Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Qatar Semiconductor Manufacturing Market reached approximately USD ~ billion based on a recent historical assessment, reflecting the country’s early stage semiconductor manufacturing ecosystem supported by advanced electronics demand and strategic industrial diversification initiatives. Market growth is primarily driven by increasing adoption of semiconductor components across telecommunications infrastructure, consumer electronics, data center equipment, and emerging artificial intelligence computing platforms. National innovation programs, government funded technology infrastructure development, and partnerships with global semiconductor technology firms also contribute to expanding domestic semiconductor manufacturing capabilities.

Doha remains the central hub for semiconductor related industrial activity due to the presence of advanced technology zones, research facilities, and digital infrastructure investments supporting electronics manufacturing and semiconductor design development. The broader Gulf region including the United Arab Emirates and Saudi Arabia also influences regional semiconductor supply chains through technology investments and electronics manufacturing expansion. Qatar benefits from strong financial capacity, strategic technology investments, and industrial diversification policies that encourage development of advanced manufacturing industries including semiconductor fabrication, packaging, and integrated circuit design ecosystems.

Market Segmentation

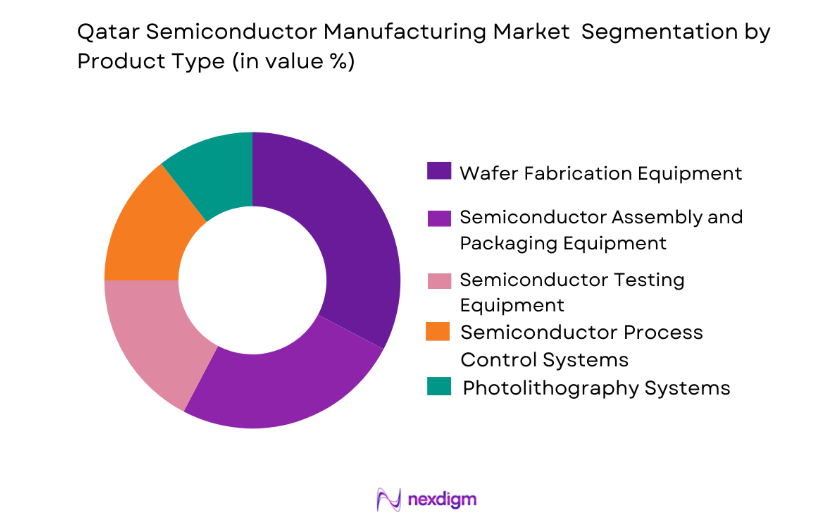

By Product Type

Qatar Semiconductor Manufacturing Market is segmented by product type into wafer fabrication equipment, semiconductor assembly and packaging equipment, semiconductor testing equipment, semiconductor process control systems, and photolithography systems. Recently, wafer fabrication equipment has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Semiconductor fabrication facilities require advanced wafer processing systems capable of performing photolithography, deposition, etching, and chemical mechanical polishing processes across integrated circuit production lines. Growing regional demand for microprocessors, memory chips, and power semiconductors further increases reliance on sophisticated wafer manufacturing platforms capable of producing high precision semiconductor devices. Large scale semiconductor fabrication facilities invest heavily in advanced lithography tools, wafer processing systems, and process control technologies to maintain consistent production quality across complex semiconductor manufacturing processes. As semiconductor devices become increasingly sophisticated with smaller node architectures and higher transistor density, wafer fabrication equipment continues to dominate capital expenditure investments within semiconductor manufacturing ecosystems.

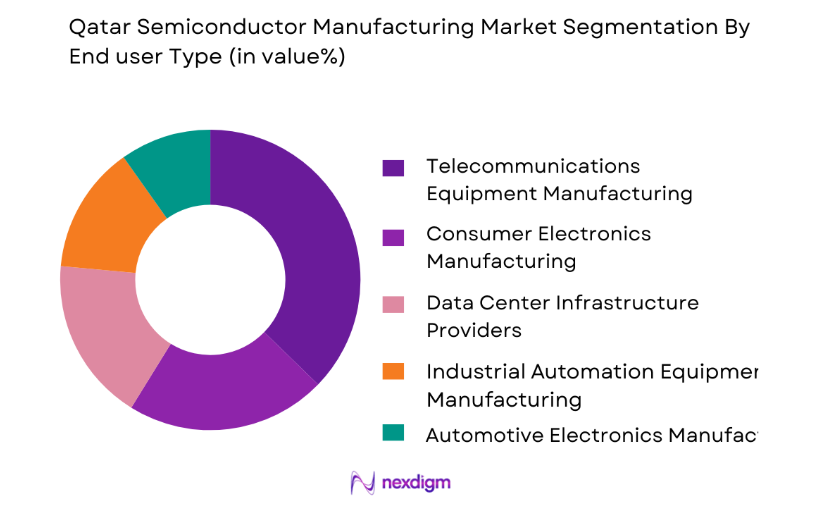

By End User Industry

Qatar Semiconductor Manufacturing Market is segmented by end user industry into consumer electronics manufacturing, telecommunications equipment manufacturing, automotive electronics manufacturing, industrial automation equipment manufacturing, and data center infrastructure providers. Recently, telecommunications equipment manufacturing has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Telecommunications infrastructure requires advanced semiconductor chips for network switching systems, fiber optic communication equipment, base station controllers, and 5G wireless communication modules supporting high speed digital connectivity networks. Qatar’s rapid digital infrastructure development including smart city initiatives, advanced telecommunications networks, and expanding digital services significantly increases semiconductor demand across communication equipment manufacturing industries. Semiconductor components used in network processors, signal amplifiers, and radio frequency integrated circuits play a critical role in enabling modern telecommunications systems. As digital connectivity infrastructure continues expanding throughout the Middle East region, telecommunications equipment manufacturing remains the dominant end user segment driving semiconductor manufacturing demand.

Competitive Landscape

The Qatar Semiconductor Manufacturing Market remains moderately concentrated with global semiconductor equipment manufacturers and technology providers playing a dominant role in shaping regional market development. Leading multinational semiconductor companies influence technology adoption, supply chain development, and production capabilities through partnerships, technology licensing agreements, and equipment supply contracts. Semiconductor manufacturing equipment providers maintain strong competitive positions due to their specialized technological capabilities and advanced manufacturing systems required for integrated circuit production.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Semiconductor Node Capability |

| Intel Corporation | 1968 | United States | ~ | ~ | ~ | ~ | ~ |

| Taiwan Semiconductor Manufacturing Company | 1987 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics Semiconductor Division | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| GlobalFoundries | 2009 | United States | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ |

Qatar Semiconductor Manufacturing Market Analysis

Growth Drivers

Expansion of National Digital Infrastructure and Telecommunications Systems:

Qatar’s rapid expansion of advanced digital infrastructure significantly accelerates demand for semiconductor manufacturing technologies across the country’s electronics and telecommunications ecosystem. National investments in high capacity fiber optic networks, cloud computing infrastructure, artificial intelligence platforms, and next generation mobile communication networks require sophisticated semiconductor components supporting digital processing capabilities. Telecommunications operators deploy semiconductor intensive networking equipment including base stations, network switches, routers, and signal processing hardware enabling high speed digital connectivity across urban and industrial environments. Semiconductor chips used within network processors, communication modules, and radio frequency integrated circuits play an essential role in enabling efficient transmission of large scale data traffic across digital communication networks. As Qatar continues expanding its digital services ecosystem including smart government services, digital banking platforms, and advanced data center infrastructure, semiconductor demand correspondingly increases across the entire technology value chain. Semiconductor manufacturing capabilities therefore become strategically important for ensuring stable supply chains supporting the country’s digital transformation programs. Government supported innovation initiatives encourage technology companies to develop advanced computing infrastructure capable of supporting artificial intelligence analytics and large scale data processing systems. These computing platforms require powerful processors, graphics processing units, and specialized semiconductor accelerators capable of handling complex computational workloads efficiently. As digital technologies become increasingly embedded across financial services, transportation systems, healthcare platforms, and industrial operations, semiconductor manufacturing demand continues expanding across Qatar’s technology ecosystem.

Economic Diversification Strategies Supporting Advanced Manufacturing Development

Qatar’s long term economic diversification strategies significantly promote development of high technology industries including semiconductor manufacturing, electronics production, and advanced digital infrastructure ecosystems. National economic development programs encourage investments in technology manufacturing sectors capable of reducing economic dependence on hydrocarbon revenues while creating new knowledge intensive industrial capabilities. Government authorities actively promote technology driven industrial diversification by supporting innovation hubs, technology parks, and research facilities capable of attracting global semiconductor companies and technology developers. Strategic partnerships between international semiconductor equipment manufacturers and local industrial development agencies enable technology transfer and knowledge sharing necessary for building domestic semiconductor production capabilities. Qatar’s strong financial resources allow large scale investments in research infrastructure, semiconductor design laboratories, and advanced manufacturing facilities supporting emerging electronics industries. These investments create opportunities for establishing semiconductor packaging, testing, and specialized chip manufacturing facilities serving regional technology markets. As Middle Eastern economies increasingly adopt advanced digital technologies including artificial intelligence systems, autonomous mobility solutions, and smart infrastructure networks, semiconductor demand across the region continues expanding rapidly. Qatar aims to position itself as a regional technology innovation hub capable of supporting semiconductor related research, development, and manufacturing activities. Long term industrial development strategies therefore prioritize advanced manufacturing sectors including semiconductor fabrication, electronics assembly, and integrated circuit design ecosystems supporting future economic diversification goals.

Market Challenges

Extremely High Capital Investment Requirements for Semiconductor Fabrication Facilities:

Semiconductor manufacturing remains one of the most capital intensive industrial sectors globally, creating substantial financial barriers for emerging semiconductor ecosystems such as Qatar. Establishing advanced semiconductor fabrication plants requires investments that frequently exceed several billion dollars due to the complexity of manufacturing equipment, ultra clean production facilities, and specialized process technologies necessary for integrated circuit production. Semiconductor fabrication equipment including photolithography systems, deposition tools, etching systems, and wafer inspection equipment represent highly specialized technologies developed by a limited number of global suppliers. These equipment platforms require precise engineering, continuous maintenance, and highly skilled technical personnel capable of operating sophisticated semiconductor manufacturing processes. Countries seeking to establish semiconductor fabrication facilities must also invest heavily in supporting infrastructure including ultra pure water systems, stable electricity supply networks, advanced chemical processing facilities, and controlled environment cleanrooms. Such infrastructure significantly increases total capital requirements for semiconductor manufacturing projects. In addition to facility construction costs, semiconductor manufacturers must continuously upgrade equipment and production technologies to remain competitive with rapidly advancing chip manufacturing processes. Semiconductor node technologies evolve rapidly, requiring periodic equipment upgrades to support smaller transistor architectures and higher performance semiconductor devices. For emerging semiconductor manufacturing regions like Qatar, the scale of financial investment required to establish globally competitive semiconductor fabrication capabilities presents a significant challenge limiting rapid industry development.

Global Semiconductor Supply Chain Dependence and Technology Access Constraints

Semiconductor manufacturing relies on extremely complex global supply chains involving specialized equipment suppliers, advanced materials manufacturers, semiconductor design companies, and technology licensing partnerships. Countries attempting to establish domestic semiconductor manufacturing capabilities often face challenges accessing critical technologies, manufacturing equipment, and intellectual property necessary for producing advanced semiconductor devices. Leading semiconductor manufacturing equipment suppliers operate within tightly integrated global technology ecosystems dominated by a small number of companies capable of producing advanced lithography systems and precision wafer processing equipment. Access to these technologies frequently requires strategic partnerships, long term supply agreements, and compliance with international technology export regulations. Semiconductor manufacturing also depends heavily on specialized materials including high purity silicon wafers, photoresists, specialty gases, and chemical compounds used throughout semiconductor fabrication processes. These materials are produced by highly specialized global suppliers located primarily in established semiconductor manufacturing regions. For emerging semiconductor ecosystems such as Qatar, developing reliable supply chains for advanced semiconductor materials and manufacturing equipment presents logistical and strategic challenges. Technology transfer limitations and intellectual property restrictions can further constrain access to cutting edge semiconductor manufacturing technologies. Building a complete semiconductor manufacturing ecosystem therefore requires coordinated development of supply chains, research capabilities, and technology partnerships capable of supporting complex semiconductor production operations.

Opportunities

Development of Regional Semiconductor Packaging and Testing Ecosystems

Semiconductor packaging and testing services represent a strategic entry point for emerging semiconductor manufacturing ecosystems seeking to participate in the global semiconductor value chain without immediately constructing full scale wafer fabrication plants. Advanced semiconductor packaging facilities perform critical functions including chip assembly, encapsulation, electrical testing, and reliability verification processes required before semiconductor devices are integrated into electronic products. These operations require significantly lower capital investment compared to advanced wafer fabrication facilities while still enabling participation in high value semiconductor manufacturing activities. Qatar’s strong financial resources and technology investment capabilities create opportunities for establishing specialized semiconductor packaging and testing centers serving regional electronics manufacturers and technology companies. As global semiconductor supply chains diversify geographically to improve resilience against disruptions, new semiconductor packaging hubs are emerging across multiple regions. Semiconductor manufacturers increasingly outsource packaging and testing services to specialized providers capable of delivering high quality assembly operations efficiently. Qatar could position itself as a regional semiconductor packaging hub supporting electronics manufacturing across the Middle East, North Africa, and South Asia regions. Establishing such facilities would also help develop domestic semiconductor engineering expertise, workforce capabilities, and industrial infrastructure supporting future expansion into additional semiconductor manufacturing activities.

Strategic Partnerships with Global Semiconductor Technology Companies

International partnerships between emerging semiconductor ecosystems and established global semiconductor manufacturers present significant opportunities for technology transfer, industrial development, and supply chain integration. Global semiconductor companies continuously seek new locations for research collaboration, advanced manufacturing support services, and regional technology partnerships capable of expanding their global operational networks. Qatar’s strong investment capabilities and strategic geographic location create favorable conditions for attracting global semiconductor companies interested in establishing regional research centers, semiconductor design facilities, or advanced packaging operations. Technology partnerships enable local engineers and technical professionals to gain expertise in semiconductor manufacturing processes, chip design methodologies, and advanced production technologies through collaborative development programs. Such partnerships often involve joint research initiatives, technology licensing agreements, and collaborative manufacturing projects capable of accelerating semiconductor ecosystem development. By establishing long term strategic alliances with global semiconductor leaders, Qatar could gain access to advanced manufacturing knowledge, specialized semiconductor technologies, and global supply chain networks. These collaborations would support development of a domestic semiconductor industry while simultaneously strengthening the country’s broader technology innovation ecosystem across multiple advanced manufacturing sectors.

Future Outlook

The Qatar Semiconductor Manufacturing Market is expected to expand steadily as the country strengthens its digital infrastructure and technology manufacturing capabilities. Continued government investments in innovation ecosystems, data centers, artificial intelligence computing, and smart infrastructure will increase semiconductor demand across multiple industries. Partnerships with global semiconductor equipment providers and technology firms will further accelerate knowledge transfer and industrial capability development. Over the next five years, the market is likely to see growth in semiconductor packaging, testing, and design activities supported by regional technology investments.

Major Players

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company

- Samsung Electronics Semiconductor Division

- GlobalFoundries

- Texas Instruments

- STMicroelectronics

- Micron Technology

- Infineon Technologies

- NXP Semiconductors

- ON Semiconductor

- Applied Materials

- Lam Research

- ASML Holding

- Tokyo Electron

- KLA Corporation

Key Target Audience

- Semiconductor Manufacturing Companies

- Consumer Electronics Manufacturers

- Telecommunications Infrastructure Providers

- Automotive Electronics Manufacturers

- Data Center Infrastructure Operators

- Industrial Automation Equipment Manufacturers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

Initial research focuses on identifying key variables influencing semiconductor manufacturing demand including electronics production, telecommunications infrastructure development, and advanced computing technology adoption. Market drivers, technology trends, and policy initiatives influencing semiconductor manufacturing ecosystems are analyzed.

Step 2: Market Analysis and Construction

Secondary research sources including industry reports, government publications, semiconductor industry databases, and financial disclosures are analyzed to estimate market size and structure. Market segmentation is constructed based on product categories, manufacturing technologies, and end user demand patterns.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including semiconductor engineers, manufacturing specialists, and technology analysts are consulted to validate research findings and confirm market assumptions. Expert insights help refine demand forecasts and validate the competitive landscape across semiconductor manufacturing sectors.

Step 4: Research Synthesis and Final Output

All research insights are synthesized into a structured market analysis combining quantitative market sizing with qualitative industry insights. Final outputs integrate technological trends, investment patterns, and policy developments shaping the future of semiconductor manufacturing in Qatar.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Electronics Manufacturing and Digital Infrastructure

Government Initiatives to Diversify Economy Beyond Hydrocarbons

Growing Demand for Advanced Chips in Telecommunications and AI Systems - Market Challenges

High Capital Investment Requirements for Semiconductor Fabrication Facilities

Limited Domestic Semiconductor Manufacturing Expertise

Complex Supply Chain Dependencies for Semiconductor Equipment - Market Opportunities

Development of Strategic Partnerships with Global Semiconductor Companies

Investment in Advanced Packaging and Semiconductor Testing Facilities

Expansion of Regional Semiconductor Supply Chains in the Middle East - Trends

Adoption of Advanced Node Semiconductor Manufacturing Technologies

Increasing Focus on Semiconductor Design and Packaging Ecosystems

Integration of Artificial Intelligence in Semiconductor Production Processes - Government Regulations

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Equipment

Semiconductor Assembly and Packaging Systems

Semiconductor Testing Equipment

Semiconductor Process Control Systems

Photolithography Systems - By Platform Type (In Value%)

Logic Semiconductor Manufacturing

Memory Semiconductor Manufacturing

Power Semiconductor Manufacturing

Analog Semiconductor Manufacturing

Mixed Signal Semiconductor Manufacturing - By Fitment Type (In Value%)

New Semiconductor Fabrication Facilities

Upgradation of Existing Fabrication Lines

Integrated Semiconductor Production Systems

Modular Semiconductor Production Units

Contract Manufacturing Semiconductor Facilities - By EndUser Segment (In Value%)

Consumer Electronics Manufacturers

Automotive Electronics Manufacturers

Telecommunications Equipment Producers

- Market Share Analysis

- Cross Comparison Parameters (Technology Node Capability, Manufacturing Capacity, Packaging Technology, Strategic Partnerships, Production Automation)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Intel Corporation

Taiwan Semiconductor Manufacturing Company

Samsung Electronics Semiconductor Division

GlobalFoundries

Texas Instruments

STMicroelectronics

Micron Technology

Infineon Technologies

NXP Semiconductors

ON Semiconductor

Applied Materials

Lam Research

ASML Holding

Tokyo Electron

KLA Corporation

- Electronics Manufacturers Increasingly Seek Regional Semiconductor Supply

- Security Telecommunications Equipment Providers Require Advanced Chips for 5G Infrastructure

- Automotive Electronics Manufacturers Expand Semiconductor Demand for Electric Vehicles

- Data Center Infrastructure Growth Drives Demand for High Performance Processors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now