Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Qatar AI servers and GPU hardware market reached approximately USD ~ million, driven by sovereign cloud expansion, national AI strategy investments, hyperscale data center deployments, and accelerated enterprise AI adoption. Government-backed digital infrastructure programs and state energy companies’ analytics initiatives significantly increased procurement of GPU-accelerated servers and high-performance compute clusters from global vendors and regional integrators.

Doha dominates regional demand due to concentration of hyperscale data centers, sovereign cloud facilities, research institutions, and government AI programs, while collaboration with US, European, and Asian technology suppliers supports advanced GPU hardware deployment. Strategic national digitization programs and energy sector AI initiatives position Qatar as a leading Gulf hub for accelerated computing infrastructure and AI-ready data center capacity.

Market Segmentation

By Product Type

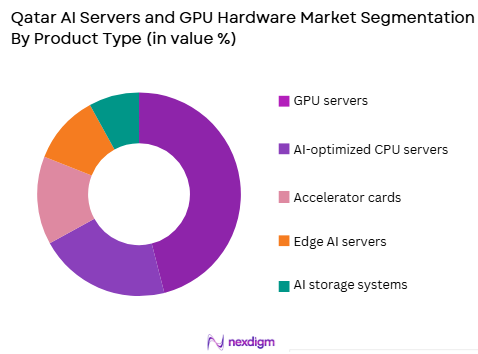

Qatar AI Servers and GPU Hardware market is segmented by product type into GPU servers, AI-optimized CPU servers, accelerator cards, edge AI servers, and AI storage systems. Recently, GPU servers have a dominant market share due to factors such as intensive AI training workloads, hyperscale cloud infrastructure requirements, and national research computing initiatives. Qatar’s sovereign cloud expansion and energy sector AI programs prioritize high-density GPU clusters capable of parallel processing for large-scale models and analytics. Government digital transformation programs and smart city platforms require accelerated compute infrastructure, further strengthening GPU server procurement. Limited domestic semiconductor fabrication leads to dependence on imported high-performance GPU systems from global vendors, consolidating demand around integrated GPU server platforms rather than standalone components. AI research institutions and university supercomputing initiatives also deploy GPU clusters for deep learning and simulation, reinforcing their dominance in the hardware mix.

By End User

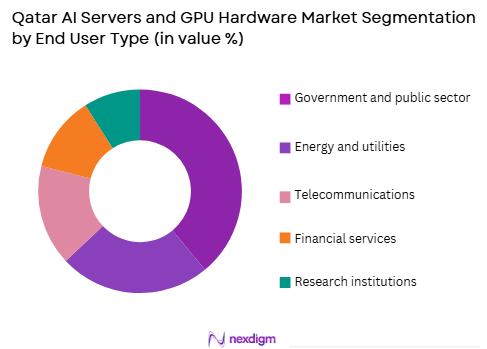

Qatar AI Servers and GPU Hardware market is segmented by end user into government and public sector, energy and utilities, telecommunications, financial services, and research institutions. Recently, government and public sector has a dominant market share due to factors such as national AI strategy funding, sovereign cloud infrastructure programs, and smart governance platforms. Public sector digitization initiatives require AI-enabled analytics, surveillance processing, and citizen services automation, driving centralized GPU data center deployments. State-owned energy companies and national research labs operate under government programs, further concentrating procurement within public sector frameworks. National security, urban planning, and digital health initiatives also rely on accelerated computing, strengthening public sector dominance. Public procurement frameworks and long-term infrastructure budgets enable large-scale GPU cluster acquisitions, reinforcing their leading share across the AI hardware ecosystem.

Competitive Landscape

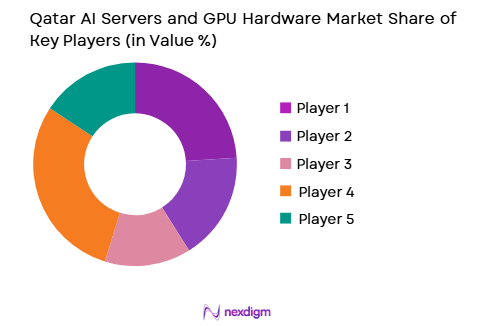

The Qatar AI servers and GPU hardware market is moderately consolidated, dominated by global GPU and accelerated computing vendors partnered with regional system integrators and cloud providers. Hyperscale-class GPU suppliers exert strong influence through proprietary architectures and software ecosystems, while telecom and sovereign cloud operators shape procurement standards. Local presence is driven primarily through channel partners and data center collaborations rather than domestic manufacturing.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Qatar Presence |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| HPE | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

Qatar AI Servers and GPU Hardware Market Analysis

Growth Drivers

National AI Strategy–Driven Sovereign Compute Infrastructure Expansion

Qatar’s national artificial intelligence and digital economy programs are driving sustained investment in sovereign compute infrastructure designed to support government analytics, smart city platforms, and secure data processing environments. Public sector modernization mandates require domestic data residency, prompting construction of GPU-accelerated data centers and sovereign cloud platforms equipped with high-performance AI servers. State energy companies deploy large-scale simulation and predictive maintenance models requiring dense GPU clusters and accelerated HPC systems. Government procurement frameworks enable multi-year hardware acquisition cycles, ensuring consistent demand visibility for AI server vendors. Collaboration with global hyperscale technology providers accelerates deployment of advanced GPU architectures within national infrastructure projects. AI-enabled surveillance, transportation optimization, and digital healthcare systems generate continuous compute workload growth across ministries and agencies. Research institutions funded under national innovation programs procure supercomputing clusters to support machine learning and scientific modeling. Regional digital leadership ambitions motivate Qatar to maintain competitive AI infrastructure capacity relative to neighboring Gulf economies. These sovereign investments collectively anchor long-term growth in the domestic AI server and GPU hardware market.

Energy Sector AI and Advanced Analytics Workload Acceleration

Qatar’s hydrocarbon and energy sector is increasingly integrating artificial intelligence into exploration, production optimization, predictive maintenance, and emissions monitoring operations, significantly expanding demand for GPU-accelerated computing infrastructure. Reservoir modeling, seismic interpretation, and process simulation require high-performance parallel computing architectures capable of handling massive datasets and complex algorithms. National energy companies deploy centralized AI data platforms within domestic data centers to ensure operational security and data sovereignty compliance. Digital oilfield initiatives integrate sensor networks and AI analytics engines that rely on accelerated servers for real-time decision support. LNG supply chain optimization and energy trading analytics also depend on GPU-driven machine learning models to improve forecasting and logistics efficiency. Partnerships between energy operators and global technology firms drive adoption of advanced AI hardware platforms tailored to industrial workloads. Carbon management and environmental monitoring programs introduce new AI processing requirements across production facilities. Continuous capital expenditure cycles in the energy sector provide stable funding for high-performance compute infrastructure upgrades. This sector-specific digital transformation trajectory acts as a major structural driver for Qatar’s AI server and GPU hardware demand.

Market Challenges

Dependence on Imported High-End GPU Supply Chains and Export Controls

Qatar’s AI server and GPU hardware ecosystem relies almost entirely on imported semiconductor technologies, exposing the market to geopolitical export controls, supply chain disruptions, and vendor allocation constraints affecting high-performance accelerators. Advanced GPUs are produced by a limited number of global manufacturers operating under export licensing regimes that can restrict availability in certain regions. Procurement cycles for sovereign and energy sector AI infrastructure may face delays due to allocation prioritization by vendors toward larger hyperscale markets. Long shipping lead times and logistics costs increase total acquisition expenses for accelerated servers and HPC clusters. Absence of domestic semiconductor fabrication or advanced assembly capability prevents localization of GPU hardware production. Dependence on foreign technology standards also creates interoperability challenges with national digital infrastructure initiatives. Currency fluctuations and import tariffs can influence procurement budgets for large-scale compute deployments. Vendor concentration around proprietary GPU architectures limits bargaining power for buyers and integrators. These structural supply chain dependencies represent a persistent constraint on the growth trajectory of Qatar’s AI hardware market.

High Capital Intensity and Utilization Optimization of AI Infrastructure

Deployment of GPU-accelerated servers and HPC clusters involves substantial upfront capital expenditure and ongoing operational costs, posing financial and utilization challenges for organizations adopting AI infrastructure at scale in Qatar. AI servers require specialized cooling, power density, and data center engineering investments that increase total cost of ownership beyond standard enterprise IT infrastructure. Organizations must maintain high utilization rates of GPU clusters to justify investment, yet AI workload maturity varies across sectors and applications. Skills shortages in AI engineering and HPC operations can limit effective deployment of accelerated computing resources. Rapid technological evolution in GPU architectures risks hardware obsolescence within short upgrade cycles. Energy consumption of dense GPU systems contributes to operational expenditure and sustainability considerations. Smaller enterprises and institutions may lack sufficient AI workloads to support dedicated GPU infrastructure. Procurement of high-end accelerators often requires long-term capacity planning and forecasting accuracy. These economic and operational factors create adoption barriers despite strong strategic demand drivers in the Qatar market.

Opportunities

Regional AI Cloud and Accelerated Computing Hub Development

Qatar has the opportunity to position itself as a regional hub for AI cloud and accelerated computing services by leveraging sovereign infrastructure investments and strategic geographic connectivity within the Gulf and Middle East region. Expansion of domestic GPU-accelerated data centers can enable provision of AI training and inference services to regional enterprises lacking local HPC capacity. Cross-border digital infrastructure partnerships and submarine cable connectivity support low-latency AI cloud service delivery. Government-backed sovereign cloud platforms can attract international AI developers seeking compliant data residency environments. Regional research collaborations and academic partnerships can utilize Qatar-based supercomputing facilities for large-scale scientific computing. Industrial AI service offerings for energy, logistics, and smart city applications can be exported to neighboring economies. Strategic incentives and digital economy policies can attract global AI technology firms to deploy regional compute nodes in Qatar. Accelerated computing capacity can also support emerging sectors such as autonomous mobility and digital healthcare. This regional positioning opportunity can expand the domestic AI server and GPU hardware market beyond internal demand drivers.

AI-Driven Smart Infrastructure and Digital Public Services Expansion

Qatar’s ongoing smart nation and digital public service programs create expanding opportunities for AI-accelerated infrastructure deployment across transportation, urban management, healthcare, and public safety systems. Intelligent traffic management and autonomous mobility platforms require GPU-powered real-time analytics and computer vision processing at centralized and edge data centers. Digital healthcare initiatives involving imaging analysis and predictive diagnostics depend on accelerated computing clusters for clinical AI applications. Smart utilities and environmental monitoring systems generate continuous data streams processed by AI servers for optimization and sustainability management. Public safety surveillance and emergency response platforms utilize GPU-enabled video analytics and pattern recognition technologies. Integration of IoT networks with AI processing engines increases compute demand across urban infrastructure layers. Government modernization strategies emphasize automation and data-driven decision making, reinforcing need for high-performance AI hardware. Expansion of e-government platforms and citizen service analytics further scales compute workloads. These smart infrastructure programs collectively create long-term growth opportunities for AI servers and GPU hardware deployment in Qatar.

Future Outlook

Over the next five years, the Qatar AI servers and GPU hardware market is expected to expand steadily as sovereign cloud infrastructure, energy sector AI adoption, and smart nation programs continue scaling accelerated compute demand. Advances in GPU architectures, AI-optimized data center design, and edge AI systems will broaden deployment across sectors. Government digital economy strategies and regional AI hub ambitions will reinforce sustained investment in domestic high-performance computing capacity and AI-ready infrastructure ecosystems.

Major Players

- NVIDIA

- AMD

- Intel

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Supermicro

- Cisco

- Huawei

- Inspur

- IBM

- Fujitsu

- Oracle

- MEEZA

- Ooredoo

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Telecommunications operators

- Energy and utilities companies

- Data center developers and operators

- Enterprise IT and digital transformation buyers

- Defense and national security agencies

Research Methodology

Step 1: Identification of Key Variables

Key variables such as GPU server deployments, AI data center capacity, sovereign cloud investments, sectoral AI adoption, and hardware procurement cycles were identified through secondary research and industry databases. Supply chain structure and vendor ecosystem mapping were established to define market boundaries.

Step 2: Market Analysis and Construction

Market size was constructed by aggregating AI server and GPU hardware procurement across government, energy, telecom, and enterprise sectors in Qatar. Vendor shipment data, data center capacity metrics, and infrastructure investment flows were triangulated to estimate market value.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with regional data center operators, AI infrastructure vendors, and technology integrators active in Gulf markets. Expert insights refined demand assumptions, deployment timelines, and sectoral adoption intensity.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured market forecasts, segmentation, and competitive analysis. Consistency checks and cross-verification ensured reliability before final report preparation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National AI and digital transformation investments driving sovereign compute infrastructure demand

Rapid expansion of hyperscale and colocation data centers in Qatar increasing GPU server deployments

Growing enterprise adoption of generative AI analytics and automation workloads requiring accelerated computing - Market Challenges

High capital intensity and cooling power requirements for large scale GPU clusters in desert climate conditions

Supply constraints and long lead times for advanced GPUs and AI accelerators affecting deployment schedules

Skills gap in AI infrastructure design integration and optimization across enterprise environments - Market Opportunities

Localization of AI compute through sovereign cloud initiatives and national data residency mandates

Deployment of liquid cooled high density AI racks aligned with energy efficiency and sustainability targets

Expansion of edge AI inference infrastructure across smart city and 5G telecom networks - Trends

Shift toward liquid cooling and high density GPU racks in Middle East data centers

Adoption of AI supercomputing clusters for national research and language model development

Integration of AI servers into telecom edge and smart infrastructure platforms - Government regulations

National AI strategy and sovereign data infrastructure policies promoting domestic AI compute

Data protection and residency regulations requiring local AI processing infrastructure

Energy efficiency and green data center standards influencing AI hardware deployments - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPU Accelerated AI Servers

AI Training Supercomputing Clusters

AI Inference Edge Servers

Hybrid CPU GPU Enterprise Servers

High Density Liquid Cooled AI Racks - By Platform Type (In Value%)

Cloud Data Center AI Infrastructure

On Premise Enterprise AI Infrastructure

Government Sovereign AI Platforms

Telecom Edge AI Platforms

Research and Academic HPC Platforms - By Fitment Type (In Value%)

Rack Scale Integrated Systems

Blade AI Server Systems

Tower AI Workstations

Modular GPU Expansion Systems

Preconfigured AI Appliances - By End User Segment (In Value%)

Hyperscale and Cloud Providers

Government and Smart City Programs

Telecommunications Operators

Energy and Industrial Enterprises

Universities and Research Institutes - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator Contracts

Government Tenders

Cloud Partnership Programs

Value Added Distributors

- Market Share Analysis

- Cross Comparison Parameters (GPU Compute Performance (FLOPS), Accelerator Memory Capacity (HBM/VRAM), Interconnect Bandwidth (NV Link/InfiniBand/Ethernet), System Power Density (kW per rack), Cooling Architecture (Air vs Liquid)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Advanced Micro Devices

Intel

Super Micro Computer

Dell Technologies

Hewlett Packard Enterprise

Lenovo

ASUSTeK Computer

Gigabyte Technology

Inspur

Huawei

Quanta Computer

MiTAC Computing Technology

Graphcore

Cisco Systems

- Government entities prioritize sovereign AI compute capacity for national digital strategy execution

- Cloud and hyperscale providers deploy large GPU clusters to serve regional AI workloads

- Telecom operators integrate edge AI servers to support 5G and smart infrastructure services

- Enterprises adopt AI servers for automation analytics and sector specific AI applications

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now