Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Renal SPECT Equipment market size is significantly influenced by the increasing demand for non-invasive diagnostic technologies in healthcare. Based on a recent historical assessment, the market for Renal SPECT equipment is expected to be valued at over USD ~ million, driven by advancements in imaging technology, an increase in renal disease diagnoses, and a growing preference for precise diagnostic methods. The market is expected to experience continued growth, with key contributors being improved healthcare infrastructure and a rise in medical imaging capabilities across the country.

Several regions in the Philippines show strong adoption of Renal SPECT equipment, particularly in metro areas like Metro Manila, Cebu, and Davao, where healthcare facilities are well-equipped with advanced diagnostic tools. The dominance of these regions is attributed to the concentration of well-established hospitals and diagnostic centers, a high volume of renal disease cases, and better access to healthcare funding. Moreover, government and private sector investments in modernizing medical infrastructure have further spurred the demand for advanced imaging solutions in these key areas.

Market Segmentation

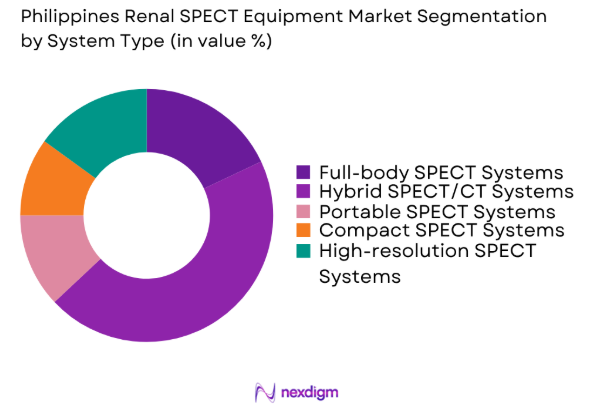

By System Type

The market for Philippines Renal SPECT Equipment is segmented into full-body SPECT systems, hybrid SPECT/CT systems, portable SPECT systems, compact SPECT systems, and high-resolution SPECT systems. The hybrid SPECT/CT system sub-segment has emerged as the dominant segment due to its high diagnostic accuracy and efficiency in detecting renal conditions in patients. The integration of SPECT with CT enhances both anatomical and functional imaging, making it an ideal solution for complex renal diagnostics. Hospitals and diagnostic centers increasingly adopt hybrid systems because of their versatility, precision, and improved patient outcomes, which drives this segment’s dominance.

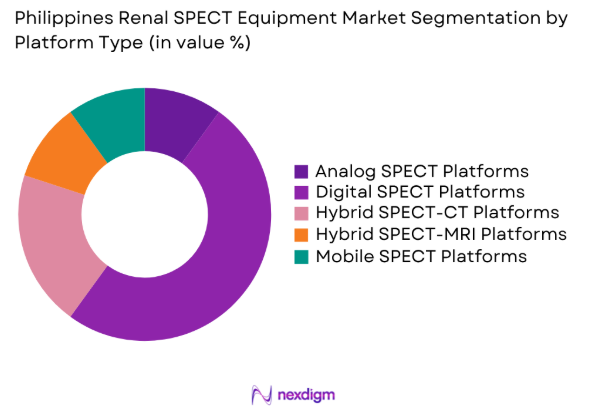

By Platform Type

The Philippines Renal SPECT Equipment market is also segmented by platform type into analog SPECT platforms, digital SPECT platforms, hybrid SPECT-CT platforms, hybrid SPECT-MRI platforms, and mobile SPECT platforms. The digital SPECT platform sub-segment is the dominant segment in this market due to the increasing shift towards digital imaging solutions, which offer superior image quality and quicker processing times compared to their analog counterparts. These platforms also integrate advanced data analysis tools that enhance diagnostic accuracy and facilitate improved patient management. Digital SPECT platforms are widely adopted due to the demand for faster, more reliable imaging solutions.

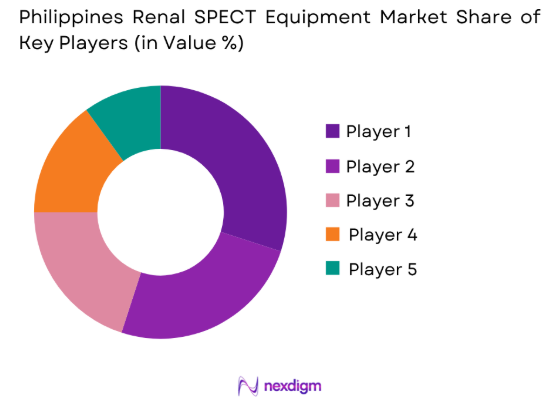

Competitive Landscape

The competitive landscape of the Philippines Renal SPECT equipment market is characterized by the presence of both global medical imaging giants and regional players, leading to intense competition. Consolidation is evident, with larger companies expanding their presence through strategic partnerships, acquisitions, and product innovations. Major players dominate the market, leveraging their advanced technology, comprehensive service offerings, and established distribution networks to maintain a competitive edge.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| GE Healthcare | 1892 | Chicago, IL, USA | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, NL | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, DE | ~ | ~ | ~ | ~ | ~ |

| Canon Medical Systems | 1933 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

| Fujifilm Healthcare | 1934 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ |

Philippines Renal SPECT Equipment Market Analysis

Growth Drivers

Technological Advancements in Imaging Technology

The continuous advancement in medical imaging technology, particularly in SPECT systems, is a major growth driver for the Renal SPECT equipment market. The development of hybrid SPECT/CT and SPECT/MRI systems allows healthcare providers to obtain detailed anatomical and functional data, which significantly enhances diagnostic accuracy. These advancements have enabled the detection of early-stage renal diseases, driving the adoption of SPECT equipment in diagnostic centers and hospitals. Additionally, the increased integration of artificial intelligence (AI) in imaging technology is improving data analysis, enabling better decision-making for clinicians. This increased technology adoption is accelerating the growth of the market as it leads to more precise, efficient, and cost-effective diagnostic procedures.

Increasing Prevalence of Renal Diseases

The rising incidence of renal diseases in the Philippines is another key driver fueling the growth of the Renal SPECT equipment market. Chronic kidney disease (CKD) and acute renal conditions are becoming more prevalent, leading to a higher demand for accurate diagnostic tools to monitor and diagnose renal diseases. According to healthcare data, the burden of kidney diseases is increasing, and the need for early diagnosis is becoming more critical. SPECT imaging is especially valuable in assessing renal function and detecting abnormalities, making it a preferred technology for renal diagnosis. As more people seek medical attention for renal-related issues, the market for Renal SPECT equipment is poised to expand.

Market Challenges

High Cost of SPECT Equipment

The high initial cost of SPECT systems is a major challenge in the Philippines market, particularly for healthcare facilities in developing regions. Budget constraints make it difficult for smaller hospitals and diagnostic centers to invest in expensive imaging equipment. While the long-term benefits of accurate diagnoses and treatment planning are clear, the high upfront costs and ongoing maintenance can deter these facilities from adopting SPECT systems. Additionally, the high cost of skilled labor needed to operate these advanced systems exacerbates the problem, further limiting adoption in certain healthcare settings. This financial barrier remains a significant obstacle for broader use of Renal SPECT technology in the country.

Limited Skilled Workforce in Medical Imaging

A shortage of skilled radiologists and technicians to operate advanced imaging equipment, including Renal SPECT systems, is another challenge for the Philippines market. Despite the growing availability of SPECT technology, healthcare facilities often struggle to find qualified personnel capable of operating these complex systems effectively. Specialized training in medical imaging techniques and SPECT systems is crucial to ensuring accurate diagnoses. As the demand for SPECT imaging continues to rise, the shortage of skilled labor presents a significant barrier to widespread adoption. Addressing this challenge requires focused workforce training and development initiatives to equip healthcare professionals with the necessary expertise to operate advanced diagnostic systems efficiently.

Opportunities

Government Initiatives for Healthcare Upgradation

The Philippine government’s focus on enhancing healthcare infrastructure, particularly in underserved regions, creates a significant opportunity for the Renal SPECT equipment market. Initiatives like the Philippine Health Facility Development Plan aim to strengthen the capacity of hospitals and diagnostic centers nationwide, driving demand for advanced medical imaging technologies. These efforts present opportunities for both local and international companies to enter the market with customized solutions. As the government invests in upgrading healthcare facilities, the Renal SPECT equipment sector is poised for growth, with increased adoption of advanced diagnostic tools to meet the rising demand for accurate renal disease diagnoses across the country.

Expanding Medical Tourism in the Philippines

The growth of medical tourism in the Philippines offers a significant opportunity for the Renal SPECT equipment market. As the country becomes a key destination for medical tourism, particularly in diagnostics and renal care, the demand for advanced imaging equipment is expected to rise. Medical tourists frequently seek high-quality diagnostic procedures, including SPECT imaging, which drives the adoption of Renal SPECT systems. This trend creates a promising opportunity for both local and international companies to expand their presence in the market. The increasing influx of medical tourists presents a chance to boost sales of diagnostic imaging products, further supporting the growth of the Renal SPECT equipment market in the Philippines.

Future Outlook

The Philippines Renal SPECT Equipment market is set to witness substantial growth over the next five years, driven by technological innovations, increasing healthcare investments, and rising demand for accurate renal disease diagnostics. Advancements in hybrid imaging technologies, such as SPECT/CT and SPECT/MRI, will continue to enhance diagnostic precision and attract more healthcare facilities to invest in these systems. Additionally, government policies aimed at strengthening healthcare infrastructure and improving access to advanced medical technologies will further boost market growth. Increased awareness of renal diseases and greater emphasis on early diagnosis will continue to drive the adoption of Renal SPECT equipment, ensuring a positive outlook for the market.

Major Players

- GE Healthcare

- Philips Healthcare

- Siemens Healthineers

- Canon Medical Systems

- Fujifilm Healthcare

- Shimadzu Corporation

- Hologic

- Samsung Medison

- Hitachi Medical Systems

- Carestream Health

- Mindray Medical International

- Esaote

- NeusoftMedical Systems

- United Imaging Healthcare

- Analogic Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals and healthcare providers

- Diagnostic imagingcenters

- Renal healthcare clinics

- Medical equipment distributors

- Health insurers

- Healthcare IT solution providers

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the key variables that influence the market dynamics, including technological advancements, healthcare infrastructure, and regulatory factors. These variables are critical in understanding market trends and demand drivers.

Step 2: Market Analysis and Construction

In this step, we analyze the market size, segment performance, and competitive landscape. This analysis includes evaluating historical trends, market drivers, and key technological innovations that impact the Renal SPECT equipment market.

Step 3: Hypothesis Validation and Expert Consultation

To validate the findings, expert consultations and feedback from industry leaders, healthcare professionals, and technology providers are conducted. These insights help refine the market forecast and address any potential gaps.

Step 4: Research Synthesis and Final Output

Finally, all data collected is synthesized to create a comprehensive report, offering a clear and actionable overview of the market. This step ensures the findings align with industry expectations and market trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Technological Advancements in Imaging Technology

Increasing Prevalence of Renal Diseases

Growing Demand for Non-invasive Diagnostic Methods - Market Challenges

High Cost of SPECT Equipment

Limited Skilled Healthcare Workforce

Regulatory and Certification Hurdles - Market Opportunities

Expansion of Healthcare Infrastructure in Emerging Areas

Government Initiatives for Healthcare Upgradation

Rising Trend of Home Healthcare Solutions - Trends

Shift Towards Hybrid Imaging Solutions (SPECT/CT, SPECT/MRI)

Increased Adoption of Portable and Compact SPECT Systems

Integration of AI and Machine Learning in Imaging Systems - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Full-body SPECT Systems

Hybrid SPECT/CT Systems

Portable SPECT Systems

Compact SPECT Systems

High-resolution SPECT Systems - By Platform Type (In Value%)

Analog SPECT Platforms

Digital SPECT Platforms

Hybrid SPECT-CT Platforms

Hybrid SPECT-MRI Platforms

Mobile SPECT Platforms - By Fitment Type (In Value%)

Ceiling-mounted SPECT Systems

Floor-mounted SPECT Systems

Wall-mounted SPECT Systems

Compact/Modular Fitment SPECT Systems

Portable Fitment SPECT Systems - By End User Segment (In Value%)

Hospitals

Diagnostic Imaging Centers

Research and Academic Institutions

Ambulatory Surgical Centers

Private Clinics - By Procurement Channel (In Value%)

Direct Procurement from Manufacturers

Third-party Procurement through Distributors

Online Procurement Platforms

Government Tendering & Procurement

Leasing & Financing Options

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Technology, Market Value, Regional Adoption, Procurement Model, Pricing Strategy, Installed Base, Brand Reputation, Regulatory Compliance, Technological Innovation)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

GE Healthcare

Philips Healthcare

Siemens Healthineers

Canon Medical Systems

Shimadzu Medical Systems

Fujifilm Healthcare

Samsung Medison

Hologic

Carestream Health

Hitachi Medical Systems

Mindray Medical International

Esaote

Neusoft Medical Systems

United Imaging Healthcare

Analogic Corporation

- High demand from government-run hospitals

- Increasing investment from private hospitals

- Growth of diagnostic imaging centers in urban and rural areas

- Expansion of specialized renal healthcare clinics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now