Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Qatar edge computing market reached approximately USD ~ billion based on a recent historical assessment derived from telecom network edge deployments, distributed data center investments, and national digital infrastructure expenditure reported by the Qatar Ministry of Communications and Information Technology and regional data center operators. Market growth is driven by 5G network rollout, latency-sensitive smart city applications, and distributed processing requirements across energy, transportation, and public safety systems requiring localized compute capacity near data generation points.

Dominance is concentrated in Doha metropolitan and industrial zones where telecom switching centers, smart city infrastructure, and enterprise digital platforms are co-located with fiber backbone and 5G base station clusters. Proximity to urban services, energy facilities, and logistics hubs enables efficient edge node placement and low-latency connectivity. Centralized national telecom architecture and state-led smart infrastructure programs reinforce Doha’s leadership in distributed computing deployment across Qatar’s digital ecosystem.

Market Segmentation

By Component

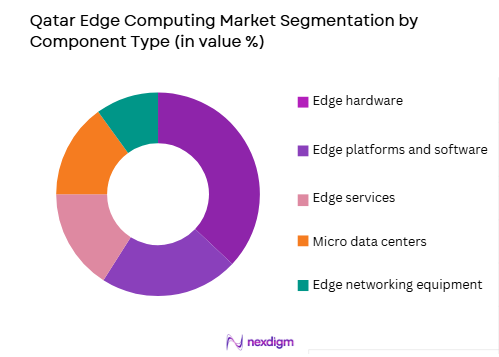

Qatar Edge Computing market is segmented by component into edge hardware, edge platforms and software, edge services, micro data centers, and edge networking equipment. Recently, edge hardware has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. National telecom and smart infrastructure deployments prioritize physical compute nodes, ruggedized servers, and embedded processing units required at base stations, substations, and industrial sites. Hardware investment forms the foundational layer for distributed computing architecture before software and services scaling. Telecom operators and utilities procure large volumes of edge servers and gateways to support 5G and IoT workloads. Edge nodes must meet environmental and reliability standards for outdoor and industrial conditions, reinforcing specialized hardware demand. Capital-intensive deployment cycles and infrastructure-first procurement strategies concentrate spending in hardware components across Qatar’s distributed computing landscape.

By End-use Industry

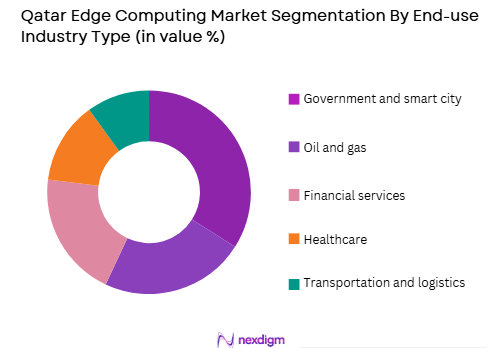

Qatar Edge Computing market is segmented by end-use industry into telecom, oil and gas, government and smart city, transportation and logistics, and healthcare. Recently, telecom has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Edge computing deployment in Qatar is tightly coupled with 5G network architecture requiring distributed processing at base stations and network aggregation points. Telecom operators deploy multi-access edge computing platforms to support low-latency applications including video analytics, IoT control, and augmented services. National broadband and 5G expansion programs generate continuous investment in edge nodes and distributed compute infrastructure. Telecom networks also host edge capacity for enterprise and government workloads, expanding utilization. As primary infrastructure owners and orchestrators of distributed connectivity, telecom providers account for the largest share of edge computing deployment across Qatar’s digital economy.

Competitive Landscape

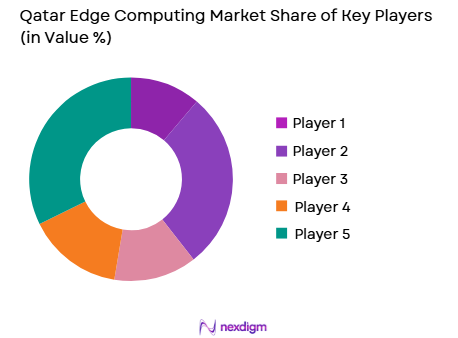

The Qatar edge computing market is moderately concentrated with telecom operators, global IT infrastructure vendors, and regional data center firms forming the core ecosystem. National telecom ownership of network infrastructure shapes deployment leadership, while partnerships with international hardware and cloud providers enable distributed computing rollout across enterprise and government sectors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Role |

| Ooredoo | 1987 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

| Vodafone Qatar | 2008 | Doha, Qatar | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | Round Rock, USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | Houston, USA | ~ | ~ | ~ | ~ | ~ |

| Cisco | 1984 | San Jose, USA | ~ | ~ | ~ | ~ | ~ |

Qatar Edge Computing Market Analysis

Growth Drivers

5G network densification and multi-access edge computing deployment across national telecom infrastructure

The nationwide rollout of 5G networks in Qatar requires distributed compute capabilities embedded within telecom architecture to enable ultra-low latency services, network virtualization, and localized data processing near users and devices. Telecom operators deploy multi-access edge computing nodes at base stations, aggregation sites, and switching facilities to support applications such as video analytics, augmented reality, and IoT automation. Edge computing reduces latency and backhaul bandwidth requirements, improving performance for smart city, public safety, and enterprise applications dependent on real-time processing. National broadband and digital infrastructure programs fund expansion of fiber and 5G coverage, directly increasing edge node density. Telecom providers monetize edge infrastructure by offering enterprise edge hosting and distributed cloud services. Integration of AI and analytics at the network edge enhances telecom service capabilities and operational efficiency. Regulatory support for advanced connectivity and digital services accelerates 5G-edge convergence. Consequently, telecom network densification remains the primary structural driver of Qatar’s edge computing market growth.

Industrial digitalization and real-time analytics requirements in oil, gas, and smart infrastructure sectors

Qatar’s industrial economy, particularly oil and gas production and smart infrastructure operations, increasingly relies on real-time data processing and automation systems that necessitate edge computing deployment near industrial assets and operational sites. Energy facilities deploy edge nodes for predictive maintenance, equipment monitoring, and safety analytics requiring low latency and localized processing due to connectivity constraints and operational criticality. Smart infrastructure such as utilities, transportation systems, and urban monitoring networks generate continuous sensor data streams processed at distributed edge locations. Industrial edge computing enhances operational efficiency, safety, and automation responsiveness in remote or high-reliability environments. National digital transformation initiatives promote adoption of industrial IoT and automation technologies requiring distributed compute capacity. Integration of AI models at the edge supports anomaly detection and autonomous control. These industrial and infrastructure use cases drive sustained investment in ruggedized edge hardware and localized computing systems across Qatar’s economy.

Market Challenges

Limited distributed data center ecosystem and concentration of compute in centralized facilities

Qatar’s digital infrastructure historically emphasizes centralized data centers and cloud platforms, creating structural imbalance in distributed compute deployment required for edge computing scalability. Limited availability of micro data center facilities and regional colocation sites constrains placement of edge nodes outside major urban zones. Telecom sites host many edge functions, but enterprise and industrial sectors lack widespread distributed hosting infrastructure. Capital intensity and relatively small geographic scale reduce incentives for extensive edge facility networks. Centralized architecture may increase latency for remote or industrial applications requiring localized processing. Developing distributed compute ecosystems requires new investment models and partnerships among telecom, utilities, and industrial operators. Absence of mature edge colocation markets slows ecosystem growth. Consequently, infrastructure concentration represents a structural challenge for widespread edge computing expansion in Qatar.

Interoperability and orchestration complexity across heterogeneous edge environments

Edge computing environments in Qatar involve diverse hardware platforms, telecom networks, industrial systems, and cloud interfaces that must interoperate seamlessly for effective distributed processing and management. Lack of standardized orchestration frameworks across telecom and enterprise edge deployments complicates integration and lifecycle management of applications. Managing distributed workloads across thousands of edge nodes requires advanced orchestration, monitoring, and security frameworks not yet fully mature in regional deployments. Vendor-specific architectures and proprietary interfaces may create fragmentation. Ensuring cybersecurity across distributed nodes introduces additional complexity. Skills shortages in edge orchestration and distributed systems engineering limit deployment efficiency. Integration with centralized cloud and AI platforms requires hybrid architecture expertise. These technical and operational complexities slow adoption and increase cost of large-scale edge computing deployment across Qatar.

Opportunities

Smart city and intelligent urban services requiring ultra-low latency distributed computing

Qatar’s smart city initiatives and urban digital infrastructure programs create substantial demand for edge computing to support real-time analytics, traffic management, surveillance, and public safety applications operating across city environments. Urban sensor networks and connected infrastructure generate continuous data streams requiring localized processing to enable immediate decision making. Edge computing enables autonomous traffic control, video analytics, and environmental monitoring without reliance on distant centralized clouds. National smart city programs prioritize responsive and resilient urban services supported by distributed compute nodes embedded within infrastructure. Integration of AI models at the edge enhances real-time analytics and automation capabilities. Telecom and municipal partnerships enable deployment across urban assets. Expansion of intelligent city platforms sustains long-term demand for distributed computing infrastructure in Qatar.

Regional edge service hub leveraging advanced connectivity and geographic position

Qatar’s advanced telecom networks, high-capacity international connectivity, and centralized governance create potential to develop distributed edge services serving regional Gulf markets and cross-border digital applications. Edge nodes integrated with submarine cable landing stations and regional network hubs can host latency-sensitive services for neighboring countries. Regional enterprises and digital platforms require distributed processing closer to end users across Gulf geography. Partnerships with international cloud and telecom providers can position Qatar as an edge service aggregation hub. Diversification of digital services exports aligns with national economic strategy. Expansion of regional IoT and connected infrastructure ecosystems increases cross-border edge demand. Consequently, regionalization of edge computing services represents a strategic growth opportunity beyond domestic deployment.

Future Outlook

The Qatar edge computing market is expected to expand as 5G densification and industrial digitalization accelerate distributed compute deployment. Growth will be driven by telecom edge platforms, smart city systems, and industrial IoT applications requiring low latency processing. Partnerships between telecom operators and global IT vendors will expand edge node infrastructure. National digital programs and connectivity investment will support deployment scale. Increasing enterprise and urban automation will sustain demand for edge computing capacity across Qatar.

Major Players

- Ooredoo

- Vodafone Qatar

- Gulf Data Hub

- Microsoft

- IBM

- Cisco

- Hewlett Packard Enterprise

- Dell Technologies

- Nokia

- Ericsson

- Huawei

- Schneider Electric

- Vertiv

- Glass House GULF

- Eden Solutions

Key Target Audience

- Government and regulatory bodies

- Investments and venture capitalist firms

- Telecom operators

- Oil and gas companies

- Smart city authorities

- Transportation and logistics operators

- Industrial automation firms

- Cloud and data center service providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including telecom edge deployment density, industrial IoT adoption, distributed data center capacity, and sectoral latency requirements were identified from national ICT strategies and telecom infrastructure data. Edge architecture layers and component categories were defined to structure the market.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using telecom network expansion, enterprise edge deployment, and industrial automation investment across sectors. Component and industry demand distribution were analyzed to estimate relative shares and deployment concentration.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with telecom engineers, edge computing vendors, and regional infrastructure experts active in Gulf markets. Deployment data and technology adoption patterns were cross-checked with industry reports and operator disclosures.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured analysis covering segmentation, competitive landscape, drivers, constraints, and opportunities. Quantitative deployment indicators and qualitative technology trends were integrated to produce a comprehensive outlook for Qatar’s edge computing ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

5G deployment enabling low latency edge computing

Smart city and IoT infrastructure expansion

Enterprise demand for real time data processing - Market Challenges

High deployment and integration cost

Limited edge ecosystem maturity

Data security and distributed management complexity - Market Opportunities

Edge AI and real time analytics applications

Industry specific edge infrastructure deployment

Integration of edge with national cloud platforms - Trends

Convergence of edge and cloud architectures

AI enabled edge processing growth

Distributed micro data center deployment - Government regulations

Data localization and edge compliance frameworks

Telecom and 5G infrastructure regulations

Cybersecurity and critical infrastructure standards - SWOT analysis

- Porters Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Data Centers

On Premise Edge Infrastructure

Industrial Edge Computing Systems

Telecom Edge Nodes

AI Enabled Edge Platforms - By Platform Type (In Value%)

Multi Access Edge Computing Platforms

Industrial IoT Edge Platforms

AI Inference Edge Systems

Edge Cloud Platforms

5G Edge Infrastructure - By Fitment Type (In Value%)

Telecom Network Integrated Edge

Enterprise Edge Deployments

Smart City Edge Infrastructure

Energy and Utility Edge Systems

Hybrid Edge Cloud Deployments - By EndUser Segment (In Value%)

Telecom and 5G Operators

Government and Smart City Programs

Energy and Industrial Enterprises

Transportation and Logistics Operators

Healthcare and Public Safety Organizations - By Procurement Channel (In Value%)

Telecom Infrastructure Providers

Cloud and Edge Platform Vendors

System Integrators

Government Technology Programs

Enterprise Direct Procurement

- Market Share Analysis

- Cross Comparison Parameters (Edge Latency Performance, Distributed Deployment Scalability, AI Inference Capability at Edge, 5G and MEC Integration, Edge Cloud Orchestration Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ooredoo Edge

Vodafone Qatar Edge

Nokia Edge Computing

Ericsson Edge Infrastructure

Huawei Edge

Dell Technologies Edge

HPE Edgeline

Cisco Edge Computing

Microsoft Azure Edge

Amazon Web Services Wavelength

Google Distributed Cloud Edge

Schneider Electric Edge

Siemens Industrial Edge

Qatar Data Centre Edge

Meeza Edge

- Telecom operators deploying MEC platforms

- Government expanding smart city edge nodes

- Energy sector adopting industrial edge systems

- Enterprises enabling real time analytics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now