Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Qatar’s home finance market demonstrates strong institutional depth, with outstanding residential mortgage lending exceeding USD ~ billion based on central bank banking sector credit disclosures. Market expansion is driven by state-backed housing programs, employer-linked expatriate financing demand, and bank balance sheet capacity supported by hydrocarbon-derived liquidity. Sharia-compliant structures dominate origination volumes as Islamic banks extend long-tenor home financing aligned with national homeownership policy frameworks and regulated mortgage caps.

Within Qatar, Doha and its metropolitan municipalities dominate home finance activity due to concentration of population, employment centers, and large-scale residential developments supported by infrastructure investment corridors. Demand is reinforced by expatriate professional housing requirements and national housing allocation programs targeting Qatari households. High-income public sector employment, stable banking liquidity, and planned urban expansion projects sustain mortgage origination volumes and property transaction financing concentration within the capital region.

Market Segmentation

By Product Type

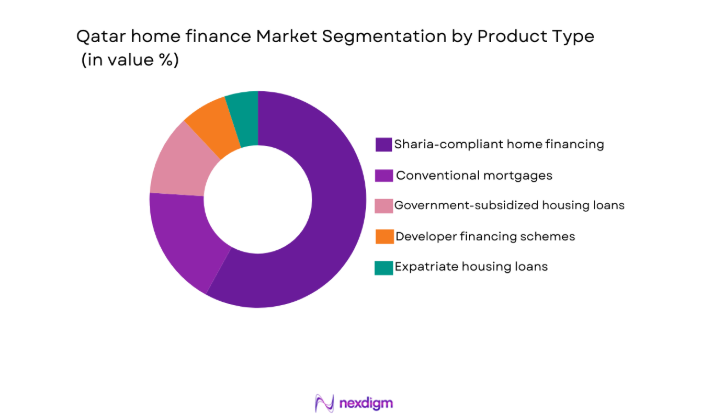

Qatar home finance market is segmented by product type into Sharia-compliant home financing, conventional mortgages, government-subsidized housing loans, developer financing schemes, and expatriate housing loans. Recently, Sharia-compliant home financing has a dominant market share due to factors such as strong consumer religious alignment, Islamic bank market leadership, regulatory encouragement of Sharia structures, and extensive availability across major lenders. Islamic contracts including Ijara and Murabaha enable asset-backed ownership transfer structures compatible with national housing programs and bank funding models. Government housing allocations for nationals are frequently structured through Islamic financing frameworks administered via domestic banks, reinforcing origination dominance. Islamic lenders maintain extensive branch networks and employer payroll-linked financing channels, facilitating borrower onboarding and repayment certainty. Customer perception of ethical finance and risk-sharing mechanisms further supports sustained preference over conventional mortgages in Qatar’s predominantly Islamic financial ecosystem.

By Platform Type

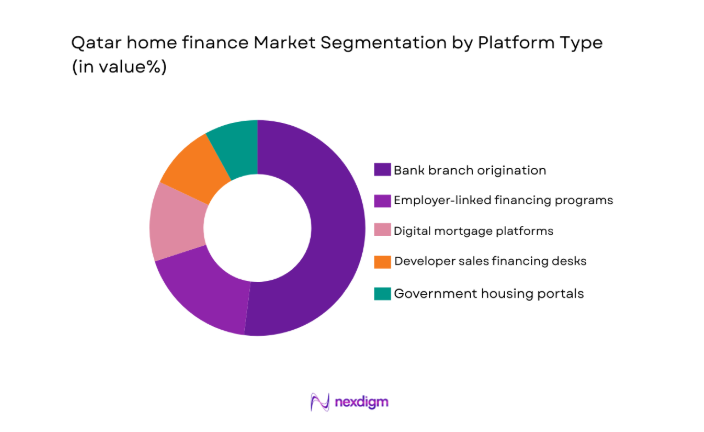

Qatar home finance market is segmented by platform type into bank branch origination, employer-linked financing programs, digital mortgage platforms, developer sales financing desks, and government housing portals. Recently, bank branch origination has a dominant market share due to factors such as relationship-based lending culture, documentation-intensive underwriting, regulatory compliance requirements, and borrower preference for in-person advisory. Mortgage approvals in Qatar often require income verification, residency status validation, and property documentation review, processes facilitated through physical banking infrastructure. Major banks maintain dedicated housing finance departments integrated with valuation and legal processing functions, enabling end-to-end origination within branches. Employer-linked payroll financing agreements are also executed through bank relationship channels rather than standalone digital platforms. Customer trust in established domestic banks and preference for advisory-led financing decisions further sustain physical origination dominance despite emerging digital application capabilities.

Competitive Landscape

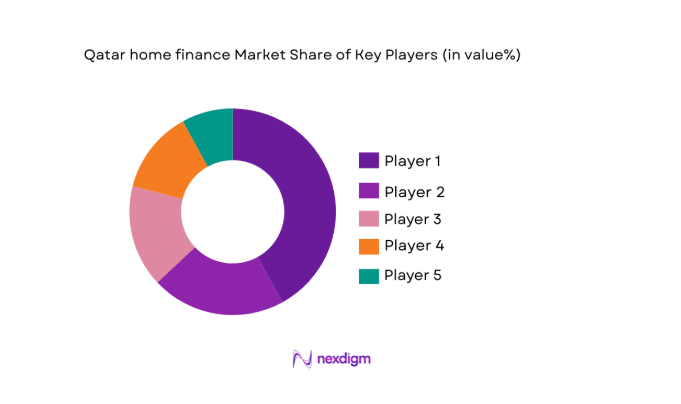

Qatar’s home finance market is moderately concentrated, with domestic banks and Islamic lenders controlling most mortgage assets under strong regulatory supervision and capital adequacy requirements. Government housing programs and payroll-linked financing arrangements favor established institutions with large balance sheets and employer relationships, reinforcing consolidation. International banks play limited roles in expatriate lending niches, while Islamic banks lead Sharia-compliant housing finance innovation and distribution reach.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Financing Model |

| Qatar National Bank | 1964 | Doha | ~ | ~ | ~ | ~ | ~ |

| Masraf Al Rayan | 2006 | Doha | ~ | ~ | ~ | ~ | ~ |

| Qatar Islamic Bank | 1982 | Doha | ~ | ~ | ~ | ~ | ~ |

| Commercial Bank of Qatar | 1974 | Doha | ~ | ~ | ~ | ~ | ~ |

| Doha Bank | 1979 | Doha | ~ | ~ | ~ | ~ | ~ |

Qatar home finance Market Analysis

Growth Drivers

Government-Backed Housing Allocation and Subsidized Mortgage Ecosystem

Qatar’s housing finance market expansion is structurally anchored in state-led residential allocation frameworks that provide land grants, subsidized financing, and bank-mediated mortgage channels for national households seeking homeownership within planned urban development zones. Government housing authorities coordinate directly with domestic banks to originate long-tenor financing linked to approved housing projects, ensuring predictable mortgage pipelines and credit risk mitigation through income-linked repayment structures. Subsidy programs covering profit rates or installment support reduce borrower cost burdens and expand eligibility among middle-income Qatari families transitioning from public housing waitlists to private ownership. Banks benefit from guaranteed borrower pools and collateralized residential assets within regulated loan-to-value caps, strengthening portfolio quality and capital efficiency under central bank oversight. Large-scale residential developments financed through public infrastructure spending create continuous demand for housing loans tied to approved master-planned communities near employment clusters. Policy alignment between urban planning, housing allocation, and banking credit provision integrates supply and financing channels, minimizing inventory risk and enabling synchronized property delivery with mortgage availability. Stable hydrocarbon revenues underpin fiscal capacity to sustain housing subsidies and public housing expansion, reinforcing long-term mortgage origination visibility for lenders. The institutionalized linkage between government housing policy and bank lending frameworks therefore establishes a structurally supported mortgage ecosystem that continuously drives home finance growth within Qatar’s regulated financial system.

Employer-Linked Expatriate Mortgage Demand within High-Income Workforce Segments

Qatar’s home finance market is significantly supported by expatriate professionals employed in government entities, energy companies, and multinational firms whose stable incomes and employer sponsorship enable access to residential financing through bank-approved payroll deduction mechanisms. Domestic banks maintain formal agreements with large employers to extend preferential mortgage terms to employees, including higher eligibility multiples and streamlined underwriting based on verified compensation structures and residency stability. Expatriate households with long-term employment contracts increasingly pursue property ownership within designated freehold zones, creating sustained demand for mortgage products tailored to non-national buyers. Financial institutions leverage employer data integration to reduce credit assessment uncertainty and automate repayment through salary assignment, lowering default risk and operational costs associated with retail lending. High-income expatriate segments in engineering, finance, healthcare, and management roles possess purchasing power aligned with premium residential developments, supporting mortgage volumes in urban housing markets. Developers actively market properties to expatriate buyers with bank financing partnerships embedded within sales processes, further expanding loan origination pipelines. Stable employment conditions in hydrocarbon-linked and government sectors provide predictable borrower repayment capacity, strengthening lender confidence in expatriate mortgage portfolios. This employer-integrated financing model therefore constitutes a structurally reliable demand channel sustaining home finance growth across Qatar’s urban residential markets.

Market Challenges

Regulatory Mortgage Caps and Borrower Eligibility Constraints

Qatar’s home finance market faces structural limitations from prudential regulations governing loan-to-value ratios, debt service thresholds, and borrower eligibility criteria designed to maintain banking stability and prevent housing market overheating. Central bank mortgage caps restrict maximum financing proportions relative to property value and borrower income, limiting leverage capacity particularly among expatriate households without government support programs. Strict documentation requirements for residency status, employment continuity, and income verification extend underwriting timelines and exclude borrowers with non-standard employment arrangements or variable compensation structures. Islamic financing contracts also require asset ownership and transfer compliance processes that increase transaction complexity relative to unsecured lending products. Banks must maintain conservative provisioning and capital allocation against long-tenor mortgage assets, constraining aggressive portfolio expansion compared with shorter-duration retail credit. Property valuation standards and approved project lists further narrow eligible housing inventory for financed purchases, particularly in emerging urban zones not yet recognized by regulators. Expatriate ownership restrictions outside designated areas limit geographic mortgage expansion opportunities for lenders targeting non-national borrowers. Compliance costs associated with mortgage monitoring, documentation retention, and regulatory reporting add operational burden that discourages smaller lenders from scaling housing finance portfolios. These regulatory and eligibility constraints collectively moderate mortgage penetration and restrict potential borrower pools within Qatar’s otherwise financially capable residential market.

Property Market Concentration and Limited Secondary Housing Supply

Qatar’s home finance market is challenged by concentration of residential property development within specific metropolitan zones and master-planned communities, resulting in constrained secondary housing supply available for mortgage-backed transactions. Much of the housing stock is delivered through large-scale new developments financed by developers or government programs, limiting resale market depth and price discovery necessary for mortgage refinancing and repeat transactions. Limited geographic diversity in freehold ownership zones for expatriates further concentrates financed property demand within select districts, increasing price levels and reducing affordability for middle-income buyers. Banks rely heavily on approved developer projects with established legal documentation and valuation certainty, restricting mortgage origination to primary market transactions rather than broader secondary housing circulation. Low turnover rates among national homeowners benefiting from subsidized housing allocations reduce availability of resale inventory eligible for conventional mortgages. Property liquidity constraints increase collateral risk perception among lenders, influencing conservative financing terms and higher equity requirements for borrowers. Absence of a deep secondary mortgage market or securitization framework limits portfolio recycling capacity for banks, reducing balance sheet flexibility to expand housing finance lending. Market transparency challenges in private property transactions also complicate valuation and risk assessment for lenders considering non-developer properties. This concentration of supply and limited resale ecosystem therefore constrains organic expansion of mortgage volumes beyond primary development cycles.

Opportunities

Digital Mortgage Processing and Automated Underwriting Integration

Qatar’s home finance market presents substantial opportunity for digitalization of mortgage origination and servicing through integrated platforms connecting banks, employers, government housing authorities, and property registries within secure electronic workflows. Automated income verification using employer payroll systems and national identity databases can significantly reduce documentation burdens and accelerate borrower approval timelines. Digital property valuation interfaces linked to approved development databases enable lenders to standardize collateral assessment and minimize manual appraisal delays. Online mortgage application portals tailored to both nationals and expatriates expand accessibility beyond branch-centric distribution, particularly among younger professional buyers accustomed to digital banking services. Integration of Sharia-compliant contract generation and documentation management within digital platforms simplifies Islamic financing execution and enhances operational efficiency for lenders. Electronic lien registration and property transfer coordination with land authorities can streamline post-approval processes and reduce administrative costs across the housing finance lifecycle. Data analytics applied to borrower profiles and repayment histories supports predictive credit risk modeling, enabling lenders to safely expand eligibility thresholds without compromising portfolio quality. Digital servicing channels including payment tracking and refinancing tools enhance borrower engagement and retention across loan tenors. Adoption of end-to-end digital mortgage ecosystems therefore represents a scalable pathway to increase origination volumes, reduce processing costs, and modernize Qatar’s housing finance infrastructure.

Expansion of Expatriate Ownership Zones and Mixed-Income Housing Development

Qatar’s home finance market holds strong growth potential through policy-driven expansion of expatriate property ownership eligibility and diversification of residential development beyond premium urban districts toward mixed-income housing communities. Allowing expatriates to purchase property in additional zones increases geographic mortgage demand and broadens borrower segments accessible to lenders. Development of mid-market residential projects aligned with expatriate income levels can stimulate mortgage uptake among professional households currently priced out of premium districts. Public-private partnerships in housing construction integrating infrastructure, utilities, and community services enhance attractiveness of new residential zones and support financed home purchases. Increased availability of resale properties within expanded ownership areas would deepen secondary housing markets, enabling refinancing and repeat mortgage transactions that strengthen loan portfolio turnover. Banks could develop tailored expatriate financing products with risk-based pricing calibrated to new housing segments, expanding market penetration while maintaining prudential safeguards. Diversification of housing supply across urban peripheries also reduces price concentration risks in central districts, improving affordability and mortgage accessibility. Infrastructure connectivity linking new residential developments to employment centers further supports borrower confidence in property investment and long-term occupancy. Expansion of ownership zones and housing typologies therefore offers a structural opportunity to scale Qatar’s home finance market across broader demographic and geographic segments.

Future Outlook

Qatar’s home finance market is expected to sustain stable expansion driven by continued government housing programs, urban development corridors, and high-income workforce housing demand. Digital mortgage processing and employer-integrated financing models will improve origination efficiency and borrower accessibility. Regulatory stability and banking liquidity derived from hydrocarbon revenues will support long-tenor lending capacity. Expansion of residential zones and diversified housing supply will gradually broaden mortgage penetration across national and expatriate segments.

Major Players

- Qatar National Bank

- Masraf Al Rayan

- Qatar Islamic Bank

- Commercial Bank of Qatar

- Doha Bank

- Ahli Bank

- International Bank of Qatar

- Barwa Bank

- Al Khaliji Bank

- Dukhan Bank

- HSBC Qatar

- Standard Chartered Qatar

- United Bank Limited Qatar

- Qatar Development Bank

- First Finance Company

Key Target Audience

- Investment and venture capitalist firms

- Government and regulatory bodies

- Domestic banks

- Islamic financial institutions

- Real estate developers

- Housing authorities

- Property investment firms

- Mortgage technology providers

Research Methodology

Step 1: Identification of Key Variables

Key market variables including mortgage outstanding volumes, housing supply pipelines, borrower segments, financing models, and regulatory constraints were identified through banking disclosures and housing policy documentation.

Macroeconomic drivers such as income levels, employment sectors, and urban development plans were mapped to assess demand-side dynamics.

Step 2: Market Analysis and Construction

Mortgage market structure was constructed using bank lending data, housing allocation frameworks, and property development distribution across urban zones. Segmentation by product type and platform was derived from financing models and origination channels observed across lenders and housing programs.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding borrower behavior, regulatory influence, and housing supply constraints were validated through financial sector reports and housing authority publications. Industry commentary and institutional lending practices were cross-checked to confirm structural drivers and challenges.

Step 4: Research Synthesis and Final Output

All validated inputs were synthesized into market structure, segmentation, and forward outlook aligned with policy and banking ecosystem dynamics. Findings were organized into standardized analytical sections to ensure consistency and comparability across housing finance markets.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising population and household formation increasing structural housing demand

Government housing initiatives and land allocation programs supporting ownership

Expansion of Islamic banking sector enabling Sharia compliant home finance growth

Urban residential development pipeline expanding mortgage eligible inventory

Stable income levels among public sector employees supporting borrowing capacity - Market Challenges

High property prices relative to median household income levels

Limited secondary mortgage market and refinancing liquidity depth

Concentration of lending among few major banks reducing competition

Expatriate eligibility restrictions constraining addressable borrower base

Interest rate sensitivity affecting affordability and loan uptake - Market Opportunities

Digital mortgage origination and approval process expansion

Affordable housing finance programs for middle income residents

Green and energy efficient housing finance products - Trends

Shift toward Islamic home finance structures among nationals

Integration of digital documentation and remote approvals

Developer bank co financing packages for new projects

Longer tenor mortgages improving affordability

Growth in refinancing and balance transfer activity - Government Regulations & Defense Policy

Qatar Central Bank mortgage lending caps and borrower eligibility rules

National housing program financing frameworks for citizens

Property ownership regulations for expatriates in designated zones - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type

Conventional fixed rate residential mortgages

Sharia compliant Ijara home financing

Murabaha property financing structures

Construction linked progressive home finance

Refinancing and equity release mortgages - By Platform Type

Bank branch originated housing finance

Digital mortgage application platforms

Broker and intermediary sourced loans

Developer tied financing programs

Employer linked housing finance schemes - By Fitment Type (In Value%)

Ready property purchase financing

Off plan property financing

Self construction home finance

Property transfer refinancing

Land purchase with construction finance - By End User Segment (In Value%)

Qatari national households

Expatriate salaried residents

High income professional buyers

Government sector employees

Real estate investors and landlords

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Financing Type, Borrower Eligibility, Profit Rate Structure, Loan Tenor, Down Payment Requirement, Digital Capability, Property Eligibility, Processing Time)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Qatar National Bank

Qatar Islamic Bank

Masraf Al Rayan

Dukhan Bank

Commercial Bank of Qatar

Doha Bank

Ahli Bank QPSC

International Bank of Qatar

Qatar Development Bank

HSBC Bank Middle East Qatar

Standard Chartered Bank Qatar

United Bank Limited Qatar

Alijarah Holding

First Finance Company

Barwa Bank

- Qatari nationals dominate demand due to state housing support and land grants

- Expatriate professionals drive urban apartment mortgage uptake in freehold zones

- Government employees show strongest credit eligibility and loan stability

- Investors utilize mortgage leverage for rental property acquisition

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now