Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines Transfer Cases market reached a value of USD ~ billion based on a recent historical assessment, driven by the increasing penetration of four-wheel drive vehicles and the expansion of logistics and construction activities. Demand is supported by rising infrastructure investments and off-road vehicle usage across diverse terrains. Growth is further influenced by increasing vehicle durability requirements and the integration of advanced drivetrain technologies, particularly in light commercial and heavy-duty vehicles used in industrial and rural applications.

Metro Manila, Cebu, and Davao emerge as dominant urban centers due to concentrated automotive demand, logistics hubs, and industrial activities requiring durable vehicles. Regions with extensive agricultural and mining operations also contribute significantly, as transfer cases are essential for vehicles operating in rugged terrains. The country’s reliance on imported automotive components and the presence of established distribution networks further reinforce these locations as critical demand centers for drivetrain components and related technologies.

Market Segmentation

By Product Type

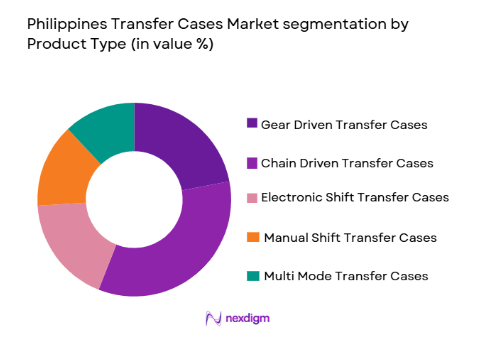

Philippines Transfer Cases market is segmented by product type into gear driven transfer cases, chain driven transfer cases, electronic shift transfer cases, manual shift transfer cases, and multi mode transfer cases. Recently, chain driven transfer cases have a dominant market share due to their cost efficiency, lower weight, and smoother operation in passenger and light commercial vehicles. Their widespread adoption is supported by growing urban mobility demand and increasing consumer preference for fuel-efficient systems. Additionally, easier maintenance and compatibility with modern drivetrain systems have strengthened their position across OEM and aftermarket applications.

By Vehicle Type

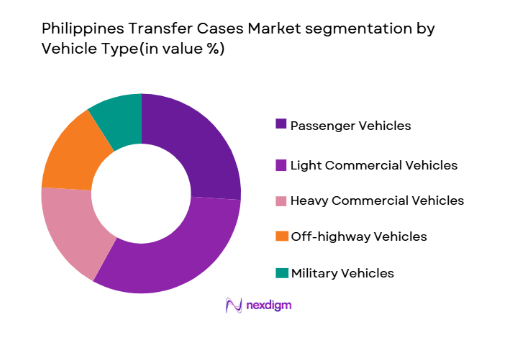

Philippines Transfer Cases market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, off-road vehicles, and military vehicles. Recently, light commercial vehicles have a dominant market share due to their extensive use in logistics, e-commerce deliveries, and small business transportation. The rapid growth of last-mile delivery services and urban distribution networks has increased reliance on these vehicles. Their adaptability to both urban and semi-rural conditions, combined with cost efficiency and fleet expansion trends, has significantly contributed to their dominance.

Competitive Landscape

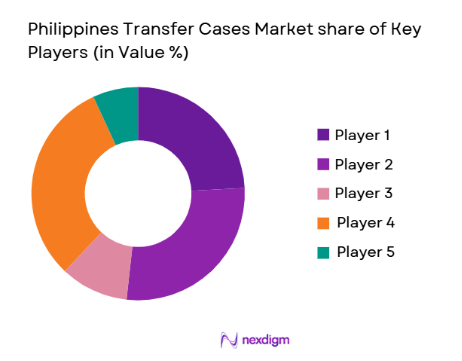

The Philippines Transfer Cases market is moderately consolidated, with global drivetrain manufacturers dominating through strong OEM partnerships and advanced technological capabilities. International suppliers maintain a competitive edge through economies of scale, while regional distributors strengthen aftermarket presence. Strategic collaborations, localization efforts, and technology integration play a critical role in shaping competition. The presence of both established global firms and emerging regional participants ensures continuous innovation and competitive pricing dynamics.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Local Distribution Strength |

| Aisin Corporation | 1965 | Japan | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

| BorgWarner Inc | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

Philippines Transfer Cases Market Analysis

Growth Drivers

Expansion of Logistics and E-Commerce Transportation Networks:

The rapid expansion of logistics and e-commerce operations across the Philippines is significantly driving demand for transfer cases, particularly in light commercial vehicles. Increased online retail activity has created a need for efficient last-mile delivery systems capable of navigating both urban and semi-rural environments. Transfer cases play a crucial role in enabling vehicles to operate under varying load conditions and terrain challenges, enhancing vehicle performance and durability. The rise in warehouse infrastructure and distribution hubs further contributes to fleet expansion, thereby increasing demand for drivetrain components. Additionally, businesses are investing in reliable vehicle systems to reduce downtime and maintenance costs, which supports the adoption of advanced transfer case technologies. As delivery networks continue to expand geographically, especially into underserved areas, vehicles equipped with robust transfer systems become essential. This trend is reinforced by increasing consumer expectations for faster delivery times and reliable logistics services. The need for operational efficiency and cost optimization also encourages fleet operators to adopt vehicles with improved drivetrain systems. Overall, logistics growth remains a fundamental driver shaping market demand.

Infrastructure Development and Off-Road Vehicle Utilization:

Ongoing infrastructure development projects across the Philippines are increasing the demand for vehicles capable of handling challenging terrains, thereby driving the transfer cases market. Construction, mining, and agricultural sectors rely heavily on vehicles equipped with durable drivetrain systems to operate efficiently in off-road conditions. Transfer cases enable power distribution between axles, making them essential for vehicles used in these industries. Government-led infrastructure initiatives are further boosting demand for heavy-duty vehicles that require reliable transfer case systems. Additionally, rural development programs are expanding accessibility to remote areas, increasing the need for off-road capable vehicles. The growth of the mining sector, which often operates in rugged and uneven terrains, also contributes significantly to market expansion. Companies are increasingly prioritizing vehicle performance and reliability to ensure operational continuity in harsh environments. Technological advancements in transfer case design are improving efficiency and reducing maintenance requirements, further encouraging adoption. As industrial activities continue to expand, the demand for advanced drivetrain solutions is expected to remain strong.

Market Challenges

Dependence on Imported Automotive Components and Supply Chain Vulnerabilities:

The Philippines Transfer Cases market faces significant challenges due to its heavy reliance on imported automotive components. Limited domestic manufacturing capabilities for precision drivetrain systems increase dependency on international suppliers, exposing the market to supply chain disruptions. Fluctuations in global trade policies and shipping costs further complicate procurement processes, leading to increased operational expenses for manufacturers and distributors. Delays in component availability can impact vehicle production timelines and aftermarket servicing. Additionally, currency fluctuations can influence import costs, affecting pricing strategies and profitability. The lack of localized production facilities also limits the ability to respond quickly to changing market demands. This dependency reduces flexibility and increases vulnerability to external economic factors. Companies must invest in supply chain diversification and strategic partnerships to mitigate these risks. However, such initiatives require substantial capital and long-term planning, posing additional challenges. Overall, supply chain constraints remain a critical barrier to market stability.

High Maintenance Costs and Technical Complexity of Advanced Systems:

The increasing adoption of advanced transfer case technologies introduces challenges related to maintenance complexity and associated costs. Modern systems often incorporate electronic controls and integrated components that require specialized knowledge for servicing and repair. This increases dependence on skilled technicians and authorized service centers, which may not be readily available in all regions. Higher maintenance costs can deter adoption, particularly among small fleet operators and individual vehicle owners. Additionally, the complexity of these systems can lead to longer repair times, impacting vehicle uptime and operational efficiency. Limited awareness regarding proper maintenance practices further exacerbates the issue. The need for specialized diagnostic tools and equipment adds to overall service expenses. As technology continues to evolve, the gap between system sophistication and available service infrastructure may widen. Addressing this challenge requires investment in training programs and service network expansion. Without such measures, market growth may face constraints due to cost and accessibility concerns.

Opportunities

Localization of Manufacturing and Component Production:

The Philippines Transfer Cases market presents significant opportunities through the localization of manufacturing and component production. Establishing domestic production facilities can reduce dependency on imports and enhance supply chain resilience. Local manufacturing can also lower production costs by minimizing transportation and import duties. Government incentives for automotive manufacturing further support this transition, encouraging investment in local production capabilities. Developing a domestic supplier base can improve responsiveness to market demands and foster innovation. Additionally, localization can create employment opportunities and contribute to economic growth. Companies that invest in local manufacturing can gain a competitive advantage through cost efficiency and faster delivery timelines. Partnerships with global technology providers can facilitate knowledge transfer and skill development. As demand for transfer cases continues to grow, localized production can play a crucial role in meeting market needs. This opportunity aligns with broader industrial development goals within the country.

Growth in Aftermarket and Vehicle Customization Demand:

The increasing trend of vehicle customization and aftermarket upgrades offers substantial opportunities for the transfer cases market. Consumers are increasingly seeking performance enhancements and modifications to improve vehicle capabilities, particularly for off-road and recreational use. The aftermarket segment provides flexibility in product offerings, allowing manufacturers to cater to diverse customer preferences. Rising disposable income and growing interest in automotive personalization are driving this trend. Additionally, fleet operators are investing in aftermarket upgrades to enhance vehicle durability and operational efficiency. The availability of a wide range of transfer case options in the aftermarket supports this demand. Technological advancements are also enabling the development of high-performance components tailored to specific use cases. Expanding distribution networks and online sales platforms further facilitate market growth in this segment. Companies can capitalize on this opportunity by offering innovative and cost-effective solutions. The aftermarket sector is expected to remain a key growth avenue for the industry.

Future Outlook

The Philippines Transfer Cases market is expected to witness steady growth driven by increasing demand for durable drivetrain systems and expanding logistics infrastructure. Technological advancements in electronic and lightweight transfer cases will enhance performance and efficiency. Government initiatives supporting automotive manufacturing and infrastructure development will further strengthen market dynamics. Rising adoption of off-road capable vehicles and aftermarket customization trends will contribute to sustained demand. Overall, the market is positioned for gradual expansion with evolving technological integration.

Major Players

- Aisin Corporation

- Magna International Inc

- BorgWarner Inc

- ZF Friedrichshafen AG

- Dana Incorporated

- GKN Automotive

- JTEKT Corporation

- Hyundai WIA Corporation

- Schaeffler AG

- American Axle & Manufacturing

- Meritor Inc

- Mitsubishi Heavy Industries

- Hitachi Astemo

- Showa Corporation

- Mahindra Systech

Key Target Audience

- Automotive OEM manufacturers

- Component distributors and suppliers

- Logistics and fleet operators

- Construction and mining companies

- Defense procurement agencies

- Automotive aftermarket retailers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market variables such as demand drivers, supply chain factors, and technological advancements were identified. These variables were analyzed to understand their impact on market growth and structural dynamics.

Step 2: Market Analysis and Construction

Comprehensive data analysis was conducted using primary and secondary sources. Market size and segmentation were constructed through triangulation of industry data and historical trends.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with industry experts and stakeholders. Feedback was incorporated to refine assumptions and ensure data accuracy.

Step 4: Research Synthesis and Final Output

All data points were synthesized into a structured report. Insights were derived to provide a clear understanding of market trends, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for four wheel drive vehicles in rural and off road applications

Expansion of construction and mining activities requiring heavy duty drivetrains

Growth in logistics sector driving commercial vehicle fleet expansion

Increasing vehicle durability requirements in diverse terrain conditions

Technological advancements in electronic transfer case systems - Market Challenges

High cost of advanced transfer case systems impacting affordability

Dependence on imported components and supply chain vulnerabilities

Limited local manufacturing capabilities for precision drivetrain parts

Maintenance complexity and higher service costs

Fluctuations in raw material prices affecting production costs - Market Opportunities

Localization of transfer case manufacturing to reduce import dependence

Growing aftermarket demand for replacement and performance upgrades

Integration of smart and electronically controlled drivetrain systems - Trends

Shift towards lightweight materials to improve fuel efficiency

Adoption of electronically controlled transfer case systems

Increasing preference for multi mode and adaptive drivetrain systems

Rising demand for rugged vehicles suited for mixed terrain conditions

Growth in aftermarket customization and performance enhancement - Government Regulations & Defense Policy

Implementation of vehicle safety and emission compliance standards

Government incentives for local automotive manufacturing

Defense procurement policies supporting utility vehicle modernization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Gear Driven Transfer Cases

Chain Driven Transfer Cases

Electronic Shift Transfer Cases

Manual Shift Transfer Cases

Multi Mode Transfer Cases - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off Road Vehicles

Military Utility Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

Retrofit Installations

Performance Upgrades

Fleet Maintenance Integration - By EndUser Segment (In Value%)

Private Vehicle Owners

Logistics and Transport Companies

Construction and Mining Firms

Defense and Government Fleets

Agriculture and Rural Mobility Users - By Procurement Channel (In Value%)

Authorized Dealerships

Independent Distributors

OEM Direct Sales

Online Automotive Platforms

Fleet Procurement Contracts - By Material / Technology (in Value %)

Aluminum Alloy Housing Systems

Cast Iron Transfer Cases

Magnesium Lightweight Systems

Electronic Control Modules Integration

Advanced Lubrication Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Depth, System Durability, Cost Competitiveness, Technology Integration, Distribution Network Strength, Aftermarket Support, OEM Partnerships, Manufacturing Capability, Innovation Pipeline, Regional Presence)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Aisin Seiki Co Ltd

Magna International Inc

BorgWarner Inc

ZF Friedrichshafen AG

GKN Automotive Limited

Dana Incorporated

American Axle and Manufacturing Holdings Inc

JTEKT Corporation

Hyundai WIA Corporation

Schaeffler AG

Meritor Inc

Showa Corporation

Mitsubishi Heavy Industries Ltd

Hitachi Astemo Ltd

Mahindra Systech

- Growing reliance of logistics companies on durable drivetrain systems for fleet efficiency

- Construction sector demand for high torque vehicles operating in harsh environments

- Increasing adoption by government and defense fleets for terrain adaptability

- Rising aftermarket engagement among private vehicle owners for performance upgrades

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now