Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Qatar Healthcare Infrastructure Market was valued at approximately USD ~ billion, supported by sustained public investment in healthcare facilities, expansion of hospital networks, and modernization of clinical infrastructure across the country. Large-scale national healthcare programs and long-term public health strategies implemented by the Ministry of Public Health and Hamad Medical Corporation continue to drive infrastructure expansion, including hospitals, specialty centers, diagnostic facilities, and primary healthcare networks across the national healthcare system.

Doha remains the dominant center for healthcare infrastructure development due to the concentration of major hospitals, specialty medical complexes, and advanced research institutions. Large public healthcare providers including Hamad Medical Corporation operate major tertiary hospitals in the capital, while new integrated medical cities and private hospital projects are expanding capacity. Rapid urbanization, strong healthcare demand, and national initiatives supporting high-quality medical services continue strengthening healthcare infrastructure development across Doha and surrounding urban districts.

Market Segmentation

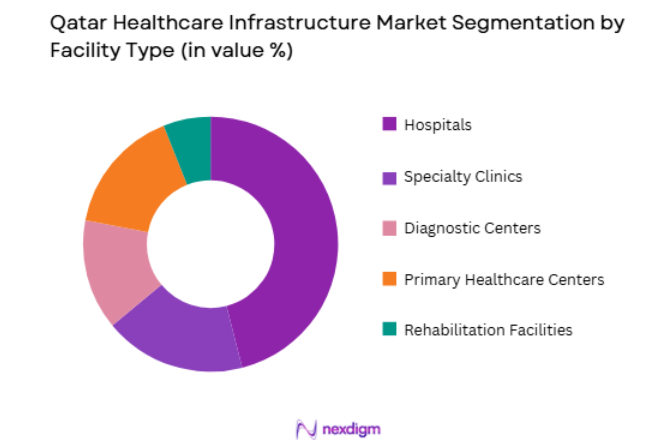

By Facility Type

Qatar Healthcare Infrastructure market is segmented by facility type into Hospitals, Specialty Clinics, Diagnostic Centers, Primary Healthcare Centers, and Rehabilitation Facilities. Recently, Hospitals has a dominant market share due to factors such as higher patient capacity, government investment in large tertiary hospitals, and the concentration of specialized medical services within hospital campuses. Large hospital complexes accommodate advanced surgical departments, emergency care units, oncology centers, and specialized diagnostic facilities, making them the central pillar of healthcare infrastructure development. Qatar’s national healthcare expansion programs emphasize hospital construction to meet rising demand from population growth and medical tourism initiatives. Government healthcare authorities prioritize hospital modernization projects including expansion of inpatient beds, advanced operating theaters, and integrated digital hospital systems. Major hospital developments in Doha incorporate multi-specialty services under a single infrastructure platform, increasing operational efficiency and clinical capacity.

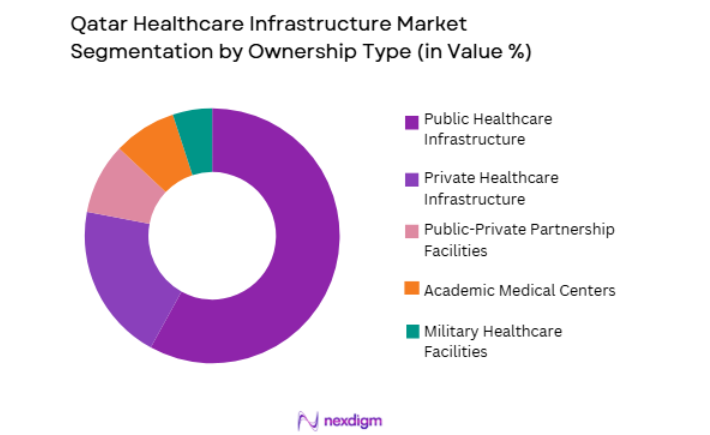

By Ownership Type

Qatar Healthcare Infrastructure market is segmented by ownership type into Public Healthcare Infrastructure, Private Healthcare Infrastructure, Public-Private Partnership Facilities, Academic Medical Centers, and Military Healthcare Facilities. Recently, Public Healthcare Infrastructure has a dominant market share due to factors such as strong government funding, centralized healthcare planning, and large-scale public hospital networks managed by national healthcare authorities. The government plays a central role in financing healthcare infrastructure projects through long-term national development programs focused on improving healthcare accessibility and clinical capacity. Major public institutions such as Hamad Medical Corporation and the Primary Health Care Corporation operate extensive networks of hospitals and primary care centers that form the backbone of the national healthcare system. These facilities deliver a large proportion of specialized medical services including trauma care, oncology treatment, cardiovascular surgery, and critical care services.

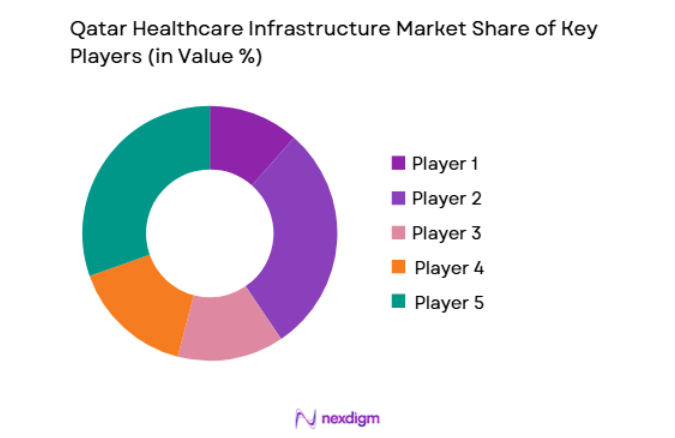

Competitive Landscape

The Qatar Healthcare Infrastructure Market is moderately consolidated, with the public healthcare sector playing a dominant role in infrastructure ownership and development while private hospital groups and international healthcare providers expand their presence through specialized medical facilities. Government-backed healthcare institutions control a large share of hospital infrastructure capacity, while private sector investment focuses on specialty hospitals, outpatient clinics, and diagnostic facilities. Strategic partnerships, hospital expansion projects, and investments in advanced medical technology continue shaping competitive dynamics.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Hospital Capacity |

| Hamad Medical Corporation | 1979 | Doha | ~ | ~ | ~ | ~ | ~ |

| Primary Health Care Corporation | 2012 | Doha | ~ | ~ | ~ | ~ | ~ |

| Aster DM Healthcare | 1987 | Dubai | ~ | ~ | ~ | ~ | ~ |

| Sidra Medicine | 2018 | Doha | ~ | ~ | ~ | ~ | ~ |

| Al Ahli Hospital | 2004 | Doha | ~ | ~ | ~ | ~ | ~ |

Qatar Healthcare Infrastructure Market Analysis

Growth Drivers

Expansion of National Healthcare Infrastructure under Qatar National Vision Programs

Expansion of National Healthcare Infrastructure under Qatar National Vision Programs drives sustained growth in the Qatar Healthcare Infrastructure Market as the government continues investing heavily in modern medical facilities to ensure long-term healthcare capacity for the country’s population. Qatar’s national development strategy places healthcare infrastructure at the center of social development policies, encouraging construction of hospitals, specialized medical centers, and primary healthcare networks that improve accessibility and service quality across the healthcare system. Large public investments support expansion of inpatient bed capacity, advanced surgical facilities, diagnostic laboratories, and integrated hospital information systems that collectively strengthen clinical service delivery. Healthcare authorities also prioritize modernization of existing hospitals by integrating digital patient management systems, advanced imaging equipment, and smart hospital technologies that improve operational efficiency and patient outcomes. Rapid population growth and increasing life expectancy increase demand for healthcare services, requiring continuous infrastructure expansion to accommodate rising patient volumes across hospitals and outpatient care facilities. The government also invests in specialized treatment centers focused on oncology, cardiology, and rehabilitation medicine to address the growing prevalence of chronic diseases and complex medical conditions among residents. National healthcare planning emphasizes geographic distribution of healthcare facilities to ensure equitable access to medical services across urban and suburban areas. Investments in research hospitals and academic medical centers also strengthen Qatar’s healthcare innovation ecosystem while improving clinical education and specialist training programs.

Rising Demand for Specialized Healthcare Services and Medical Technology Integration

Rising Demand for Specialized Healthcare Services and Medical Technology Integration drives expansion of healthcare infrastructure across Qatar as hospitals and medical centers increasingly adopt advanced medical technologies to deliver specialized clinical services and improve treatment outcomes. Growing prevalence of chronic diseases including cardiovascular conditions, diabetes, and cancer increases demand for sophisticated diagnostic and treatment facilities capable of managing complex patient cases. Healthcare providers therefore invest in advanced imaging centers, surgical theaters equipped with robotic technology, and specialized clinical units dedicated to oncology, cardiology, neurology, and intensive care services. Technological advancements in medical equipment also require modern hospital infrastructure capable of supporting high-precision diagnostic systems, integrated digital health platforms, and real-time patient monitoring technologies. Hospitals increasingly integrate artificial intelligence-based diagnostic systems and digital patient management platforms that require advanced IT infrastructure within healthcare facilities. Rising patient expectations regarding healthcare quality and accessibility also encourage hospitals to expand outpatient departments, ambulatory surgery centers, and specialty clinics that deliver faster medical services. Medical tourism initiatives further increase demand for high-quality healthcare facilities capable of attracting international patients seeking specialized treatments. Healthcare providers respond by constructing new private hospitals and upgrading existing medical campuses to include advanced medical technologies and luxury patient care environments.

Market Challenges

High Capital Expenditure Requirements for Healthcare Infrastructure Projects

High Capital Expenditure Requirements for Healthcare Infrastructure Projects presents a significant challenge for the Qatar Healthcare Infrastructure Market because construction and modernization of hospitals require substantial financial investment across building development, medical equipment procurement, and digital infrastructure implementation. Advanced hospital facilities involve complex architectural design, specialized clinical equipment installation, and strict regulatory compliance standards that increase project costs and extend construction timelines. Large tertiary hospitals require extensive capital investment to establish operating theaters, intensive care units, diagnostic laboratories, and specialized treatment centers capable of delivering advanced healthcare services. Additionally, integration of modern digital hospital technologies including electronic medical records, telemedicine platforms, and automated diagnostic systems increases infrastructure development costs. Healthcare infrastructure projects also involve significant operational expenses associated with staffing, maintenance of medical equipment, and continuous upgrades to clinical technologies. While government funding supports many public healthcare facilities, large private sector investments may face financial constraints due to the high upfront capital required for hospital development. Long development cycles associated with healthcare construction projects further increase financial risks for investors because infrastructure projects often require several years before generating stable operational revenue. Healthcare developers must also allocate additional resources to meet international healthcare accreditation standards and ensure patient safety regulations are fully implemented within medical facilities.

Healthcare Workforce Availability and Specialized Medical Staffing Constraints

Healthcare Workforce Availability and Specialized Medical Staffing Constraints represents another major challenge affecting the Qatar Healthcare Infrastructure Market because healthcare facilities require a highly skilled workforce to operate advanced hospitals and specialized medical centers effectively. Expansion of hospital infrastructure must be accompanied by sufficient availability of trained physicians, nurses, technicians, and healthcare administrators capable of managing complex clinical operations. Qatar relies significantly on an international healthcare workforce, making recruitment dependent on global medical labor markets and immigration policies. Competition for highly specialized medical professionals such as surgeons, oncologists, and intensive care specialists increases recruitment challenges for newly developed hospitals. Healthcare facilities also require trained biomedical engineers, medical technologists, and health information system professionals to operate advanced medical equipment and digital healthcare platforms. Rapid expansion of healthcare infrastructure therefore creates simultaneous demand for skilled medical personnel across multiple healthcare institutions. Training programs and medical education initiatives help address workforce gaps, but developing specialized expertise requires significant time and investment. Healthcare institutions must also implement continuous training programs to ensure medical staff remain updated with evolving clinical technologies and treatment protocols.

Opportunities

Development of Integrated Medical Cities and Healthcare Clusters

Development of Integrated Medical Cities and Healthcare Clusters creates significant opportunities for the Qatar Healthcare Infrastructure Market because large integrated healthcare campuses enable efficient delivery of multidisciplinary medical services within a single infrastructure ecosystem. Healthcare clusters combine hospitals, specialty clinics, research institutions, and medical education facilities within coordinated medical campuses that improve collaboration between healthcare providers and research organizations. These integrated healthcare environments support advanced treatment capabilities, clinical research initiatives, and medical training programs simultaneously, creating comprehensive healthcare ecosystems capable of delivering complex medical services. Governments increasingly support development of such medical clusters to enhance healthcare accessibility while promoting medical innovation and international healthcare collaboration. Integrated medical cities also attract private healthcare investment and international hospital operators seeking opportunities to participate in large healthcare infrastructure projects. Medical clusters facilitate centralized procurement of medical equipment, shared diagnostic services, and coordinated patient care pathways that improve healthcare delivery efficiency. These healthcare ecosystems also support development of biotechnology research facilities, pharmaceutical innovation centers, and academic medical institutions that strengthen the broader healthcare industry. Medical tourism initiatives further encourage investment in integrated healthcare campuses capable of delivering specialized treatments for international patients. Expansion of such healthcare clusters therefore represents a major infrastructure development opportunity for Qatar’s healthcare sector.

Expansion of Digital Healthcare Infrastructure and Smart Hospital Systems

Expansion of Digital Healthcare Infrastructure and Smart Hospital Systems presents a strong opportunity for the Qatar Healthcare Infrastructure Market because digital technologies are transforming hospital operations, patient management, and clinical decision-making processes across modern healthcare systems. Smart hospitals integrate advanced digital technologies including electronic medical records, artificial intelligence diagnostic tools, telemedicine platforms, and automated patient monitoring systems to improve healthcare delivery efficiency. Healthcare providers increasingly invest in digital infrastructure capable of supporting real-time data exchange between hospitals, clinics, laboratories, and pharmacies within the national healthcare network. Digital healthcare platforms enable remote consultations, digital prescriptions, and continuous patient monitoring which reduce hospital congestion and improve healthcare accessibility. Hospitals also implement smart building technologies that optimize energy usage, equipment maintenance, and patient flow management within healthcare facilities. Integration of big data analytics allows healthcare institutions to analyze clinical outcomes and optimize treatment protocols using large patient datasets. Digital hospital infrastructure therefore enhances operational efficiency while improving diagnostic accuracy and patient care coordination. Continued government support for digital health innovation further accelerates investments in smart hospital technologies and healthcare information systems. These technological advancements create substantial opportunities for healthcare infrastructure developers and technology providers operating within the Qatar healthcare ecosystem.

Future Outlook

The Qatar Healthcare Infrastructure Market is expected to expand steadily over the next five years as the government continues prioritizing healthcare modernization and capacity expansion. Investments in hospital construction, digital health systems, and specialized medical centers are likely to strengthen the country’s healthcare capabilities. Technological innovation in smart hospitals and advanced diagnostics will shape infrastructure development. Rising healthcare demand, population growth, and medical tourism initiatives will further support long-term infrastructure expansion.

Major Players

- Hamad Medical Corporation

- Primary Health Care Corporation

- Sidra Medicine

- Aster DM Healthcare

- Al Ahli Hospital

- NMC Healthcare

- Aman Hospital

- Doha Clinic Hospital

- Turkish Hospital Qatar

- Al Emadi Hospital

- Elegancia Healthcare

- Al Wakra Hospital

- Qatar Rehabilitation Institute

- Heart Hospital Qatar

- Hazm Mebaireek General Hospital

Key Target Audience

- Government and regulatory bodies

- Hospital operators

- Healthcare infrastructure developers

- Private hospital groups

- Medical equipment manufacturers

- Healthcare technology providers

- Investments and venture capitalist firms

- Health insurance providers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing the Qatar Healthcare Infrastructure Market were identified through analysis of healthcare investment patterns, hospital capacity expansion, government health programs, and infrastructure development initiatives across the national healthcare system.

Step 2: Market Analysis and Construction

Market structure was developed by analyzing healthcare facility expansion, hospital construction projects, infrastructure spending, and healthcare demand indicators across Qatar’s public and private healthcare sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry insights were validated through expert interviews with healthcare administrators, hospital planners, and healthcare infrastructure specialists to confirm market assumptions and infrastructure development trends.

Step 4: Research Synthesis and Final Output

All findings were synthesized through data triangulation combining infrastructure investment data, healthcare policy analysis, and expert inputs to produce a structured and validated market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government investments in healthcare infrastructure under Qatar National Vision 2030

Expansion of advanced hospitals and specialty care facilities

Rising healthcare demand driven by population growth and expatriate workforce - Market Challenges

High capital investment required for healthcare facility development

Dependence on imported medical equipment and technologies

Shortage of specialized healthcare professionals in certain fields - Market Opportunities

Development of integrated medical cities and specialized healthcare zones

Expansion of private sector participation in healthcare infrastructure

Investment in digitally integrated smart hospital infrastructure - Trends

Adoption of smart hospital technologies and AI driven healthcare systems

Growth of specialized treatment centers for oncology cardiology and fertility care - Government Regulations

Healthcare licensing and accreditation under the Ministry of Public Health

Regulatory standards governing hospital construction and medical equipment

Policies supporting medical tourism and healthcare infrastructure development - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hospital Infrastructure Development

Specialty Medical Center Infrastructure

Ambulatory Surgical Center Infrastructure

Diagnostic and Imaging Center Infrastructure

Primary Healthcare Clinic Infrastructure - By Platform Type (In Value%)

Public Healthcare Infrastructure

Private Healthcare Infrastructure

Public Private Partnership Healthcare Projects

Integrated Healthcare City Developments

Academic Medical Center Infrastructure - By Fitment Type (In Value%)

New Hospital Construction Projects

Hospital Expansion and Capacity Upgrade Projects

Advanced Medical Equipment Infrastructure Integration

Smart Hospital Digital Infrastructure - By End User Segment (In Value%)

Government Healthcare Authorities

Private Hospital Groups

Diagnostic and Specialty Medical Centers

- Market Share Analysis

- Cross Comparison Parameters (Hospital Bed Capacity Expansion, Infrastructure Investment Scale, Technology Integration Level, Specialty Care Capability, Healthcare Accreditation Standards)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Hamad Medical Corporation

Sidra Medicine

Aster DM Healthcare Qatar

Naseem Healthcare

Al Emadi Hospital

Doha Clinic Hospital

Al Ahli Hospital

Qatar Medical Center

The View Hospital

Al Khor Hospital

Rumailah Hospital

Heart Hospital Qatar

Aspetar Orthopedic and Sports Medicine Hospital

Al Wakra Hospital

Al Aziziyah Medical Center

- Government authorities expanding public hospitals and community healthcare centers

- Private hospital groups investing in advanced multi specialty facilities

- Diagnostic centers deploying high precision imaging and laboratory technologies

- Medical tourism providers developing specialized treatment facilities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now