Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Smart Parking Solutions market is valued at USD ~, reflecting consolidated revenues from smart parking hardware, digital platforms, and managed services deployed across urban and commercial environments. The market has emerged as a structural enabler of urban mobility, driven by chronic parking shortages, rising vehicle density, and the modernization of municipal transport systems. Demand is further supported by the digitalization of payment ecosystems and the growing need for data-driven parking management that reduces congestion, increases turnover efficiency, and improves user experience across public and private parking assets nationwide.

The Philippines Smart Parking Solutions market is primarily concentrated in major urban centers such as Metro Manila, Cebu City, and Davao City, where population density, traffic congestion, and commercial development intensify parking demand and justify advanced management systems. These cities dominate adoption because they host large business districts, airports, retail complexes, and transport terminals that require continuous parking optimization. On the supply side, technology influence is shaped by countries that lead in mobility software, sensor manufacturing, and automation platforms, which provide the core systems adopted locally through partnerships and regional system integrators, accelerating deployment quality and operational sophistication.

Market Segmentation

By Parking Type

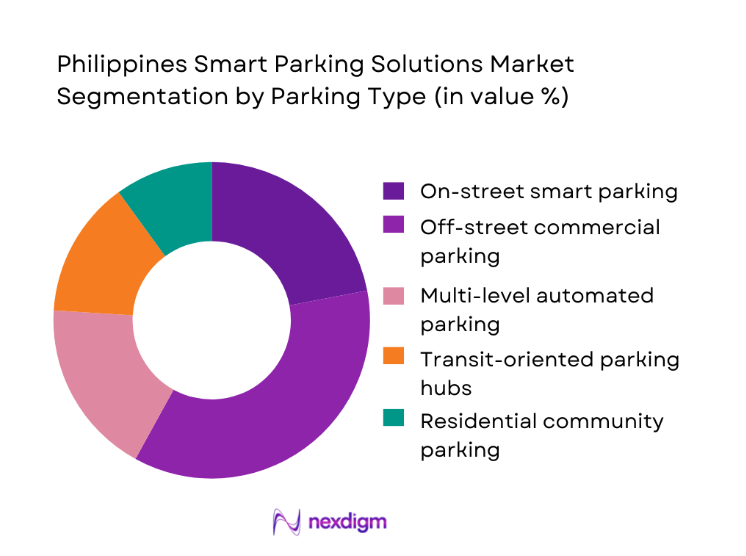

The Philippines Smart Parking Solutions market is segmented by parking type into on-street smart parking, off-street commercial parking, multi-level automated parking, transit-oriented parking hubs, and residential community parking. Off-street commercial parking currently dominates this segmentation because shopping malls, mixed-use developments, and office complexes represent the largest concentration of monetized parking assets in urban centers. These facilities prioritize smart parking to improve traffic circulation, reduce entry and exit bottlenecks, and enhance customer experience through guided parking and digital payments. The consistent footfall in commercial zones creates a strong business case for operators to invest in automation and analytics, enabling better revenue assurance and operational transparency. In contrast, municipal on-street deployments often face slower procurement cycles and budget constraints, allowing the private commercial segment to lead adoption in both scale and technological sophistication.

By Solution Component

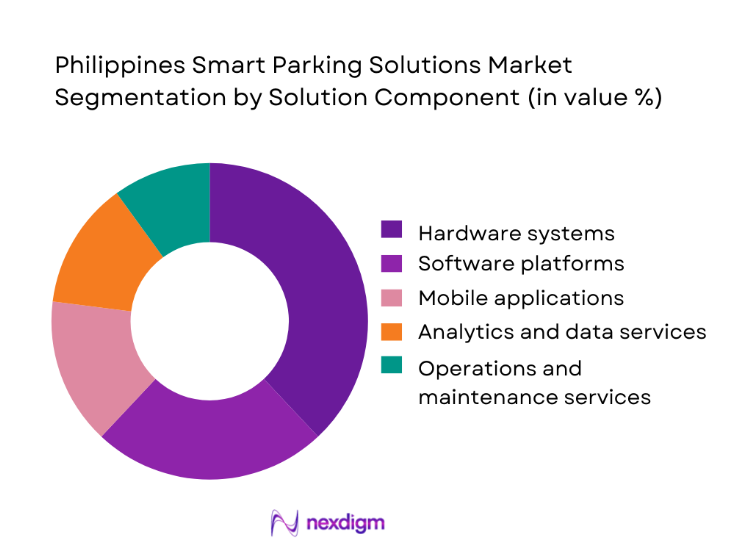

The Philippines Smart Parking Solutions market by solution component includes hardware systems, software platforms, mobile applications, analytics and data services, and operations and maintenance services. Hardware systems dominate this segmentation because sensors, access barriers, cameras, and payment terminals form the physical backbone of every smart parking deployment. Most parking operators begin their digital transformation by upgrading physical infrastructure before layering software intelligence on top. This has created sustained demand for hardware investments, particularly in high-traffic commercial facilities and transport hubs. Additionally, many older parking structures across the country still operate on manual or semi-automated systems, making hardware modernization the first and largest capital expenditure. While software and analytics are growing rapidly, the continued expansion of new parking sites and retrofit projects ensures that hardware remains the leading revenue contributor within the solution ecosystem.

Competitive Landscape

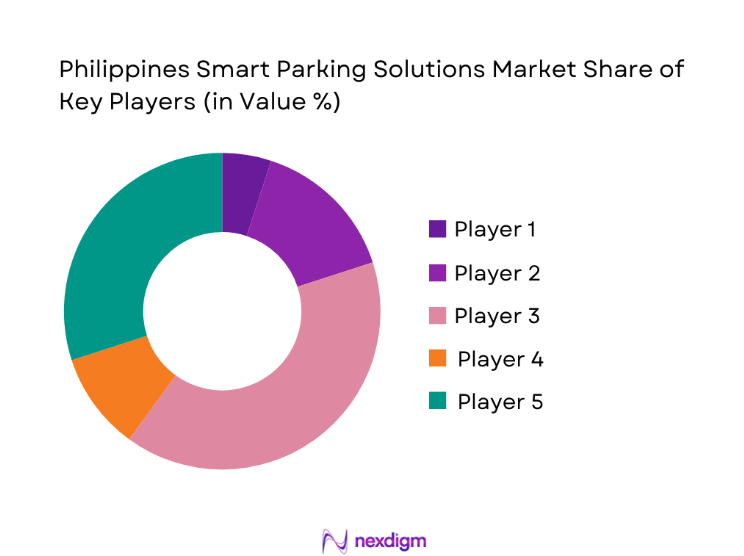

The Philippines Smart Parking Solutions market is dominated by a few major players, including Parkade Solutions Philippines and global or regional brands like SKIDATA, Amano, and Bosch Mobility Solutions. This consolidation highlights the significant influence of these key companies.

| Company | Establishment Year | Headquarters | Sensor Tech Maturity | Mobile Integration | LGU Partnerships | Analytics Capability | Service Coverage | Deployment Footprint |

| Parkade Solutions Philippines | 2010 | Manila, PH | ~ | ~ | ~ | ~ | ~ | ~ |

| Fastpark Technologies | 2015 | Cebu, PH | ~ | ~ | ~ | ~ | ~ | ~ |

| Zentech Smart Parking Systems | 2008 | Davao, PH | ~ | ~ | ~ | ~ | ~ | ~ |

| Amano Philippines | 1978 | Manila, PH | ~ | ~ | ~ | ~ | ~ | ~ |

| SKIDATA Philippines | 1977 | Salzburg, AT (local PH office) | ~ | ~ | ~ | ~ | ~ | ~ |

Philippines Smart Parking Solutions Analysis

Growth Drivers

Urban congestion and vehicle density

Rising vehicle ownership and chronic congestion in major Philippine cities have made parking inefficiency a visible urban problem. As drivers spend more time searching for available spaces, productivity losses and traffic spillovers increase, pushing both municipalities and private operators to adopt smart parking solutions. These systems directly address pain points by improving space utilization, shortening search times, and enabling real-time availability updates. The result is not only better mobility outcomes but also improved public perception of urban transport services, reinforcing investment momentum in smart parking infrastructure.

Smart city and digital governance programs

National and local digitalization agendas have elevated smart mobility as a priority pillar of urban development. Smart parking solutions align naturally with these programs because they offer measurable improvements in service delivery, transparency, and revenue management. Municipal governments increasingly view parking digitization as a low-risk, high-impact entry point into broader smart city transformation, accelerating pilot projects and scaled deployments that strengthen market growth fundamentals.

Challenges

High upfront infrastructure cost

Smart parking deployments require significant capital investment in sensors, networking equipment, control systems, and software platforms. For many local governments and smaller private operators, these costs remain a barrier to adoption, particularly where parking revenue streams are uncertain or regulated. This financial hurdle slows market penetration beyond major urban and commercial centers.

Fragmented municipal regulations

Parking governance in the Philippines varies widely across cities and municipalities, creating a fragmented regulatory environment. Differences in fee structures, enforcement policies, and data governance standards complicate the rollout of standardized smart parking platforms. Vendors must frequently customize solutions for each locality, increasing project complexity and limiting economies of scale.

Opportunities

EV infrastructure convergence

The gradual rise of electric vehicles presents a strong opportunity for smart parking providers to integrate charging management into their platforms. Parking facilities that combine space management with EV charging orchestration can create new revenue streams and strengthen their relevance in future mobility ecosystems, positioning smart parking as a critical node in sustainable transport networks.

Mobility-as-a-service integration

Smart parking solutions are increasingly becoming part of integrated mobility platforms that combine public transport, ride-hailing, and micro-mobility services. This convergence opens opportunities for parking operators to embed their systems within broader urban travel apps, enhancing user convenience while unlocking data-sharing and partnership-driven growth models across the transport value chain.

Future Outlook

The Philippines Smart Parking Solutions market is expected to evolve into a core component of urban mobility infrastructure as cities continue to digitize transport services and prioritize congestion management. Strategic partnerships between technology providers, real estate developers, and government agencies will shape scalable deployment models, while advances in analytics and automation will shift the market from basic space management toward predictive and integrated mobility solutions that redefine how parking contributes to urban efficiency and sustainability.

Major Players

- Parkade Solutions Philippines

- Fastpark Technologies

- Zentech Smart Parking Systems

- Amano Philippines

- SKIDATA Philippines

- Bosch Mobility Solutions Philippines

- Hikvision Philippines Parking Division

- Dahua Smart Parking Philippines

- PayParking Philippines

- SICE Philippines

- Nedap Philippines

- Huawei Smart City Parking Philippines

- ParknCharge Solutions

- GetGo Smart Parking

- Smart Bay Systems

Key Target Audience

- Urban mobility and traffic management authorities

- Commercial real estate developers and mall operators

- Transport hub and airport parking authorities

- Investments and venture capitalist firms

- Government and regulatory bodies

- Telecommunications and IoT infrastructure providers

- Public-private partnership project sponsors

- Parking infrastructure owners and operators

Research Methodology

Step 1: Identification of Key Variables

The research begins with mapping the complete smart parking ecosystem in the Philippines, covering government agencies, private operators, technology vendors, and infrastructure partners. Secondary research and proprietary databases are used to identify critical demand drivers, regulatory influences, and technology adoption variables shaping the market.

Step 2: Market Analysis and Construction

Historical deployment patterns and revenue flows are analyzed to build a bottom-up market model. This includes evaluating solution mix performance, installation density across urban zones, and the balance between public and private sector demand.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market assumptions are validated through structured interviews with parking operators, urban mobility planners, and system integrators. These consultations provide operational insights that refine adoption trends, pricing models, and competitive dynamics.

Step 4: Research Synthesis and Final Output

All qualitative and quantitative findings are synthesized through triangulation, ensuring consistency across data sources. The final output integrates market sizing, segmentation, and strategic analysis into a comprehensive client-ready report.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, smart parking taxonomy across guidance enforcement and payments, market sizing logic by managed bays and contract value, revenue attribution across hardware software and services, primary interview program with LGUs mall operators and parking managers, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Adoption Maturity of Smart Parking in the Philippines

- Urban Congestion Context and Parking Demand Hotspots

- Parking Value Chain Mapping Across Site Owners Operators and Technology Providers

- Integration Landscape with Digital Payments and Mobility Platforms

- Growth Drivers

Urban congestion and rising vehicle ownership

Mall and estate focus on customer experience and dwell time

Growth of digital payments and QR acceptance

Demand for revenue assurance and reduced leakage

Expansion of mixed use developments and transport hubs - Challenges

Fragmented parking ownership and operator structures

Capex constraints and long payback expectations

Connectivity reliability issues for real time systems

User adoption friction and cash preference pockets

Enforcement complexity for on street parking zones - Opportunities

City led smart curb and on street digitization programs

Integration with MaaS apps and navigation platforms

Dynamic pricing adoption in high demand districts

EV charging and parking bundling in premium sites

Analytics monetization for footfall and demand forecasting - Trends

Shift toward LPR and camera analytics based solutions

Cashless parking growth through wallets and QR

Rise of multi site cloud managed parking operations

Adoption of reservation features for event and airport parking

Increased focus on fraud control and audit trails - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Managed Parking Bay Count, 2019–2024

- By Software and Services Revenue Split, 2019–2024

- By Mall vs Municipal vs Private Site Deployment Split, 2019–2024

- By Fleet Type (in Value %)

Shopping malls and mixed use estates

Airports ports and transport terminals

Office buildings and business districts

Hospitals and institutional campuses

Municipal and on street parking zones - By Application (in Value %)

Real time occupancy detection and guidance

Digital payment and cashierless parking

Reservation and pre booking parking

Access control and license plate recognition

Enforcement and violation management - By Technology Architecture (in Value %)

Sensor based bay detection systems

Camera based LPR and video analytics

Barrier gate and access hardware systems

Cloud based parking management platforms

Dynamic pricing and demand analytics engines - By Connectivity Type (in Value %)

Standalone site deployments

Wallet and QR payment integrated systems

API integrated systems with mall apps and loyalty

City platform integrated smart curb systems

Cloud managed multi site parking operations - By End-Use Industry (in Value %)

Parking operators and facility managers

Real estate developers and property managers

Local government units and transport authorities

Airports terminal operators and logistics hubs

Payment wallets and fintech partners - By Region (in Value %)

NCR

CALABARZON

Central Luzon

Visayas

Mindanao

- Competitive ecosystem structure across parking operators technology providers and payment partners

- Positioning driven by LPR accuracy integration capability and service footprint

- Partnership models between mall operators LGUs and fintech ecosystems

- Cross Comparison Parameters (occupancy detection accuracy, LPR performance in low light and rain, payment integration breadth and settlement speed, system uptime and incident response, scalability across multi site operations, enforcement workflow capability, data analytics and reporting depth, total cost of ownership per bay)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Detailed Profiles of Major Companies

ParkSecure

ParkingPlus Philippines

Swarco

SKIDATA

Tiba Parking Systems

ParkHelp Technologies

Bosch Building Technologies

Huawei

Xerox Transportation Solutions

PayMaya Enterprise

GCash for Business

AF Payments Inc

Megawide Parking Systems

SM Prime Parking Management

Ayala Land Parking Operations

- Site owner priorities for revenue uplift and customer experience

- Operator procurement criteria for uptime and service levels

- Local government decision logic for enforcement and compliance

- User willingness to pay and adoption drivers for cashless

- Total cost of ownership drivers across hardware software and maintenance

- By Value, 2025–2030

- By Managed Parking Bay Count, 2025–2030

- By Software and Services Revenue Split, 2025–2030

- By Mall vs Municipal vs Private Site Deployment Split, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now