Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Systemic Lupus Erythematosus testing market is valued at USD ~, reflecting the specialized segment of autoimmune diagnostics that supports early detection, disease monitoring, and long-term management of lupus patients. Demand for SLE testing is structurally anchored in the rising burden of autoimmune disorders, increasing clinical awareness among physicians, and broader access to diagnostic services through public and private healthcare systems. The market’s importance is amplified by the chronic nature of lupus, which requires repeated laboratory monitoring across patient lifecycles, creating sustained utilization of immunological assays and reinforcing the strategic relevance of this diagnostic segment.

Within the Philippines, major urban healthcare hubs dominate testing demand due to their concentration of tertiary hospitals, rheumatology specialists, and advanced laboratory infrastructure capable of handling complex immunoassays. These cities act as referral centers for surrounding regions, consolidating diagnostic volumes and accelerating adoption of new testing technologies. Globally, countries with strong diagnostic manufacturing ecosystems and innovation leadership influence the Philippine market through technology transfer, reagent supply, and analyzer platforms. Their dominance stems from deep investments in immunology research, established regulatory expertise, and long-standing partnerships with local distributors that ensure consistent access to high-quality lupus testing solutions.

Market Segmentation

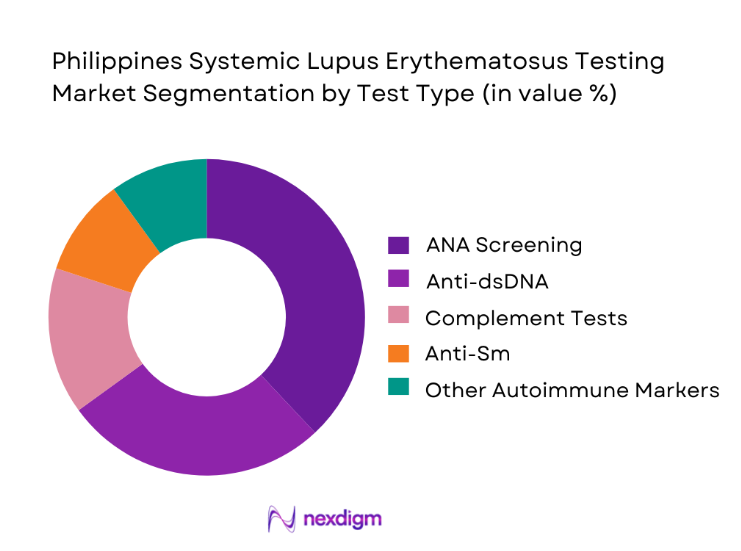

By Test Type

The Philippines Systemic Lupus Erythematosus testing market is segmented by test type into ANA screening tests, anti-dsDNA assays, complement level tests, anti-Sm assays, and antiphospholipid antibody panels. Among these, ANA screening tests dominate overall market value because they represent the primary diagnostic gateway for suspected lupus cases. Clinicians rely heavily on ANA as the first-line investigation, making it a routine inclusion in autoimmune workups across both public and private healthcare facilities. The widespread availability of ANA assays, combined with their relatively lower cost and high sensitivity, drives consistent test volumes. Hospitals and diagnostic laboratories prioritize maintaining steady stocks of ANA reagents, ensuring uninterrupted service. As patient awareness improves and referrals increase, the frequency of ANA testing continues to outpace more specialized assays, reinforcing its leadership position in the testing mix.

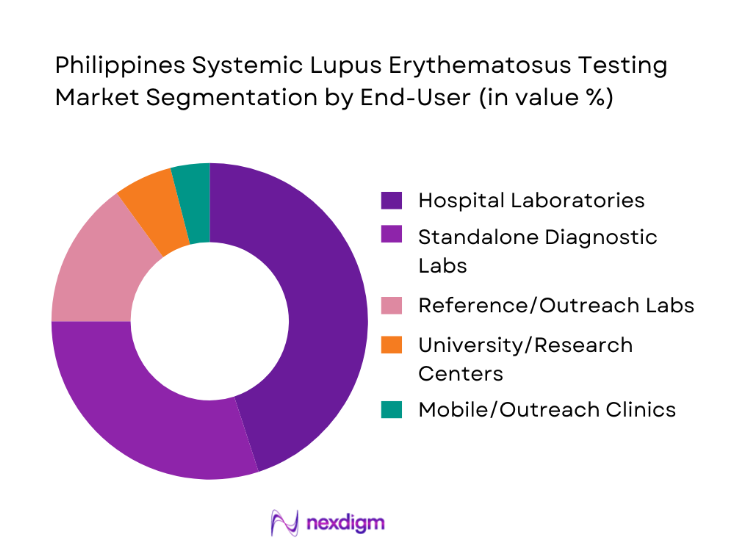

By End-Use

The Philippines Systemic Lupus Erythematosus testing market is segmented by end-use customer type into government tertiary hospitals, private multispecialty hospitals, standalone diagnostic laboratories, academic and research institutions, and mobile and outreach diagnostic units. Government and private hospitals dominate this segmentation due to their central role in managing chronic autoimmune conditions. These facilities act as primary touchpoints for lupus patients, coordinating diagnostics, treatment, and long-term monitoring under one roof. Their in-house laboratories are equipped with automated immunoassay platforms that support high test throughput and faster turnaround times, making them the preferred setting for both clinicians and patients. Additionally, hospitals benefit from structured reimbursement pathways and procurement contracts that stabilize demand for SLE testing, ensuring consistent utilization and reinforcing their dominant share in the market landscape.

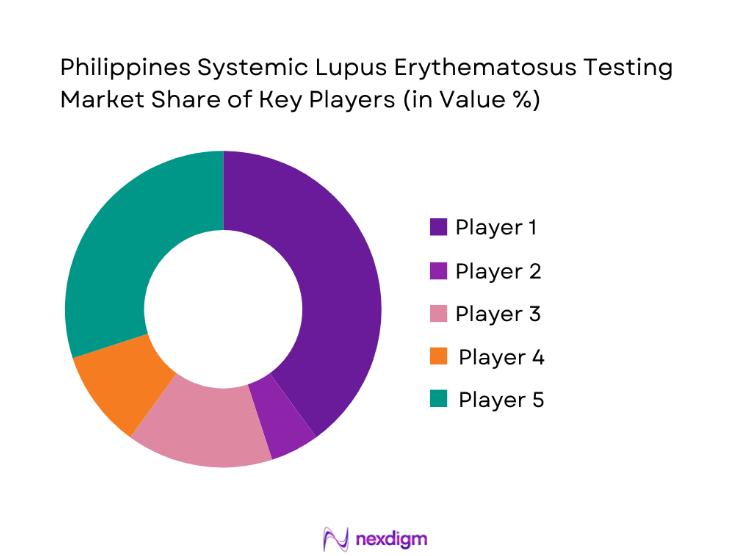

Competitive Landscape

The Philippines Systemic Lupus Erythematosus testing market is dominated by a few major players, including Roche Diagnostics and global or regional brands like Abbott Diagnostics, Siemens Healthineers, and Bio-Rad Laboratories. This consolidation highlights the significant influence of these key companies.

| Company | Establishment Year | Headquarters | Assay Platform Availability | Local Distribution Reach | After-Sales Support Quality | Local Validation Support | Range of SLE Test Panels |

| Roche Diagnostics | 1896 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Abbott Diagnostics | 1888 | USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

| Bio-Rad Laboratories | 1952 | USA | ~ | ~ | ~ | ~ | ~ |

| Thermo Fisher Scientific | 1956 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Systemic Lupus Erythematosus Testing Market Analysis

Growth Drivers

Rising Autoimmune Disease Awareness

Growing awareness of autoimmune diseases among healthcare professionals and patients has significantly increased the demand for early diagnostic interventions in the Philippines. As public health campaigns and medical education programs highlight the importance of timely detection of lupus, more patients are being referred for confirmatory testing at earlier stages of disease progression. This shift from symptom-based diagnosis to evidence-based laboratory confirmation strengthens the role of SLE testing as a routine clinical tool. The resulting increase in test volumes drives laboratory investments in immunology platforms and expands the reach of diagnostic services beyond major hospitals, ultimately reinforcing market growth and establishing diagnostics as a core pillar of lupus management pathways.

Expansion of Diagnostic Infrastructure

The continuous expansion of diagnostic infrastructure across urban and semi-urban areas has improved access to specialized testing services in the Philippines. New laboratory facilities, upgrades to automated immunoassay systems, and the establishment of regional reference centers have collectively increased the capacity to process complex autoimmune tests. This infrastructure growth reduces turnaround times and enhances clinician confidence in relying on laboratory data for treatment decisions. As testing becomes more accessible, physicians are more likely to include comprehensive lupus panels in routine evaluations, leading to higher utilization rates and stronger revenue streams for testing providers.

Challenges

High Cost of Specialized Testing

One of the major challenges facing the Philippines Systemic Lupus Erythematosus testing market is the high cost associated with specialized immunological assays. Advanced tests such as anti-dsDNA and antiphospholipid antibody panels often require imported reagents and sophisticated equipment, increasing operational expenses for laboratories. These costs are frequently passed on to patients, limiting affordability and potentially delaying diagnosis for individuals in lower-income segments. Although public healthcare programs provide partial support, gaps in reimbursement and budget constraints continue to restrict universal access, slowing the overall penetration of comprehensive SLE testing across the healthcare system.

Uneven Regional Access to Diagnostics

Another critical challenge is the uneven distribution of diagnostic capabilities across different regions of the Philippines. While major cities benefit from well-equipped laboratories and specialist services, many rural and remote areas lack access to advanced immunology testing. Patients in these regions often rely on referrals to distant urban centers, leading to delays in diagnosis and increased out-of-pocket expenses. This disparity not only affects patient outcomes but also limits the market’s ability to achieve balanced national growth, as significant portions of the population remain underserved by modern diagnostic infrastructure.

Opportunities

Expansion of Decentralized Testing Models

The development of decentralized testing models presents a strong opportunity for the Philippines Systemic Lupus Erythematosus testing market. By extending diagnostic services through satellite laboratories, mobile clinics, and community-based collection centers, providers can reach patients who previously had limited access to specialized tests. This approach reduces logistical barriers, shortens diagnostic timelines, and encourages earlier intervention. For manufacturers and service providers, decentralized models open new revenue channels and strengthen brand presence in emerging healthcare markets, supporting sustainable long-term growth.

Adoption of Automated Diagnostic Platforms

The increasing adoption of automated diagnostic platforms offers another major opportunity for market expansion. Automation improves test accuracy, enhances throughput, and reduces dependency on highly specialized laboratory personnel. As healthcare institutions modernize their laboratory operations, demand for integrated immunoassay systems is expected to rise, driving sales of analyzers, reagents, and maintenance services. This technological shift not only improves operational efficiency but also elevates the overall standard of lupus care, positioning diagnostics as a strategic investment area within the Philippine healthcare ecosystem.

Future Outlook

The Philippines Systemic Lupus Erythematosus testing market is expected to evolve into a more technologically advanced and accessible diagnostic landscape, driven by sustained investments in laboratory automation, expansion of regional healthcare infrastructure, and deeper integration of diagnostics into chronic disease management programs. As awareness and early screening initiatives gain momentum, testing volumes are likely to increase steadily, creating long-term opportunities for equipment manufacturers, reagent suppliers, and service providers to strengthen their footprint and contribute to improved patient outcomes nationwide.

Major Players

- Roche Diagnostics

- Abbott Diagnostics

- Siemens Healthineers

- Beckman Coulter

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Ortho Clinical Diagnostics

- Euroimmun

- DiaSorin

- Snibe Diagnostics

- Mindray Diagnostics

- ARKRAY Philippines

- Fujirebio

- Randox Laboratories

- Inova Diagnostics

Key Target Audience

- Hospital laboratory procurement heads

- Private diagnostic laboratory chains

- Pharmaceutical and diagnostics manufacturers

- Healthcare investment and venture capitalist firms

- Government and regulatory bodies Department of Health and PhilHealth

- Medical device distributors and importers

- Hospital group administrators

- National rheumatology and autoimmune disease associations

Research Methodology

Step 1: Identification of Key Variables

This phase focused on mapping the diagnostic ecosystem for lupus testing, identifying major stakeholders, and defining critical variables such as test categories, end users, and technology platforms. Extensive desk research and internal databases were used to establish the analytical foundation for the study.

Step 2: Market Analysis and Construction

Historical utilization trends, service delivery patterns, and revenue flows were analyzed to construct a comprehensive market framework. Both bottom-up and top-down approaches were applied to ensure consistency across market dimensions.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market assumptions were validated through structured interactions with laboratory directors, clinicians, and distribution partners. These discussions provided operational insights that strengthened the reliability of the analytical model.

Step 4: Research Synthesis and Final Output

All data points were triangulated and synthesized into a cohesive narrative, ensuring alignment between qualitative insights and quantitative frameworks. The final output reflects a balanced, client-ready assessment of the market landscape.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, SLE testing taxonomy and diagnostic pathway mapping, market sizing logic by test volume and panel utilization, revenue attribution across assays analyzers controls and service, primary interview program with rheumatologists labs hospitals and distributors, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Evolution of SLE Diagnostics in the Philippines

- Clinical Pathway Mapping Across Rheumatology Nephrology and OB GYN Care

- Referral Flow and Centralized Testing Dynamics for Specialty Immunology

- Access Barriers and Turnaround Time Constraints Outside Metro Centers

- Growth Drivers

Improving awareness and earlier referral to rheumatology care

Rising test menu expansion in private diagnostic chains

Demand for faster confirmatory testing to reduce diagnostic delay

Increased monitoring needs for lupus nephritis and complications

Greater use of classification aligned antibody panels - Challenges

High cost of confirmatory antibody and complement testing

Sample referral delays and limited specialty testing outside NCR

Interpretation variability for ANA patterns and antibody panels

Limited reimbursement coverage for specialized immunology workups

Supply continuity risk for imported reagents and controls - Opportunities

Expansion of centralized immunology reference laboratories

Distributor led automation upgrades and reagent rental programs

Standardized testing algorithms and reflex pathways for ANA positive cases

Growth of women’s health programs supporting SLE pregnancy monitoring

Digital reporting tools with interpretive comments for clinicians - Trends

Shift toward multiplex panels for ENA and dsDNA workflows

Greater adoption of automated CLIA platforms for antibody testing

Increasing use of reflex testing to optimize cost and turnaround time

Emphasis on accreditation readiness and stronger QC governance

Rising demand for integrated renal monitoring in lupus nephritis pathways - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Test Volume, 2019–2024

- By ANA Screening vs Confirmatory Testing Split, 2019–2024

- By Hospital vs Independent Lab Revenue Split, 2019–2024

- By Fleet Type (in Value %)

Public tertiary hospitals

Private hospital networks

Independent reference laboratories

Specialty rheumatology clinics

Academic medical centers - By Application (in Value %)

Initial screening for suspected SLE

Confirmatory antibody testing and classification support

Lupus nephritis monitoring and renal risk assessment

Pregnancy and maternal risk monitoring in SLE

Treatment monitoring and flare tracking - By Technology Architecture (in Value %)

ANA IFA screening platforms

ELISA based autoantibody assays

CLIA and automated immunoassay analyzers

Multiplex and line immunoassay panels

Complement testing platforms and inflammation marker integration - By Connectivity Type (in Value %)

Standalone analyzers with local reporting

LIS integrated laboratory workflows

Hub and spoke sample referral networks

Cloud enabled inventory and QC analytics tools

Remote service monitoring and uptime support - By End-Use Industry (in Value %)

Clinical laboratories and pathology networks

Rheumatology and nephrology clinics

Hospitals and inpatient care providers

Diagnostic distributors and reference testing partners

Women’s health and maternity care providers - By Region (in Value %)

NCR

CALABARZON

Central Luzon

Visayas

Mindanao

- Competitive ecosystem structure across IVD majors specialty immunology vendors and distributors

- Positioning driven by assay performance panel breadth and turnaround time capability

- Partnership models between distributors hospital groups and reference labs

- Cross Comparison Parameters (ANA IFA pattern capability and automation, anti dsDNA assay performance, ENA panel breadth and reflex support, complement testing integration readiness, turnaround time and referral network fit, LIS connectivity and reporting capability, QC and calibration burden, cost per patient workup)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Detailed Profiles of Major Companies

Roche Diagnostics

Abbott

Siemens Healthineers

Beckman Coulter

Thermo Fisher Scientific

DiaSorin

QuidelOrtho

Euroimmun

Inova Diagnostics

Bio Rad Laboratories

Randox Laboratories

Sysmex

Mindray

Hologic

bioMérieux

- Rheumatologist preferences for panel selection and interpretive reporting

- Lab priorities for throughput QC burden and reagent cost management

- Procurement models in public hospitals and private lab networks

- Distributor selection criteria for service reliability and training support

- Total cost of ownership drivers across assays controls and analyzer service

- By Value, 2025–2030

- By Test Volume, 2025–2030

- By ANA Screening vs Confirmatory Testing Split, 2025–2030

- By Hospital vs Independent Lab Revenue Split, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now