Download PDF

Download PDFMarket Overview

The Philippines Toys & Games market is valued at USD ~ billion in 2025, up from USD ~ billion in 2024, reflecting strong consumer demand and rising disposable income. Growth is largely driven by increasing awareness of early childhood education, rising popularity of branded and licensed toys, and expansion of e-commerce channels. Retailers and online platforms are rapidly expanding their offerings, providing both domestic and international toy options, which has contributed significantly to market expansion and higher consumer accessibility.

Metro Manila, Cebu, and Davao dominate the Philippines Toys & Games market due to their higher urban populations, rising middle-class income, and concentration of retail and specialty stores. These cities have strong consumer purchasing power, access to global brands, and well-developed logistics and distribution infrastructure, making them attractive hubs for toy sales. Additionally, the presence of large shopping malls and online retail networks ensures these cities consistently lead in toy consumption and trends across the country.

Market Segmentation

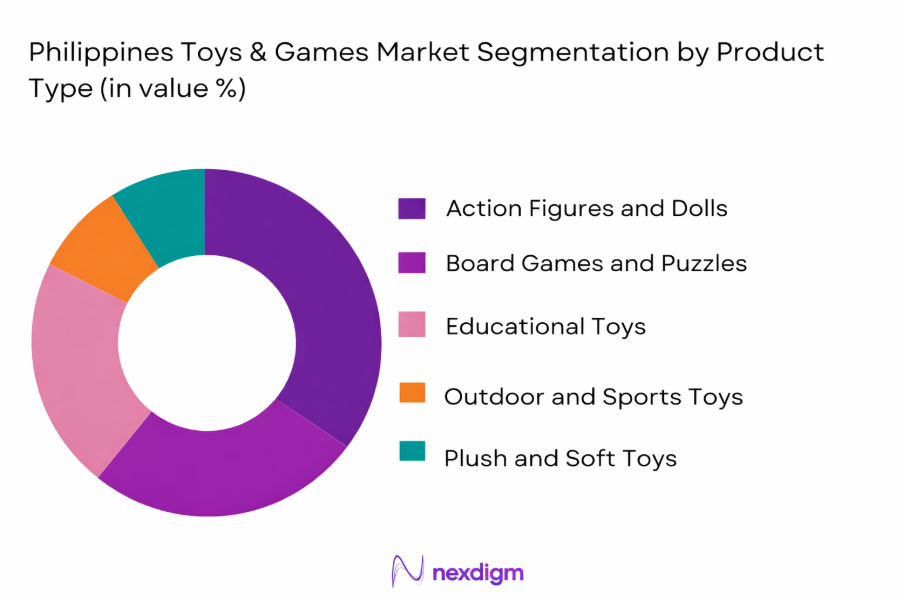

By Product Type

The Philippines Toys & Games market is segmented by product type into action figures and dolls, board games and puzzles, electronic and educational toys, outdoor and sports toys, plush and soft toys, and others. Among these, electronic and educational toys dominate the market due to growing consumer preference for products that combine entertainment with learning. Interactive features, STEM-based content, and licensed electronic educational kits appeal to parents seeking value-added toys for their children, boosting demand and adoption in urban and suburban areas.

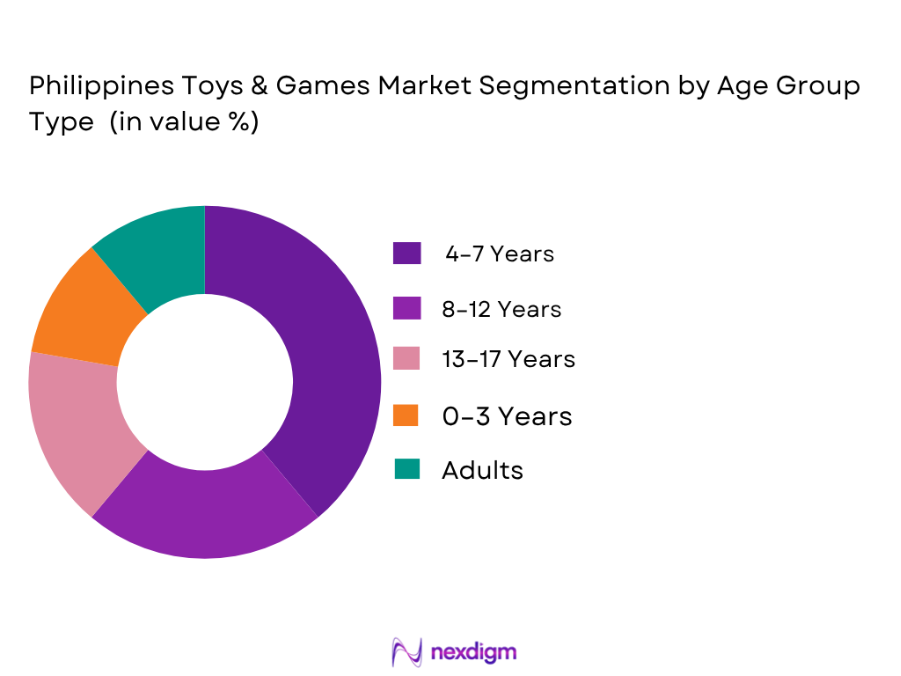

By Age Group

The market is segmented into 0–3 years, 4–7 years, 8–12 years, 13–17 years, and adults. The 4–7 years segment holds the largest share due to high demand for developmental toys that encourage creativity, learning, and social interaction. Parents in urban centers increasingly invest in age-appropriate toys to improve early learning outcomes. Popularity of branded and licensed toys targeting this age group, along with e-commerce availability, further consolidates its dominance.

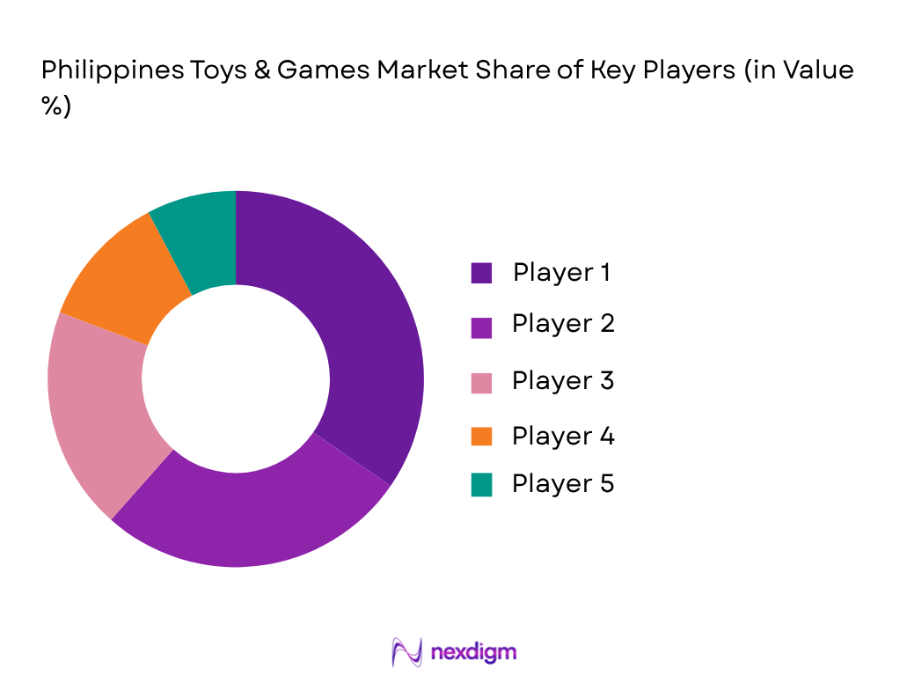

Competitive Landscape

The Philippines Toys & Games market is dominated by major international and regional players, including Mattel, LEGO, and Hasbro. These companies leverage strong brand equity, extensive distribution networks, and diverse product portfolios. Local manufacturers also contribute, though at a smaller scale, focusing on niche and traditional toys. The consolidation of key players demonstrates the influence of brand reputation, product innovation, and strategic partnerships in maintaining competitive advantage.

| Company | Establishment Year | Headquarters | Product Focus | Retail Strategy | Online Presence | Pricing Tier | Distribution Network |

| Toy Kingdom | 1991 | Philippines | ~ | ~ | ~ | ~ | ~ |

| Toys “R” Us Philippines | 1957 | USA/Philippines | ~ | ~ | ~ | ~ | ~ |

| Richprime Global | 1995 | Philippines | ~ | ~ | ~ | ~ | ~ |

| SM Store Toys | 1978 | Philippines | ~ | ~ | ~ | ~ | ~ |

| LEGO Philippines | 1932 | Denmark | ~ | ~ | ~ | ~ | ~ |

Philippines Toys & Games Market Analysis

Growth Drivers

Rising Disposable Income and Middle-Class Expansion

Rising disposable income and the expansion of the middle class have significantly fueled the Philippines Toys & Games market. With higher household spending capacity, families are increasingly investing in toys that offer both entertainment and educational value. Urban centers with growing populations, such as Metro Manila, Cebu, and Davao, witness higher retail activity, enabling manufacturers to introduce premium and licensed toys. Coupled with this, increasing awareness of early childhood education is influencing parental buying behavior. Parents are actively seeking products that enhance cognitive, motor, and social development, driving demand for STEM-based and educational toys. The combination of affordability, availability, and educational relevance has positioned this market segment as a key growth engine for the industry.

Increasing Awareness of Early Childhood Education

The growing popularity of licensed and branded toys has become a pivotal factor in market growth. International franchises like LEGO, Disney, and Marvel have a strong influence on consumer preferences, particularly among children and collectors. The emotional connection and perceived quality associated with well-known brands encourage repeat purchases and premium spending. Expansion of e-commerce and online retail channels further amplifies accessibility, enabling consumers in smaller cities and remote areas to access global toy offerings. Government initiatives supporting child development, such as early learning programs and educational campaigns, also bolster demand by promoting structured play. Collectively, these factors strengthen the market’s overall growth trajectory.

Market Challenges

Import Dependency and Supply Chain Disruptions

Import dependency and supply chain disruptions continue to pose significant challenges for the Philippines Toys & Games market. A large portion of toys are imported from countries such as China, the United States, and European nations. Any disruptions in manufacturing, shipping delays, or regulatory changes can affect product availability and pricing. Price sensitivity among consumers further complicates market dynamics, as buyers often weigh cost against perceived educational or entertainment value. Rapidly changing consumer preferences require manufacturers to continuously innovate and refresh product lines. Ensuring safety and regulatory compliance adds additional operational costs, particularly for imported toys that must meet local standards. Competition from unorganized and local toy manufacturers also pressures margins and market share.

Safety and Regulatory Compliance

Safety and regulatory compliance challenges are critical in the Philippines Toys & Games market. The Department of Trade and Industry (DTI) enforces toy safety standards, requiring companies to adhere to strict guidelines. Compliance with labeling, chemical content restrictions, and quality inspections increases operational complexity, particularly for small manufacturers and importers. Additionally, competition from unorganized local producers offering low-cost alternatives creates pricing pressures on established brands. Fluctuating import costs and supply chain uncertainties exacerbate these challenges, often affecting product availability during peak seasons. Rapid shifts in consumer trends further demand continuous innovation, forcing companies to balance compliance, quality, and affordability while maintaining brand trust and market relevance.

Opportunities

Rising Demand for Educational and STEM Toys

Rising demand for educational and STEM toys presents a major opportunity in the Philippines Toys & Games market. Parents increasingly seek products that enhance learning outcomes while entertaining children. STEM-focused kits, coding robots, and science experiment sets are gaining traction due to their dual educational and recreational appeal. Simultaneously, the emergence of eco-friendly and sustainable toys caters to environmentally conscious consumers who prioritize non-toxic materials, recyclability, and minimal packaging. This trend allows brands to differentiate their offerings while building long-term customer loyalty. Expansion of online retail and direct-to-consumer channels enables faster distribution, higher accessibility, and better consumer engagement, opening avenues for innovative marketing and personalized product offerings.

Licensing Opportunities and Technology-Integrated Toys

Licensing opportunities with international brands and innovation in interactive, technology-integrated toys further expand market potential. Global franchises such as Disney, Marvel, and Nickelodeon provide licensing agreements that allow local distributors to offer high-demand products. Additionally, advancements in augmented reality, app-connected toys, and interactive gaming experiences create new consumer engagement avenues. These technology-driven products appeal to tech-savvy parents and children, providing differentiation from traditional toys. By combining licensing and technological innovation, companies can capture niche segments, boost brand recognition, and drive both domestic and online sales. The market is thus positioned to capitalize on innovation-led growth.

Future Outlook

Over the next decade, the Philippines Toys & Games market is expected to experience sustained growth driven by rising urbanization, increasing disposable income, and a growing focus on early childhood education. Expansion of e-commerce and technological integration into toys will further accelerate adoption, while consumer interest in eco-friendly and STEM-based products will shape product development. International licensing and brand collaborations will continue to influence consumer preferences, supporting both innovation and market expansion across urban and emerging regions.

Major Players

- Mattel, Inc.

- LEGO Group

- Hasbro, Inc.

- VTech Holdings Ltd.

- Spin Master Corp.

- Fisher-Price

- Bandai Namco Holdings

- Funko, Inc.

- Playmates Toys

- Tomy Company, Ltd.

- Clementoni S.p.A.

- Ravensburger AG

- Mega Bloks

- Jakks Pacific, Inc.

- Schleich GmbH

Key Target Audience

- Toy Manufacturers and Distributors

- Retail Chains and Specialty Toy Stores

- E-commerce Retailers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Licensing and Brand Partnership Firms

- Parenting and Family-focused Consumer Groups

- Corporate Buyers for Educational and Recreational Institutions

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Philippines Toys & Games Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to the Philippines Toys & Games Market is compiled and analyzed. This includes assessing market penetration, sales distribution across segments, and revenue trends. Additionally, a review of consumer behavior patterns and competitive dynamics is conducted to ensure accurate market representation.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through interviews with industry experts, including executives from leading toy manufacturers and distributors. These discussions provide operational insights, financial perspectives, and direct feedback on trends, challenges, and growth opportunities, which enhances the reliability of the analysis.

Step 4: Research Synthesis and Final Output

The final phase involves engaging with multiple toy companies and retailers to acquire detailed insights on product sales, market preferences, and segment-specific trends. This information is cross-verified with the bottom-up and top-down market estimation approaches to ensure a comprehensive and validated report output.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Dynamics Overview

- Market Genesis

- Major Players and Market Timeline

- Business Cycle and Trends

- Supply Chain and Value Chain Analysis

- Growth Drivers

Rising Disposable Income and Middle-Class Expansion

Increasing Awareness of Early Childhood Education

Growing Popularity of Licensed and Branded Toys

Expansion of E-commerce and Online Retail Channels

Government Initiatives Supporting Child Development and Education - Market Challenges

Import Dependency and Supply Chain Disruptions

Price Sensitivity Among Consumers

Rapidly Changing Consumer Preferences

Safety and Regulatory Compliance

Competition from Unorganized and Local Toy Manufacturers - Opportunities

Rising Demand for Educational and STEM Toys

Emergence of Eco-friendly and Sustainable Toy Products

Expansion of Online Retail and Direct-to-Consumer Channels

Licensing Opportunities with International Brands

Innovation in Interactive and Technology-Integrated Toys - Key Trends

Shift Toward Educational and STEM-based Toys

Rising Popularity of Collectibles and Branded Merchandise

Integration of AR/VR and Digital Elements in Toys

Growing Preference for Eco-friendly and Non-toxic Materials

Expansion of Toy Subscription Services and On-demand Play Experiences - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Value, 2020–2025

- By Volume, 2020–2025

- By Average Price, 2020–2025

- By Product Type (In Value %)

Action Figures and Dolls

Board Games and Puzzles

Electronic and Educational Toys

Outdoor and Sports Toys

Plush and Soft Toys - By Age Group (In Value %)

0–3 Years

4–7 Years

8–12 Years

13–17 Years

Adults - By Material Type (In Value %)

Plastic

Wood

Electronic Components

Textile

Others - By Distribution Channel (In Value %)

Retail Stores

Toy Specialty Shops

E-commerce/Online Channels

Supermarkets and Hypermarkets

Convenience Stores - By Region (In Value %)

Luzon

Visayas

Mindanao

Rest of Philippines

- Market Share of Major Players by Value/Volume

- Market Share of Major Players by Product Type

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strength, Weakness, Organizational Structure, Revenues, Revenues by Product Type, Number of Touchpoints, Distribution Channels, Number of Dealers and Distributors, Margins, Production Plant, Capacity, Unique Value Offering and Others)

- SWOT Analysis of Major Players

- Pricing Analysis Based on Product Categories for Major Players

- Detailed Profiles of Major Companies

Hasbro, Inc.

Mattel, Inc.

LEGO Group

Bandai Namco Holdings

Spin Master Corp.

Fisher-Price

VTech Holdings Ltd.

Funko, Inc.

Playmates Toys

Tomy Company, Ltd.

Clementoni S.p.A.

Ravensburger AG

Mega Bloks

Jakks Pacific, Inc.

Schleich GmbH

MGA Entertainment

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- By Value, 2026–2035

- By Volume, 2026–2035

- By Average Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now