Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines semiconductor infrastructure market forms a core part of the national electronics manufacturing and semiconductor assembly ecosystem, valued at approximately USD ~ billion based on a recent historical assessment of semiconductor facilities, packaging plants, and supporting infrastructure. Growth is driven by global semiconductor outsourcing, OSAT expansion, and electronics export manufacturing across automotive, consumer electronics, and industrial components. Investments in advanced packaging lines, wafer probing, and semiconductor test facilities are strengthening domestic semiconductor production capabilities.

Calabarzon, particularly Laguna and Cavite, dominates semiconductor infrastructure concentration due to established electronics manufacturing zones, export processing facilities, and proximity to Metro Manila logistics and ports. Cebu hosts significant semiconductor assembly and test operations supported by export-oriented manufacturing clusters and skilled technical workforce availability. The Philippines is integrated within East Asian semiconductor supply chains led by Taiwan, South Korea, and Japan, positioning the country as a key backend manufacturing and packaging hub in global semiconductor production networks.

Market Segmentation

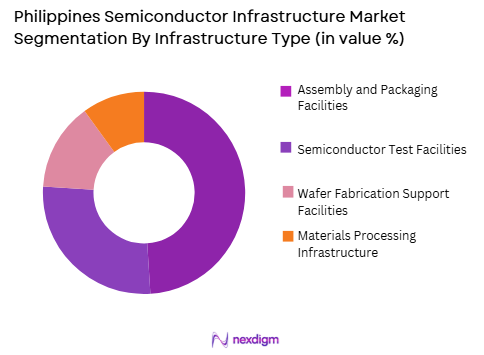

By Infrastructure Type

Philippines Semiconductor Infrastructure market is segmented by infrastructure type into assembly and packaging facilities, wafer fabrication support facilities, semiconductor test facilities, and materials processing infrastructure. Recently, assembly and packaging facilities has a dominant market share due to factors such as strong OSAT industry presence, export-oriented semiconductor manufacturing, and global outsourcing of backend semiconductor processes. The Philippines hosts numerous multinational semiconductor firms specializing in packaging and assembly operations serving global electronics supply chains. Lower labor costs, skilled technicians, and established industrial parks support expansion of assembly and packaging infrastructure. Wafer fabrication presence remains limited domestically, reinforcing dominance of backend processing infrastructure in the semiconductor ecosystem.

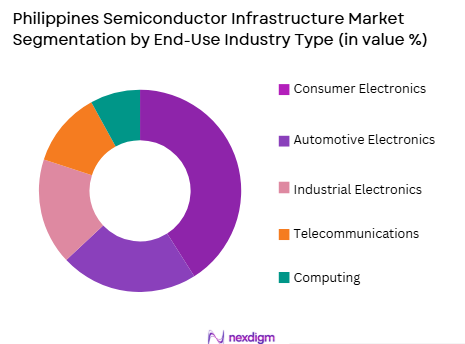

By End-Use Industry

Philippines Semiconductor Infrastructure market is segmented by end-use industry into consumer electronics, automotive electronics, industrial electronics, telecommunications, and computing. Recently, consumer electronics has a dominant market share due to factors such as global demand for mobile devices, computing peripherals, and household electronics assembled using Philippine semiconductor packaging and test services. Semiconductor firms in the Philippines primarily serve multinational electronics manufacturers supplying consumer products. High-volume production cycles and stable export demand sustain infrastructure utilization in this segment. Automotive and industrial electronics segments are expanding but remain smaller compared to consumer-driven semiconductor manufacturing demand across Philippine facilities.

Competitive Landscape

The Philippines semiconductor infrastructure market is characterized by strong presence of multinational semiconductor assembly and test companies operating export-oriented facilities within industrial zones. Market concentration is high in backend semiconductor services, with global OSAT leaders controlling major packaging and test capacity. Domestic firms participate mainly in materials, equipment support, and subcontracting roles. Competition centers on advanced packaging capability, automation level, yield efficiency, and global supply chain integration with electronics manufacturers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Infrastructure Specialization |

| Amkor Technology | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| ASE Technology | 1984 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | USA | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| ON Semiconductor | 1999 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Semiconductor Infrastructure Market Analysis

Growth Drivers

Global Outsourcing of Semiconductor Assembly and Packaging to the Philippines

The Philippines has become a strategic global destination for outsourced semiconductor assembly and packaging operations as multinational semiconductor companies seek cost-efficient, scalable backend manufacturing capacity within established electronics ecosystems. The country offers a mature OSAT environment with decades of operational experience, skilled labor, and export-oriented industrial zones supporting high-volume semiconductor production. Global chip manufacturers increasingly externalize backend processes such as packaging, wire bonding, and testing to specialized facilities in Southeast Asia to optimize capital allocation and focus on wafer fabrication and design. Philippine semiconductor infrastructure benefits from strong integration with international electronics supply chains serving consumer, automotive, and industrial markets. Established logistics connectivity and proximity to Asian semiconductor hubs enable efficient material flow and component distribution. Continuous expansion of advanced packaging technologies such as system-in-package and flip-chip requires facility upgrades and new infrastructure investment. Competitive labor and operational costs sustain attractiveness relative to developed markets. Government incentives for electronics manufacturing encourage facility expansion and modernization. Automation and smart manufacturing integration in packaging plants further increase capacity and efficiency. As global semiconductor demand expands across digital technologies, outsourcing to Philippine infrastructure continues to accelerate sector growth.

Expansion of Electronics Export Manufacturing and Semiconductor Demand

The Philippines electronics sector remains a major contributor to national exports, driving sustained demand for semiconductor assembly, packaging, and testing infrastructure supporting production of integrated circuits used in global electronic devices. Consumer electronics, computing equipment, telecommunications hardware, and industrial systems rely on semiconductors processed in Philippine facilities before integration into finished products. Rising global consumption of connected devices, automotive electronics, and industrial automation components increases throughput requirements for semiconductor backend infrastructure. Electronics manufacturing clusters in Calabarzon and Cebu create localized demand for semiconductor processing facilities within integrated supply chains. Export-oriented production necessitates scalable and reliable semiconductor infrastructure capable of high-volume output. International electronics firms operating in the Philippines require local packaging and test capacity to reduce logistics complexity and production lead times. Increasing semiconductor content per device amplifies infrastructure utilization across industries. Advanced packaging requirements for miniaturized electronics drive technology upgrades in domestic facilities. Supply chain diversification strategies among global manufacturers favor Southeast Asian production bases including the Philippines. Continued expansion of electronics manufacturing output ensures long-term growth in semiconductor infrastructure demand nationwide.

Market Challenges

Absence of Domestic Wafer Fabrication and Frontend Semiconductor Capability

The Philippines semiconductor infrastructure ecosystem is heavily concentrated in backend assembly and test operations with minimal domestic wafer fabrication capability, creating structural limitations in value chain integration and technological advancement. Dependence on imported semiconductor wafers from fabrication hubs such as Taiwan and South Korea restricts domestic industry control over upstream production processes. Lack of advanced fabrication facilities limits participation in high-value semiconductor manufacturing segments and advanced node technologies. Backend-focused infrastructure constrains technology transfer and innovation opportunities compared to integrated semiconductor ecosystems. Global semiconductor firms maintain fabrication operations in technologically advanced countries, leaving the Philippines positioned primarily as a packaging and test location. Absence of fabrication investment reduces incentives for advanced materials and equipment ecosystems to develop locally. Skilled workforce specialization remains concentrated in backend processes rather than wafer engineering. High capital requirements and technological complexity deter domestic fabrication initiatives. National semiconductor competitiveness remains tied to global supply chain decisions. This structural gap restricts expansion into higher value semiconductor manufacturing activities.

Vulnerability to Global Semiconductor Cycles and External Demand Fluctuations

The Philippines semiconductor infrastructure market is highly exposed to global electronics demand cycles and semiconductor industry fluctuations due to its export-oriented production model and reliance on multinational client demand. Semiconductor packaging and test facilities operate according to global electronics production volumes rather than domestic consumption patterns. Economic downturns, consumer electronics demand contractions, or technology transitions can rapidly affect facility utilization and revenue stability. Concentration in specific product segments such as consumer electronics amplifies cyclical exposure. Global semiconductor oversupply or inventory corrections reduce outsourcing demand impacting Philippine infrastructure operations. Dependence on multinational corporations for facility investment decisions limits domestic strategic control. Exchange rate volatility influences export competitiveness and operational costs. Supply chain disruptions or geopolitical tensions affecting semiconductor trade directly impact infrastructure activity. Limited diversification into domestic semiconductor markets increases vulnerability. Industry employment and investment levels fluctuate with global semiconductor cycles. These external dependencies create structural volatility in the Philippines semiconductor infrastructure sector.

Opportunities

Development of Advanced Packaging and Heterogeneous Integration Capabilities

The global semiconductor industry is transitioning toward advanced packaging technologies such as system-in-package, chiplet integration, and heterogeneous assembly to improve performance and miniaturization, creating significant opportunities for Philippine semiconductor infrastructure expansion. Advanced packaging processes require specialized facilities, precision equipment, and skilled workforce capabilities aligned with the Philippines’ existing backend expertise. Multinational semiconductor firms are upgrading packaging plants in Southeast Asia to support next-generation semiconductor architectures. Philippine facilities can evolve from traditional packaging to advanced integration technologies supporting AI, automotive, and high-performance computing chips. Investments in automation, precision assembly, and materials processing infrastructure enable advanced packaging capability development. Training programs and technical education expansion can support workforce transition toward higher complexity processes. Advanced packaging commands higher value and margins compared to conventional assembly. Regional semiconductor ecosystem partnerships facilitate technology transfer. Growing demand for compact and integrated semiconductor solutions across industries supports facility modernization. Transition to advanced packaging positions the Philippines for higher-value participation in global semiconductor manufacturing.

Strengthening Role in Regional Semiconductor Supply Chain Diversification

Global semiconductor manufacturers are diversifying supply chains across Southeast Asia to reduce concentration risk and geopolitical exposure, creating strategic opportunities for expanded semiconductor infrastructure investment in the Philippines. Companies seek geographically distributed backend processing capacity complementing fabrication hubs in East Asia. The Philippines offers stable manufacturing environment, established electronics clusters, and export-oriented industrial zones attractive for diversification. Government investment promotion programs encourage semiconductor infrastructure expansion. Regional trade agreements facilitate integration with Asian semiconductor supply chains. Infrastructure upgrades in logistics, power, and industrial parks enhance investment attractiveness. Diversification strategies require new packaging, test, and materials facilities across multiple countries. Philippine workforce expertise in semiconductor processes supports rapid capacity expansion. Foreign direct investment inflows into electronics manufacturing stimulate infrastructure growth. As global semiconductor firms pursue multi-country production networks, the Philippines can strengthen its position as a key backend manufacturing node in regional semiconductor ecosystems.

Future Outlook

The Philippines semiconductor infrastructure market is expected to expand steadily as global semiconductor outsourcing and electronics manufacturing demand continue rising. Advanced packaging technology adoption will drive facility modernization and capacity upgrades. Regional supply chain diversification strategies will increase foreign investment in semiconductor infrastructure. Government support for electronics manufacturing and industrial zones will strengthen sector growth. The Philippines will remain a critical backend semiconductor hub within Southeast Asia production networks.

Major Players

- Amkor Technology

- ASE Technology

- Texas Instruments

- STMicroelectronics

- ON Semiconductor

- NXP Semiconductors

- Analog Devices

- Infineon Technologies

- Renesas Electronics

- Toshiba Electronic Devices

- ROHM Semiconductor

- Microchip Technology

- Maxim Integrated

- Broadcom

- Qualcomm

Key Target Audience

- Semiconductor manufacturers

- Electronics manufacturing firms

- Automotive electronics companies

- Telecommunications equipment firms

- Industrial automation companies

- Data center hardware firms

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Semiconductor facility capacity, packaging technology level, electronics manufacturing output, and export demand drivers were identified as core variables. Infrastructure distribution across industrial zones and workforce availability were mapped. Global supply chain dependencies were assessed.

Step 2: Market Analysis and Construction

Market structure was constructed through analysis of semiconductor firm presence, facility types, and industry segmentation across electronics sectors. Infrastructure categories including packaging, test, and support facilities were modeled. End-use demand linkages were evaluated.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions regarding outsourcing trends, technology shifts, and demand cycles were validated through semiconductor ecosystem benchmarking and technology analysis. Regional manufacturing dynamics were incorporated. Competitive positioning factors were verified.

Step 4: Research Synthesis and Final Output

All findings were synthesized into a structured market model describing segmentation, competition, growth drivers, and opportunities. Infrastructure investment trends and supply chain roles were integrated. Final outputs reflected technology and manufacturing dynamics shaping the Philippines semiconductor infrastructure outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of semiconductor assembly and packaging capacity in Philippines

Rising global demand for electronics manufacturing diversification

Government incentives to strengthen domestic semiconductor ecosystem - Market Challenges

Limited advanced wafer fabrication capability within the country

Dependence on imported semiconductor equipment and materials

Infrastructure and power reliability constraints for fabs - Market Opportunities

Upgrading OSAT facilities toward advanced packaging technologies

Attracting foreign semiconductor supply chain investments

Development of local semiconductor materials and support services - Trends

Shift toward advanced packaging and heterogeneous integration lines

Increasing automation and robotics in assembly and test facilities

Integration of smart manufacturing and fab digitalization systems - Government regulations

Semiconductor industry investment incentive and tax policies

Export control and technology transfer compliance frameworks

Industrial zone and electronics cluster development programs - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Facilities

Semiconductor Assembly and Packaging Lines

Test and Inspection Systems

Cleanroom and Fab Support Infrastructure

Semiconductor Materials Handling Systems - By Platform Type (In Value%)

Integrated Device Manufacturer Facilities

Outsourced Semiconductor Assembly and Test Sites

Foundry Partner Facilities

Research and Pilot Production Labs

Electronics Manufacturing Clusters - By Fitment Type (In Value%)

Greenfield Fab Construction

Brownfield Facility Expansion

Equipment Retrofit and Upgrade

Modular Production Line Integration

Automation and Robotics Add-ons - By End User Segment (In Value%)

OSAT Providers

IDM Companies

Electronics Manufacturing Services Firms

Automotive Electronics Suppliers

Government and Research Institutes - By Procurement Channel (In Value%)

Direct Equipment Procurement

Engineering Procurement Construction Contracts

OEM Integrated Supply

Distributor and Agent Supply

Government Incentive Programs

- Market Share Analysis

- Cross Comparison Parameters (Packaging Technology Capability, Process Node Compatibility, Production Automation Level, Cleanroom Class Standard, Yield Optimization Systems, Capacity Scalability, Materials Handling Automation, Test and Inspection Integration, Energy and Utility Efficiency, Facility Expansion Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amkor Technology Philippines

ASE Philippines

STATS ChipPAC Philippines

Texas Instruments Philippines

Analog Devices Philippines

Nexperia Philippines

Onsemi Philippines

IMI Philippines

Cirtek Holdings

Integrated Microelectronics Inc

PTON Corporation

SFA Semicon Philippines

Fastech Synergy Philippines

ATEC Philippines

ROHM Electronics Philippines

- OSAT providers expanding advanced packaging and testing capacity

- EMS firms integrating semiconductor back-end production lines

- Automotive and industrial electronics suppliers localizing assembly

- Government and research institutes building pilot semiconductor labs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now