Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Shared Mobility Platforms market is valued at USD ~billion in 2024, with the market driven by increasing urbanization, traffic congestion, and the rising adoption of sustainable transport solutions. In 2023, the Philippines saw a significant increase in shared mobility adoption as the government supported green mobility initiatives and technology adoption. The market’s growth is further fueled by advancements in mobile technologies, improvements in payment systems, and rising consumer awareness of eco-friendly transportation alternatives. Additionally, the pandemic’s impact has accelerated the shift toward contactless and flexible transport solutions, thereby contributing to the market’s growth.

Metro Manila is the dominant region for shared mobility in the Philippines, as the high population density, urban sprawl, and traffic congestion demand efficient and flexible transport options. In addition to Metro Manila, cities like Cebu, Davao, and Quezon City also contribute significantly to the market, with expanding adoption of ride-hailing services, bike-sharing platforms, and electric scooters. The development of infrastructure and government incentives to support green mobility initiatives further bolsters the presence and demand for shared mobility services in these regions.

Market Segmentation

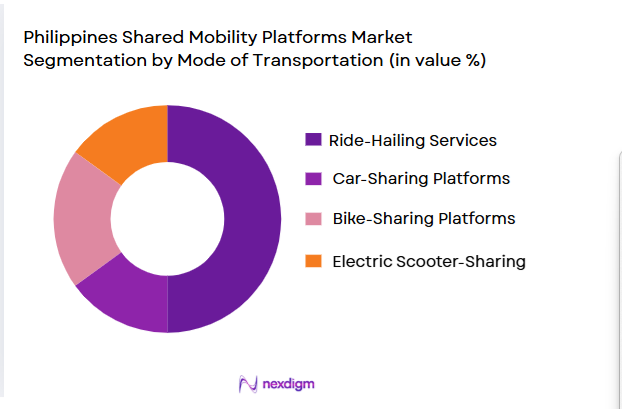

By Mode of Transportation

The Philippines Shared Mobility Platforms market is primarily segmented by mode of transportation, with major segments being ride-hailing services, car-sharing platforms, bike-sharing platforms, and electric scooter-sharing services. Ride-hailing services, such as Grab and Angkas, currently dominate the market. Their widespread popularity stems from the convenience of on-demand transportation and the growing urbanization of major cities. Car-sharing and bike-sharing services have also witnessed growth, particularly with the rising demand for more sustainable transport solutions. The ongoing trend toward the adoption of electric vehicles and micro-mobility solutions such as e-scooters is expected to gain more market share in the coming years.

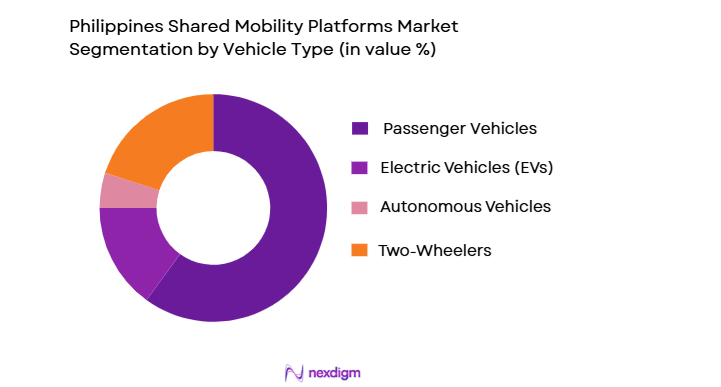

By Vehicle Type

The market is also segmented by vehicle type, including passenger vehicles, electric vehicles (EVs), autonomous vehicles, and two-wheelers like motorcycles and e-scooters. Passenger vehicles and motorcycles dominate the market share due to the prevalent use of motorcycles for transport services, particularly for two-wheeled ride-hailing services. The adoption of electric vehicles (EVs) is expected to rise, as government policies promote sustainable and eco-friendly transportation solutions. Meanwhile, the emergence of autonomous vehicles is still in its nascent stages but holds potential for long-term market growth.

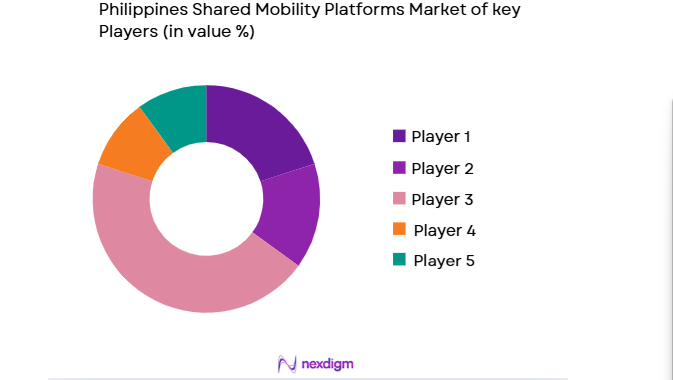

Competitive Landscape

The Philippines Shared Mobility Platforms market is characterized by a mix of local and international players offering a variety of services, including ride-hailing, bike-sharing, and car-sharing platforms. Major players in the market include Grab, Angkas, and GoJek, which dominate the ride-hailing and motorcycle taxi sectors. Additionally, electric scooter-sharing services are gaining traction with platforms such as Move It and Beep. The market remains competitive, with companies increasingly investing in technology and expanding service offerings to cater to growing consumer demand.

| Company | Establishment Year | Headquarters | Mode of Transportation | Vehicle Type | Service Area | Notable Partnership |

| Grab | 2012 | Singapore | ~ | ~ | ~ | ~ |

| Angkas | 2010 | Philippines | ~ | ~ | ~ | ~ |

| Move It | 2015 | Philippines | ~ | ~ | ~ | ~ |

| Beep | 2017 | Philippines | ~ | ~ | ~ | ~ |

| GoJek | 2010 | Indonesia | ~ | ~ | ~ | ~

|

Philippines Shared Mobility Platforms Market Analysis

Growth Drivers

Urbanization

Urbanization in the Philippines is a significant factor driving the adoption of shared mobility services. With over ~million people living in urban areas as of 2025, the urbanization rate has been steadily increasing. The Philippines’ urban population is expected to grow, with the majority of this growth concentrated in Metro Manila and surrounding cities. This rapid urban expansion creates a demand for efficient, flexible, and sustainable transportation alternatives, propelling the growth of shared mobility services such as ride-hailing, car-sharing, and bike-sharing platforms. The government’s development plans, including the “Build, Build, Build” program, are enhancing urban infrastructure and facilitating easier access to shared mobility services.

Traffic Congestion and Public Transportation Deficiencies

The Philippines struggles with traffic congestion, particularly in Metro Manila, where average commute times can exceed 2 hours each day. The lack of an efficient public transport system contributes to this issue, which has led to an increased demand for shared mobility platforms. In 2025, the National Economic and Development Authority (NEDA) reported that traffic congestion costs the Philippine economy USD ~billion annually. This economic burden has made shared mobility services an essential solution for daily commuters looking for faster, more reliable alternatives to traditional public transportation.

Restraints

High Initial Costs

A key restraint for the shared mobility market in the Philippines is the high initial investment required for the establishment and expansion of such platforms. For instance, ride-hailing services and fleet operators need to invest heavily in purchasing and maintaining vehicles, particularly electric ones, which tend to have higher upfront costs compared to conventional vehicles. According to the Department of Energy, the cost of acquiring an electric vehicle (EV) can be as high as PHP ~million per unit, significantly higher than traditional gasoline vehicles. This initial cost barrier prevents some potential service providers from entering the market and hampers the overall market growth.

Regulatory Hurdles

While government support for shared mobility services has increased, regulatory hurdles remain a significant challenge for service providers. The Land Transportation Franchising and Regulatory Board (LTFRB) continues to implement complex regulations on the operation of ride-hailing platforms, including fare pricing, fleet size, and vehicle standards. In 2025, the LTFRB imposed a cap on the number of ride-hailing vehicles in Metro Manila, which has limited the ability of companies like Grab and Angkas to scale up their services. These regulations create operational challenges for companies trying to expand their fleets to meet increasing demand.

Opportunities

Technological Advancements

Technological innovations present significant opportunities for the growth of shared mobility services in the Philippines. The integration of artificial intelligence (AI) and machine learning into ride-hailing platforms enhances operational efficiency by optimizing route planning, reducing waiting times, and improving customer experience. In 2025, the Philippines saw the launch of several AI-powered mobility apps that allow real-time tracking, predictive maintenance, and dynamic pricing. The adoption of blockchain technology for secure transactions and payment systems is also expected to improve service transparency and customer trust in shared mobility platforms.

International Collaborations

International collaborations can provide shared mobility companies in the Philippines with the expertise and resources needed to scale their operations. Partnerships with global electric vehicle manufacturers and technology companies can help local players enhance their fleets and incorporate advanced technologies such as autonomous driving and vehicle-to-everything (V2X) communication. In 2025, the Philippines’ government entered into discussions with international mobility firms like Uber and Lyft to expand the country’s shared mobility infrastructure, particularly in underserved regions outside Metro Manila. These collaborations can create new growth avenues for local companies.

Future Outlook

Over the next five years, the Philippines Shared Mobility Platforms market is poised to experience significant growth driven by the increasing adoption of digital technologies, urbanization, and government support for sustainable transportation. The rise of electric vehicles and micro-mobility solutions, such as e-scooters, is expected to play a key role in reshaping the market dynamics. The growing demand for flexible, eco-friendly transport options and the integration of smart city initiatives will fuel market growth, presenting substantial opportunities for new and existing players.

Major Players in the Market

- Grab

- Angkas

- Move It

- Beep

- GoJek

- MiCab

- Lyft Philippines

- Uber

- JoyRide

- Trebble

- Cebu Ride

- Micromobility Philippines

- Carpool Philippines

- Easy Taxi

- GogoRides

Key Target Audience

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies

- Shared Mobility Providers

- Vehicle Manufacturers and OEMs

- Fleet Operators

- Electric Vehicle (EV) Manufacturers

- Smart City Development Agencies

- Public Transportation Authorities

Research Methodology

Step 1: Identification of Key Variables

In this phase, the key variables affecting the growth of the Philippines Shared Mobility Platforms market are identified through a combination of secondary research and expert interviews. This includes assessing transportation preferences, regulatory frameworks, and adoption rates for shared mobility solutions.

Step 2: Market Analysis and Construction

Historical data on the adoption of shared mobility services in the Philippines is compiled and analyzed, focusing on service types, vehicle usage patterns, and demand across different regions. The analysis also evaluates factors influencing market growth, such as urbanization and government support for eco-friendly transportation.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses related to the adoption rates of different shared mobility services are validated through consultations with industry experts, including mobility service providers, government agencies, and technology developers. These interviews provide insights into market challenges and growth drivers.

Step 4: Research Synthesis and Final Output

The final phase synthesizes all the data gathered through desk research and expert consultations to generate actionable insights. The research is further validated by engaging with mobility service providers and stakeholders to refine the market data and forecast future trends.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Philippines-Specific Terminologies, Abbreviations, Market Sizing Logic, Bottom-Up & Top-Down Validation, Triangulation Framework Primary Interviews Across Mobility Service Providers, Government Agencies, Industry Experts, and Technology Developers, Demand-Side & Supply-Side Weightage, Data Reliability Index, Limitations & Forward-Looking Assumptions)

- Definition and Scope

- Market Genesis and Evolution Pathway

- Philippines Shared Mobility Industry Timeline

- Shared Mobility Business Cycle

- Shared Mobility Supply Chain & Value Chain Analysis

- Market Trends Shaping the Shared Mobility Landscape

- Regulatory Landscape Impacting Shared Mobility Systems

- Key Growth Drivers

Urbanization and Increasing Population Density

Government Support for Sustainable Mobility

Growing Consumer Preference for Mobility-as-a-Service

Technological Innovations in Mobility Platforms - Market Opportunities

Growing Demand for Electric and Sustainable Shared Mobility Solutions

Integration of Multi-modal Mobility Platforms

Expanding Presence in Tier-2 and Tier-3 Cities - Key Trends

Adoption of Electric Vehicles in Shared Mobility Fleets

Integration of Smart City Infrastructure with Shared Mobility Platforms

Use of AI and Data Analytics for Fleet Management and Consumer Insights - Regulatory & Policy Landscape

National Government Policies on Shared Mobility

Local Government Regulations and Incentives for Mobility Providers

Environmental and Safety Standards for Shared Mobility Services - SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces Analysis

- By Value, 2019-2025

- By Volume, 2019-2025

- By Average Price, 2019-2025

- By Vehicle Type Adoption, 2019-2025

- By Mobility Service Type, 2019-2025

- By Region, 2019-2025

- By Mode of Transportation (In Value %)

Ride-Hailing Services

Car-Sharing Platforms

Bike-Sharing Platforms

Scooter-Sharing Platforms

Peer-to-Peer Car Rentals - By End-User (In Value %)

Corporate Sector

Individual Consumers

Public Sector (Government and Institutional Use) - By Vehicle Type (In Value %)

Passenger Vehicles

Electric Vehicles

Autonomous Vehicles

Motorcycles and Scooters - By Service Model (In Value %)

Subscription-Based Models

Pay-as-You-Go Models

Hybrid Models - By Region (In Value %)

Metro Manila

Northern Luzon

Visayas

Mindanao

- Market Share Analysis

By Mode of Transportation

By Vehicle Type - Cross Comparison Parameters (Product Portfolio Breadth, Service Reliability & Availability, Technological Advancements & Integration, Distribution Footprint and Geographic Reach, Regulatory Approvals and Compliance, Strategic Partnerships & Collaborations, R&D Investment and Innovation)

- SWOT Analysis of Key Players

- Pricing Analysis

- Detailed Company Profiles

Grab Philippines

Angkas

Lyft

Uber Philippines

Beep

Move It

MiCab

GoJek

JoyRide

Trebble

Micromobility

Carpool Philippines

Easy Taxi

TnT Express

Lyft Philippines

- Demand Pattern & Utilization Metrics

- Procurement Models & Purchasing Cycles for Shared Mobility Services

- Compliance & Certification Expectations

- Consumer Needs, Desires & Pain-Point Mapping

- Decision-Making Framework for Mobility Providers and Government Authorities

- By Value, 2026-2030

- By Volume, 2026-2030

- By Average Price, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now