Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Qatar last-mile delivery market generated approximately USD ~ billion in revenue, driven primarily by strong growth in e-commerce transactions, food delivery platforms, and rapid urban logistics networks. Increasing online retail adoption and mobile commerce platforms have significantly expanded parcel delivery volumes across the country. Logistics companies and digital platforms continue investing in delivery fleets, fulfillment hubs, and digital logistics systems to support rising consumer demand for faster delivery services.

Major urban centers including Doha, Al Rayyan, and Al Wakrah dominate last-mile delivery demand because these cities host the largest concentration of e-commerce customers, retail stores, and food delivery platforms. Doha operates as the primary logistics hub where courier companies, distribution centers, and delivery startups manage regional delivery networks. The presence of modern infrastructure, high smartphone penetration, and dense urban populations encourages rapid delivery adoption, allowing logistics providers to operate highly efficient last-mile delivery services across metropolitan zones.

Market Segmentation

By Service Type

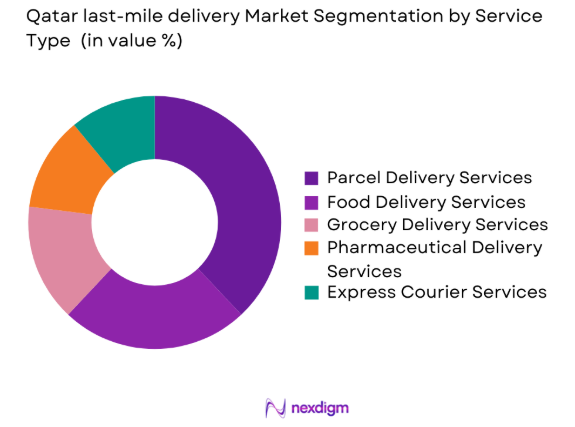

Qatar Last-Mile Delivery market is segmented by product type into parcel delivery services, food delivery services, grocery delivery services, pharmaceutical delivery services, and express courier services. Recently, parcel delivery services have a dominant market share due to strong growth in e-commerce retail platforms and the increasing number of online shoppers purchasing electronics, fashion products, and consumer goods. Online marketplaces and retail platforms rely heavily on courier networks for direct-to-consumer parcel deliveries across urban areas. Major logistics providers operate dedicated parcel distribution hubs and vehicle fleets designed for rapid parcel handling and door-to-door distribution. The continuous expansion of online retail platforms and international e-commerce sellers shipping products to consumers has further increased parcel delivery demand. Courier companies continue investing in automated parcel sorting systems, warehouse facilities, and digital logistics platforms to improve delivery efficiency and handle growing parcel volumes.

By Delivery Mode

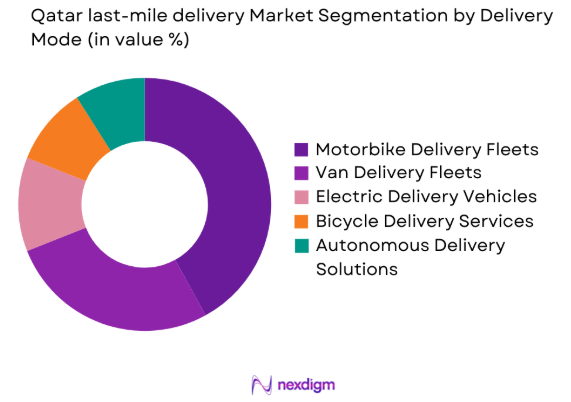

Qatar Last-Mile Delivery market is segmented by platform type into motorbike delivery fleets, van delivery fleets, electric delivery vehicles, bicycle delivery services, and autonomous delivery solutions. Recently, motorbike delivery fleets have a dominant market share due to their ability to navigate dense urban streets and deliver packages quickly across congested city areas. Motorbike fleets are widely used by food delivery platforms and courier companies because they offer faster transportation and lower operational costs compared with larger vehicles. Logistics providers operate extensive motorbike fleets to support rapid deliveries across Doha and surrounding urban districts. The flexibility of two-wheel vehicles allows drivers to reach residential areas, commercial buildings, and apartment complexes more efficiently than larger vans. Increasing demand for same day delivery services and instant food delivery continues to expand the use of motorbike delivery networks across Qatar.

Competitive Landscape

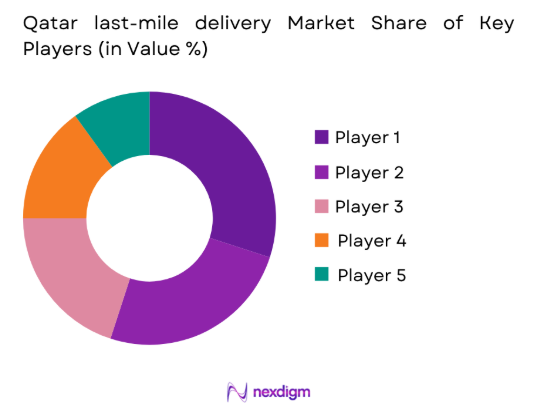

The Qatar last-mile delivery market features a competitive ecosystem composed of international logistics companies, regional courier operators, and technology driven delivery startups. Global firms such as DHL, UPS, and FedEx maintain strong operational networks supported by advanced logistics infrastructure and international shipping capabilities. Regional companies including Aramex and Agility Logistics leverage strong distribution networks and partnerships with e-commerce retailers. Local digital delivery platforms such as Snoonu and Talabat continue expanding rapidly by integrating mobile ordering platforms with dedicated delivery fleets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Capacity |

| Aramex | 1982 | Dubai | Logistics Technology | Global | Courier Services | USD 1.6B | 10,000 Vehicles |

| DHL eCommerce | 1969 | Bonn | Logistics Automation | Global | Parcel Logistics | USD 94B | 30,000 Vehicles |

| Qatar Post | 1950 | Doha | Postal Logistics Systems | National | Postal and Parcel Delivery | USD 150M | 1,200 Vehicles |

| FedEx Logistics | 1971 | Memphis | Digital Logistics Systems | Global | Courier and Freight | USD 90B | 40,000 Vehicles |

| Agility Logistics | 1979 | Kuwait | Supply Chain Platforms | International | Logistics Services | USD 5B | 8,000 Vehicles |

Qatar last-mile delivery Market Analysis

Growth Drivers

Rapid Expansion of E-commerce and Digital Retail Platforms

The rapid expansion of e-commerce platforms across Qatar significantly increases demand for last-mile delivery services as consumers purchase products through digital marketplaces and mobile commerce applications. Online retail platforms provide access to electronics, fashion, groceries, and household goods through convenient ordering systems. Rising parcel volumes require efficient logistics networks capable of delivering goods quickly across urban areas. Retail companies increasingly partner with logistics providers specializing in last-mile distribution to meet strict delivery timelines. Digital payment adoption further strengthens online purchasing by enabling secure transactions and frequent mobile orders. Logistics firms expand delivery fleets and deploy route optimization technologies to improve operational efficiency. Automated dispatch platforms and real-time tracking systems enhance delivery transparency while helping companies manage growing parcel volumes.

Growing Demand for On-Demand Food and Grocery Delivery Services

The rapid rise of on-demand food delivery platforms and online grocery ordering services accelerates demand for last-mile logistics infrastructure across Qatar’s urban areas. Consumers increasingly order meals, groceries, and essential goods through mobile applications that provide convenient home and workplace delivery. Restaurants, supermarkets, and convenience stores depend on delivery platforms capable of ensuring fast order fulfillment throughout the day. Digital delivery platforms use advanced dispatch systems that assign riders in real time and optimize routes to reduce travel time. This efficiency enables businesses to reach more customers without expanding physical stores. Logistics providers invest in specialized delivery vehicles and insulated containers to maintain food quality during transport. Expanding app coverage increases daily delivery volumes across cities.

Market Challenges

High Operational Costs for Delivery Fleet Management

Logistics providers operating within the Qatar Last-Mile Delivery Market face substantial operational costs related to fleet maintenance, driver management, and digital logistics systems needed for efficient parcel distribution. Vehicle acquisition, fuel expenses, insurance, and regular maintenance significantly increase financial pressure on logistics operators. Companies also invest in dispatch software, real-time tracking platforms, and warehouse management technologies to maintain service efficiency and customer satisfaction. These systems require frequent upgrades and integration with e-commerce platforms, raising operational expenditure. Labor costs remain high as companies recruit drivers and delivery riders to handle growing order volumes. Promotional pricing strategies used to attract retailers further reduce margins, increasing financial pressure on logistics providers.

Urban Traffic Congestion Affecting Delivery Efficiency

Urban traffic congestion in densely populated areas of Doha creates operational challenges for logistics providers delivering parcels across the Qatar Last-Mile Delivery Market. Delivery vehicles frequently encounter heavy traffic during peak commuting hours, delaying shipments and increasing delivery times. These delays reduce efficiency and raise fuel consumption as drivers spend longer navigating busy urban roads. Logistics companies must carefully plan delivery schedules and optimize routing strategies to maintain service reliability. Rapid urban expansion and rising vehicle ownership continue intensifying congestion across metropolitan areas. Infrastructure improvements and new road networks reduce traffic in some districts, yet congestion remains a key operational constraint. Logistics firms increasingly use route optimization technologies and dynamic dispatch systems to manage traffic conditions.

Opportunities

Expansion of Smart Locker Networks and Automated Parcel Pickup Infrastructure

Growing demand for flexible delivery solutions in Qatar creates opportunities for logistics companies to deploy automated parcel locker networks across urban locations. These lockers allow consumers to collect parcels from secure self-service stations placed in shopping malls, residential complexes, and transportation hubs. Smart lockers operate through digital authentication systems that enable parcel retrieval using secure mobile codes. Logistics providers reduce delivery costs because multiple parcels can be delivered to one locker point rather than individual addresses. This consolidation improves operational efficiency and lowers fleet travel distances in congested areas. Retailers benefit from flexible pickup schedules that enhance customer convenience and reduce missed deliveries. Smart city initiatives further encourage deployment of automated parcel infrastructure.

Adoption of Electric Delivery Vehicles and Sustainable Logistics Infrastructure

Environmental sustainability initiatives in Qatar create opportunities for logistics companies to adopt electric delivery vehicles and low-emission transportation technologies within the Qatar Last-Mile Delivery Market. Government environmental policies encourage businesses to reduce carbon emissions and transition toward sustainable transport systems supporting national sustainability goals. Electric delivery vehicles help logistics providers lower fuel expenses and reduce environmental impact associated with conventional fleets. Improvements in battery performance and expanding charging infrastructure make electric fleets more practical for urban parcel distribution. Logistics companies adopting sustainable vehicles also strengthen brand reputation among environmentally conscious consumers. Retailers increasingly partner with logistics providers offering green delivery services, creating competitive advantages for operators investing in electric vehicle fleets.

Future Outlook

The Qatar last-mile delivery market is expected to expand steadily as e-commerce platforms, food delivery services, and retail logistics networks continue to grow across the country. Increasing digital commerce activity and mobile ordering platforms will continue driving parcel delivery volumes across urban regions. Logistics companies are expected to invest further in automation technologies, electric vehicle fleets, and smart route optimization platforms to improve operational efficiency. Government support for digital trade and logistics infrastructure development will further strengthen the national delivery ecosystem.

Major Players

- Aramex

- DHL eCommerce

- Qatar Post

- Fetchr

- iMileDelivery

- J&T Express

- SMSA Express

- UPS Supply Chain Solutions

- FedEx Logistics

- Careem

- Talabat

- Snoonu

- Gulf Warehousing Company

- Agility Logistics

- Qatar Logistics

Key Target Audience

- E-commerce retail companies

- Food delivery platform operators

- Logistics and courier companies

- Retail supermarket chains

- Pharmaceutical distribution companies

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying key variables affecting the Qatar last-mile delivery market including delivery demand patterns, e-commerce shipment volumes, urban logistics infrastructure, fleet capacity, and regulatory frameworks governing logistics operations.

Step 2: Market Analysis and Construction

Researchers construct the market model using secondary data from government logistics statistics, transportation reports, and industry databases. Market segmentation is developed by analyzing logistics service types, delivery platforms, and operational delivery models.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, supply chain managers, and technology providers validate the assumptions regarding delivery demand, fleet expansion, and logistics technology adoption trends across the market.

Step 4: Research Synthesis and Final Output

Validated insights are synthesized into a structured market report that includes market sizing, segmentation analysis, competitive benchmarking, and long-term industry outlook for the Qatar last-mile delivery ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid Expansion of E-commerce Retail Platforms

Growth in On-Demand Food Delivery Services

Urban Infrastructure Supporting Quick Delivery Networks - Market Challenges

High Operational Costs in Urban Delivery Networks

Traffic Congestion and Delivery Time Constraints

Workforce Availability and Driver Retention Issues - Market Opportunities

Expansion of Same Day and Instant Delivery Services

Adoption of Smart Logistics Technologies

Growth of Cross Border E-commerce Fulfillment - Trends

Integration of AI Driven Route Optimization

Increasing Adoption of Micro Fulfillment Centers

Expansion of Electric Delivery Vehicle Fleets - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Food and Grocery Delivery

E-commerce Courier Delivery

Pharmaceutical Delivery Services

Same Day Express Delivery - By Platform Type (In Value%)

Mobile Application Platforms

Web Based Ordering Platforms

Integrated Retail Logistics Platforms

Marketplace Delivery Platforms

Enterprise Delivery Management Platforms - By Fitment Type (In Value%)

In-House Delivery Networks

Third Party Logistics Services

Crowdsourced Delivery Networks

Hybrid Logistics Models

Dedicated Fleet Operations - By End User Segment (In Value%)

E-commerce Retailers

Food and Beverage Platforms

Healthcare and Pharmacy Chains

Retail Supermarkets and Hypermarkets

Electronics and Consumer Goods Retailers - By Procurement Channel (In Value%)

Direct Corporate Contracts

Online Delivery Aggregators

Retail Logistics Partnerships

Government and Institutional Contracts

Third Party Logistics Providers

- Market Share Analysis

- Cross Comparison Parameters (Delivery Fleet Size, Technology Integration, Service Coverage Area, Same Day Delivery Capability, Strategic Partnerships, Delivery Speed Performance, Warehouse and Fulfillment Infrastructure, Route Optimization Systems, E-commerce Platform Integration, Reverse Logistics Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Aramex

DHL eCommerce

Qatar Post

Fetchr

iMile Delivery

J&T Express

SMSA Express

UPS Supply Chain Solutions

FedEx Logistics

Careem

Talabat

Snoonu

Gulf Warehousing Company

Agility Logistics

Qatar Logistics

- Growing reliance of e-commerce retailers on specialized delivery services

- Food delivery platforms increasing demand for rapid logistics networks

- Healthcare pharmacies expanding prescription home delivery services

- Retail supermarkets integrating delivery into omnichannel retail models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now