Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines printed circuit board market reached approximately USD ~ billion based on a recent historical assessment, supported by expansion of electronics manufacturing services, semiconductor packaging, and export-oriented assembly operations. Demand is primarily driven by multilayer and flexible circuit boards used in telecommunications equipment, automotive electronics modules, and consumer devices produced in export processing zones. Government investment in electronics manufacturing clusters and steady inflow of foreign electronics firms further sustain production scale and domestic PCB consumption.

Metro Manila, Calabarzon, and Central Luzon dominate the Philippines printed circuit board market due to concentration of electronics manufacturing services plants, semiconductor assembly facilities, and export-oriented industrial parks. These regions host major multinational electronics manufacturers and PCB assembly lines supported by skilled technical labor pools, port connectivity, and infrastructure availability. Proximity to semiconductor packaging ecosystems and established supply chains for copper laminates and components strengthens regional PCB fabrication and assembly capacity.

Market Segmentation

By Product Type:

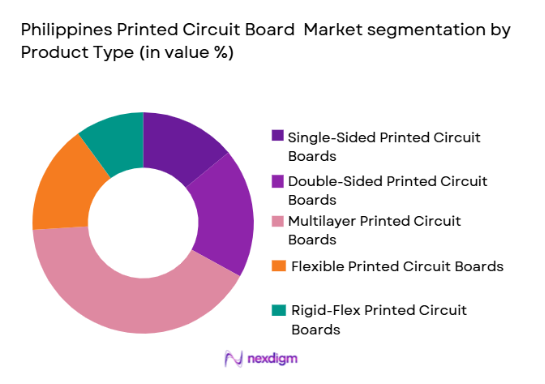

Philippines printed circuit board market is segmented by product type into single-sided printed circuit boards, double-sided printed circuit boards, multilayer printed circuit boards, flexible printed circuit boards, and rigid-flex printed circuit boards. Recently, multilayer printed circuit boards has a dominant market share due to factors such as rising electronics complexity, strong telecom equipment assembly demand, and widespread adoption in automotive and industrial electronics modules produced in export manufacturing facilities.

By End-Use Industry:

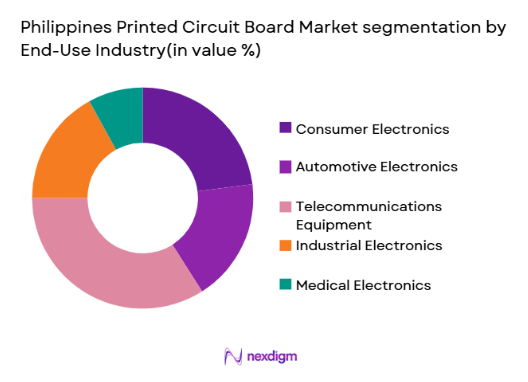

Philippines printed circuit board market is segmented by end-use industry into consumer electronics, automotive electronics, telecommunications equipment, industrial electronics, and medical electronics. Recently, telecommunications equipment has a dominant market share due to factors such as sustained network infrastructure deployment, strong export manufacturing of communication devices, and demand for high-density multilayer boards used in routers, base stations, and broadband hardware produced domestically.

Competitive Landscape

The Philippines printed circuit board market is moderately consolidated, with multinational electronics manufacturing services firms and semiconductor companies controlling a substantial share of domestic PCB assembly and fabrication capacity. Competition centers on multilayer and high-density board production capabilities, export relationships, and integration with semiconductor packaging operations. Major players maintain long-term supply agreements with global electronics brands, while regional PCB producers compete on cost efficiency, manufacturing scale, and compliance with international electronics quality standards.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | PCB Capability |

| IMI | 1980 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Ionics EMS | 1974 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Sumitronics Philippines | 1990 | Japan | ~ | ~ | ~ | ~ | ~ |

| Murata Philippines | 1944 | Japan | ~ | ~ | ~ | ~ | ~ |

| Amkor Technology Philippines | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Printed Circuit Board Market Analysis

Growth Drivers

Expansion of Export-Oriented Electronics Manufacturing Ecosystem:

The Philippines printed circuit board market benefits significantly from the country’s role as a major export hub for electronics manufacturing services and semiconductor assembly, which directly increases domestic demand for multilayer and flexible PCBs. Large multinational EMS companies operate extensive manufacturing campuses in industrial zones, producing telecom equipment, automotive electronics modules, and consumer devices requiring high-density circuit boards. Export-driven production ensures stable PCB consumption volumes, as international brands rely on Philippine assembly plants for global supply chains. Government incentives for electronics investors, including tax benefits and special economic zones, further attract PCB-intensive manufacturing operations. The presence of semiconductor packaging and testing facilities also increases demand for substrate-level circuit boards used in chip packaging. Strong linkages with Japanese, American, and South Korean electronics firms provide technology transfer and advanced PCB manufacturing practices. Continuous capacity expansion by EMS firms in regions such as Calabarzon and Central Luzon reinforces local PCB sourcing. Growing global demand for connected devices and communication hardware manufactured in the Philippines sustains PCB production scale. As electronics exports remain the largest industrial sector, PCB demand maintains structural growth momentum across domestic manufacturing ecosystems.

Rising Adoption of High-Density and Flexible PCB Technologies in Telecommunications and Automotive Electronics:

Increasing technological complexity in communication equipment and vehicle electronics significantly drives demand for advanced printed circuit boards in the Philippines manufacturing sector. Telecom infrastructure devices such as routers, base stations, and broadband equipment require multilayer and high-frequency PCBs capable of supporting high-speed signal transmission and compact design architectures. Automotive electronics modules produced for export markets incorporate flexible and rigid-flex boards for sensors, control units, and infotainment systems, expanding technology requirements beyond conventional rigid boards. Electronics manufacturers operating in Philippine facilities increasingly adopt HDI and microvia PCB technologies to meet global product standards. Integration of 5G and connected vehicle electronics further accelerates transition toward high-density boards with fine-line circuitry and multilayer stacking. PCB suppliers within the country upgrade fabrication capabilities to align with these advanced design specifications. Demand for miniaturized electronic assemblies also increases use of flexible circuits in wearable and compact communication devices assembled locally. Export-focused production ensures adherence to stringent reliability and performance standards, reinforcing technology-driven PCB adoption. As telecommunications and automotive electronics manufacturing expands regionally, Philippine PCB demand continues shifting toward advanced board categories.

Market Challenges

Dependence on Imported Raw Materials and Advanced PCB Laminates

: The Philippines printed circuit board market faces structural challenges due to heavy reliance on imported copper laminates, specialty resins, and high-frequency substrate materials required for multilayer and flexible PCB production. Domestic fabrication facilities often depend on suppliers from Japan, Taiwan, and China for critical inputs, exposing manufacturers to supply disruptions and currency fluctuations. Limited local upstream material production constrains cost competitiveness compared with integrated PCB manufacturing countries. Import dependence also increases logistics lead times and inventory requirements for PCB producers operating within export manufacturing schedules. Fluctuations in global copper and laminate prices directly affect PCB production costs, reducing margin stability for local manufacturers. The absence of domestic advanced material manufacturing ecosystems limits capability expansion into high-end PCB categories such as IC substrates and high-frequency boards. Small-scale PCB fabricators face difficulty achieving economies of scale in raw material procurement. Global supply chain disruptions can delay electronics production timelines in Philippine EMS plants relying on PCB imports. This structural material dependency continues to constrain long-term competitiveness of domestic PCB fabrication operations.

Limited Domestic Advanced PCB Fabrication and Design Capabilities:

While the Philippines hosts significant PCB assembly and EMS operations, advanced multilayer and high-density PCB fabrication capacity remains relatively limited compared with regional manufacturing leaders. Many electronics manufacturers import high-complexity PCBs from neighboring countries with mature fabrication ecosystems, reducing local value addition. Domestic PCB producers often specialize in standard multilayer or assembly-level boards rather than cutting-edge HDI or IC substrate technologies. Insufficient investment in advanced fabrication equipment, microvia drilling, and fine-line lithography restricts capability expansion. Skilled workforce availability in high-precision PCB design and fabrication engineering also remains constrained. Research and development activity in advanced PCB materials and processes is limited within the domestic electronics sector. As global electronics shift toward miniaturized and high-density circuit architectures, capability gaps may widen. EMS firms operating in the Philippines often rely on overseas PCB suppliers for complex boards, reducing domestic manufacturing depth. Lack of integrated PCB clusters comparable to Taiwan or China limits innovation diffusion. These structural capability limitations challenge the Philippines in moving up the PCB value chain.

Opportunities

Localization of PCB Supply Chains within Export Electronics Manufacturing Zones:

The Philippines printed circuit board market has substantial opportunity to localize PCB fabrication near large electronics manufacturing services hubs concentrated in export processing zones. EMS companies operating major production facilities require stable and proximate PCB supply to reduce logistics costs, lead times, and inventory risks. Establishing local PCB fabrication plants integrated with EMS campuses would increase domestic value addition and manufacturing efficiency. Government industrial policies promoting electronics localization could attract investment in multilayer and flexible PCB production facilities. Integration of PCB fabrication with semiconductor packaging and assembly ecosystems would strengthen electronics clusters. Domestic PCB sourcing would enhance resilience against global supply chain disruptions affecting imported boards. Regional EMS firms may partner with international PCB manufacturers to establish joint ventures within Philippine industrial parks. Localization also supports technology transfer and workforce skill development in advanced PCB processes. Proximity to export assembly lines improves responsiveness to design modifications and production scaling. As electronics manufacturing output grows, localized PCB production presents significant expansion potential for domestic suppliers.

Development of High-Frequency and Automotive-Grade PCB Manufacturing for Export Markets:

Rising global demand for telecommunications infrastructure and automotive electronics creates opportunity for the Philippines to expand into high-frequency and automotive-grade PCB production segments. Telecom equipment assembled domestically requires RF and high-speed signal boards compliant with stringent performance standards, creating incentives for local fabrication upgrades. Automotive electronics modules manufactured for export markets require high-reliability PCBs capable of withstanding thermal and mechanical stress. Investments in advanced materials processing, multilayer stacking, and precision drilling technologies could enable Philippine manufacturers to enter these higher-value segments. Collaboration with Japanese and American electronics firms already operating in the country can accelerate capability development. Automotive supply chain integration within Southeast Asia further increases PCB demand for vehicle electronics. High-frequency PCB production also aligns with expanding 5G infrastructure equipment manufacturing. Establishing certification and testing facilities for automotive-grade boards would strengthen market positioning. Transition toward these advanced PCB categories would enhance export competitiveness and technological depth of the Philippine electronics sector. Long-term growth potential exists in supplying specialized PCBs to regional automotive and telecom manufacturers.

Future Outlook

The Philippines printed circuit board market is expected to expand steadily as electronics manufacturing services and semiconductor assembly sectors maintain strong export momentum. Increasing adoption of multilayer, flexible, and high-density PCBs in telecommunications and automotive electronics will drive technological upgrades in domestic fabrication. Government industrial policies supporting electronics localization and supply chain resilience are likely to encourage PCB investment. Integration with regional semiconductor and electronics ecosystems will strengthen demand and production capacity over the next five years.

Major Players

- IMI Printed Circuit Solutions

- Ionics EMS PCB Division

- Sumitronics Philippines

- Murata Electronics Philippines

- Amkor Technology Philippines

- Fujitsu Die-Tech Philippines

- Toshiba Information Equipment Philippines

- Nidec Philippines Electronics

- Samsung Electro-Mechanics Philippines

- Cirtek Electronics Corporation

- Onsemi Philippines PCB

- Nexperia Philippines PCB

- First Sumiden Circuits Philippines

- SunPower Electronics Manufacturing

- Philippine Circuit Technology Inc

Key Target Audience

- Electronics manufacturing services companies

- Semiconductor packaging firms

- Telecommunications equipment manufacturers

- Automotive electronics suppliers

- Industrial electronics OEMs

- Investments and venture capitalist firms

- Government and regulatory bodies

- PCB material and laminate suppliers

Research Methodology

Step 1: Identification of Key Variables

Market variables including PCB types, electronics manufacturing output, expore volumes, and technology adoption levels were identified from industry databases and electronics production statistics to define the Philippines printed circuit board market structure.

Step 2: Market Analysis and Construction

Supply chain mapping and manufacturing capacity analysis were conducted across Philippine electronics clusters to estimate PCB demand by product type and end-use industry segments within the domestic electronics ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from electronics manufacturing services firms and PCB suppliers validated demand patterns, technology trends, and competitive positioning assumptions relevant to the Philippines printed circuit board market.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized to produce segmentation, competitive landscape, and growth analysis reflecting current market dynamics and future outlook for the Philippines printed circuit board market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of electronics manufacturing hubs in economic zones

Rising demand for consumer electronics assembly in Southeast Asia

Growth in automotive electronics integration in regional supply chains

Increasing telecom infrastructure deployment and upgrades

Government incentives for semiconductor and electronics production - Market Challenges

Dependence on imported laminate and copper foil materials

Limited domestic advanced multilayer fabrication capability

Cost pressures from regional PCB manufacturing competitors

Workforce skill gaps in high-density PCB design and fabrication

Compliance costs with international electronics certification standards - Market Opportunities

Localization of PCB supply for EMS exporters

Adoption of high-frequency PCBs for 5G equipment production

Integration into global automotive electronics supply chains - Trends

Shift toward high-density interconnect and miniaturized boards

Increasing use of flexible and rigid-flex PCBs in devices

Automation of PCB assembly and inspection processes

Adoption of halogen-free and environmentally compliant materials

Collaboration with global EMS firms for export manufacturing - Government Regulations & Defense Policy

Electronics industry development incentives under national programs

Environmental compliance for PCB chemical processing and waste

Standards alignment with international electronics certification - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Single-Sided Printed Circuit Boards

Double-Sided Printed Circuit Boards

Multilayer Printed Circuit Boards

Flexible Printed Circuit Boards

Rigid-Flex Printed Circuit Boards - By Platform Type (In Value%)

Consumer Electronics Devices

Automotive Electronics Systems

Industrial Control Equipment

Telecommunications Infrastructure

Medical Electronic Devices - By Fitment Type (In Value%)

Surface Mount Technology Boards

Through-Hole Technology Boards

Embedded Component Boards

High-Density Interconnect Boards

Hybrid Assembly Boards - By EndUser Segment (In Value%)

Electronics Manufacturing Services Providers

Automotive Component Manufacturers

Telecom Equipment Manufacturers

Medical Device Manufacturers

Industrial Automation OEMs - By Procurement Channel (In Value%)

Direct OEM Procurement

Contract Manufacturing Sourcing

Electronics Component Distributors

Global Sourcing Platforms

Local PCB Fabrication Vendors - By Material / Technology (in Value %)

FR-4 Epoxy Glass Laminates

Polyimide Flexible Substrates

High-Frequency PTFE Laminates

Metal-Core Substrates

Halogen-Free Laminates

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (PCB Layer Count Capability, Substrate Material Range, HDI Technology Support, Production Capacity Scale, End-Use Industry Focus, Quality Certifications, Export Orientation, Design Support Services, Lead Time Performance, Cost Competitiveness)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

IMI Printed Circuit Solutions

Ionics EMS PCB Division

Fujitsu Die-Tech Philippines

Sumitronics Philippines PCB

Nidec Philippines Electronics

Philippine Circuit Technology Inc

Cirtek Electronics PCB Unit

Toshiba Information Equipment PCB

Samsung Electro-Mechanics Philippines

Murata Electronics Philippines

Amkor Technology Philippines Substrates

SunPower Electronics PCB

First Sumiden Circuits Philippines

Nexperia Philippines PCB

Onsemi Philippines PCB Solutions

- Electronics manufacturing services firms drive volume PCB demand

- Telecom equipment assembly increases multilayer PCB adoption

- Automotive electronics integration raises reliability requirements

- Medical device producers require precision and certified PCBs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now