Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines truck aggregator market reached USD ~ billion based on a recent historical assessment, supported by rapid digitalization of domestic freight matching and logistics coordination across fragmented trucking networks. Expansion of e-commerce distribution, inter-island trade logistics, and urban delivery requirements has accelerated platform adoption among small fleet operators. Government transport modernization initiatives and mobile connectivity penetration exceeding 170 million cellular subscriptions further enabled aggregator platform scalability across nationwide freight corridors and regional logistics hubs.

Metro Manila, Cebu, and Davao dominate the Philippines truck aggregator market due to dense commercial activity, port connectivity, and concentration of distribution centers serving nationwide trade flows. These metropolitan logistics clusters host major seaports handling cargo valued above USD 250 billion annually, strengthening demand for digital freight matching and trucking coordination. High e-commerce parcel throughput exceeding 900 million shipments and industrial manufacturing zones in Calabarzon reinforce aggregator platform utilization across urban and peri-urban logistics networks.

Market Segmentation

By Service Type:

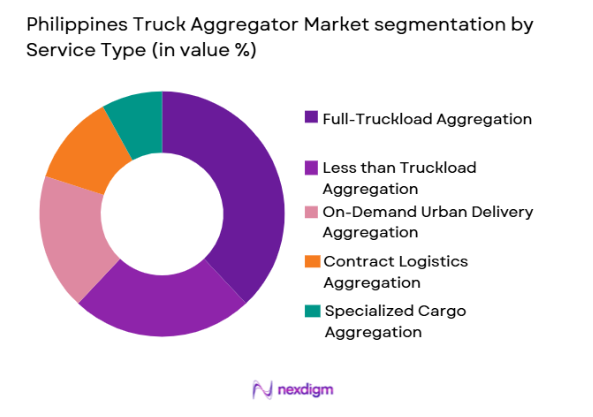

Philippines truck aggregator market is segmented by service type into full-truckload aggregation, less-than-truckload aggregation, on-demand urban delivery aggregation, contract logistics aggregation, and specialized cargo aggregation. Recently, full-truckload aggregation has a dominant market share due to strong demand from inter-city manufacturing and wholesale distribution flows across major islands. Long-haul cargo transport between ports, warehouses, and industrial estates requires dedicated truck capacity and predictable routing, favoring full-truckload digital matching platforms. Large retailers and industrial shippers prefer full-truckload bookings to ensure shipment integrity and cost efficiency across long distances. Aggregator platforms prioritize full-truckload freight due to higher transaction values and simplified operational coordination compared to partial loads. Nationwide infrastructure corridors linking Luzon, Visayas, and Mindanao further sustain demand for long-distance truck aggregation services across logistics operators and fleet owners.

By End User:

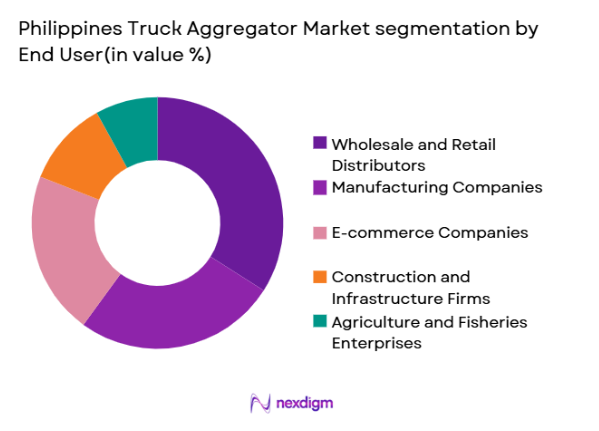

Philippines truck aggregator market is segmented by end user into manufacturing companies, wholesale and retail distributors, e-commerce companies, construction and infrastructure firms, and agriculture and fisheries enterprises. Recently, wholesale and retail distributors have a dominant market share due to continuous replenishment logistics requirements across nationwide store networks and regional distribution centers. Retail supply chains depend on predictable trucking capacity to maintain inventory movement between ports, warehouses, and stores, making aggregators essential logistics partners. Large retail chains operating thousands of outlets across islands generate recurring freight demand suitable for digital truck booking platforms. Seasonal demand fluctuations in consumer goods distribution also encourage aggregator usage for flexible fleet access. The expansion of modern trade and supermarket penetration in secondary cities reinforces distributor reliance on trucking aggregation solutions for inter-city freight flows.

Competitive Landscape

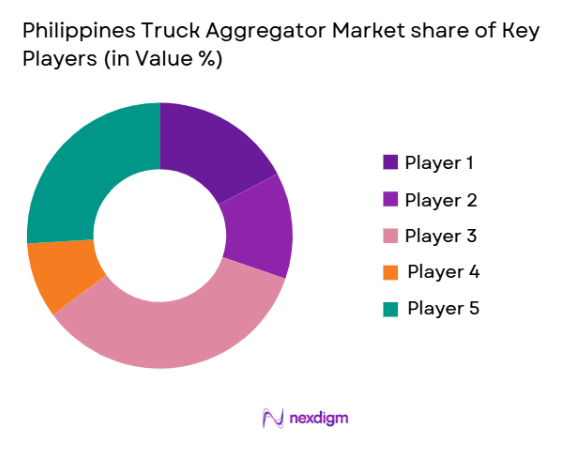

The Philippines truck aggregator market remains moderately fragmented with a mix of digital logistics startups, last-mile delivery platforms, and integrated logistics providers expanding aggregator capabilities. Market consolidation is gradually emerging as regional logistics firms partner with technology platforms to extend nationwide fleet coverage and service reliability. Major players leverage mobile-first booking systems, telematics integration, and multi-service logistics portfolios to capture enterprise freight demand and inter-island cargo flows.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Integration Depth |

| Transportify Philippines | 2016 | Manila | ~ | ~ | ~ | ~ | ~ |

| Mober Technology | 2015 | Manila | ~ | ~ | ~ | ~ | ~ |

| Lalamove Philippines | 2013 | Manila | ~ | ~ | ~ | ~ | ~ |

| Fast Logistics Group | 1972 | Manila | ~ | ~ | ~ | ~ | ~ |

| Ninja Van Philippines | 2014 | Manila | ~ | ~ | ~ | ~ | ~ |

Philippines Truck Aggregator Market Analysis

Growth Drivers

Ecommerce Logistics Expansion Across Archipelagic Supply Chains:

The rapid growth of digital commerce distribution networks across island geographies has significantly increased dependence on coordinated trucking capacity across ports, warehouses, and urban fulfillment centers. The Philippines processes hundreds of millions of parcels annually, creating sustained demand for first-mile and mid-mile freight transport between regional logistics nodes. Aggregator platforms enable flexible truck sourcing to manage fluctuating shipment volumes generated by online retail campaigns and nationwide promotions. Small fleet operators benefit from digital marketplaces that reduce idle capacity and increase trip utilization across inter-city corridors. Large retailers and logistics providers rely on aggregators to supplement contracted fleets during peak demand periods and seasonal spikes. Geographic fragmentation across more than seven thousand islands requires dynamic routing coordination that traditional brokerage models struggle to provide. Mobile connectivity and digital payments adoption have lowered entry barriers for truck operators joining aggregator platforms. The combination of e-commerce scale and logistical complexity has structurally embedded aggregation platforms into domestic freight distribution ecosystems. Continuous expansion of regional fulfillment infrastructure further strengthens long-term dependence on digital truck aggregation solutions.

Fragmented Trucking Industry Requiring Digital Capacity Matching:

The domestic trucking sector consists predominantly of small and medium operators owning limited vehicle fleets, creating inefficiencies in freight matching and asset utilization across supply chains. Aggregator platforms address structural fragmentation by digitally connecting thousands of independent truckers with shippers requiring flexible transport capacity. Many operators historically relied on manual brokerage networks that lacked transparency and predictable pricing mechanisms. Digital aggregation reduces empty backhaul journeys by matching return loads and optimizing route assignments across geographic regions. Fleet visibility tools and telematics integration improve reliability and performance monitoring, encouraging enterprise adoption of aggregator services. The platform model also facilitates standardized pricing benchmarks that reduce negotiation friction between shippers and carriers. Increasing fuel and operating costs incentivize truck owners to maximize utilization through continuous load availability provided by aggregators. Government logistics modernization policies support digitalization of freight operations, indirectly promoting aggregator adoption. Over time, structural inefficiencies in fragmented trucking markets continue to drive sustained growth of aggregation platforms.

Market Challenges

Digital Adoption Barriers Among Small Fleet Operators:

A large proportion of trucking operators remain micro-enterprises with limited technological familiarity, constraining onboarding and effective utilization of digital aggregation platforms across the country. Many drivers and fleet owners rely on traditional brokerage relationships and informal booking channels that are deeply embedded in local logistics ecosystems. Smartphone usage is widespread, yet operational literacy in logistics applications and digital documentation remains uneven across regions. Training requirements and resistance to transparent pricing structures slow platform migration among independent operators. Payment settlement processes through digital wallets or banking systems also present adoption hurdles for cash-dependent truckers. Limited trust in platform intermediaries and concerns over service fees further discourage participation among smaller fleets. Aggregator companies must invest heavily in onboarding support, education programs, and offline engagement to expand supply networks. Without sufficient truck participation, platform liquidity and load availability can be constrained in secondary logistics corridors. These structural adoption barriers slow scaling efficiency despite strong demand from shippers.

Infrastructure and Connectivity Constraints Across Island Logistics Corridors:

The archipelagic geography of the country imposes logistical complexities that directly affect aggregator service reliability and operational efficiency across trucking routes. Road infrastructure quality varies significantly between metropolitan corridors and rural island regions, increasing transit time unpredictability and vehicle operating costs. Ferry schedules and port congestion create intermodal bottlenecks that disrupt coordinated truck dispatching and delivery timelines. Cellular connectivity gaps persist in remote logistics routes, limiting real-time tracking and communication between drivers and platforms. Aggregator algorithms depend on consistent location data and route optimization inputs that become unreliable in low-coverage regions. Weather disruptions such as typhoons frequently interrupt road and maritime transport, reducing predictability of trucking operations. Infrastructure constraints also increase maintenance costs and vehicle downtime among fleet operators participating in platforms. These geographic and structural challenges reduce efficiency advantages typically associated with digital freight aggregation. As a result, nationwide platform scalability faces persistent operational limitations.

Opportunities

Inter-Island Freight Consolidation and Multimodal Aggregation Platforms: The

fragmented island geography presents significant opportunity for platforms that integrate trucking aggregation with maritime scheduling and cargo consolidation services across domestic trade routes. Coordinated multimodal aggregation can streamline cargo transfers between trucks, ferries, and regional distribution hubs, improving reliability and cost efficiency. Shippers transporting goods across Luzon, Visayas, and Mindanao require integrated logistics visibility that single-mode aggregators cannot fully provide. Platforms combining truck booking with port scheduling and cargo consolidation can capture high-value inter-island freight flows. Such integration reduces dwell time at ports and improves utilization of both trucking and maritime capacity. Digital documentation and cargo tracking across modes enhance supply chain transparency for industrial and retail clients. Government focus on domestic shipping modernization supports development of integrated logistics platforms. Inter-island aggregation services also enable participation of smaller regional fleets in national freight networks. This multimodal aggregation opportunity remains largely untapped relative to urban delivery segments.

Embedded Logistics Financing and Fleet Modernization Services:

Aggregator platforms possess transactional visibility into fleet utilization and revenue streams, enabling development of financing solutions tailored to small trucking operators. Access to credit remains a major constraint for independent fleet owners seeking vehicle upgrades or expansion. Platforms can leverage booking data to assess creditworthiness and offer asset financing, fuel credit, and insurance products integrated with logistics operations. Such embedded services improve fleet reliability and capacity availability across aggregation networks. Financing support also incentivizes operator loyalty to specific platforms, strengthening supply stability. Modernized fleets reduce breakdown risk and improve service quality for enterprise shippers using aggregator marketplaces. Integration of financial services diversifies platform revenue beyond transaction commissions. Partnerships with banks and fintech providers can accelerate rollout of fleet financing solutions nationwide. This opportunity enhances both market penetration and operational efficiency of aggregation platforms.

Future Outlook

The Philippines truck aggregator market is expected to experience sustained expansion driven by continued e-commerce logistics growth, inter-island trade intensification, and nationwide supply chain digitalization. Technology adoption including AI-based routing, telematics analytics, and integrated logistics platforms will enhance operational efficiency. Infrastructure investments in ports and highways will improve trucking reliability across regions. Regulatory support for logistics modernization and digital transport documentation will further accelerate aggregator penetration across domestic freight ecosystems.

Major Players

- TransportifyPhilippines

- Mober Technology

- Lalamove Philippines

- Ninja Van Philippines

- Fast Logistics Group

- 2GO Group

- XDE Logistics

- AP Cargo Logistics Network

- J&T Express Philippines

- GrabExpress Philippines

- DHL Supply Chain Philippines

- DB Schenker Philippines

- Maersk Logistics Philippines

- Kuehne+Nagel Philippines

- Royal Cargo

Key Target Audience

- Trucking and fleet operators

- Logistics and freightforwarding companies

- E-commerce and retail companies

- Manufacturing and industrial companies

- Construction and infrastructure firms

- Agriculture and fisheries exporters

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including fleet size distribution, freight demand patterns, digital platform adoption, logistics infrastructure intensity, and end-user industry demand were identified. These variables formed the analytical foundation for assessing platform penetration and market value generation across trucking aggregation services nationwide.

Step 2: Market Analysis and Construction

Supply-side evaluation of aggregator platforms and trucking operators was combined with demand-side analysis across retail, manufacturing, and logistics sectors. Market size construction integrated freight transaction volumes, platform commission structures, and service utilization patterns across major logistics corridors and urban clusters.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from logistics providers, fleet operators, and digital freight platforms were consulted to validate assumptions regarding pricing, adoption barriers, and operational structures. Regional logistics specialists confirmed segmentation logic and realistic distribution of platform utilization across end-user industries.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into market sizing models and competitive analysis frameworks. Cross-verification ensured consistency between platform supply capacity, freight demand indicators, and logistics infrastructure constraints to produce the final Philippines truck aggregator market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid ecommerce logistics expansion across archipelagic regions

Fragmented trucking sector requiring digital aggregation

Rising fuel and operating cost pressures on fleet operators

Infrastructure modernization and inter-island trade growth

Government digitalization initiatives in transport and logistics - Market Challenges

Limited digital adoption among small trucking operators

Connectivity gaps in remote island logistics corridors

Regulatory fragmentation across local jurisdictions

Low platform loyalty and multi-homing behavior

Payment security and trust issues in digital freight booking - Market Opportunities

Inter-island freight visibility and consolidation platforms

SME fleet financing and embedded logistics services

Cold chain and specialized cargo aggregation networks - Trends

AI-enabled dynamic pricing and load optimization

Integration of fintech and digital payments in freight platforms

Telematics-driven fleet performance analytics

Sustainability and fuel-efficiency tracking solutions

Marketplace consolidation and strategic partnerships - Government Regulations & Defense Policy

National logistics and supply chain modernization programs

Digital transport documentation and e-governance initiatives

Road freight safety and vehicle monitoring regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Matching Platforms

Fleet Management & Telematics Systems

Route Optimization & Dispatch Systems

Load Consolidation & Brokerage Platforms

End-to-End Logistics Aggregation Suites - By Platform Type (In Value%)

Mobile App-Based Aggregators

Web-Based Aggregation Portals

API-Integrated Enterprise Platforms

Cloud-Native Logistics Platforms

AI-Driven Smart Dispatch Platforms - By Fitment Type (In Value%)

Standalone Aggregator Platforms

Integrated Transport Management Suites

Embedded OEM Telematics Integration

Third-Party Logistics Integration

Custom Enterprise Deployments - By EndUser Segment (In Value%)

SME Truck Operators

Large Fleet Operators

Freight Forwarders & 3PL Providers

Ecommerce & Retail Shippers

Construction & Industrial Logistics Firms - By Procurement Channel (In Value%)

Direct Platform Subscription

Enterprise SaaS Contracts

Logistics Marketplace Enrollment

Government or Institutional Tenders

Channel Partner Resellers - By Material / Technology (in Value %)

GPS & IoT Telematics Integration

AI-Based Load Matching Algorithms

Cloud Computing Infrastructure

Blockchain Freight Documentation

Data Analytics & Predictive Optimization

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Platform Capability, Fleet Coverage, Pricing Model, Technology Stack, Integration Capability, Service Portfolio, Geographic Reach, Customer Segment Focus, Data Analytics Capability, Partnership Ecosystem)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Transportify Philippines

Mober Technology

Ninja Van Philippines

Lalamove Philippines

2GO Group

AP Cargo Logistics Network

J&T Express Philippines

GrabExpress Philippines

XDE Logistics

Royal Cargo

Fast Logistics Group

DHL Supply Chain Philippines

DB Schenker Philippines

Maersk Logistics Philippines

Kuehne+Nagel Philippines

- SME operators adopt aggregators to reduce empty backhauls

- Large fleets leverage platforms for route and asset utilization

- Ecommerce shippers require nationwide scalable freight access

- Industrial sectors demand reliable inter-island cargo capacity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now