Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Qatar Fighter Aircraft Market is primarily driven by the country’s growing defense expenditure and strategic need to modernize its military capabilities. As of the most recent data, Qatar’s military spending has been consistently rising, with defense budgets allocated to acquiring cutting-edge fighter aircraft to ensure air superiority in the Gulf region. The market size for fighter aircraft is estimated at USD ~ billion in 2024. This figure reflects Qatar’s robust spending on both new acquisitions and fleet modernization, aiming to maintain technological parity with regional powers. The driving factors include geopolitical tensions, defense alliances with global powers, and a constant need to upgrade its military capabilities to ensure national security.

In the Qatar Fighter Aircraft Market, the country itself is the dominant player, with the Qatar Emiri Air Force (QEAF) being the principal end-user. Qatar has been actively expanding and modernizing its fleet, and its strong economic standing, bolstered by natural gas exports, allows it to invest significantly in advanced military systems. Additionally, Qatar has fostered strong defense relationships with global powers like the United States and France, which allows it to acquire state-of-the-art fighter aircraft like the Dassault Rafale and Boeing F-15QA. This strategic focus on acquiring technologically advanced fighter platforms has positioned Qatar as a leader in the Gulf region in terms of air defense.

Market Segmentation

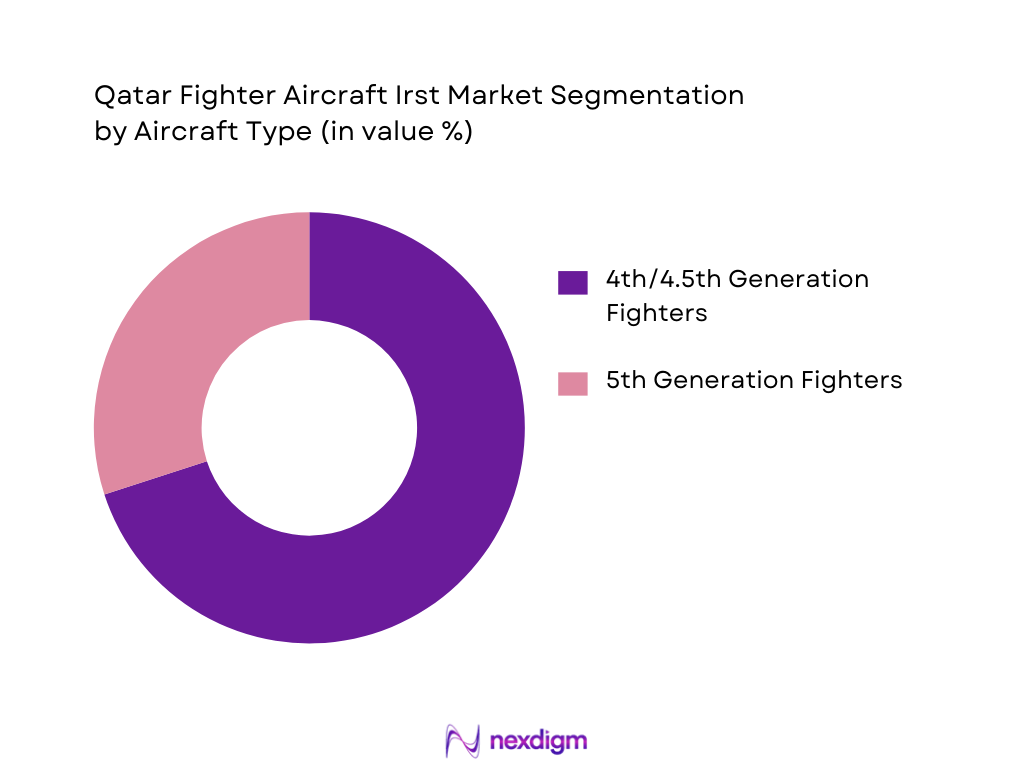

By Aircraft Type

The Qatar fighter aircraft market is primarily segmented into 4th/4.5th Generation Fighters and 5th Generation Fighters. The 4th/4.5th Generation Fighters, including the Dassault Rafale and Boeing F-15QA, dominate the market due to Qatar’s focus on advanced yet proven aircraft. These platforms offer a balance of performance and cost-effectiveness, and they are highly integrated into regional defense systems. These fighter jets are used for air superiority, precision strike, and close air support missions. The demand for 4th/4.5th Generation Fighters is driven by Qatar’s immediate need to enhance its defense capabilities, while future investments are likely to shift towards 5th Generation Fighters as the region’s security dynamics evolve.

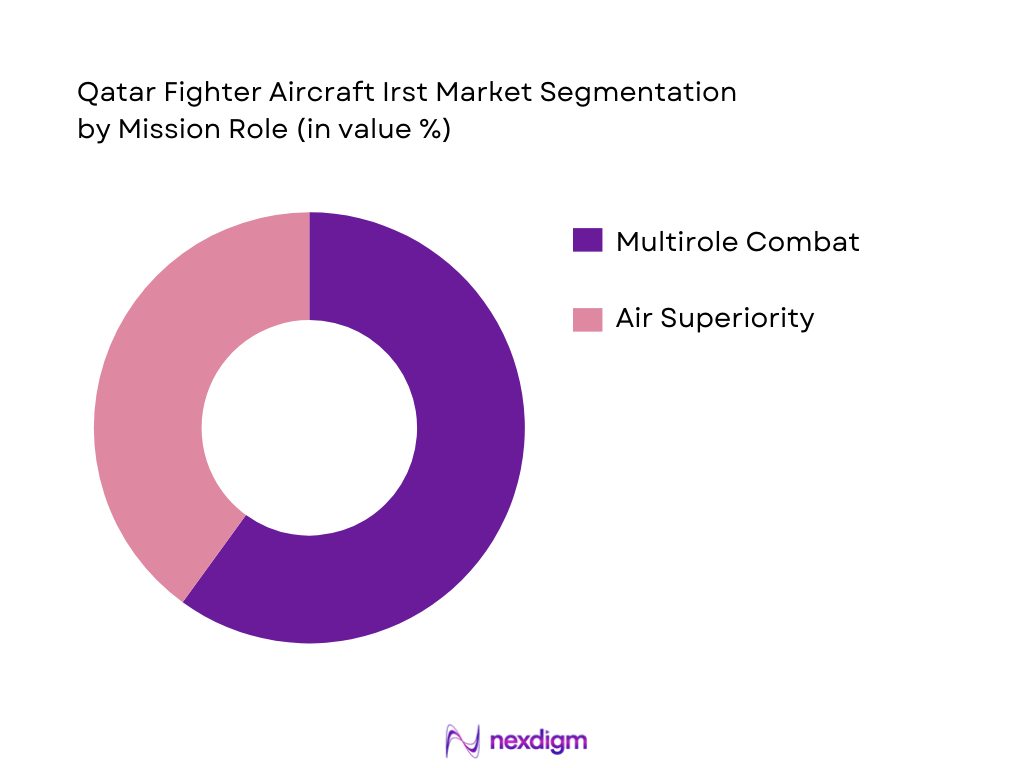

By Mission Role

The market is further divided based on the mission roles of the aircraft. Qatar places significant emphasis on multirole combat fighters, which contribute heavily to its fleet composition. These versatile aircraft serve a broad range of functions, from air superiority to precision strike and reconnaissance. Air Superiority is another dominant segment in Qatar’s fighter aircraft market, as controlling the skies is a top priority for ensuring national security. The Multirole category is likely to see sustained growth as the demand for versatile platforms increases, with advanced multirole fighters capable of adapting to different combat scenarios being prioritized in Qatar’s defense strategy.

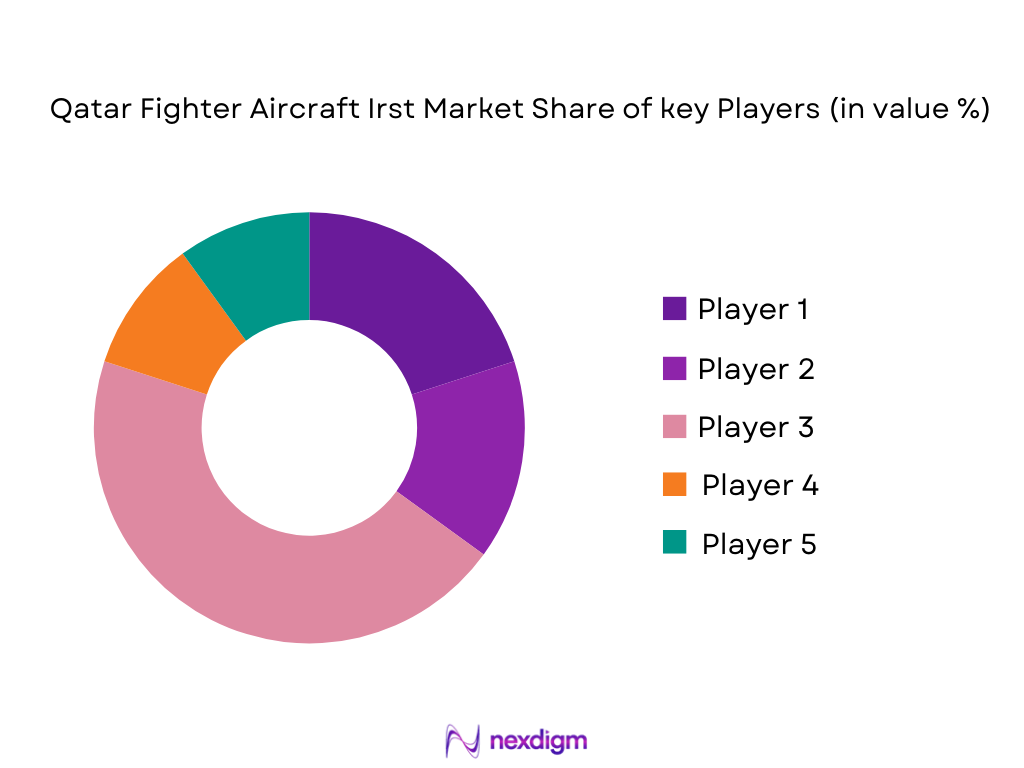

Competitive Landscape

The Qatar Fighter Aircraft Market is dominated by a few key global players, each offering a wide range of fighter platforms tailored to Qatar’s defense needs. Major defense contractors, including Dassault Aviation, Boeing, Lockheed Martin, BAE Systems, and Airbus Defense, dominate the market. These companies benefit from long-standing relationships with Qatar, providing not only advanced aircraft but also comprehensive support and maintenance services.

| Company | Establishment Year | Headquarters | Product Range | Global Presence | Military Contracts | Support Services |

| Boeing | 1916 | Chicago, USA | ~ | ~ | ~ | ~ |

| Dassault Aviation | 1929 | Paris, France | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | London, UK | ~ | ~ | ~ | ~ |

| Airbus Defense | 2000 | Toulouse, France | ~ | ~ | ~ | ~ |

Qatar Fighter Aircraft Irst Market Analysis

Growth Drivers

Strategic Fleet Expansion and Airpower Modernization

Qatar’s focus on strategic fleet expansion and airpower modernization is a significant growth driver for its fighter aircraft market. With increasing regional tensions and a focus on technological superiority, Qatar aims to modernize its fleet by acquiring advanced 4th and 5th-generation fighter aircraft. This strategy enhances the country’s defense capabilities, ensuring air dominance and the ability to meet evolving security threats. Modernizing the air force also involves updating avionics, weaponry, and integrating the latest technologies into existing platforms.

Regional Air Defense Requirements

The geopolitical landscape of the Middle East, with ongoing security challenges, drives the demand for robust air defense systems in Qatar. With neighboring countries like Iran exerting influence in the region, Qatar requires a strong air defense mechanism to maintain its territorial integrity. The country’s reliance on air superiority to safeguard its borders and strategic interests compels it to invest in advanced fighter aircraft capable of securing airspace, performing high-value strike missions, and contributing to broader regional defense initiatives alongside allied forces.

Restraints

High Acquisition & Lifecycle Costs

A significant challenge for Qatar’s fighter aircraft market lies in the high acquisition and lifecycle costs associated with advanced fighter platforms. The price of procuring state-of-the-art aircraft like the Rafale or F-15QA involves substantial financial investment, which puts pressure on defense budgets. Additionally, maintenance, repair, and operational costs throughout the lifecycle of these aircraft can be significant, affecting the long-term sustainability of fleet operations. These financial constraints force Qatar to balance between cutting-edge technology and cost-effectiveness in its procurement decisions.

Pilot & Technical Skill Constraints

Qatar faces challenges related to pilot training and technical skill development. As the country invests in more advanced fighter aircraft, there is an increasing need for highly skilled pilots and maintenance personnel to operate and maintain these sophisticated platforms. The rapid pace of technological advancements in avionics, weapons systems, and flight dynamics requires continuous training programs. Qatar must ensure that it develops a sufficient pool of qualified personnel through investment in training infrastructure, partnerships with defense contractors, and knowledge transfer from allied nations.

Opportunities

Local Maintenance, Repair & Overhaul (MRO) and Sustainment Hubs

The establishment of local Maintenance, Repair & Overhaul (MRO) facilities in Qatar is an opportunity that can significantly enhance the country’s defense self-sufficiency. Developing indigenous MRO capabilities for fighter aircraft can reduce dependency on foreign contractors for routine maintenance and repairs. These hubs also offer potential for long-term cost savings, improved operational readiness, and faster turnaround times for aircraft. Qatar’s investment in MRO can also stimulate the local economy by creating skilled jobs and fostering technological expertise in the defense sector.

Technology Transfer & Joint Development Options

Technology transfer and joint development opportunities present significant growth potential for Qatar’s fighter aircraft market. By engaging in strategic partnerships with major defense contractors, Qatar can gain access to advanced technology and engineering expertise. These partnerships can lead to the development of bespoke solutions tailored to Qatar’s specific defense needs. Furthermore, technology transfer agreements allow the country to boost its local defense capabilities, reduce reliance on foreign suppliers, and enhance its overall self-reliance in military technologies, fostering long-term national security benefits.

Future Outlook

Over the next five years, the Qatar Fighter Aircraft Market is expected to continue growing at a robust pace. This growth will be driven by sustained government defense spending, which is expected to prioritize the acquisition of next-generation fighter aircraft and advanced avionics systems. Qatar’s strategic focus on air superiority and the modernization of its air fleet, including potential procurements of 5th-generation fighters, will play a crucial role in expanding the market. Additionally, increasing tensions in the Gulf and the broader Middle East region, coupled with rising defense budgets, will further fuel demand for state-of-the-art combat aircraft. The market will also witness a rise in upgrades and enhancements of existing fleets, further propelling growth in maintenance, repair, and overhaul (MRO) services.

Major Players

- Boeing

- Dassault Aviation

- Lockheed Martin

- BAE Systems

- Airbus Defense

- Northrop Grumman

- Raytheon Technologies

- General Dynamics

- Thales

- Leonardo

- Rolls-Royce

- SAAB

- Embraer

- Elbit Systems

- MBDA

Key Target Audience

- Defense Ministry and Armed Forces (Qatar Ministry of Defense)

- Government and Regulatory Bodies (Qatar Civil Aviation Authority)

- Defense Contractors and OEMs (Boeing, Lockheed Martin, Dassault Aviation, etc.)

- Investment and Venture Capitalist Firms

- Military and Defense Analysts

- Regional Security Agencies (Gulf Cooperation Council Defense Committees)

- International Defense Procurement Agencies

- Aerospace and Defense Suppliers

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Qatar Fighter Aircraft Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the Qatar Fighter Aircraft Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIS) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple fighter aircraft manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Qatar Fighter Aircraft Market.

- Executive Summary

- Research Methodology (Market Definitions and Defense Classifications (fighter generations, mission roles), Abbreviations (e.g., EW, ISR, AEW&C, AESA, MRO), Data Collection Framework (DEFEX, SIPRI, IHS Markit, government procurement disclosures), Market Sizing Methodology (Top‑down defense budget allocation, bottom‑up fleet valuation), Primary Research Protocol (Defense OEMs, military analysts, procurement officers), Forecast Assumptions and Constraints

- Qatar Fighter Aircraft Market Context

- Strategic Defense Posture and Airpower Doctrine

- Regional Security Dynamics (Gulf safety corridors, air denial zones)

- Role of Fighter Aircraft in National Air Defense vs. Air Superiority

- National Defense Budget & Fighter Procurement Share

- Growth Drivers

Strategic Fleet Expansion and Airpower Modernization

Regional Air Defense Requirements

Acquisition of Advanced Sensors, AESA Radars, EW Suites

Pilot Training & Simulation Scaling - Market Challenges

High Acquisition & Lifecycle Costs

Pilot & Technical Skill Constraints

Export Control Regimes and Compliance

Geopolitical Constraints on 5th Gen Procurement - Market Opportunities

Potential F‑35 Procurement Pathways

Local Maintenance, Repair & Overhaul (MRO) and Sustainment Hubs

Technology Transfer & Joint Development Options - Market Trends

Stealth & Sensor Fusion Emphasis

Data Links & Network‑Centric Warfare Integration

Indigenous Support Ecosystem Growth - Regulatory & Policy Landscape

Foreign Military Sales (FMS) Governance

Offset Agreements & Local Capability Development

Export Licensing and ITAR Impacts - SWOT and PESTLE Highlights

- Market Value, 2020-2025

- Volume Consumption Across Subsegments, 2020-2025

- Composite Adoption Intensity, 2020-2025

- By Aircraft Generation (In Value %)

4th/4.5th Generation (e.g., Rafale, Typhoon)

5th Generation (potential F‑35 acquisition interest) - By Mission Role (In Value %)

Air Superiority

Multirole Combat

Interceptor

Close Air Support

Electronic Warfare / SEAD/DEAD - By Take‑Off and Landing Configuration (In Value %)

Conventional Take‑Off and Landing (CTOL)

Short Take‑Off/Vertical Landing (STOVL) (if applicable) - By Engine Configuration (In Value %)

Twin‑Engine Fighters

Single‑Engine Fighter - By End User (In Value %)

Qatar Emiri Air Force (QEAF)

Defense Joint Programs / Coalition Integrations

- Market Share & Positioning

- Cross‑Comparison Parameters (Company Overview, Fighter Platform Portfolio, Contract Backlog in Region, Combat Capability Index, Integration Support Network, After‑Sales Sustainment Capability, Local Presence / Defense Offset Engagement, R&D Technology Roadmap)

- Detailed Profiles of Major Competitors

Boeing – F‑15QA Platform

Lockheed Martin – F‑35 / F‑16 Family

Dassault Aviation – Rafale

BAE Systems – Eurofighter Typhoon

SAAB – Gripen Offerings

Northrop Grumman – Avionics & EW Systems

Raytheon Technologies – Missile & Sensor Systems

Airbus Defense – Tornado/Support Solutions

Leonardo – EW & Mission Systems

General Dynamics – Support & Training Solutions

Rolls‑Royce – Engine Support (RB Series)

MBDA – Air‑to‑Air Missiles (Meteor, ASRAAM)

Elbit Systems – Avionics Upgrades

Thales – Radar & Defense Electronics

Kongsberg Defense – Integrated Weapons

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- Forecast by Value & Growth Scenarios, 2026-2035

- Forecast by Volume & Composite Penetration, 2026-2035

- Future Demand by Aircraft Segment, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now