Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The market size for the Qatar Wind Energy sector is projected to reach USD ~ billion, driven by the country’s strategic push towards renewable energy sources as part of its Vision 2030 plan. This growth is primarily fueled by governmental initiatives aimed at diversifying the energy mix, reducing dependence on fossil fuels, and achieving sustainability goals. As part of this strategy, large investments are being directed into both onshore and offshore wind energy projects, further accelerated by global technological advancements in wind turbine systems.

Key cities like Doha and Al Khobar are at the forefront of wind energy projects due to their favorable geographic conditions and proximity to national infrastructure. Qatar’s National Vision 2030 further ensures continued dominance of the country in the wind energy space by providing a robust regulatory framework and funding mechanisms to encourage private sector involvement. Furthermore, Qatar’s government is committed to leveraging its position as a regional energy leader to foster growth in wind energy and meet its climate goals.

Market Segmentation

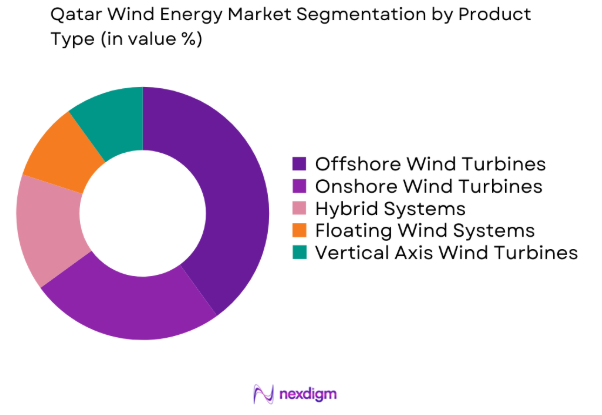

By Product Type

The Qatar Wind Energy market is segmented by product type into offshore wind turbines, onshore wind turbines, hybrid systems, floating wind systems, and vertical axis wind turbines. Offshore wind turbines currently lead the market due to their higher energy efficiency and capability to harness stronger and more consistent wind patterns. Qatar’s geographical conditions, particularly along its coastlines, present a significant opportunity for offshore wind farms, further driving this sub-segment’s dominance. With continued technological advancements and favorable government policies, offshore wind turbines are expected to maintain a dominant market position.

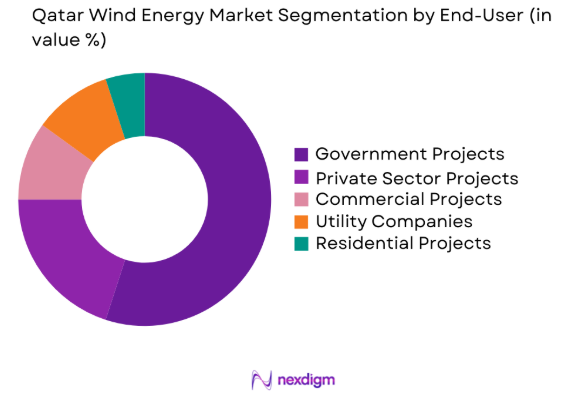

By End User Segment

The Qatar Wind Energy market is segmented by end-user into government projects, private sector projects, commercial projects, utility companies, and residential projects. Government projects hold the largest share due to Qatar’s robust support for large-scale renewable energy initiatives, including the National Renewable Energy Strategy. These projects are designed to achieve national energy security, reduce emissions, and diversify the energy mix. With strong financial backing and regulatory support, government projects are set to dominate, attracting further investments from both local and international players.

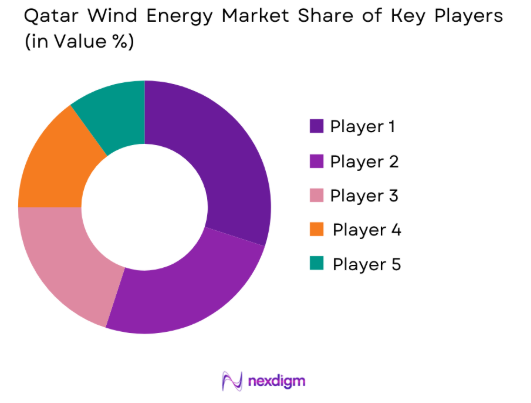

Competitive Landscape

The competitive landscape in Qatar’s wind energy market is shaped by global industry leaders who are establishing a strong presence in the region. Key players such as Siemens Gamesa, Vestas, and GE Renewable Energy have dominated the market, bringing their cutting-edge wind turbine technologies to Qatar. These companies benefit from Qatar’s favorable investment climate and government policies aimed at renewable energy development. The market is also marked by increasing collaborations between international and local firms, enabling efficient project execution and technology transfer.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Siemens Gamesa | 1976 | Spain | ~ | ~ | ~ | ~ | ~ |

| Vestas Wind Systems | 1945 | Denmark | ~ | ~ | ~ | ~ | ~ |

| GE Renewable Energy | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| Nordex | 1985 | Germany | ~ | ~ | ~ | ~ | ~ |

| Acciona Energia | 1985 | Spain | ~ | ~ | ~ | ~ | ~ |

Qatar Wind Energy Market Analysis

Growth Drivers

Government Support for Renewable Energy

Qatar’s commitment to renewable energy is a major driver of growth in its wind energy market. The country’s National Vision 2030 outlines ambitious sustainability goals, including reducing carbon emissions. To achieve these objectives, Qatar has made significant investments in wind energy, focusing not only on large-scale wind farms but also on advancing wind technologies through research and development. The government supports this growth with subsidies and incentives, further fostering a favorable environment for the wind energy sector. These efforts are attracting both local and international companies, positioning the market for continued expansion and technological innovation as Qatar works to diversify its energy sources and meet its sustainability targets.

Technological Advancements in Wind Turbine Efficiency

The growing efficiency of wind turbines, especially offshore turbines, is a key driver of market growth. Technological advancements, such as larger turbine blades, enhanced capacity factors, and improved materials, have lowered the cost per unit of energy generated. Innovations in turbine design enable better performance under diverse environmental conditions, further boosting their effectiveness. These improvements make wind energy increasingly competitive with traditional energy sources, positioning it as a cost-effective alternative. As a result, the efficiency gains in wind turbine technology are accelerating the adoption of wind energy in Qatar’s market, contributing to its broader integration into the country’s energy strategy and sustainable development goals.

Market Challenges

High Capital Investment

The high capital required for wind energy infrastructure is a major challenge in Qatar. While operational costs are relatively low once turbines are installed, the initial investment for land acquisition, wind farm construction, and turbine installation can be substantial. Offshore wind projects, in particular, demand more advanced infrastructure and technology, further increasing costs. Despite the long-term savings wind energy offers, the high upfront costs often discourage private sector investment. Additionally, limited financing options, particularly in rural and remote areas of Qatar, make it difficult for projects to secure the necessary capital. These financial barriers hinder the rapid expansion of wind energy in the country.

Grid Integration and Intermittency Issues

A major challenge for wind energy in Qatar is the intermittency of wind power generation. Unlike conventional energy sources, wind energy depends heavily on weather conditions, with variations in wind speed leading to periods of low or no energy production. This variability makes it difficult to integrate wind energy into Qatar’s national grid. To address this, the power grid requires substantial upgrades to accommodate renewable energy fluctuations. Investments in energy storage systems and advanced grid management solutions are essential to ensure a consistent and reliable power supply. Without these upgrades, the integration of wind energy into the grid may remain a significant hurdle for the country’s energy transition.

Opportunities

Expansion of Offshore Wind Projects

One of the most significant opportunities in the Qatar wind energy market is the expansion of offshore wind projects. Offshore wind farms have the potential to generate large amounts of energy due to stronger and more consistent wind patterns at sea. The Qatari government has already begun to explore offshore wind farms, with several projects under development. This segment offers high growth potential, as the government continues to prioritize renewable energy solutions and seeks to meet its ambitious sustainability targets. The development of offshore wind farms would significantly contribute to Qatar’s renewable energy capacity and play a central role in its energy transition.

International Collaboration and Investment

As Qatar advances its renewable energy goals, there is significant opportunity for international companies to partner with local entities in developing large-scale wind energy projects. Major global players like Siemens Gamesa, Vestas, and GE Renewable Energy are already active in the market, creating a growing demand for local collaborations and joint ventures. These partnerships can introduce advanced technology, operational expertise, and investment capital, driving the expansion of Qatar’s wind energy sector. Additionally, such collaborations facilitate knowledge transfer and capacity building, helping to accelerate the development of the country’s wind energy infrastructure. This cooperative approach can play a crucial role in achieving Qatar’s renewable energy objectives.

Future Outlook

The future outlook for the wind energy market in Qatar is promising, driven by a combination of technological advancements, government support, and increasing demand for sustainable energy solutions. With significant investments in renewable energy, Qatar is expected to strengthen its position as a leader in the Middle East’s energy transition. The government’s focus on expanding both onshore and offshore wind projects will likely continue, providing long-term opportunities for growth. Additionally, advancements in wind turbine efficiency and grid integration technologies will further enhance the competitiveness of wind energy, ensuring its role in Qatar’s energy mix for years to come.

Major Players

- Siemens Gamesa

- Vestas Wind Systems

- GE Renewable Energy

- Nordex

- Acciona Energia

- Suzlon Energy

- Enel Green Power

- Iberdrola

- Siemens Energy

- Goldwind

- NextEra Energy

- Ørsted

- EDF Renewables

- Trina Solar

- Mitsubishi Power

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Utility companies

- Wind turbine manufacturers

- Engineering, procurement, and construction (EPC) firms

- Environmental consultancies

- Private sector energy developers

- Renewable energy technology providers

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the core variables that influence the wind energy market, including government policies, technology advancements, and market demand factors.

Step 2: Market Analysis and Construction

In this phase, comprehensive data is gathered and analyzed to construct a detailed market model. This includes market size, growth trends, and key drivers.

Step 3: Hypothesis Validation and Expert Consultation

Expert opinions from industry leaders and market participants are sought to validate the findings from the initial analysis and to refine the market model.

Step 4: Research Synthesis and Final Output

The final step consolidates all findings into a coherent market report that provides actionable insights and forecasts for stakeholders in the wind energy market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Government Investment in Renewable Energy

Rising Demand for Clean Energy Solutions

Technological Advancements in Wind Turbines

Favorable Regulatory Framework

Integration of Wind Energy into National Energy Strategy - Market Challenges

High Initial Capital Investment

Intermittency of Wind Energy

Limited Land for Large-Scale Installations

Regulatory and Compliance Barriers

Technical Challenges in Grid Integration - Market Opportunities

Expansion of Offshore Wind Projects

Partnerships with International Wind Energy Players

Development of Floating Wind Systems - Trends

Advancement in Wind Turbine Efficiency

Shift Toward Hybrid and Integrated Energy Systems

Increase in Public-Private Partnerships for Wind Energy Projects - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Offshore Wind Turbines

Onshore Wind Turbines

Hybrid Systems

Floating Wind Systems

Vertical Axis Wind Turbines - By Platform Type (In Value%)

Land-Based Systems

Offshore Systems

Floating Systems

Hybrid Platforms

Integrated Systems - By Fitment Type (In Value%)

Standalone Systems

Grid-Connected Systems

Hybrid Solutions

Modular Systems

Integrated Solutions - By End User Segment (In Value%)

Government Projects

Private Sector Projects

Commercial Projects

Utility Companies

Residential Projects - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Wind Turbine Capacity, Installation Type, Location, Energy Storage Integration, Financing Models)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens Gamesa

Nordex

GE Renewable Energy

Suzlon Energy

Vestas Wind Systems

Mitsubishi Power

Enel Green Power

Acciona Energia

Goldwind

Siemens Energy

NextEra Energy

Ørsted

Iberdrola

EDF Renewables

Brookfield Renewable Partners

- Government Agencies as Key Drivers of Demand

- Private Sector’s Increasing Investment in Clean Energy

- Commercial Sector’s Growing Adoption of Wind Energy

- Utility Providers Leading Wind Energy Integration

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now