Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Philippines warehousing aggregator market is valued at approximately USD ~ billion, with growth driven by the expansion of the retail, e-commerce, and manufacturing sectors. Increased demand for efficient supply chain solutions and the rise of global trade have further fueled the need for modern, integrated warehousing services. As the country’s logistics infrastructure continues to improve, businesses are increasingly turning to third-party logistics providers for storage and distribution, resulting in sustained market growth.

Metro Manila, Cebu, and Davao are the dominant cities in the Philippines warehousing market. Metro Manila, being the country’s economic hub, hosts numerous logistics and warehousing facilities catering to diverse industries. Cebu’s strategic location and growing infrastructure make it an ideal logistics center for the Visayas region. Davao, with its proximity to key export sectors and ports, serves as an essential warehousing and distribution center for Mindanao. These cities are central to the growth of the warehousing aggregator market due to their strategic locations and developing transportation networks.

Market Segmentation

By Product Type

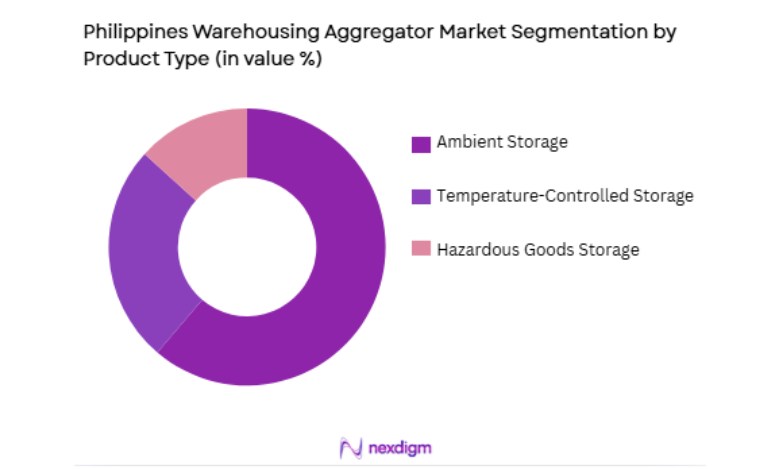

The Philippines warehousing aggregator market is segmented by product type into ambient storage, temperature-controlled storage, and hazardous goods storage. Recently, ambient storage has gained the largest market share due to the growing demand for non-perishable consumer goods in e-commerce, retail, and manufacturing sectors. Ambient storage requires less specialized infrastructure and is more cost-effective, which aligns with the increasing need for fast and efficient inventory management. The expansion of e-commerce and the availability of large warehouse spaces in Metro Manila and Cebu further contribute to the dominance of this sub-segment.

By Warehouse Size

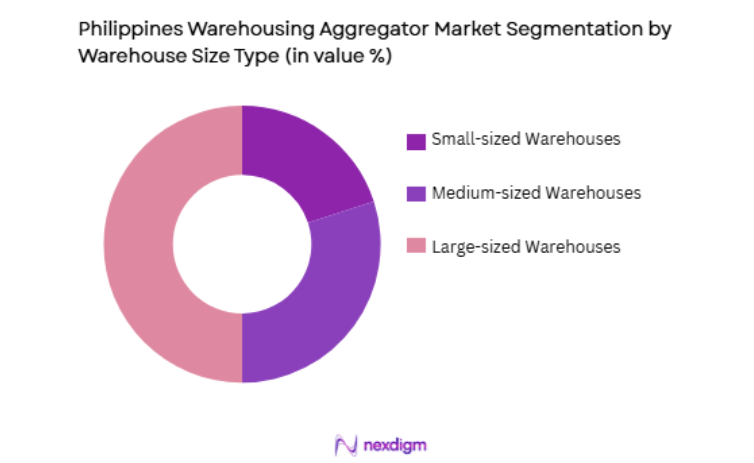

The Philippines warehousing aggregator market is segmented by warehouse size into small, medium, and large-sized warehouses. Large-sized warehouses are the dominant sub-segment due to the demand from businesses requiring substantial storage capacity for high-volume goods, particularly in the e-commerce and manufacturing sectors. These warehouses provide ample space, reduce operational costs, and offer economies of scale, which are particularly beneficial for logistics operators managing large inventories. Metro Manila and Cebu are key locations for large warehouses due to their strategic transport links and proximity to major industries.

Competitive Landscape

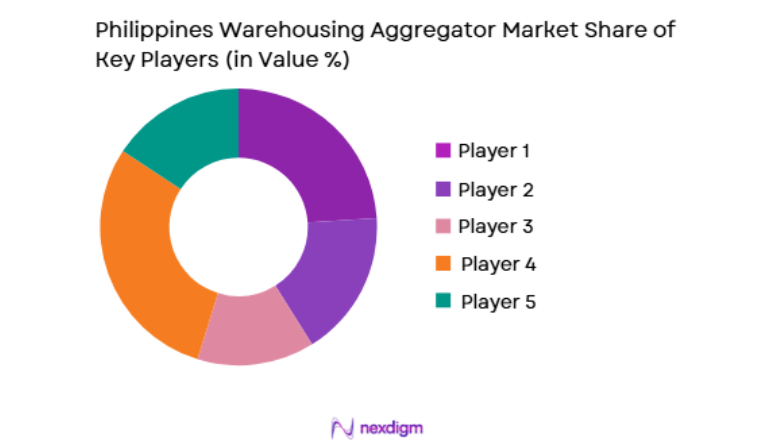

The competitive landscape of the Philippines warehousing aggregator market is marked by a mix of local players and multinational companies. As demand for warehousing services grows, consolidation in the industry is expected, with larger companies acquiring smaller competitors to increase capacity and geographic reach. Companies are also integrating technology into their operations, utilizing automation, AI, and IoT systems to enhance operational efficiency and meet the increasing demand for faster delivery times. Players in the market are expanding their offerings to include value-added services such as inventory management and distribution solutions to stay competitive.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| 2GO Logistics | 2004 | Manila | ~ | ~ | ~ | ~ | ~ |

| APL Logistics | 2000 | Manila | ~ | ~ | ~ | ~ | ~ |

| XPO Logistics | 1989 | Quezon City | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Makati | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Manila | ~ | ~ | ~ | ~ | ~ |

Philippines Warehousing Aggregator Market Analysis

Growth Drivers

Expansion of E-commerce in the Philippines

The rapid growth of e-commerce in the Philippines is a major driver of the warehousing aggregator market. As more consumers turn to online shopping platforms, businesses are increasingly investing in efficient warehousing solutions to manage the growing volume of goods and ensure faster delivery. Leading e-commerce players, such as Lazada, Shopee, and Zalora, are expanding their operations in the Philippines, driving demand for large-scale warehouses and distribution centers. The need for faster fulfillment, particularly for consumer electronics, fashion, and groceries, is leading businesses to seek third-party warehousing services that can handle inventory management and delivery logistics efficiently. This trend is supported by increasing internet penetration and the shift toward digital transactions, contributing significantly to the growth of warehousing aggregation services.

Government Infrastructure Initiatives

The Philippines government has prioritized the development of logistics infrastructure under the “Build, Build, Build” program, which is accelerating the growth of the warehousing sector. Investments in key infrastructure projects, including roads, bridges, and port facilities, are enhancing the country’s transportation network, making it easier to transport goods across the country. This infrastructure development is crucial in addressing the growing demand for warehousing services in major cities like Metro Manila and Cebu. The improvement of key logistics hubs is creating an environment conducive to warehousing growth, attracting both local and international players to expand their operations. Government policies that support foreign investments in logistics infrastructure also present opportunities for warehousing aggregators to grow their market presence.

Market Challenges

High Real Estate Costs

One of the key challenges in the Philippines warehousing aggregator market is the rising cost of real estate, particularly in prime logistics hubs such as Metro Manila and Cebu. With the growing demand for warehouse space, rental prices in these areas have surged, making it difficult for warehousing companies to secure affordable facilities. Additionally, limited land availability near major transportation hubs has driven up property prices, making it challenging for businesses to scale their operations. The high cost of land, coupled with the need for large, specialized warehouse spaces, increases operational costs for warehousing operators. To mitigate this challenge, companies must find innovative ways to optimize existing warehouse space and explore alternative locations that offer more cost-effective solutions.

Labor and Skill Shortages in the Warehousing Sector

The Philippines warehousing market faces challenges related to labor shortages and skill gaps in the workforce. As the demand for advanced warehousing solutions grows, there is an increasing need for skilled workers to operate automated systems, manage inventory, and maintain technology. However, there is a shortage of workers with the necessary skills to handle complex logistics operations, particularly in the areas of robotics, data analytics, and supply chain management. This shortage is leading to higher labor costs and longer recruitment cycles, which can affect the ability of warehousing aggregators to meet customer demands. Companies must invest in training and development programs to ensure their workforce can adapt to new technologies and meet the growing requirements of the logistics sector.

Opportunities

Adoption of Automation and Smart Warehousing Solutions

One of the most significant opportunities in the Philippines warehousing aggregator market lies in the adoption of automation and smart warehousing technologies. As the demand for faster and more accurate order fulfillment continues to rise, businesses are increasingly investing in technologies like robotics, IoT, and AI to optimize their warehousing operations. Automated storage and retrieval systems, robotics for picking and packing, and real-time inventory tracking are transforming the efficiency and accuracy of warehouse operations. The integration of cloud-based warehouse management systems (WMS) also enables businesses to streamline inventory management, reduce errors, and increase operational efficiency. As these technologies become more affordable and accessible, there is significant potential for warehousing aggregators to gain a competitive edge by offering advanced, automated solutions to their clients.

Sustainability in Warehousing and Green Logistics Solutions

With increasing awareness of environmental issues, there is growing demand for sustainable warehousing and green logistics solutions in the Philippines. Businesses are increasingly focused on reducing their carbon footprint and adopting environmentally friendly practices within their supply chains. This trend presents opportunities for warehousing aggregators to differentiate themselves by offering green logistics solutions, such as energy-efficient warehouses, solar-powered facilities, and sustainable packaging materials. Additionally, the Philippine government’s push toward green infrastructure and sustainability initiatives provides incentives for businesses to invest in eco-friendly solutions. Warehousing companies that adopt sustainable practices not only help reduce environmental impact but also attract clients looking to align their supply chains with sustainable business practices.

Future Outlook

The future outlook for the Philippines warehousing aggregator market is optimistic, with continued growth expected driven by the rise of e-commerce, the expansion of infrastructure, and technological advancements in logistics. Over the next five years, the demand for automated warehousing solutions will increase, as businesses seek to improve supply chain efficiency and reduce operational costs. The ongoing government investment in logistics infrastructure will support the development of key transportation hubs, further enhancing the competitiveness of warehousing services. Additionally, the growing emphasis on sustainability in the logistics sector presents new opportunities for companies to differentiate themselves and meet the demands of environmentally conscious customers.

Major Players

- 2GO Logistics

- APL Logistics

- XPO Logistics

- DB Schenker

- DHL Supply Chain

- J.B. Hunt Transport Services

- UPS Supply Chain Solutions

- C.H. Robinson

- Ryder Supply Chain Solutions

- Lineage Logistics

- Scania Logistics

- Kuehne + Nagel

- Maersk Logistics

- Geodis

- FedEx Logistics

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce companies

- Logistics service providers

- Retailers and wholesalers

- Manufacturing companies

- Industrial parks and real estate developers

- Freight forwarding companies

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying critical market drivers such as technological advancements, demand for warehousing, e-commerce growth, and government infrastructure initiatives.

Step 2: Market Analysis and Construction

The analysis of market conditions and segmentation allows for the construction of a detailed model that highlights the current trends and future growth areas in the warehousing aggregator market.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts validate market assumptions, providing insights into the validity of the current trends and expected future developments.

Step 4: Research Synthesis and Final Output

The final report integrates the collected data, providing actionable insights and recommendations based on the comprehensive market analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E-commerce Sector

Increasing Demand for Warehouse Automation

Government Support for Logistics Infrastructure Development - Market Challenges

High Initial Capital Investment

Technological Integration Challenges

Labor Shortage and Skills Gap - Market Opportunities

Growth in Real-time Inventory Management Solutions

Expansion of Warehouse Automation Technologies

Increase in Cross-border E-commerce Demand - Trends

Adoption of AI and Robotics in Warehousing

Shift Towards Green and Sustainable Technologies

Use of Real-time Data Analytics in Warehousing Operations - Government regulations

Warehouse Safety and Compliance Regulations

Environmental Sustainability Regulations

Regulations on Data Protection and Privacy - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Inventory Management Systems

Order Fulfillment Systems

Warehouse Management Systems

Automated Storage & Retrieval Systems

Warehouse Control Systems - By Platform Type (In Value%)

Cloud-based Platforms

On-premise Platforms

Hybrid Platforms

Mobile Platforms

Integrated Platforms - By Fitment Type (In Value%)

Standalone Solutions

Modular Solutions

Cloud-based Solutions

Hybrid Solutions

Custom Solutions - By End User Segment (In Value%)

E-commerce Retailers

Third-party Logistics Providers

Manufacturers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Technological Innovation, Operational Efficiency, Service Delivery Speed, Scalability, Market Penetration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DB Schenker

DHL Supply Chain

Agility Logistics

Kuehne + Nagel

Siemens Logistics

XPO Logistics

FedEx Logistics

Manhattan Associates

Dematic

Honeywell Intelligrated

JDA Software

Savills

GLP

Cushman & Wakefield

DHL

- E-commerce Companies Seeking Efficient Fulfillment Solutions

- Logistics Providers Looking for Cost-effective Automation

- Manufacturers Seeking Advanced Warehouse Management Systems

- Food & Beverage Industry Requiring Temperature-controlled Storage

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now