Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Philippines wealth management market managed approximately USD ~ billion in assets under management, driven by growth in high-net-worth individuals, rising mutual fund and unit-linked insurance investments, and expanding digital investment platforms reported by the Bangko Sentral ng Pilipinas and the Philippine Investment Funds Association. Increasing bank-led advisory services, discretionary portfolio management adoption, and offshore diversification among affluent households further accelerated managed asset inflows across equities, fixed income, and alternative investment products distributed through private banking and digital channels.

Metro Manila dominates the Philippines wealth management market due to concentration of private banks, asset managers, brokerage firms, and affluent households supported by corporate headquarters and financial infrastructure. Cebu and Davao are emerging regional wealth hubs as entrepreneurial growth, real estate development, and family-owned business expansion increase investable assets. Overseas Filipino wealth inflows into these cities strengthen demand for advisory, estate planning, and portfolio diversification services delivered through both relationship-based and digital wealth platforms.

Market Segmentation

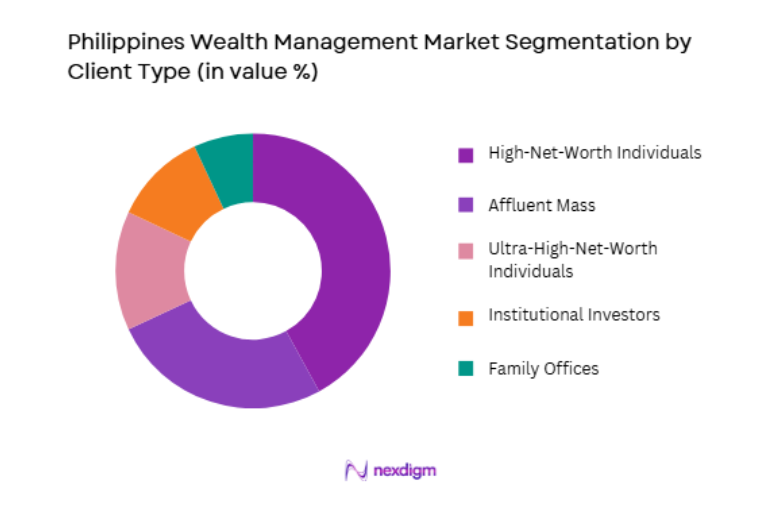

By Client Type

Philippines wealth management market is segmented by client type into high-net-worth individuals, ultra-high-net-worth individuals, affluent mass segment, family offices, and institutional investors. Recently, high-net-worth individuals have a dominant market share due to factors such as rapid growth in entrepreneurial wealth, rising professional incomes, and expanding bank-led advisory penetration targeting this segment. Private banks and asset managers prioritize HNWI portfolios through tailored discretionary mandates and structured investment products, while digital wealth platforms provide scalable portfolio management solutions suited to their asset levels. This segment also shows strong demand for diversification into global equities and alternative assets, reinforcing advisory engagement and managed asset accumulation nationwide.

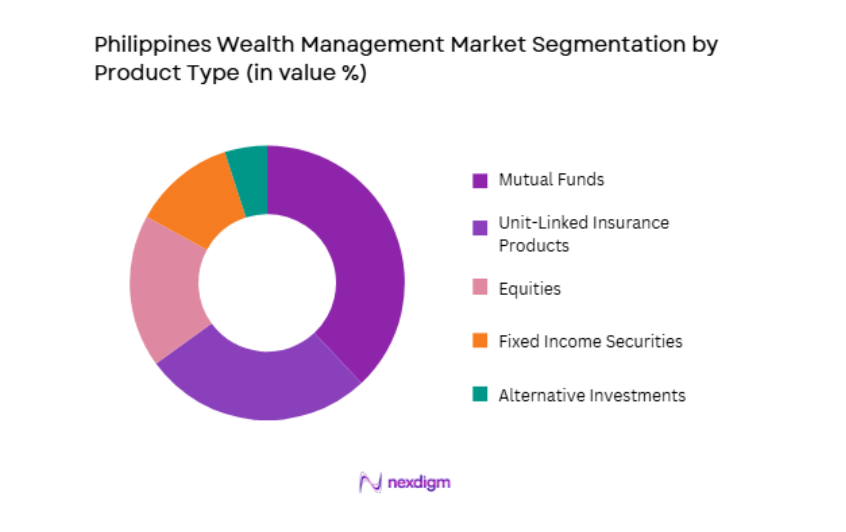

By Product Type

Philippines wealth management market is segmented by product type into mutual funds, unit-linked insurance products, equities, fixed income securities, and alternative investments. Recently, mutual funds have a dominant market share due to factors such as accessibility through banks, diversified portfolios, and regulatory familiarity among investors. Banks distribute mutual funds extensively through branch and digital channels, enabling affluent and HNWI clients to allocate across domestic and global asset classes without direct market trading complexity. Professional fund management and liquidity features further enhance investor preference for managed collective investment structures within diversified wealth portfolios nationwide.

Competitive Landscape

The Philippines wealth management market is moderately concentrated, led by universal banks and international asset managers offering private banking, discretionary portfolio management, and investment distribution services. Bank-affiliated asset managers dominate through branch networks and relationship managers, while global firms serve offshore diversification needs of affluent Filipinos. Digital wealth platforms are expanding access among emerging affluent segments, but traditional advisory relationships remain central for high-value portfolios and estate planning services.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AUM |

| BDO Private Bank | 1976 | Makati | ~ | ~ | ~ | ~ | ~ |

| BPI Wealth | 1994 | Makati | ~ | ~ | ~ | ~ | ~ |

| Metrobank Trust Banking | 1962 | Makati | ~ | ~ | ~ | ~ | ~ |

| Sun Life Asset Management | 2011 | Taguig | ~ | ~ | ~ | ~ | ~ |

| ATRAM Trust Corporation | 2010 | Makati | ~ | ~ | ~ | ~ | ~ |

Philippines Wealth Management Market Analysis

Growth Drivers

Rapid expansion of affluent and high-net-worth population with investable financial assets

The Philippines has experienced sustained growth in entrepreneurial wealth creation, professional income expansion, and family-owned business valuation increases that collectively enlarge the pool of individuals requiring formal wealth management services, particularly within urban economic centers where corporate activity and capital accumulation are concentrated. Rising property values and liquidity events from business sales or generational succession further convert illiquid wealth into financial assets requiring portfolio allocation and advisory oversight. High-net-worth households increasingly seek diversification beyond domestic bank deposits and real estate into equities, funds, and global securities, driving demand for structured wealth management solutions. Financial literacy improvements and exposure to international investment trends encourage Filipino investors to adopt managed portfolios and professional advisory services to optimize risk-adjusted returns. Banks and asset managers respond by expanding private banking and discretionary portfolio offerings tailored to varying wealth tiers, increasing penetration across emerging affluent segments. Overseas income flows and repatriated savings from expatriate Filipinos further augment investable asset pools managed domestically.

Digital investment platforms and bank-led wealth advisory integration

Philippine banks and asset managers increasingly integrate digital investment platforms within online banking ecosystems, enabling clients to access portfolio management, mutual funds, and advisory services through familiar financial interfaces, which significantly enhances participation in wealth products among digitally engaged consumers. Digital onboarding and automated suitability assessments reduce friction in investment account opening, allowing banks to scale wealth distribution beyond traditional relationship-manager channels into self-directed and hybrid advisory models. Mobile-based portfolio tracking, performance analytics, and automated rebalancing tools improve transparency and engagement, encouraging investors to maintain diversified portfolios managed through institutional platforms. Banks leverage existing customer data to personalize investment recommendations and cross-sell wealth products to depositors transitioning from savings accounts to investment portfolios.

Market Challenges

Limited depth of domestic capital markets and product diversification constraints

The Philippines wealth management market faces structural constraints arising from relatively shallow domestic capital markets, limited listed securities diversity, and concentration in a narrow set of large corporations, which restricts portfolio diversification opportunities within local investment options available to wealth managers and clients. Asset managers must often rely on offshore funds and global securities to achieve diversification, introducing currency risk, regulatory complexity, and additional costs that can deter some investors from allocating significant portions of wealth into managed portfolios. The limited availability of alternative investments such as private equity, venture capital, infrastructure funds, and real estate investment trusts reduces opportunities for sophisticated portfolio construction within domestic wealth management offerings. Investors accustomed to bank deposits and real estate holdings may perceive capital market investments as volatile or unfamiliar, further constraining adoption of diversified wealth strategies. Liquidity constraints in local bond and equity markets can also impact portfolio execution and pricing efficiency for large mandates.

Low financial advisory penetration and investor trust gaps outside metropolitan centers

Wealth management services in the Philippines remain concentrated in major urban areas, while large segments of affluent and emerging affluent individuals in secondary cities and provincial regions lack exposure to professional financial advisory services and diversified investment products, limiting nationwide market penetration. Many investors outside metropolitan hubs rely primarily on bank deposits, informal investments, or real estate due to limited access to certified advisors and wealth platforms capable of delivering personalized portfolio management. Cultural preference for tangible assets and intergenerational business ownership also reduces willingness to allocate wealth into financial instruments managed by external institutions. Trust gaps regarding advisory transparency, fees, and investment risk persist among investors unfamiliar with wealth management practices, slowing adoption beyond established financial centers.

Opportunities

Growth of offshore and global investment allocation among Filipino investors

Filipino high-net-worth and affluent investors increasingly seek international diversification to hedge domestic market concentration and currency risk, creating substantial opportunity for wealth managers to expand offshore portfolio offerings including global equities, bonds, funds, and alternative investments accessed through cross-border platforms and custodial arrangements. Regulatory frameworks permitting outward investment and global fund distribution enable asset managers to construct internationally diversified portfolios tailored to client risk profiles and return objectives. Offshore investments also appeal to expatriate Filipinos managing wealth across jurisdictions, reinforcing demand for globally integrated wealth advisory services. Wealth managers can differentiate through access to international asset classes, research expertise, and currency management strategies supporting global diversification.

Emergence of family office and intergenerational wealth planning services

The maturation of entrepreneurial wealth in the Philippines is generating demand for sophisticated family office structures and intergenerational wealth planning services addressing succession, governance, tax optimization, and legacy preservation for multi-generational business families and ultra-high-net-worth households. Wealth managers and private banks have opportunities to establish dedicated family office advisory platforms integrating investment management, estate planning, philanthropic structuring, and risk management services tailored to complex family wealth needs. As business founders transition ownership to next-generation leaders, demand for structured governance frameworks and long-term asset allocation strategies increases. Family offices also require access to private markets and bespoke investment opportunities beyond traditional portfolios, expanding advisory scope and fee potential for wealth managers. Growing awareness of global family office models encourages Philippine wealth holders to formalize asset management and succession planning. Regulatory and legal developments supporting trusts and estate structures further facilitate this segment’s expansion.

Future Outlook

The Philippines wealth management market is expected to expand steadily as affluent population growth, digital investment platforms, and offshore diversification demand strengthen managed asset inflows. Private banks and asset managers will continue integrating digital advisory tools with relationship-based services to reach emerging affluent clients. Expansion of global investment access and family office solutions will deepen portfolio sophistication. Regulatory support for capital market development and digital finance will further enhance wealth participation across metropolitan and regional investor segments.

Major Players

- BDO Private Bank

- BPI Wealth

- Metrobank Trust Banking

- Sun Life Asset Management

- ATRAM Trust Corporation

- Philippine Trust Company

- HSBC Private Banking Philippines

- Security Bank Wealth

- EastWest Bank Wealth Management

- UnionBank Wealth

- PNB Trust Banking

- Manulife Asset Management Philippines

- Insular Life Investment Management

- Allianz Global Investors Philippines

- First Metro Asset Management

Key Target Audience

- Private banks

- Asset management firms

- Family offices

- High-net-worth individuals

- Investments and venture capitalist firms

- Government and regulatory bodies

- Brokerage firms

- Digital investment platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables including investable assets, client segments, product categories, advisory channels, and regulatory frameworks were identified through financial institution disclosures and capital market data. Market scope was defined to include managed financial assets under advisory or discretionary mandates. Wealth distribution drivers and demographic indicators were mapped to investment participation.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using banking AUM reports, fund industry statistics, and trust asset disclosures. Client tier distribution and product allocation patterns were triangulated across institutions. Competitive positioning and advisory models were analyzed to determine structural market characteristics.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through discussions with private bankers, asset managers, and investment advisors regarding client behavior, portfolio allocation, and digital wealth adoption trends. Assumptions on segment dominance and product preferences were refined. Market share structures were cross-checked against industry insights.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were synthesized into an integrated analysis covering market size, segmentation, drivers, challenges, and opportunities. Strategic implications and outlook were derived from structural trends in wealth creation and investment behavior. Final outputs were reviewed for consistency and analytical robustness.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising affluent and high net worth population from entrepreneurship and remittances

Expansion of universal bank wealth divisions and private banking services

Growing investor interest in diversified global and alternative assets - Market Challenges

Limited penetration of formal wealth advisory beyond top-tier clients

Shortage of certified financial advisors and relationship managers

Market volatility affecting investor confidence and asset allocation - Market Opportunities

Digital wealth platforms targeting emerging affluent investors

Cross-border wealth structuring and offshore investment services

Sharia-compliant and sustainable investment offerings - Trends

Shift toward goal-based and holistic financial planning models

Integration of digital portfolio reporting and client engagement tools - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory and Financial Planning Services

Trust and Estate Planning Services

Alternative Investment Advisory

Retirement and Pension Solutions - By Platform Type (In Value%)

Private Banking Platforms

Independent Wealth Advisory Platforms

Digital Wealth and Robo-advisory Platforms

Brokerage-led Wealth Platforms

Universal Bank Wealth Platforms - By Fitment Type (In Value%)

Onshore Wealth Management

Offshore Wealth Management

Hybrid Advisory Models

Fully Digital Wealth Solutions - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Affluent Mass Segment

- Market Share Analysis

- Cross Comparison Parameters (Client Segment Focus, Asset Class Coverage, Advisory Model, Digital Platform Capability, Pricing Structure, Relationship Management Depth, Geographic Investment Access, Alternative Investment Capability, Reporting Transparency, Regulatory Compliance Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BDO Private Bank

BPI Wealth

Metrobank Trust Banking Group

Security Bank Wealth Management

UnionBank Wealth and Brokerage

RCBC Trust and Investments

China Bank Trust and Asset Management

AIA Philippines Wealth

Sun Life Asset Management Philippines

Manulife Investment Management Philippines

ATR Asset Management

First Metro Asset Management

Philam Asset Management

SBG Securities Wealth

COL Financial Wealth Advisory

- Entrepreneurs and business owners seeking succession and liquidity planning

- Affluent professionals increasing participation in managed investments

- Family offices formalizing multi-generational wealth governance

- Overseas Filipinos allocating savings into domestic investment vehicles

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now