Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Qatar 3PL market recorded a market size of approximately USD ~ billion, supported by expanding logistics outsourcing activities and increasing trade flows across the Gulf region. Growth is driven by the country’s strategic investments in transportation infrastructure, free trade zones, and logistics parks that enhance freight efficiency. Rising e-commerce activity, growing imports of consumer goods, and large infrastructure development programs further accelerate demand for third-party logistics services including warehousing, freight forwarding, and integrated supply chain management solutions.

Based on a recent historical assessment, Doha functions as the dominant logistics hub within the Qatar 3PL market due to its concentration of industrial zones, seaport connectivity, and international airport cargo capacity. The Hamad Port and Hamad International Airport cargo terminals support high freight throughput and facilitate regional trade routes linking Asia, Europe, and Africa. Industrial zones in Ras Laffan and Mesaieed also contribute significantly because oil, gas, and petrochemical companies rely heavily on specialized logistics providers for transportation, warehousing, and project logistics.

Market Segmentation

By Service Type

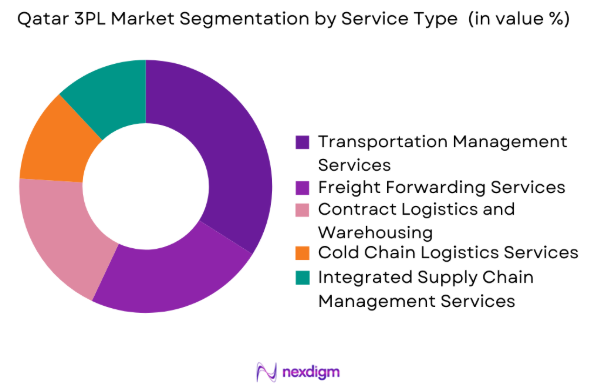

Qatar 3PL market is segmented by product type into transportation management services, freight forwarding services, contract logistics and warehousing services, cold chain logistics services, and integrated supply chain management services. Recently, transportation management services has a dominant market share due to strong demand for domestic distribution and cross-border cargo transportation across the Gulf region. Rapid infrastructure expansion including highways, ports, and cargo terminals has strengthened road-based logistics operations and improved delivery efficiency. E-commerce retailers, industrial manufacturers, and energy companies rely heavily on transportation outsourcing to ensure reliable distribution across urban and industrial regions. Logistics providers continue to expand fleet capacity, route optimization systems, and real-time cargo monitoring solutions. These developments enable logistics firms to handle large shipment volumes while maintaining delivery reliability and cost efficiency, making transportation management services the most widely adopted service category within the Qatar 3PL market.

By End User

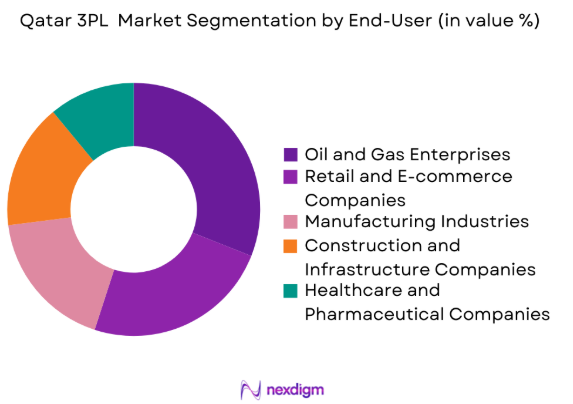

Qatar 3PL market is segmented by product type into retail and e-commerce companies, oil and gas enterprises, manufacturing industries, healthcare and pharmaceutical companies, and construction and infrastructure companies. Recently, oil and gas enterprises has a dominant market share due to the central role of energy production within the national economy. Energy companies require complex logistics operations for transporting heavy equipment, drilling materials, and specialized industrial components. Project logistics, offshore supply services, and equipment warehousing are widely outsourced to specialized third-party providers capable of handling high-value industrial cargo. Large infrastructure investments within the energy sector also generate demand for integrated supply chain coordination involving sea freight, air freight, and road transportation. As energy projects expand and supply chains become more complex, logistics providers offering specialized industrial transport capabilities continue to gain strong demand within this segment.

Competitive Landscape

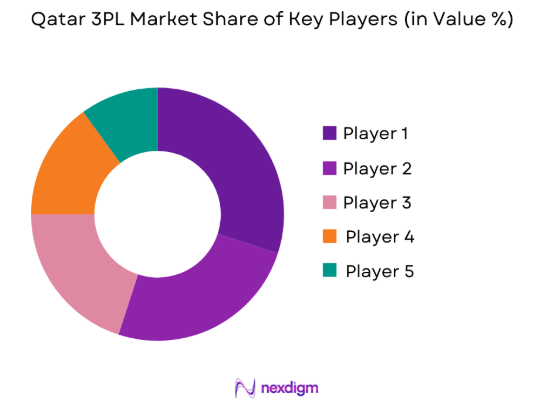

The Qatar 3PL market demonstrates a moderately consolidated competitive structure characterized by the presence of global logistics providers alongside regional supply chain companies. International firms contribute advanced logistics technologies, digital freight management platforms, and global transportation networks, while domestic companies provide strong local distribution capabilities and regulatory familiarity. Strategic partnerships, long-term logistics contracts, and infrastructure investments have strengthened competitive positioning. Major companies continue expanding warehouse capacity, fleet networks, and digital logistics solutions to improve operational efficiency and meet growing demand from energy, industrial, and e-commerce sectors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Logistics Infrastructure Capacity |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Aramex | 1982 | UAE | ~ | ~ | ~ | ~ | ~ |

| Agility Logistics | 1979 | Kuwait | ~ | ~ | ~ | ~ | ~ |

| Gulf Warehousing Company | 2004 | Qatar | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

Qatar 3PL Market Analysis

Growth Drivers

Expansion of Regional Trade and Logistics Infrastructure Development

Large scale investments in logistics infrastructure and regional trade connectivity strongly influence the Qatar 3PL market and strengthen the country’s role as a transportation hub in the Middle East. Development of modern seaports, international cargo airports, and advanced highway networks has improved cargo handling efficiency and expanded freight capacity across major logistics corridors. Facilities such as Hamad Port increase maritime cargo throughput while integrated logistics zones provide warehouse space and distribution centers supporting import and export activities. Growing trade within Gulf Cooperation Council markets increases cross border freight complexity, encouraging companies to rely on specialized logistics providers. Logistics firms continue investing in digital tracking systems, route optimization technologies, and regional distribution networks.

Rapid Expansion of E-Commerce and Retail Distribution Networks

Growth of online retail platforms and digital marketplaces has become a major factor driving demand within the Qatar 3PL market as retailers increasingly rely on logistics providers for order fulfillment and last mile delivery services. Online commerce generates high shipment volumes that require efficient distribution centers, parcel sorting facilities, and real time inventory management systems. Logistics companies are investing in automated warehouses equipped with barcode scanning and robotics assisted picking systems to improve operational productivity. Retail networks depend on transportation outsourcing to manage deliveries across cities and suburban areas efficiently. Rising consumer expectations for faster delivery encourage logistics providers to expand vehicle fleets and establish localized distribution hubs near urban population centers.

Market Challenges

High Operational Costs Associated with Logistics Infrastructure Development

The Qatar 3PL market faces operational challenges due to high capital requirements for establishing logistics infrastructure such as warehouses, transportation fleets, and cargo handling equipment. Companies must invest heavily in automated warehouses, storage facilities, and digital supply chain systems to maintain efficiency and meet client expectations. Logistics parks require specialized infrastructure including climate controlled storage and heavy cargo handling areas. Operating costs also involve fuel, vehicle maintenance, and workforce expenses for distribution operations. Firms engaged in international trade must additionally manage compliance systems, customs documentation, and cargo security requirements. Smaller providers often face financial limitations that restrict technology adoption and expansion capabilities.

Dependence on Imported Logistics Technologies and Skilled Workforce

The Qatar 3PL market faces structural challenges due to reliance on imported logistics technologies and specialized workforce expertise required for advanced supply chain operations. Many logistics providers depend on international suppliers for warehouse automation systems, cargo tracking solutions, and transportation management software, increasing operational costs and procurement delays. Advanced logistics services also require skilled professionals capable of managing digital platforms, automated warehouses, and international freight coordination. Recruiting qualified personnel remains difficult because the sector relies heavily on expatriate workers. Developing domestic logistics talent requires significant investment in training programs, while evolving regulatory compliance requirements further increase operational complexity for logistics providers.

Opportunities

Development of Integrated Logistics Zones and Free Trade Hubs

Expansion of integrated logistics zones and special economic areas creates major opportunities for companies operating in the Qatar 3PL market. Logistics parks located near key ports and airports provide advanced warehousing, cargo handling infrastructure, and strong transportation connectivity that improves freight distribution efficiency. Businesses operating within these zones benefit from streamlined customs procedures, simplified regulatory systems, and improved access to multimodal transport networks. Third party logistics providers can establish regional distribution centers that facilitate cross border trade across the Middle East and North Africa. These integrated logistics hubs also attract multinational firms seeking centralized supply chain operations, strengthening long term logistics sector growth.

Adoption of Smart Logistics Technologies and Digital Supply Chain Platforms

Technological innovation in supply chain management creates significant opportunities for logistics companies in the Qatar 3PL market. Digital platforms integrating inventory tracking, warehouse automation, and transportation management systems improve cargo movement efficiency and supply chain visibility. Smart technologies such as Internet of Things sensors, automated sorting solutions, and predictive analytics enable real time shipment monitoring, demand forecasting, and improved delivery coordination. These capabilities help logistics providers enhance operational reliability while reducing costs through automation and data driven decision making. Companies adopting advanced logistics technologies can also provide value added services including real time cargo tracking, predictive inventory control, and integrated supply chain analytics for business clients.

Future Outlook

The Qatar 3PL market is expected to experience steady expansion as trade activity, industrial diversification, and e-commerce development continue increasing demand for logistics outsourcing services. Infrastructure investments in ports, airports, and logistics parks will strengthen regional supply chain connectivity and support higher cargo throughput. Technological adoption including smart warehouses and digital freight platforms will enhance logistics efficiency. Regulatory initiatives encouraging trade facilitation and foreign investment will further support logistics sector growth.

Major Players

- DHL Supply Chain

- Aramex

- Agility Logistics

- Gulf Warehousing Company

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- DSV

- UPS Supply Chain Solutions

- FedEx Logistics

- MilahaLogistics

- Qatar Navigation QPSC

- Yusen Logistics

- Al Jaber Logistics

- NAQEL Express

Key Target Audience

- Logistics and supply chain companies

- Retail and e-commerce enterprises

- Manufacturing and industrial companies

- Oil and gas industry companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- International trade and export companies

Research Methodology

Step 1: Identification of Key Variables

Key supply chain indicators including trade volumes, infrastructure development, and logistics outsourcing trends are identified to define market dynamics. Industry data sources, trade statistics, and logistics sector reports are evaluated to determine relevant variables affecting demand for third-party logistics services.

Step 2: Market Analysis and Construction

Market modeling is conducted by analyzing logistics service adoption across industries including retail, energy, manufacturing, and healthcare. Infrastructure capacity, freight transportation volumes, and logistics outsourcing patterns are evaluated to construct the market framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists, logistics operators, and supply chain analysts are consulted to validate market assumptions and operational insights. Their perspectives help refine supply chain trends, technology adoption levels, and infrastructure expansion impacts.

Step 4: Research Synthesis and Final Output

Validated datasets, industry insights, and analytical models are integrated to produce final market assessments. Findings are organized into structured research sections highlighting segmentation, competitive positioning, and future opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Fulfillment and Parcel Logistics Infrastructure

Increasing Trade Volumes through Regional Logistics Hubs

Rising Outsourcing of Supply Chain Management by Enterprises - Market Challenges

High Logistics Infrastructure and Operational Costs

Dependence on Imported Logistics Technologies and Equipment

Limited Skilled Workforce in Advanced Logistics Operations - Market Opportunities

Development of Integrated Logistics Parks and Free Zones

Adoption of Smart Warehousing and Automation Technologies

Growth of Cold Chain Logistics for Healthcare and Food Distribution - Trends

Digitalization of Supply Chain Management Platforms

Growth of Multimodal Freight Transportation Networks

Integration of Real-Time Tracking and Data Analytics Systems - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Transportation Management Services

Freight Forwarding and Brokerage Services

Contract Logistics and Warehousing

Integrated Supply Chain Management Services

Cold Chain Logistics Services - By Platform Type (In Value%)

Road Logistics Platforms

Air Cargo Logistics Platforms

Sea Freight Logistics Platforms

Multimodal Transportation Platforms

Digital Logistics Management Platforms - By Fitment Type (In Value%)

Fully Outsourced Logistics Contracts

Hybrid Logistics Service Models

Project-Based Logistics Solutions

Dedicated Contract Logistics Services

Integrated End-to-End Logistics Solutions - By End User Segment (In Value%)

Retail and E-commerce Enterprises

Oil and Gas Industry Companies

Manufacturing and Industrial Firms

Healthcare and Pharmaceutical Organizations

Construction and Infrastructure Developers - By Procurement Channel (In Value%)

Direct Corporate Logistics Contracts

Government Tender-Based Procurement

Strategic Logistics Partnerships

Supply Chain Vendor Agreements

Third-Party Logistics Marketplaces

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio, Warehouse Capacity, Technology Integration, Geographic Coverage, Industry Focus)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

Aramex

Agility Logistics

Gulf Warehousing Company

Kuehne + Nagel

DB Schenker

CEVA Logistics

DSV

UPS Supply Chain Solutions

FedEx Logistics

Milaha Logistics

Qatar Navigation QPSC

Yusen Logistics

Al Jaber Logistics

NAQEL Express

- Increasing logistics outsourcing by oil and gas sector operators

- Rapid growth in fulfillment demand from e-commerce retailers

- Expanding logistics requirements from infrastructure construction projects

- Rising cold chain demand among healthcare and pharmaceutical distributors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now