Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Qatar aircraft flight control systems market is estimated to reach USD ~ billion by 2025, driven by the expanding aviation and aerospace sectors within the region. The market’s growth is largely attributed to the continuous modernization of aircraft fleets, along with increasing government investments in aviation infrastructure. Additionally, Qatar’s commitment to enhancing its aviation and defense capabilities has been pivotal in driving demand for advanced flight control systems. This growth is further fueled by the adoption of next-generation flight control technologies like fly-by-wire systems, which improve operational efficiency and safety standards across both commercial and military aircraft sectors.

Qatar dominates the regional aircraft flight control systems market due to its strong aviation infrastructure, bolstered by a growing airline industry and strategic military developments. Doha, the capital, plays a central role as a hub for both commercial and defense aviation activities, making it a focal point for global aerospace manufacturers. The country’s investment in national airlines like Qatar Airways and its focus on becoming an aerospace leader within the Gulf Cooperation Council (GCC) region further solidifies its market dominance. Additionally, the presence of state-backed aviation initiatives and defense contracts fuels the demand for advanced flight control systems.

Market Segmentation

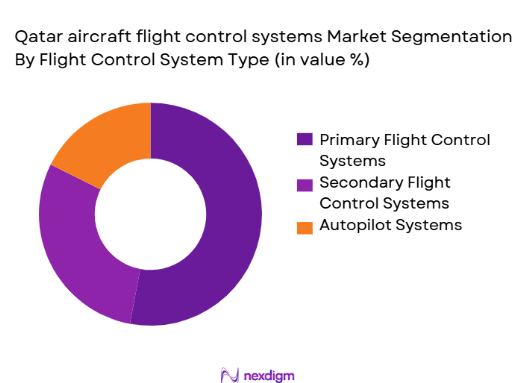

By Flight Control System Type

The aircraft flight control systems market is segmented by flight control system type into primary, secondary, and autopilot systems. Among these, primary flight control systems dominate the market. This segment includes the actuation and control of the critical flight surfaces such as ailerons, rudders, and elevators, which are vital for aircraft stability and safety. Primary flight control systems are crucial in modern aviation, as they directly influence the performance and safety of the aircraft. The demand for these systems is particularly high in both commercial and military aircraft, where safety and reliability are paramount. Primary systems also benefit from the increasing trend toward automation and precision in aircraft operation.

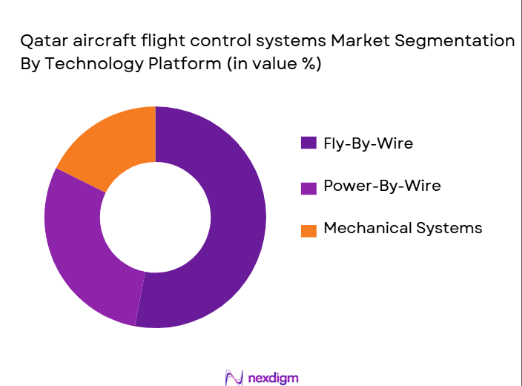

By Technology Platform

The technology platform segment includes fly-by-wire, power-by-wire, and mechanical/hydromechanical systems. The fly-by-wire (FBW) technology platform currently holds the largest share in the market. FBW systems have seen significant adoption in modern commercial aircraft because they offer superior safety, reliability, and weight reduction compared to traditional mechanical systems. These systems replace conventional mechanical linkages with electronic controls, improving efficiency, reducing weight, and enabling more precise flight control. Moreover, FBW technology aligns with the industry’s push towards more sustainable, fuel-efficient, and automated aviation solutions, further driving its dominance.

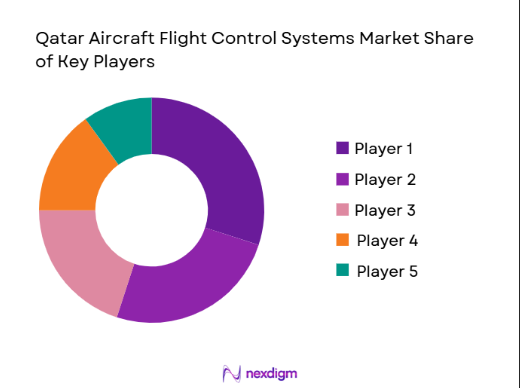

Competitive Landscape

The Qatar aircraft flight control systems market is dominated by several global players, including aerospace giants like Honeywell, Moog, and BAE Systems, as well as specialized firms like Safran Electronics & Defense. The competitive landscape is shaped by these major players’ investments in cutting-edge flight control technologies, such as fly-by-wire systems and advanced autopilot systems. These companies hold a significant share of the market by leveraging their technological expertise, long-term relationships with aircraft manufacturers, and robust support infrastructure. Their dominance is further reinforced by their ability to innovate continuously in avionics systems and offer scalable solutions for both commercial and military applications.

| Company | Establishment Year | Headquarters | Revenue (2023) | Product Portfolio | Key Market | Technology Focus |

| Honeywell Aerospace | 1906 | USA | ~ | ~ | ~ | ~ |

| Moog Inc. | 1951 | USA | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | UK | ~ | ~ | ~ | ~ |

| Safran Electronics & Defense | 2005 | France | ~ | ~ | ~ | ~ |

| Parker Hannifin | 1917 | USA | ~ | ~ | ~ | ~ |

Qatar Aircraft Flight Control Systems Market Analysis

Growth Drivers

Increased Commercial Aircraft Deliveries & Fleet Expansion

Qatar’s aviation ecosystem continues to drive demand for aircraft flight control systems due to sustained expansion in commercial airline operations, supported by fleet growth and increased global traffic. According to the latest Qatar Airways Annual Report, the airline’s fleet grew to ~ aircraft from 265 in the prior year, with~passenger aircraft and ~ cargo aircraft in service as part of its expansion strategy. This sizable fleet expansion underpins the demand for advanced flight control system upgrades, maintenance, and newinstall capabilities critical to flight safety, automation, and airworthiness compliance. Additionally, Qatar’s Hamad International Airport served a record ~ million passengers in 2025, marking strong operational throughput and aircraft movements, which directly correlates to elevated demand for avionics and flight control systems support in both commercial and cargo operations. Robust passenger traffic reflects flight frequency increases that necessarily raise utilization and, therefore, replacement and upgrade cycles for core aircraft systems like flight controls. These operational and fleet growth statistics illustrate how ongoing commercial fleet expansion translates into sustained demand for flight control system integration, especially as carriers modernize fleets with nextgeneration avionics and control technologies to manage increased traffic volumes and aircraft utilization.

Global Aviation Activity & Passenger Traffic Growth

The broader global aviation rebound significantly reinforces Qatar’s flight control systems demand. The International Air Transport Association (IATA) reported that global air passenger traffic in 2025 reached nearly ~ billion, a ~% rise over the previous year, demonstrating that international air mobility continues expanding despite industry volatility. This global traffic surge, combined with Middle Eastern carriers posting a ~% traffic rise in 2025 over 2024, signals elevated aircraft utilization and operational requirements for avionics systems, including flight control units. In the context of Qatar, Hamad International Airport’s achievement of record passenger volumes reflects the nation’s strategic hub status that drives aircraft operational cycles, necessitating more frequent maintenance, checks, and flight control system overhauls or retrofits required to support safe, highfrequency operations. As both airline load and fleet utilization expand, there is a correlative increase in the need for advanced, reliable flight control systems capable of supporting enhanced automation, redundancy, and safety requirements. This macro trend of rising global passenger and aircraft movements supports the flight control systems market through heightened aircraft activity demands and modernization efforts across fleet operators serving the Doha hub.

Market Challenges

Certification Barriers & Compliance Costs

Aircraft flight control systems are among the most regulated components in aerospace, requiring stringent certification from multiple aviation authorities due to their direct impact on flight safety. In Qatar, compliance with Qatar Civil Aviation Authority standards, aligned with International Civil Aviation Organization protocols, necessitates extensive testing and validation regimes for any modification or new installation of flight control hardware and software. Certification processes for flight control computers and associated systems involve rigorous environmental, software, and redundancy testing long before they are installed on aircraft, often leading to extended qualification timelines and high compliance costs. These regulatory demands significantly impact procurement cycles and increase barriers to market entry for smaller suppliers who lack the resources to secure full airworthiness approvals. Field certifications for avionics, especially for nextgeneration flybywire systems, require multijurisdictional validation because aircraft typically operate across international boundaries, which can result in duplication of compliance procedures. These regulatory overheads impact manufacturers’ operating costs and slow the introduction of updated or improved flight control solutions, acting as a key restraint despite strong demand from airlines and defense operators in the region.

High R&D & Qualification Costs for New Technologies

Developing and qualifying new flight control technologies—such as advanced flybywire processors, digital control algorithms, and highreliability actuators—involves substantial research and development investment. These costs are amplified by the need for rigorous testing against safety standards, redundancy requirements, and integration with existing aircraft architectures. Unlike simpler avionics subsystems, flight control systems must meet extremely high reliability thresholds due to their safetycritical nature, meaning prototype development, simulation, hardwareintheloop testing, and qualification flights are required before commercial or military deployment. This financial burden often restricts innovation to larger aerospace integrators with extensive engineering resources, potentially slowing the pace of adoption of cuttingedge flight control systems in emerging markets. In Qatar, where aerospace modernization is tied to commercial airline competitiveness and defense capabilities, the cost of innovation and qualification poses a structural challenge that can moderate the pace at which new technologies are fielded, especially for localized MRO partners seeking to diversify beyond traditional maintenance services.

Market Opportunities

Localization of MRO & Avionics Testing in Qatar

The rapid growth of Hamad International Airport as a global hub, handling over ~ million passengers in 2025, reflects rising aviation throughput and aircraft operations. This expansion creates a compelling opportunity for establishing localized Maintenance, Repair, and Overhaul facilities with specialized avionics and flight control system capabilities in Qatar. Currently, many regional carriers and aircraft operators depend on overseas service providers for advanced flight control diagnostics and repairs, which extends turnaround times and elevates logistical costs. Investing in onsite avionics testing and certification infrastructure would allow Qatar to capture a greater share of lifecycle service value for flight control components, supporting quicker turnaround and enhancing fleet readiness. Localization efforts could also attract regional demand from Gulf carriers, given Doha’s strategic geographic position between Europe, Asia, and Africa. By cultivating specialized technical talent and equipping facilities with advanced simulation and testing tools, Qatar could reduce dependency on foreign MRO hubs, increasing operational efficiency for airlines and defense fleets alike. As air traffic continues to grow, this presents a clear opportunity to elevate the country’s aerospace ecosystem while lowering lifecycle costs associated with flight control system support.

NextGen Fly By Wire Systems for Sustainable Aviation

Airlines globally are transitioning to more automated and fuel efficient aircraft, and Qatar is no exception. Fly by wire (FBW) systems, which replace mechanical flight control linkages with electronic interfaces, play a crucial role in weight reduction and fuel efficiency. With global passenger demand rising and aircraft utilization increasing, the implementation of FBW upgrades and newbuild installations offers opportunities for flight control suppliers. Modern aircraft such as Airbus A350 and Boeing 787 models widely used by Qatar Airways employ advanced FBW systems that support optimized flight profiles and lower fuel burn. As carriers pursue sustainability goals aligned with international emission reduction targets, there is an incentive to adopt next generation flight control technologies that enable more precise aircraft control, enhanced autopilot integration, and reduced pilot workload. These technology trends represent market opportunities for suppliers that can develop compliant, reliable, and future ready flight control platforms, given the increasing emphasis on operational efficiency and environmental performance in airline fleets.

Future Outlook

Over the next five years, the Qatar aircraft flight control systems market is expected to show significant growth driven by continuous technological advancements, government investment in defense and aviation infrastructure, and the adoption of automation systems. The increasing demand for fuel-efficient, lightweight, and automated systems, coupled with Qatar’s ambitions to solidify its position as a global aviation hub, will contribute to the expanding market opportunities. Furthermore, the growth of Qatar Airways and increased defense procurement will create new avenues for innovation and partnerships in the flight control systems sector.

Major Players

- Honeywell Aerospace

- Moog Inc.

- BAE Systems

- Safran Electronics & Defense

- Parker Hannifin

- Raytheon Technologies

- Thales Group

- Lockheed Martin

- Northrop Grumman

- Collins Aerospace

- General Electric Aviation

- Mitsubishi Heavy Industries

- Leonardo S.p.A

- United Technologies Corporation

- Rolls-Royce

Key Target Audience

- Aircraft Manufacturers

- Military and Defense Procurement Agencies

- Aviation MRO Providers

- Airlines Operating in Qatar

- Aerospace Component Suppliers

- Aircraft Leasing Companies

- Government and Regulatory Bodies

- Investment and Venture Capital Firms

Research Methodology

Step 1: Identification of Key Variables

This phase involves mapping the ecosystem and identifying all major stakeholders within Qatar’s aircraft flight control systems market. We combine secondary research with proprietary data sources, focusing on understanding the drivers, restraints, and competitive dynamics influencing the market. The primary goal is to identify key variables such as system type, technology platforms, and end-users that significantly impact the market’s future direction.

Step 2: Market Analysis and Construction

During this phase, we analyze historical data concerning Qatar’s aircraft flight control systems market, including key adoption rates, the ratio of service providers to system manufacturers, and overall market revenue. The analysis will also evaluate how various components contribute to the total market value. We will assess service quality statistics and cross-reference them with global standards to ensure accurate revenue projections.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, we validate market hypotheses using expert consultations. We conduct interviews with aviation professionals, engineers, and industry practitioners to understand real-time developments, challenges, and opportunities. These insights are essential for refining the data and ensuring that our market projections align with industry realities.

Step 4: Research Synthesis and Final Output

The final step involves validating our findings with key aircraft manufacturers and system providers to corroborate the results from the data and expert consultations. This phase ensures that all insights are verified, offering a comprehensive, accurate, and reliable analysis of the Qatar aircraft flight control systems market.

- Executive Summary

- Research Methodology (Definitions Specific to Flight Control Systems & Certification Standards Market Assumptions, Data Sources: Primary Interviews, Secondary Databases Sizing & Forecasting Methodology, Limitations & Adjustments for Forecast Variability)

- Definition & Scope of Qatar Flight Control Systems Market

- Market Genesis & Evolution in Qatar’s Aerospace Sector

- Flight Control System Ecosystem in Qatar

- Key Regulatory & Certification Bodies

- Supply Chain & Value Chain Analysis

- Growth Drivers

Increased Commercial Aircraft Deliveries & Fleet Expansion

Defense Modernization & ISR Platform Acquisition

Shift to Digital FBW & Predictive Systems

Focus on Safety, Fuel Efficiency, and Automation - Market Restraints

Certification Barriers & Compliance Costs

High R&D & Qualification Costs for New Technologies - Market Opportunities

Localization of MRO & Avionics Testing in Qatar

NextGen FBW Systems for Sustainable Aviation

Advanced Control Algorithms & AIAssisted Systems - Market Trends

Digital Twins & Simulation for Flight Control Qualification

Modular & Scalable Control Architectures

Adoption of Smart Actuators & Predictive Health Monitoring - Regulatory & Certification Landscape

QCAA, EASA, FAA Standards & Test Protocols

Safety & Redundancy Requirements for FCS

- SWOT Analysis

- Porter’s Five Forces

- Industry Value Chain & Stakeholder Mapping

- By Market Value, 2019-2025

- By System Type, 2019-2025

- By Flight Control Hardware Volume, 2019-2025

- By Pricing Trends by Product & Technology, 2019-2025

- By Installed Base & Replacement Cycles, 2019-2025

- By Flight Control System Type (In Value %)

Primary Flight Control Systems

Secondary Flight Controls

Autopilot/AutoFlight Control Modules

Redundant/Backup Control Systems - By Technology Platform (In Value %)

FlybyWire Systems

PowerbyWire

Mechanical & Hydromechanical Systems

Integrated Avionics & Flight Control Computing Platforms - By Aircraft Platform (In Value %)

Commercial Linefit

Business & VIP Jets

Military Fixed Wing

Rotorcraft & Helicopters

UAS/UAV Flight Control Systems - By EndUser (In Value %)

OEM

Aftermarket

Defense & Government Procurement

Lease Operators & Airlines - By Component (In Value %)

Flight Control Computers

Sensors & Actuators

Software & Firmware Modules

Redundancy & Safety Management Units

- Market Share Analysis

- Cross Comparison Parameters (Marketspecific: Flight Control Architecture Complexity, Redundancy Level, Certification Duration, SWAP (Size/Weight/Power), Mean Time Between Failures, System Safety Integrity Level, InService Support Capability, Price Per Unit)

- SWOT Profiles of Key Competitors

- Competitive Strategy Mapping

- Price & Technology Positioning Analysis

- Detailed Company Profiles

Safran Electronics & Defense

Collins Aerospace (RTX)

Honeywell Aerospace

Moog Inc.

BAE Systems PLC

Raytheon Technologies Corp.

Nabtesco Corporation

Thales Group

Lockheed Martin

Northrop Grumman

General Atomics

CurtissWright Corporation

Saab AB

Parker Hannifin Corporation

Liebherr Aerospace

- Demand by Airlines

- Decision Drivers

- Procurement Cycle & Budget Allocations

- Operator Technical Preferences

- Forecast Market Size (Revenue & Units) by Segmentation, 2026-2035

- Future Pricing Trends & Technology Adoption, 2026-2035

- Growth Rates & Regional Demand Projections, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now