Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Timing Belts market reached a value of USD ~ billion based on a recent historical assessment, driven primarily by increasing vehicle parc, rising automotive aftermarket demand, and expansion in industrial machinery usage. Growth is supported by consistent vehicle maintenance cycles, especially in aging fleets, alongside increasing adoption of durable and high-performance timing belt systems in manufacturing. Import dependency and expanding distribution networks also contribute to stable market expansion, reinforcing demand across automotive and industrial applications.

Metro Manila, Cebu, and Davao dominate the Philippines Timing Belts market due to higher vehicle density, established automotive service infrastructure, and concentration of industrial operations. These urban hubs benefit from extensive logistics activity, large fleet operations, and higher disposable incomes supporting vehicle maintenance spending. Additionally, proximity to ports and trade routes enhances availability of imported components, while industrial zones in Luzon and Visayas further strengthen demand from manufacturing and processing sectors.

Market Segmentation

By Product Type:

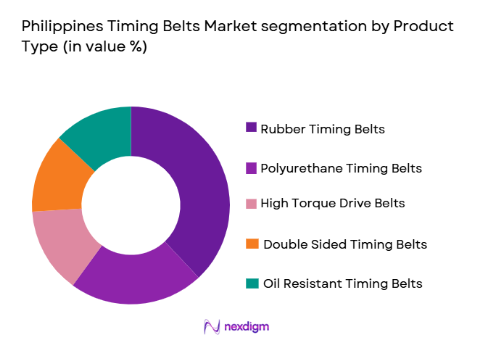

Philippines Timing Belts market is segmented by product type into Rubber Timing Belts, Polyurethane Timing Belts, High Torque Drive Belts, Double Sided Timing Belts, and Oil Resistant Timing Belts. Recently, Rubber Timing Belts has a dominant market share due to factors such as widespread compatibility with conventional vehicles, affordability, and strong availability across aftermarket channels. Their cost effectiveness and sufficient durability for standard automotive applications make them the preferred choice for fleet operators and individual vehicle owners. Moreover, local service providers commonly stock rubber-based belts, ensuring easy accessibility and quicker replacement cycles, which further strengthens their market position.

By EndUser:

Philippines Timing Belts market is segmented by end-user into Automotive Manufacturers, Automotive Aftermarket Service Providers, Fleet Operators, Industrial Manufacturing Units, and Agricultural Equipment Operators. Recently, Automotive Aftermarket Service Providers has a dominant market share due to factors such as frequent replacement cycles, growing number of aging vehicles, and increasing consumer reliance on third-party repair networks. The expansion of organized service chains and independent garages across urban and semi-urban areas further drives demand. Additionally, aftermarket providers offer a wide range of pricing options and brands, attracting cost-conscious consumers and ensuring sustained dominance in the segment.

Competitive Landscape

The Philippines Timing Belts market is moderately fragmented with the presence of global manufacturers and regional distributors competing on pricing, durability, and distribution reach. Leading players leverage strong supply chains, partnerships with OEMs, and established aftermarket networks to maintain their positions. Market consolidation is gradually increasing as international brands strengthen their presence through local partnerships and distribution agreements, enhancing product availability and brand visibility across key urban and industrial regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Strength |

| Bando Manufacturing Philippines Inc | 1906 | Japan | ~ | ~ | ~ | ~ | ~ |

| Mitsuboshi Belting Ltd | 1919 | Japan | ~ | ~ | ~ | ~ | ~ |

| Gates Corporation | 1911 | USA | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Dayco Products LLC | 1905 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Timing Belts Market Analysis

Growth Drivers

Rising Vehicle Parc and Aging Fleet Driving Replacement Demand:

The Philippines automotive landscape is witnessing a steady increase in vehicle ownership, particularly in urban and peri-urban regions, which significantly contributes to the demand for timing belts. As vehicles age, the need for periodic maintenance and component replacement becomes essential to ensure engine performance and safety. Timing belts, being critical engine components, require scheduled replacement, thereby creating consistent aftermarket demand. Fleet operators, including logistics and ride-hailing services, are increasingly adopting preventive maintenance practices to reduce downtime and operational costs. This behavior is further supported by rising awareness among vehicle owners regarding the risks of belt failure. Additionally, government initiatives promoting vehicle safety indirectly support maintenance activities. The presence of a large base of older vehicles ensures recurring demand cycles. Import-driven availability of replacement parts also ensures supply continuity. Expansion of service centers and workshops further facilitates access to maintenance services. Overall, the growing vehicle base and aging fleet structure act as a strong and sustained growth driver for the market.

Expansion of Industrial Machinery and Manufacturing Activities:

Industrial growth across sectors such as food processing, packaging, and construction materials is significantly driving demand for timing belts in the Philippines. Manufacturing facilities rely on timing belts for synchronized operations in machinery, ensuring efficiency and precision. The rise in automation and mechanization in production lines has increased the need for high-performance belt systems capable of handling continuous operations. Government support for industrialization and infrastructure development further boosts machinery deployment. Small and medium enterprises are also adopting modern equipment, increasing overall demand. The reliability and low maintenance characteristics of timing belts make them suitable for industrial applications. Additionally, the expansion of export-oriented manufacturing hubs contributes to higher machinery utilization. The need for operational efficiency and reduced downtime drives replacement cycles in industrial belts. Growth in sectors such as agriculture processing and logistics also contributes to demand. This industrial expansion provides a parallel growth trajectory alongside automotive applications.

Market Challenges

Volatility in Raw Material Prices Affecting Production Costs:

The Philippines Timing Belts market faces significant challenges due to fluctuations in the prices of key raw materials such as rubber, polyurethane, and synthetic fibers. These materials are largely imported, making costs sensitive to global commodity price movements and currency exchange fluctuations. Manufacturers often struggle to maintain stable pricing, which impacts profit margins and competitiveness. Frequent price changes also create uncertainty for distributors and retailers. Smaller players face greater challenges in absorbing cost increases compared to larger multinational companies. Additionally, rising logistics and transportation costs further add to overall production expenses. These cost pressures may result in higher product prices, affecting demand among price-sensitive consumers. The presence of low-cost counterfeit products intensifies pricing competition. Manufacturers must balance cost management with maintaining product quality. This volatility ultimately poses a significant operational and strategic challenge for market participants.

Prevalence of Counterfeit and Low-Quality Products in Aftermarket:

The widespread availability of counterfeit and substandard timing belts in the aftermarket poses a major challenge to the Philippines Timing Belts market. These products are often sold at significantly lower prices, attracting cost-conscious consumers but compromising quality and safety. Counterfeit belts can lead to engine failures and increased maintenance costs, negatively impacting consumer trust in the overall market. Authorized distributors and established brands face revenue losses due to unfair competition. Regulatory enforcement remains limited, allowing counterfeit products to penetrate both urban and rural markets. Lack of consumer awareness regarding product authenticity further exacerbates the issue. Service providers sometimes prioritize cost over quality, contributing to the problem. This environment creates challenges for premium brands attempting to maintain pricing and quality standards. Addressing counterfeit products requires stronger regulatory intervention and awareness initiatives. The persistence of this issue continues to hinder market growth and brand integrity.

Opportunities

Expansion of Organized Automotive Aftermarket and Service Networks:

The growth of organized automotive service chains presents a significant opportunity for the Philippines Timing Belts market. As consumers increasingly prefer reliable and standardized services, organized workshops and service centers are gaining traction across major cities. These establishments typically use branded and high-quality components, including timing belts, ensuring better performance and customer trust. The expansion of franchise-based service networks enhances accessibility to quality maintenance services. Additionally, partnerships between component manufacturers and service providers strengthen distribution channels. Digital platforms enabling service bookings further contribute to market penetration. Organized networks also promote preventive maintenance practices, increasing replacement frequency. Training and certification programs for technicians improve service quality. This shift toward structured service ecosystems supports demand for premium timing belts. The trend is expected to continue as urbanization and vehicle ownership increase.

Adoption of High-Performance and Long-Life Timing Belt Technologies:

Technological advancements in timing belt materials and design offer significant growth opportunities in the Philippines market. Manufacturers are introducing belts with enhanced durability, heat resistance, and extended service life, catering to evolving consumer expectations. High-performance belts reduce maintenance frequency and improve engine efficiency, making them attractive for both automotive and industrial applications. Fleet operators, in particular, benefit from reduced downtime and operational costs. Increasing awareness of total cost of ownership encourages adoption of premium products. Innovations such as reinforced materials and noise reduction features further enhance product appeal. Industrial users also demand advanced belts for continuous operations. The availability of technologically advanced products differentiates established brands from low-cost competitors. As consumers prioritize reliability and performance, the market is expected to shift toward higher-value products. This transition creates opportunities for innovation-driven growth.

Future Outlook

The Philippines Timing Belts market is expected to witness steady growth driven by rising vehicle ownership, expanding industrial activities, and increasing awareness of preventive maintenance practices. Technological advancements in belt materials and design will support longer product lifecycles and improved performance. Regulatory focus on vehicle safety and quality standards is likely to enhance demand for reliable components. Additionally, the expansion of organized aftermarket networks and digital service platforms will further strengthen distribution and accessibility across urban and emerging regions.

Major Players

- Bando Manufacturing Philippines Inc

- Mitsuboshi Belting Ltd

- Gates Corporation

- Continental AG

- Dayco Products LLC

- Optibelt GmbH

- Megadyne Group

- Fenner Drives

- Habasit AG

- Pix Transmissions Ltd

- Goodyear Belting

- Tsubaki Nakashima Co Ltd

- Dongil Rubber Belt Co Ltd

- Sanlux Co Ltd

- Mitsubishi Chemical Group

Key Target Audience

- Automotivecomponentmanufacturers

- Automotive aftermarket service providers

- Fleet management companies

- Industrial machinery manufacturers

- Agricultural equipment operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive distributors

Research Methodology

Step 1: Identification of Key Variables

Primary variables such as vehicle parc, replacement cycles, industrial demand, and pricing trends are identified. Secondary variables include import patterns, distribution channels, and regulatory frameworks influencing market dynamics.

Step 2: Market Analysis and Construction

Comprehensive data analysis is conducted using both primary and secondary sources. Market sizing is developed through bottom-up and top-down approaches, ensuring consistency across automotive and industrial segments.

Step 3: Hypothesis Validation and Expert Consultation

Insights are validated through consultations with industry experts, distributors, and service providers. Assumptions are tested against real market conditions to ensure accuracy and reliability of findings.

Step 4: Research Synthesis and Final Output

All data points are consolidated into a structured framework. Final outputs are generated through analytical models, ensuring clarity, consistency, and actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising vehicle parc and aging vehicle fleet increasing replacement demand

Expansion of automotive assembly and manufacturing activities

Growth in logistics and fleet operations driving maintenance cycles

Increasing awareness of preventive vehicle maintenance practices

Industrial automation growth requiring reliable belt drive systems - Market Challenges

Volatility in raw material prices impacting production costs

Availability of low cost counterfeit products in aftermarket

Limited technical awareness among small scale service providers

Supply chain disruptions affecting timely availability

Dependence on imports for advanced belt technologies - Market Opportunities

Expansion of e commerce driven aftermarket distribution channels

Adoption of high performance and long life timing belts

Growth in industrial automation and machinery demand - Trends

Shift toward high durability and heat resistant belt materials

Increasing penetration of branded aftermarket components

Integration of predictive maintenance technologies in fleets

Growth of organized automotive service networks

Rising demand for noise reducing and efficient belt systems - Government Regulations & Defense Policy

Implementation of vehicle safety and maintenance standards

Import regulations and quality certification requirements

Industrial standards for machinery safety and performance - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Rubber Timing Belts

Polyurethane Timing Belts

High Torque Drive Belts

Double Sided Timing Belts

Oil Resistant Timing Belts - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Two Wheelers

Industrial Machinery - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

Fleet Maintenance Fitment

Performance Upgrade Fitment

Industrial Equipment Fitment - By EndUser Segment (In Value%)

Automotive Manufacturers

Automotive Aftermarket Service Providers

Fleet Operators

Industrial Manufacturing Units

Agricultural Equipment Operators - By Procurement Channel (In Value%)

Direct OEM Contracts

Authorized Distributors

Independent Aftermarket Retailers

Online Automotive Platforms

Industrial Supply Vendors - By Material / Technology (in Value %)

Neoprene Based Belts

Polyurethane Reinforced Belts

Glass Fiber Reinforced Belts

Kevlar Reinforced Belts

Hybrid Composite Belts

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Durability, Material Composition, Price Competitiveness, Distribution Network Strength, OEM Partnerships, Aftermarket Presence, Brand Recognition, Technological Innovation, Warranty Offering, Supply Chain Efficiency)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Bando Manufacturing Philippines Inc

Mitsuboshi Belting Philippines Corporation

Gates Philippines Inc

Continental Philippines Inc

Dayco Philippines Inc

Optibelt Philippines Inc

Megadyne Philippines Inc

Sanlux Timing Belt Philippines Inc

Fenner Drives Philippines Inc

Habasit Philippines Inc

Pix Transmissions Philippines Inc

Goodyear Belting Philippines Inc

Mitsubishi Chemical Advanced Materials Philippines Inc

Tsubaki Belt Philippines Inc

Dongil Rubber Belt Philippines Inc

- Automotive OEMs focusing on reliability and lifecycle cost optimization

- Fleet operators prioritizing preventive maintenance and uptime

- Aftermarket service providers expanding product portfolios and services

- Industrial users demanding high performance and durable belt systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now