Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Propeller Shafts market is valued at approximately USD ~ billion based on a recent historical assessment, supported by increasing automotive production and aftermarket replacement demand. Growth is driven by expansion in logistics fleets, rising commercial vehicle usage, and ongoing infrastructure development projects. The steady increase in vehicle parc and aging fleet conditions contributes significantly to recurring demand for replacement propeller shafts across passenger and commercial segments.

Metro Manila, Cebu, and Davao dominate the Philippines Propeller Shafts market due to their concentration of automotive assembly units, logistics operations, and aftermarket service networks. These regions benefit from better infrastructure, higher vehicle density, and stronger supply chain connectivity. Additionally, industrial clusters and port proximity enable efficient distribution and import of components, reinforcing their leadership in demand and servicing of drivetrain components across various vehicle categories.

Market Segmentation

By Product Type

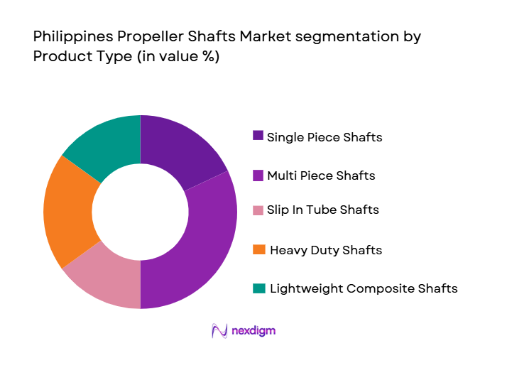

Philippines Propeller Shafts market is segmented by product type into single piece shafts, multi piece shafts, slip in tube shafts, heavy duty shafts, and lightweight composite shafts. Recently, multi piece shafts have a dominant market share due to their widespread application in commercial vehicles and heavy-duty operations. These shafts provide flexibility, better torque handling, and improved alignment for longer vehicles, making them suitable for logistics and construction fleets. Increasing freight movement and infrastructure activities have boosted demand for such vehicles, thereby strengthening adoption. Their cost-effectiveness compared to composite alternatives and compatibility with existing vehicle architectures further support their dominance. Additionally, ease of maintenance and availability of replacement components contribute to sustained demand across both OEM and aftermarket channels.

By Vehicle Type

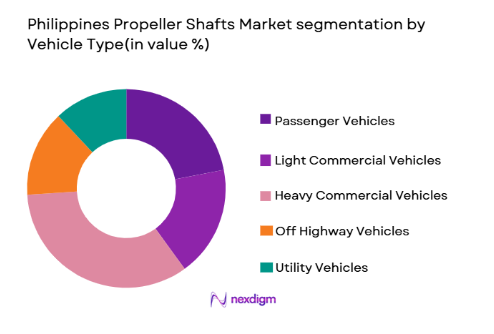

Philippines Propeller Shafts market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, off highway vehicles, and utility vehicles. Recently, heavy commercial vehicles have a dominant market share due to strong demand from logistics, construction, and mining sectors. The increasing movement of goods across islands and infrastructure expansion projects drive consistent utilization of heavy trucks and trailers. These vehicles require robust drivetrain systems capable of handling high loads and long operational hours, leading to higher consumption of propeller shafts. Frequent wear and tear in demanding conditions also accelerates replacement demand. Additionally, government-backed infrastructure initiatives and port development further support heavy vehicle usage, reinforcing their dominance in the propeller shafts market ecosystem.

Competitive Landscape

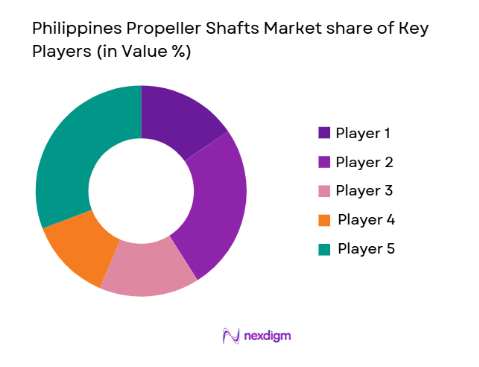

The Philippines Propeller Shafts market is moderately consolidated with a mix of global drivetrain manufacturers and regional suppliers competing across OEM and aftermarket segments. Major players leverage technological expertise, distribution networks, and partnerships with automotive manufacturers to strengthen their presence. Competitive intensity is driven by pricing strategies, product durability, and aftermarket service capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Manufacturing Capability |

| GKN Automotive | 1759 | UK | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

| American Axle & Manufacturing | 1994 | USA | ~ | ~ | ~ | ~ | ~ |

| NTN Corporation | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

| JTEKT Corporation | 2006 | Japan | ~ | ~ | ~ | ~ | ~ |

Philippines Propeller Shafts Market Analysis

Growth Drivers

Expansion of Logistics and Freight Transportation Sector:

rapid growth of e-commerce and inter-island trade has significantly increased the demand for commercial vehicles, directly influencing the consumption of propeller shafts. Logistics companies are expanding their fleets to meet delivery timelines and improve operational efficiency, resulting in higher demand for durable drivetrain components. The need for reliable transportation across varying terrains increases wear on propeller shafts, driving replacement cycles. Continuous infrastructure development such as highways and ports enhances connectivity, further supporting freight movement. Fleet operators prioritize maintenance and component upgrades to ensure minimal downtime. Additionally, government initiatives to boost trade and transport infrastructure indirectly support vehicle usage. The increased operational hours of commercial vehicles amplify demand for high-performance shafts. OEM partnerships with logistics firms also drive consistent supply of components. Overall, the expanding logistics ecosystem creates sustained demand for propeller shafts across both new and replacement markets.

Rising Vehicle Parc and Aftermarket Replacement Demand:

Increasing number of vehicles on the road contributes significantly to aftermarket demand for propeller shafts. Aging vehicles require frequent maintenance and component replacement due to wear and fatigue in drivetrain systems. Propeller shafts, being critical for power transmission, experience stress under continuous use, leading to higher replacement frequency. The growth of independent service centers enhances accessibility to replacement components. Consumers are increasingly opting for cost-effective aftermarket solutions instead of new vehicle purchases. Availability of refurbished and remanufactured shafts further supports market expansion. Additionally, rising awareness about vehicle maintenance improves replacement cycles. Fleet operators prioritize preventive maintenance to avoid operational disruptions. Technological advancements in materials also encourage upgrades. This combination of aging fleet and maintenance awareness drives consistent aftermarket demand.

Market Challenges

Dependence on Imported Raw Materials and Components:

The Philippines Propeller Shafts market heavily relies on imported steel alloys and advanced materials required for manufacturing high-performance shafts. This dependency exposes the market to global price fluctuations and supply chain disruptions. Currency volatility can further increase procurement costs, impacting pricing strategies for manufacturers. Limited domestic production capabilities restrict local value addition. Import delays and logistics bottlenecks can disrupt production timelines. Manufacturers face challenges in maintaining competitive pricing while ensuring quality standards. Smaller players are particularly affected due to limited financial resilience. Additionally, geopolitical factors can influence trade routes and supply stability. The absence of strong local supplier ecosystems adds to operational complexity. These factors collectively hinder market growth and profitability.

Limited Adoption of Advanced Lightweight Materials:

While global markets are shifting toward lightweight composite propeller shafts, adoption in the Philippines remains limited due to cost constraints and technological barriers. Composite materials offer improved efficiency and reduced vehicle weight, but higher production costs deter widespread use. OEMs often prioritize affordability over advanced material integration in cost-sensitive markets. Lack of local expertise in composite manufacturing further slows adoption. Infrastructure limitations also restrict advanced production processes. Consumers and fleet operators may not fully recognize long-term benefits of lightweight shafts. Additionally, compatibility issues with existing vehicle platforms can limit retrofitting opportunities. Supply chain gaps for composite materials add complexity. As a result, traditional steel shafts continue to dominate despite technological advancements. This limits innovation-driven growth in the market.

Opportunities

Adoption of Lightweight Composite Propeller Shafts in Fuel Efficient Vehicles:

The growing focus on fuel efficiency and emission reduction presents significant opportunities for composite propeller shafts. Lightweight materials reduce vehicle weight, improving fuel economy and performance. Automotive manufacturers are gradually exploring composite integration in new vehicle designs. Increased awareness of environmental benefits supports adoption trends. Government initiatives promoting fuel efficiency can further accelerate demand. Technological advancements are gradually reducing production costs of composites. Collaboration between global manufacturers and local suppliers can enhance knowledge transfer. Fleet operators may adopt composite shafts for long-term operational savings. Electric vehicles also require lightweight components, creating additional demand. This shift toward efficiency-driven design opens new growth avenues.

Expansion of Local Manufacturing and Aftermarket Service Networks:

Strengthening domestic manufacturing capabilities can reduce dependence on imports and improve supply chain resilience. Investment in local production facilities can enhance cost competitiveness and reduce lead times. The growing network of aftermarket service providers increases accessibility to replacement components. Partnerships between global players and local firms can facilitate technology transfer. Government support for industrial development can encourage investment in automotive component manufacturing. Expansion of regional service centers improves market penetration. Local production can also cater to customization needs for specific vehicle segments. Additionally, increased employment opportunities support economic growth. Enhanced distribution networks ensure timely availability of components. This creates a robust ecosystem for sustainable market expansion.

Future Outlook

The Philippines Propeller Shafts market is expected to experience steady growth driven by expanding logistics operations and increasing vehicle ownership. Technological advancements in materials and manufacturing processes will enhance product durability and efficiency. Regulatory focus on vehicle performance and emissions will encourage adoption of advanced components. Growing infrastructure investments and regional connectivity improvements will further support demand. The market is likely to benefit from both OEM expansion and aftermarket replacement cycles over the coming years.

Major Players

- GKN Automotive Philippines

- Dana Incorporated Philippines

- American Axle Philippines

- NTN Philippines

- JTEKT Philippines

- Hyundai WIA Philippines

- ZF Philippines

- Schaeffler Philippines

- Neapco Philippines

- Meritor Philippines

- Showa Corporation Philippines

- Mitsubishi Steel Philippines

- Toyota Boshoku Philippines

- Bharat Forge Philippines

- Denso Philippines

Key Target Audience

- Automotive OEM manufacturers

- Automotivecomponent distributors

- Fleet operators

- Logistics companies

- Construction companies

- Mining companies

- Government and regulatory bodies

- Investment firms

Research Methodology

Step 1: Identification of Key Variables

Primary and secondary research was conducted to identify key demand drivers, supply chain factors, and technological trends influencing the Philippines Propeller Shafts market. Data points were validated through industry databases and expert inputs.

Step 2: Market Analysis and Construction

Market size estimation involved analysis of vehicle production, aftermarket demand, and component pricing. Segmentation was developed based on product type and vehicle category using structured analytical frameworks.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, including manufacturers and distributors, were consulted to validate assumptions and refine market estimates. Feedback was incorporated to ensure accuracy and reliability of findings.

Step 4: Research Synthesis and Final Output

All data points were consolidated and analyzed to generate insights, trends, and forecasts. The final report was structured to provide actionable intelligence and comprehensive market understanding.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising commercial vehicle demand driven by logistics sector expansion

Increasing infrastructure development projects boosting heavy vehicle usage

Growth in vehicle parc leading to higher replacement demand - Market Challenges

High dependency on imported raw materials impacting cost stability

Limited local manufacturing capabilities for advanced shaft technologies

Wear and tear issues in harsh operating environments affecting lifecycle - Market Opportunities

Expansion of lightweight composite shaft adoption in fuel efficient vehicles

Growth in aftermarket servicing networks across regional markets

Integration of advanced manufacturing technologies for precision components - Trends

Shift toward lightweight materials to improve fuel efficiency

Increasing adoption of modular shaft designs for easier maintenance

Growth in demand for corrosion resistant coatings in coastal regions

Technological advancements in vibration reduction and balancing

Expansion of electric commercial vehicles influencing shaft design - Government Regulations & Defense Policy

Vehicle safety and emission compliance standards enforcement

Import regulations impacting automotive component sourcing

Infrastructure development policies supporting transport sector growth - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Single Piece Propeller Shafts

Multi Piece Propeller Shafts

Slip In Tube Propeller Shafts

Heavy Duty Reinforced Shafts

Lightweight Composite Shafts - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off Highway Vehicles

Specialty Utility Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

Performance Upgrade Fitment

Remanufactured Fitment

Custom Engineered Fitment - By EndUser Segment (In Value%)

Automotive Manufacturers

Fleet Operators

Logistics and Transportation Companies

Construction and Mining Operators

Automotive Aftermarket Service Providers - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Distributors

Independent Aftermarket Suppliers

Online Automotive Platforms

Fleet Procurement Agreements - By Material / Technology (in Value %)

Steel Alloy Shafts

Aluminum Shafts

Carbon Fiber Composite Shafts

Hybrid Metal Composite Shafts

Advanced Corrosion Resistant Coated Shafts

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Durability, Material Composition, Load Capacity, Cost Efficiency, Manufacturing Capability, Distribution Network, Aftermarket Support, Technological Innovation, Customization Capability, Supply Chain Strength)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

GKN Automotive Philippines

AAM Philippines Driveline Systems

Dana Incorporated Philippines

NTN Corporation Philippines

JTEKT Philippines Corporation

Hyundai WIA Philippines

Mitsubishi Steel Manufacturing Philippines

Toyota Boshoku Philippines Driveline Division

ZF Asia Pacific Philippines

Schaeffler Philippines Driveline Systems

Neapco Asia Philippines

Meritor Philippines Inc

Showa Corporation Philippines

American Axle Asia Philippines

Bharat Forge Philippines Drivetrain Components

- Increasing demand from logistics fleets for durable and high performance shafts

- Rising preference among OEMs for lightweight and efficient drivetrain components

- Growth in aftermarket demand due to aging vehicle population

- Adoption of advanced shaft technologies by construction and mining operators

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now