Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Qatar Aviation Market is valued at USD ~ billion. This growth is driven by the rapid expansion of the aviation sector in the region, supported by the increasing demand for air travel, robust infrastructure developments, and strong government investments. Qatar’s strategic location as a key hub in the Middle East also contributes to the growing aviation market, attracting investments from global stakeholders and airlines aiming to expand their presence in the region.

The dominant players in the Qatar Aviation Market include cities and countries such as Qatar, the UAE, and Saudi Arabia. Qatar stands as a key player in the global aviation market due to its advanced infrastructure, such as Hamad International Airport, and its flagship carrier, Qatar Airways. The country’s investments in state-of-the-art airports and growing air traffic have solidified its position as a leading aviation hub in the Middle East, serving as a critical gateway for international travel and cargo transit.

Market Segmentation

By Product Type

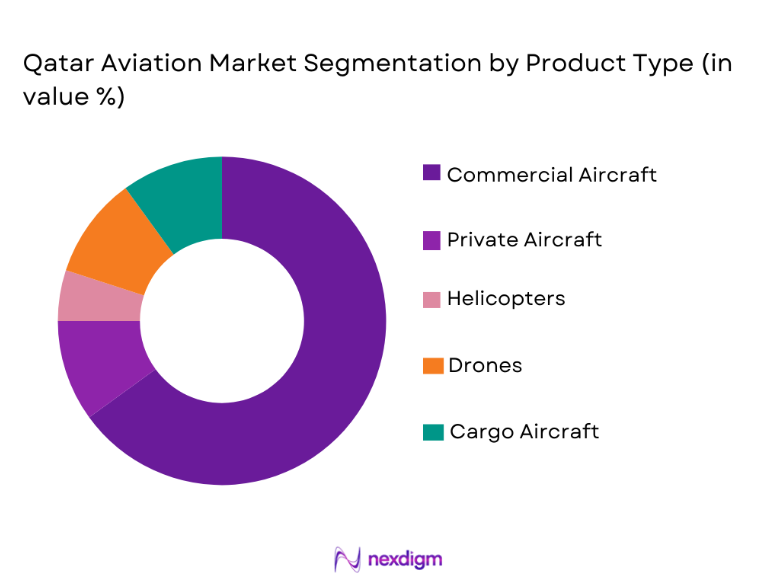

The Qatar Aviation Market is segmented by product type into commercial aircraft, private aircraft, helicopters, drones, and cargo aircraft. Recently, commercial aircraft has maintained a dominant market share due to the growing demand for air travel both domestically and internationally. The increasing tourism, business travel, and the region’s position as a global travel hub have created strong demand for commercial airliners, with Qatar Airways playing a central role in this expansion. Moreover, the development of Qatar’s aviation infrastructure, such as the expansion of Hamad International Airport, has bolstered the growth of commercial aircraft purchases, further solidifying its dominant position.

By Platform Type

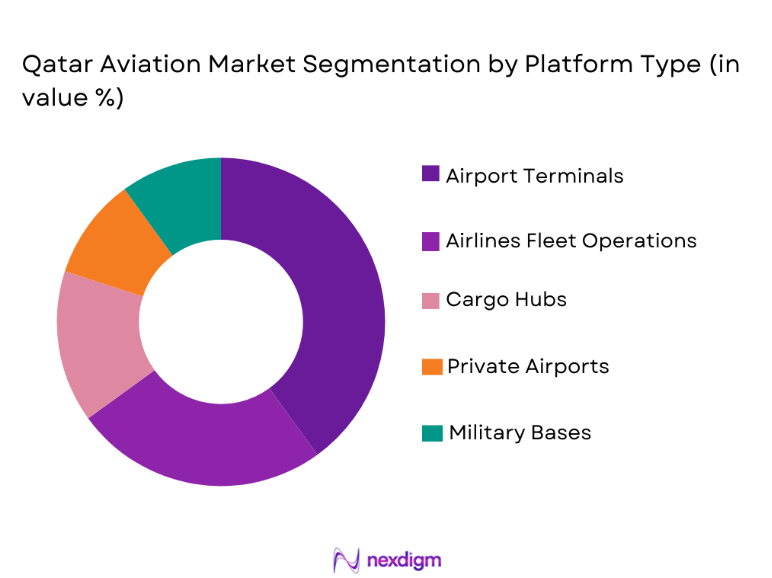

The Qatar Aviation Market is segmented by platform type into airport terminals, airlines fleet operations, cargo hubs, private airports, and military bases. Recently, airport terminals have seen a dominant market share as the development and expansion of Hamad International Airport has been a key enabler of air travel growth. The modernization and expansion of airport facilities have increased the capacity for passenger and cargo handling, reinforcing Qatar’s status as a global aviation hub. Additionally, Qatar’s strategic investment in airport infrastructure has attracted international airlines and cargo operators, making airport terminals the most significant platform for aviation in the region.

Competitive Landscape

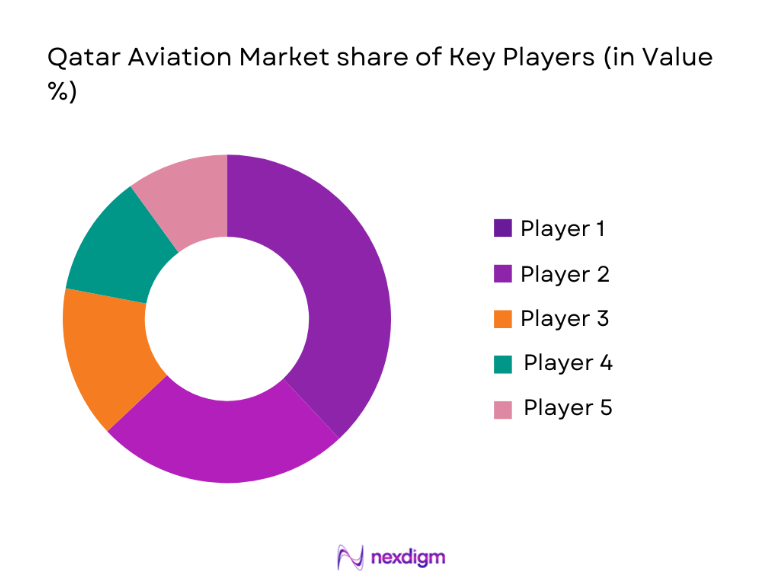

The Qatar Aviation Market is characterized by a competitive landscape marked by consolidation among key players in both commercial and cargo aviation sectors. Major players such as Qatar Airways, which enjoys a dominant market position, work alongside government entities and private stakeholders to further develop Qatar’s aviation infrastructure. The market is heavily influenced by the innovation and technological capabilities of global aviation players, creating opportunities for new entrants and local players alike.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Qatar Airways | 1993 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

| Gulf Air | 1950 | Manama, Bahrain | ~ | ~ | ~ | ~ | ~ |

| Doha International Airport | 2014 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

| Al Jaber Aviation | 1990 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

| Oryx Aerospace | 2010 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

Qatar Aviation Market Analysis

Growth Drivers

Increasing tourism and business travel

Increasing tourism and business travel has significantly contributed to the expansion of the Qatar Aviation Market. The country’s strategic location between Asia, Europe, and Africa makes it an ideal hub for international flights. Moreover, Qatar’s modern infrastructure and high-quality services attract both leisure and business travelers. As the number of international travelers increases, the demand for commercial aircraft grows, benefiting local airlines like Qatar Airways. Additionally, the government’s focus on tourism development and the country’s efforts to host international events, such as the FIFA World Cup, have led to higher air traffic volumes. This has subsequently resulted in more investments in infrastructure, ensuring the continued growth of the aviation sector. Furthermore, the rise of business travel from neighboring countries and emerging markets has added to the demand for flights, driving the need for expanding fleets, newer aircraft, and enhanced airport facilities to meet passenger demands.

Government investments in aviation infrastructure

Government investments in aviation infrastructure are another key growth driver for the Qatar Aviation Market. Qatar’s ongoing efforts to modernize its airports, including the expansion of Hamad International Airport, have laid the foundation for the continued growth of the aviation sector. The government’s commitment to boosting the region’s aviation capabilities has led to the establishment of world-class facilities that enhance passenger experience and operational efficiency. This infrastructure development also contributes to Qatar’s goal of becoming a global aviation hub by offering more capacity for airlines to expand their routes and services. In addition to airport expansions, investments in air traffic control systems, cargo handling facilities, and maintenance services are essential to meeting the demands of the growing aviation market. The national airline, Qatar Airways, plays a central role in these developments by acquiring newer aircraft to cater to increased passenger and cargo traffic, thus reinforcing Qatar’s position as an aviation leader in the Middle East.

Market Challenges

High operational costs

High operational costs in the Qatar Aviation Market present a significant challenge to market growth. Rising fuel prices, the cost of maintaining modern fleets, and the need for advanced infrastructure continue to pressure aviation companies. For instance, the operational costs for Qatar Airways are heavily influenced by fluctuating fuel prices, which can impact profitability. Moreover, the high costs associated with airport expansions and maintaining state-of-the-art facilities add to the financial burden of operating in the region. These increased costs can affect pricing strategies and limit the ability of airlines to offer competitive rates, particularly in the face of growing competition from low-cost carriers. Additionally, the constant need for investment in technology and infrastructure makes it difficult for smaller players to sustain operations in such a capital-intensive environment. As the market grows, managing operational costs efficiently will be crucial for companies to remain competitive while maintaining profitability.

Regulatory compliance complexity

Regulatory compliance complexity in the Qatar Aviation Market poses another challenge to growth. Qatar’s aviation industry is governed by strict regulations set by national authorities and international bodies such as the International Civil Aviation Organization (ICAO). While these regulations are necessary for ensuring safety and security, they can also increase the operational complexity and cost for airlines and aviation service providers. Regulatory requirements for flight safety, air traffic management, environmental standards, and passenger services require continuous updates to comply with changing global norms. This constant evolution of aviation regulations demands significant investment in compliance processes, technology upgrades, and employee training. Furthermore, the complex regulatory landscape may also delay new entrants into the market, as it can take considerable time to meet the stringent approval processes. For established players, navigating this complex regulatory environment while scaling operations and maintaining service quality becomes increasingly challenging.

Opportunities

Development of green aviation technologies

The development of green aviation technologies presents a significant opportunity for growth in the Qatar Aviation Market. As global concerns about climate change increase, there is growing demand for sustainable aviation solutions, such as electric aircraft and alternative fuel-powered planes. Qatar is well-positioned to adopt these technologies due to its commitment to sustainability and infrastructure investments. By transitioning to greener technologies, Qatar can not only reduce its carbon footprint but also improve operational efficiency and lower long-term costs. Moreover, adopting green aviation technologies can enhance Qatar’s reputation as a forward-thinking, environmentally responsible aviation hub. Airlines in the region, such as Qatar Airways, are already exploring alternative fuel options and sustainable practices to meet future demand while aligning with global environmental standards. This presents an opportunity for both local and international stakeholders to invest in research and development for new eco-friendly aircraft, which will create growth opportunities in the aviation market.

Expansion of low-cost carriers (LCCs)

The expansion of low-cost carriers (LCCs) in the Qatar Aviation Market represents another opportunity for market growth. LCCs have gained significant traction globally due to their affordability and flexibility, and the Middle East region is no exception. With increasing demand for budget travel, particularly in the post-pandemic era, there is an opportunity for LCCs to increase their market presence in Qatar. The government’s supportive policies, such as low taxes and subsidies for air transport, make Qatar an attractive destination for LCCs. Furthermore, the region’s strategic location as a gateway between Asia, Africa, and Europe presents an ideal market for low-cost carriers looking to expand their reach. By introducing affordable and flexible flight options, LCCs can tap into the growing middle-class population in the region and cater to the increasing demand for short-haul flights. As the aviation market continues to grow, LCCs will play a crucial role in making air travel more accessible to a broader demographic.

Future Outlook

The Qatar Aviation Market is expected to experience steady growth in the next five years, driven by increasing demand for both passenger and cargo services. Technological advancements, such as the adoption of electric aircraft and digital air traffic management systems, will be critical in shaping the future of the sector. The expansion of Hamad International Airport and the development of regional airports will further enhance Qatar’s position as a leading aviation hub. Government initiatives to support sustainability and economic diversification will continue to foster the growth of the aviation industry, while a strong regulatory framework will ensure the safe and efficient operation of aviation services. With rising air traffic and improved infrastructure, the market is poised for a bright future.

Major Players

- Qatar Airways

- Gulf Air

- Doha International Airport

- Al Jaber Aviation

- Oryx Aerospace

- Emirates Aviation

- Flynas

- Air Arabia

- Etihad Airways

- Saudia

- Air India

- Turkish Airlines

- Singapore Airlines

- Lufthansa

- British Airways

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aircraftmanufacturers

- Airlines and aviation service providers

- Airport management companies

- Aviation technology providers

- Aerospace equipment suppliers

- Aviation infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables affecting the market are identified through industry reports, expert opinions, and data analytics. This includes demand for specific aviation products, technological advancements, and market challenges.

Step 2: Market Analysis and Construction

A thorough analysis is conducted to construct an accurate picture of the market. This includes studying historical data, competitor analysis, and identifying growth opportunities.

Step 3: Hypothesis Validation and Expert Consultation

The research hypotheses are validated by consulting with industry experts, stakeholders, and through secondary research sources such as government publications.

Step 4: Research Synthesis and Final Output

The collected data is synthesized, analyzed, and then transformed into a detailed report with actionable insights, supported by credible and recent information.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Tourism and Business Travel

Government Investments in Infrastructure

Expansion of Air Freight Services

Rising Adoption of Sustainable Aviation Technologies

Growth in Middle East Aviation Hub - Market Challenges

High Operational Costs

Regulatory Compliance Complexity

Volatility in Fuel Prices

Dependence on Global Supply Chains

Security and Safety Concerns - Market Opportunities

Development of Green Aviation Technologies

Expansion of Low-Cost Carriers

Growth in Air Cargo Demand - Trends

Increase in Aircraft Electrification

Adoption of Smart Airports

Implementation of Autonomous Aircraft

Integration of AI in Aviation Operations

Growth in Cross-Border Aviation Services - Government Regulations & Defense Policy

Aviation Security Policies

Airline Operational Standards

Emission Reduction Policies - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Commercial Aircraft

Private Aircraft

Helicopters

Drones

Cargo Aircraft - By Platform Type (In Value%)

Airport Terminals

Airlines Fleet Operations

Cargo Hubs

Private Airports

Military Bases - By Fitment Type (In Value%)

OEM Aircraft

Aftermarket Aircraft

Integrated Aircraft

Customized Aircraft

Electric Aircraft - By EndUser Segment (In Value%)

Government

Private Airlines

Cargo Operators

Military

General Aviation - By Procurement Channel (In Value%)

Direct Procurement

Distributors

Online Channels

B2B Procurement

Third-Party Procurement - By Material / Technology (in Value%)

Composite Materials

Metal Alloys

Avionics Systems

Electrical Systems

Autonomous Flight Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Market Value, Installed Units, Average System Price, System Complexity, Growth Rate, Regional Presence, Product Innovation, Sustainability Initiatives, Operational Efficiency, Customer Satisfaction)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Qatar Airways

Gulf Air

Doha International Airport

Qatar Aeronautical College

Qatar Aircraft Catering Company

Qatar Aviation Services

Qatar Amiri Flight

Qatar Maintenance Services

Bee’ah Aviation

Oryx Aerospace

Al Jaber Aviation

Qatar Jet Services

Emirates Aviation

Flynas

Air Arabia

- Growth in Corporate Aviation Demand

- Demand for Air Cargo in E-Commerce

- Rising Air Travel from Emerging Markets

- Growth in Military Aviation Needs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now