digital marketplaces that cater to both local and imported brands. Brand direct retail outlets, including flagship stores and official brand counters, contribute moderately, often supported by marketing pull and brand loyalty. Multibrand department stores and discount channels make up the balance, often focused on value propositions or seasonal promotions.

Competitive Landscape

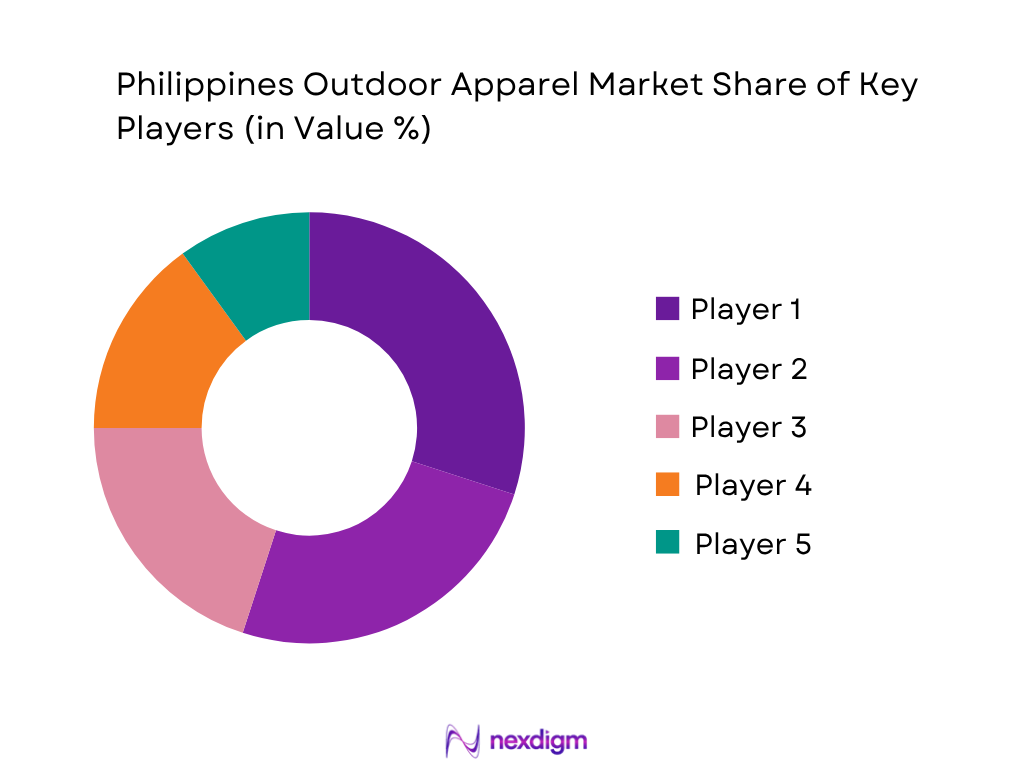

The Philippines outdoor apparel market is moderately consolidated, with a mix of local brands specialising in tropical‑climate outdoor apparel and global outdoor/international sportswear brands extending their distribution via retail partners and digital platforms. This blend reflects both consumer preference for performance items and rising demand for brand‑led product experiences. The competitive landscape reflects consolidation among a few local leaders with strong outdoor brand identities, supported by growing listings on online marketplaces and expanding retail footprints in urban and regional centres. International brands participate largely through multibrand-store partnerships or e‑commerce channels, adding technology differentiation but often at higher price points. The competitive set is diversified by focus areas from lightweight tropical performance apparel to lifestyle and casual outdoor lines.

| Brand/Company | Est. Year | Headquarters | Technical Fabric Adoption | Retail Footprint | E‑Commerce Presence | Activity Focus | Local Brand Recognition |

| Professional Gear, Inc. | 1990* | Philippines | ~ | ~ | ~ | ~ | ~ |

| Habagat Outdoor Goods | 2005* | Philippines | ~ | ~ | ~ | ~ | ~ |

| Lagalag Outdoor Co. | 2010* | Philippines | ~ | ~ | ~ | ~ | ~ |

| Sandugo PH | 2000* | Philippines | ~ | ~ | ~ | ~ | ~ |

| 8a Outdoor Apparel | 2012* | Philippines | ~ | ~ | ~ | ~ | ~ |

Philippines Outdoor Apparel Market Analysis

Growth Drivers

Adventure Tourism

The Philippines’ adventure and nature tourism sectors are key underlying drivers for outdoor apparel demand because they generate direct and indirect expenditures linked to outdoor activity participation. According to the Philippine Statistics Authority, the tourism industry contributed PHP 2.35 trillion to the economy, representing 8.9 % of GDP, with internal tourism expenditure (domestic plus inbound) reaching PHP 3.86 trillion in 2024, indicating strong consumer spending on travel, recreation, and related gear purchases. Domestic tourism expenditure alone grew to PHP 3.16 trillion, while outbound tourism expenditure expanded to PHP 345.68 billion. Adventure tourism, including hiking, beach activities, diving, and island excursions is a significant portion of these expenditures, as natural attractions like Palawan, Batanes, and the Cordillera mountain regions attract millions of Filipinos and foreign visitors yearly, driving the need for performance outdoor clothing suited to rugged terrain and varied weather. Employment in tourism industries also rose to 6.75 million, accounting for 13.8 % of total employment, further reflecting the broad engagement in tourism and associated outdoor activities that stimulate apparel demand. These strong tourism receipts and employment levels demonstrate how adventure tourism supports increased outdoor apparel consumption from coastal to high‑altitude regions.

Fitness Lifestyle

Macro‑economic indicators show that the Philippines’ economy and population dynamics are supportive of a rising fitness and active lifestyle culture that fuels demand for outdoor and performance apparel. According to World Bank data, the Philippines’ GDP reached USD 461.62 billion in 2024, while GDP per capita reached USD 3,984.8, both reflecting continued economic expansion and rising consumer purchasing power despite global pressures. The country’s unemployment rate declined to 2.2 %, a relatively low level that can translate into more discretionary spending on lifestyle goods, including sports and outdoor apparel. Furthermore, the population grew to 115.84 million in 2024, with a young demographic profile that tends to participate in fitness, trekking, cycling, and recreational sports. This demographic trend aligns with increased fitness‑related expenditure on apparel designed for comfort, breathability, and performance. Tourism data also supports fitness trends: the travel services sector (including recreational travel and fitness tourism segments) accounted for 34.08 % of service imports, indicating significant movement associated with leisure and activity‑based travel. Together, robust employment, rising per capita GDP, and substantial travel activity form a macro backdrop where fitness lifestyles and recreational outdoor participation drive consistent demand for outdoor apparel suited to physical activity and adventure experiences.

Market Challenges

Import Dependency

A significant market challenge for the Philippines outdoor apparel sector is its heavy dependence on imported goods and textiles, which affects pricing, availability, and seasonal inventory planning. According to World Bank trade data, the total value of Philippine imports reached USD 185.16 billion in 2024, up from previous years, illustrating the economy’s reliance on foreign‑sourced products, including apparel, textiles, and specialized outdoor fabrics. The Philippine merchandise trade, a combined measure of exports and imports as a share of GDP, stood at 44.9 % of GDP, highlighting the importance of cross‑border supply chains to meet domestic demand for apparel and gear. Apparel categories such as articles of clothing (including performance and outdoor wear) are typically part of these imported goods, making the market susceptible to international price fluctuations, shipping costs, and foreign tariff changes. WTO data shows that applied tariffs in the Philippines averaged 6.0 % in 2024, which can add cost burdens to imported apparel items beyond base FOB prices and affect retail affordability for outdoor performance apparel. In addition, reliance on imports can lead to supply chain disruptions from global manufacturing hubs, for example, delays, port congestion, or raw material shortages that impact inventory planning for retail seasons like summer beach months and peak trekking periods. These macro trade dynamics reflect how import dependency remains a structural challenge for pricing stability and consistent product availability in the outdoor apparel segment.

Price Sensitivity

Price sensitivity among Filipino consumers is another pivotal challenge in the outdoor apparel market, influenced by overall economic conditions and income levels. Although GDP per capita increased to USD 3,984.8 in 2024, it remains significantly below global averages, roughly one‑fifth of the world average of USD 19,439 — implying that discretionary spending on premium outdoor apparel may be constrained for a large segment of consumers. This pressure is reinforced by inflation and cost‑of‑living factors: in 2024, consumer price inflation was reported at 3.2 %, which affects real purchasing power and consumer choices between essential goods and leisure‑related apparel purchases. The youth and fitness sectors often seek performance clothing, but high retail apparel pricing (especially for imported brands) can limit penetration in middle‑income and regional consumer bases. Furthermore, while tourism expenditure figures like PHP 760.5 billion in tourism receipts reflect spending on travel experiences, not all of this filters into high‑end outdoor apparel purchases, which remain aspirational for many local consumers. The combination of modest per capita income and broader inflationary pressures results in Filipino buyers often prioritising value for money, affordable functional apparel, or domestic brands over premium imported lines. This price sensitivity translates into competitive retail dynamics where affordability can be as decisive as performance features for apparel choice.

Opportunities

Direct‑to‑Consumer Expansion

The Philippines presents significant opportunity for direct‑to‑consumer (DTC) retail expansion within the outdoor apparel market through both physical and digital channels. With over 115 million people and increasing urbanisation, consumers are increasingly engaging with online shopping platforms facilitated by improved internet penetration and mobile connectivity, creating favourable conditions for direct brand interactions without intermediaries. The robust performance of the tourism and outdoor recreation sectors provides a complementary backdrop: in 2024, international tourism revenue reached PHP 760.5 billion, and tourism contributed PHP 2.35 trillion to GDP, reflecting heightened consumer activity and spending that can be leveraged by outdoor brands to market performance and adventure‑specific apparel directly to end users. For outdoor apparel brands, establishing DTC channels allows greater control over marketing, product education, and customer experience, especially in key urban centres with strong tourism and fitness participation. These channels also support engagement with consumer communities that value technical features such as moisture‑management, UV protection, and climate‑responsive fabrics, enabling brands to cultivate loyalty and repeat purchase behaviour.

Sustainable Product Lines

Sustainability and eco‑friendly product lines present a differentiated growth avenue for outdoor apparel brands in the Philippine market. Consumers increasingly value environmental stewardship, and brands that adopt sustainable materials such as recycled polyester or eco‑certified fabrics and transparent supply chains can attract conscious buyers willing to invest in products that align with global sustainability trends. This opportunity is reinforced by broader tourism and outdoor recreation data that show rising engagement with nature‑based experiences: the tourism sector’s expansion to PHP 760.5 billion in revenue suggests that a significant portion of both international and domestic travellers participate in outdoor activities such as trekking, diving, and nature tours that naturally align with sustainability messaging. Further, macroeconomic indicators such as growing service sector contributions and rising employment in recreation‑related industries provide structural context for enhanced consumer willingness to pay for performance apparel with sustainable credentials, especially among younger demographics more attuned to environmental issues.

Future Outlook

The Philippines outdoor apparel market is poised for continued expansion over the next decade, underpinned by increasing participation in outdoor recreational activities, improving retail infrastructure, and digital commerce acceleration. Outdoor apparel brands that prioritise technical innovation (moisture‑wicking, UV protection, breathable fabrics) and sustainable material adoption are expected to resonate strongly with evolving consumer preferences. Growth will also be supported by rising middle‑class incomes, an expanding youth demographic engaging in adventure tourism, and the proliferation of direct‑to‑consumer channels that broaden market access. As domestic tourism infrastructure continues to mature, especially in nature‑‑based destinations, outdoor apparel consumption is expected to deepen beyond major urban hubs into emerging provincial markets, strengthening the long‑term growth trajectory.

Major Players

- Professional Gear, Inc.

- Habagat Outdoor Goods

- Lagalag Outdoor Co.

- Sandugo PH

- 8a Outdoor Apparel

- Conquer Outdoors

- Brown Trekker

- Groundzero Apparel

- Burger & Bones

- Flatisboring PH

- SAM Outdoors

- Columbia Sportswear

- The North Face

- Patagonia

- Salomon

Key Target Audience

- Outdoor Apparel Retail Chains & Specialty Stores

- Brand Licensing & Franchise Investors

- Sporting Goods Manufacturers & Material Technology Suppliers

- Investments and Venture Capitalist Firms (Outdoor & Sports Sector)

- E‑Commerce and Direct‑to‑Consumer Platforms

- Outdoor Tourism & Adventure Package Operators

- Government and Regulatory Bodies (e.g., Department of Trade and Industry; Bureau of Philippine Standards)

- Retail Real Estate & Distribution Network Investors

Research Methodology

Step 1: Identification of Key Variables

The initial phase involved mapping stakeholders across the Philippines outdoor apparel ecosystem, including manufacturers, importers, retailers, and consumer groups. Desk research leveraged secondary databases, market intelligence platforms, and trade data to define variables affecting demand, pricing, and distribution.

Step 2: Market Analysis and Construction

Historical revenue and volume data were compiled for outdoor apparel categories. Distribution channel dynamics, consumer behaviour, and pricing data were assessed using retail analytics, point‑of‑sale data sources, and secondary industry forecasts to construct a bottom‑up market sizing model.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding growth drivers, consumer preferences, and product adoption were validated through expert interviews with apparel buyers, brand managers, and retail executives operating in the Philippines. Qualitative insights refined segmentation and competitive analysis.

Step 4: Research Synthesis and Final Output

Final analysis integrated quantitative models and qualitative feedback, ensuring consistency and validation. This phase included cross‑verification with available third‑party market studies and export‑import statistics to ensure the Philippines outdoor apparel market estimate is robust and credible.

- Executive Summary

- Research Methodology (Market Definitions and Scope of Philippines Outdoor Apparel, Abbreviations, Data Sources, Top‑Down and Bottom‑Up Market Sizing Approach, Primary Research Protocol, Sampling Framework, Data Validation and Triangulation, Assumptions & Limitations)

- Market Definition and Scope

- Market Genesis & Evolution

- Philippines Macro‑Economic Indicators Impacting Outdoor Apparel Demand

- Supply Chain and Value Chain Analysis

- Distribution Channel Ecosystem

- Growth Drivers (Adventure Tourism, Fitness Lifestyle, Tropical Outdoor Activities, Rising Income, Performance Apparel Innovation, Brand Loyalty, Omni-Channel Expansion, Sustainable Fabrics)

- Market Challenges (Import Dependency, Price Sensitivity, Seasonal Demand, Low Technical Awareness, Counterfeit Products, Inventory Management, High Specialty Store Costs)

- Opportunities (Direct-to-Consumer Expansion, Sustainable Product Lines, Customization Services, Local-International Brand Collaboration, Rental & Resale Models, E-Commerce Growth, Activity-Specific Lines)

- Emerging Trends (Smart & Technical Fabrics, Influencer Marketing, Seasonal Collections, Eco Packaging, Hybrid Urban-Outdoor Apparel, Activity-Based Personalization, Mobile Commerce Integration)

- Regulatory Environment (DTI Apparel Standards, Import Tariffs, Consumer Protection & Labeling, Environmental & Labor Compliance, OEKO-TEX / Bluesign Certification, Advertising Verification, Packaging Guidelines)

Porter’s Five Forces Analysis (New Entrants, Supplier Power, Buyer Power, Substitutes, Competitive Rivalry) - SWOT Analysis (Market Level) (Strengths: Outdoor Culture, Technical & Eco Fabrics; Weaknesses: Import Dependency, Price Sensitivity; Opportunities: E-Commerce, Sustainability & Customization; Threats: Supply Disruption, Competitive Saturation)

- Value Chain & Supply Chain Analysis (Raw Materials – Polyester, Nylon, Wool, Recycled Fabrics, Laminates; Domestic vs Imported Production; Capacity & Lines; Logistics Hubs; Retail & E-Commerce Channels; Quality Testing; Returns & Reverse Logistics)

- Consumer Purchase Behavior & Retail Analytics (Purchase Frequency, Basket & Cross-Sell, Brand Loyalty, Online vs In-Store, Social Media Impact, Seasonal & Weather Buying, Willingness-to-Pay for Sustainability & Technical Features, Activity-Specific Adoption)

- By Market Value (2020-2025)

- By Market Volume (2020-2025)

- By Average Selling Price Trends (2020-2025)

- By Product Category (In Value%)

Top Wear

Bottom Wear

Outerwear

Protective Gear

Accessories - By Material Technology (In Value%)

Breathable/Synthetic Performance Fabrics

Natural Fibers

Hybrid Materials - By Distribution Channel (In Value%)

Specialty Outdoor Stores

Department Stores

E‑Commerce

Direct Brand Stores - By Consumer Type (In Value%)

Men

Women

Youth & Kids Outdoor Enthusiasts - By Activity Use Case (In Value%)

Hiking & Trekking Apparel

Water Sports Apparel

Cycling Apparel

Camping & Mountaineering Apparel

- Market Share of Major Players (Retail Revenue, Volume by SKU, Local vs International Brands)

- Cross Comparison Parameters (Company Overview, Brand Positioning & Value Proposition, Distribution Footprint, Product Portfolio Depth, Fabric & Material Technology Adoption, Pricing Positioning & Price Band Coverage, Retail Channel Mix, Marketing & Sponsorship Initiatives)

- Competitive Benchmarking (Operational Efficiency, Activity-Specific Line Depth, Regional Presence, Product Differentiation, Retail & E-Commerce Integration)

- Pricing Benchmarking (SKU-Level Pricing, Price Bands, Promotions, Premium vs Value Lines)

- SWOT Analysis of Key Players (Strengths: Brand Equity, Technical Performance; Weaknesses: Limited Local Manufacturing, Price Sensitivity; Opportunities: Expansion of Eco & Direct-to-Consumer Lines; Threats: Competitive Saturation, Import Reliance)

- Profiles of Key Market Participants

Professional Gear, Inc.

Habagat Outdoor Goods

Lagalag Outdoor Co.

Sandugo PH

8a Outdoor Apparel

Conquer Outdoor

Burger and Bones Apparel

Brown Trekker

Groundzero Apparel

Flatisboring PH

SAM Outdoors

Columbia Sportswear

The North Face

Patagonia

Salomon

- Demographics & Target Segments (Age Groups, Gender, Income Levels, Urban vs Rural, Lifestyle & Outdoor Activity Participation)

- Purchase Behavior & Decision Drivers (Category Preference, Brand Loyalty, Price Sensitivity, Technical Features, Sustainability Awareness, Peer & Social Media Influence, Seasonal & Weather Impact, Activity-Specific Needs)

- Spending Patterns & Budget Allocation (Average Basket Value, Premium vs Mid-Tier Spending, Channel Preference [Online vs Offline], Frequency of Purchase, Multi-Item Bundling, Promotional Impact)

- Channel & Platform Preferences (Brand Stores, Multi-Brand Retailers, Specialty Retailers, E-Commerce Platforms, Offline Marketplaces, Social Commerce Influence)

Consumer Awareness & Attitude (Brand Recognition, Technical Fabric Understanding, Sustainability & Eco-Friendly Awareness, Willingness-to-Pay for Innovation, Fashion vs Performance Orientation, Adoption of Hybrid/Urban-Outdoor Apparel) - Customer Journey & Purchase Funnel (Discovery, Research & Evaluation, Trial & Purchase, Post-Purchase Experience, Returns & Exchange Behavior, Referral & Repeat Buying)

- Lifestyle & Activity Segmentation (Hiking/Trekking, Mountaineering, Trail Running, Camping, Cycling, Adventure Tourism, Fitness-Oriented Outdoor Engagement)

- Consumer Satisfaction & Pain Points (Product Fit & Comfort, Durability & Quality, Pricing vs Value, Channel Convenience, Delivery & Returns Experience, Availability of Technical Features, Seasonal Stock Limitations)

- By Value (2025-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now