Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Singapore’s third-party logistics industry represents a critical component of the country’s international trade ecosystem. Based on a recent historical assessment, the Singapore 3PL market generated approximately USD ~ billion in total service revenue according to logistics industry datasets compiled by Enterprise Singapore and the World Bank logistics performance database. Demand is primarily driven by cross-border trade flows, e-commerce fulfillment requirements, and integrated supply chain management services for manufacturing and technology sectors operating regional headquarters within Singapore’s logistics infrastructure network.

Singapore’s logistics ecosystem is heavily concentrated around globally connected transport hubs that support large-scale freight and distribution activity. The city-state functions as a strategic logistics gateway linking Southeast Asia, East Asia, and global maritime trade corridors. Logistics activity clusters around the Port of Singapore, Changi Air Cargo Hub, and Jurong industrial zone where advanced warehousing infrastructure, digital trade platforms, and integrated freight networks allow logistics providers to manage international cargo flows efficiently while supporting regional distribution operations.

Market Segmentation

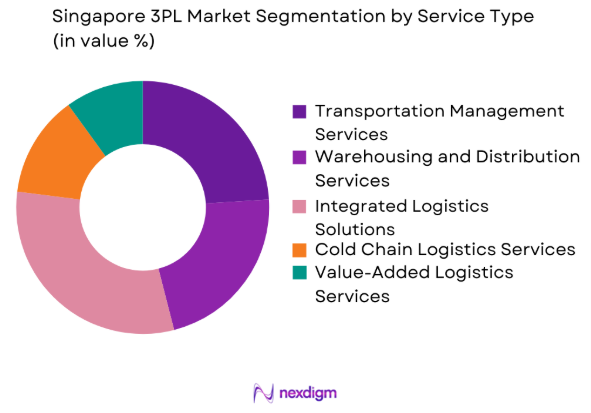

By Service Type

Singapore 3PL market is segmented by product type into transportation management services, warehousing and distribution services, integrated logistics solutions, cold chain logistics services, and value-added logistics services. Recently, integrated logistics solutions has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Companies operating regional distribution hubs increasingly outsource end-to-end supply chain management to 3PL providers capable of coordinating transportation, warehousing, customs clearance, and inventory control through a single service platform. Singapore’s position as a regional headquarters location for multinational manufacturers and technology companies also increases demand for integrated logistics coordination across multiple Southeast Asian markets. Integrated service models allow enterprises to consolidate supply chain functions and reduce operational complexity while improving delivery performance across global trade routes. Advanced warehouse automation systems, digital supply chain platforms, and integrated freight forwarding capabilities offered by major logistics firms further strengthen the dominance of integrated logistics service models across Singapore’s logistics sector.

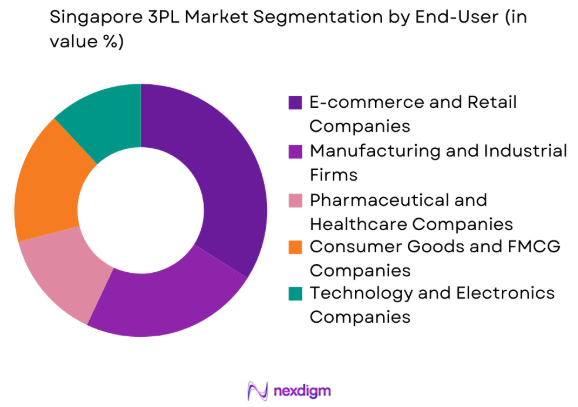

By End User Industry

Singapore 3PL market is segmented by product type into e-commerce and retail companies, manufacturing and industrial firms, pharmaceutical and healthcare companies, consumer goods and FMCG companies, and technology and electronics companies. Recently, e-commerce and retail companies has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Rapid expansion of online retail platforms across Southeast Asia has increased demand for fulfillment centers, cross-border parcel logistics, and last-mile delivery services managed through Singapore-based logistics hubs. Major e-commerce companies utilize Singapore as a regional logistics gateway because of its efficient port infrastructure, strong digital trade ecosystem, and advanced customs clearance processes. Logistics providers continue investing in automated distribution centers and high-capacity parcel sorting facilities that support fast order fulfillment across regional markets. Consumer demand for faster delivery services and cross-border e-commerce transactions also increases dependence on third-party logistics providers that offer scalable distribution infrastructure across the regional supply chain network.

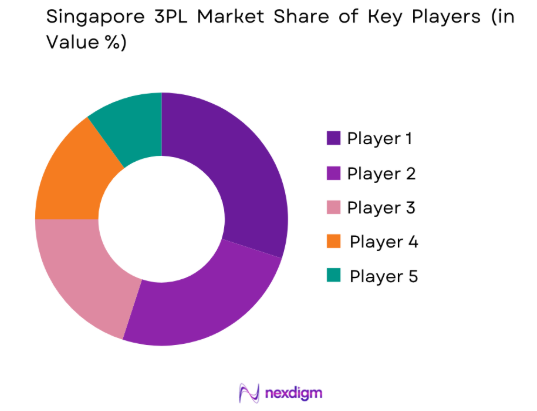

Competitive Landscape

The Singapore 3PL market is characterized by the presence of global logistics providers, regional freight forwarding companies, and specialized contract logistics operators competing across integrated supply chain services. Market consolidation has increased as multinational logistics firms expand warehousing capacity, digital freight platforms, and cross-border logistics networks across Southeast Asia. Large logistics companies leverage advanced warehouse automation, multimodal freight operations, and integrated technology platforms to strengthen service capabilities while maintaining strong relationships with multinational corporations operating regional distribution centers in Singapore.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Germany | ~ | ~ | ~ | ~ | ~ |

| DSV | 1976 | Denmark | ~ | ~ | ~ | ~ | ~ |

| UPS Supply Chain Solutions | 1907 | United States | ~ | ~ | ~ | ~ | ~ |

Singapore 3PL Market Analysis

Growth Drivers

Expansion of Cross Border Trade and Regional Supply Chain Hub Development

Singapore’s position as a global trade gateway strengthens demand for third party logistics services as international trade across Southeast Asia expands. Its location along major maritime routes connecting Asia, Europe, and the Americas allows logistics providers to manage large volumes of containerized cargo moving through regional supply chains. The Port of Singapore handles extensive merchandise trade flows that support logistics operations. Multinational manufacturers and technology firms establish regional distribution hubs due to efficient customs procedures, reliable infrastructure, and advanced logistics capabilities. Integrated logistics parks and free trade zones support cross border supply chain coordination. Investments in port expansion, automated terminals, and air cargo infrastructure further strengthen Singapore’s logistics capacity.

Rapid Growth of E Commerce Fulfillment and Regional Distribution Networks

Rapid growth of e commerce activity across Southeast Asia significantly increases demand for third party logistics providers capable of managing large scale order fulfillment and parcel distribution operations. Singapore serves as a central logistics hub for regional online retail platforms due to advanced warehousing infrastructure, strong digital payment systems, and reliable transportation networks. Logistics providers develop automated fulfillment centers with robotic sorting and advanced inventory management technologies to improve processing efficiency. These facilities enable centralized inventory management and distribution across multiple Southeast Asian markets. Companies also deploy data analytics platforms for real time shipment tracking and demand forecasting. Rising consumer expectations for faster delivery further encourage expansion of last mile networks and specialized logistics services across regional supply chains.

Market Challenges

High Operating Costs and Limited Land Availability for Logistics Infrastructure

Singapore’s logistics sector faces structural challenges due to high operating costs and limited industrial land for large scale logistics infrastructure development. Warehousing and distribution centers require substantial space for inventory storage, cargo handling, and automated equipment, yet Singapore’s limited land availability restricts expansion opportunities. High real estate prices significantly raise the cost of building logistics parks and warehouse facilities compared with neighboring Southeast Asian markets. Logistics companies therefore optimize existing space through automation technologies and high density storage systems. Labor expenses remain higher than many regional markets, increasing operational costs for logistics providers. Firms invest in robotics and automated systems to improve efficiency, while strict zoning regulations and limited urban logistics facilities further complicate distribution operations.

Intense Competition Among Global Logistics Providers and Regional Operators

Singapore’s logistics industry faces strong competition from multinational logistics corporations, regional freight forwarding firms, and technology driven logistics startups. Global logistics providers possess extensive transportation networks, advanced supply chain technologies, and large warehousing capacity, giving them advantages when serving multinational clients. Regional logistics companies compete by offering specialized services, local expertise, and flexible pricing strategies aimed at small and medium sized enterprises across Southeast Asia. Digital logistics platforms add further competitive pressure by enabling online freight booking, real time shipment tracking, and data driven logistics optimization. These platforms increase market transparency and price comparison across providers. Logistics companies therefore invest in technology, service innovation, and value added supply chain solutions to maintain competitiveness.

Opportunities

Development of Smart Logistics Infrastructure and Automated Warehousing Technologies

Singapore’s logistics sector offers strong opportunities for companies investing in automation technologies and smart logistics infrastructure to improve supply chain efficiency. Automated warehouses equipped with robotics, autonomous forklifts, and high speed sorting systems increase cargo handling capacity while reducing labor requirements. Logistics firms are deploying warehouse management software integrated with artificial intelligence to optimize inventory placement, order picking, and shipment routing. These technologies enable operators to manage high cargo volumes efficiently despite limited warehouse space. Smart logistics infrastructure also allows real time monitoring of cargo movement using Internet of Things sensors and digital tracking platforms. Investments in automated container terminals and smart port systems further strengthen logistics efficiency and support advanced supply chain operations.

Expansion of Pharmaceutical and Cold Chain Logistics Services Across Asia Pacific

Rising healthcare demand and pharmaceutical manufacturing expansion across Asia Pacific create strong opportunities for logistics providers specializing in temperature controlled supply chain management. Pharmaceutical products, vaccines, and biotechnology materials require strict temperature monitoring and specialized storage infrastructure during transportation and distribution. Singapore’s advanced healthcare ecosystem and supportive regulatory framework make the country an important location for regional cold chain logistics hubs serving pharmaceutical companies across Asia. Logistics providers are developing temperature controlled warehouses, refrigerated transportation fleets, and digital monitoring systems that ensure compliance with pharmaceutical storage standards. Cold chain operators also deploy advanced sensors that track temperature conditions across supply routes and alert logistics managers to deviations. These developments strengthen demand for reliable temperature controlled logistics supporting healthcare supply chains.

Future Outlook

Singapore’s 3PL market is expected to expand steadily as regional trade flows and e-commerce logistics volumes continue increasing across Southeast Asia. Logistics providers are investing heavily in warehouse automation, smart port infrastructure, and digital supply chain management platforms to improve operational efficiency. Government initiatives supporting trade facilitation and logistics infrastructure modernization further strengthen Singapore’s position as a regional distribution hub. Demand from pharmaceutical, electronics, and online retail sectors will continue driving advanced logistics service adoption across integrated supply chain networks.

Major Players

- DHL Supply Chain

- DB Schenker

- Kuehne + Nagel

- DSV

- UPS Supply Chain Solutions

- FedEx Logistics

- CEVA Logistics

- Nippon Express

- Yusen Logistics

- Expeditors International

- Bolloré Logistics

- CJ Logistics

- Agility Logistics

- Maersk Logistics & Services

- SATS Ltd

Key Target Audience

- Logistics and supply chain companies

- E-commerce and retail companies

- Manufacturing and industrial exporters

- Pharmaceutical and healthcare companies

- Technology and electronics manufacturers

- Transportation infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identification of major industry variables affecting the Singapore 3PL market including trade flows, logistics infrastructure, warehousing capacity, supply chain outsourcing trends, and e-commerce fulfillment demand. Data points are mapped across logistics services including transportation management, warehousing, and integrated supply chain operations.

Step 2: Market Analysis and Construction

Market modeling is conducted by combining secondary research sources including government trade statistics, port throughput data, logistics industry reports, and corporate financial disclosures. Data triangulation methods are used to construct a comprehensive market structure including service segmentation and industry revenue distribution.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary research findings are validated through consultations with logistics industry professionals, supply chain managers, freight forwarding executives, and technology providers operating within Singapore’s logistics ecosystem. Expert insights help confirm demand drivers and operational trends affecting third party logistics service adoption.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights are consolidated to develop a structured analysis of the Singapore 3PL market including segmentation trends, competitive landscape, infrastructure developments, and future growth opportunities. Final outputs integrate validated data sources and expert insights into a comprehensive research framework.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Fulfillment and Cross Border Trade

Strategic Development of Integrated Logistics Infrastructure

Rising Demand for Supply Chain Optimization and Outsourcing - Market Challenges

High Operating Costs and Warehouse Space Constraints

Intense Competition Among Regional Logistics Providers

Complex Regulatory Compliance for Cross Border Logistics - Market Opportunities

Expansion of Automated Warehousing and Smart Logistics Facilities

Growth in Pharmaceutical and Cold Chain Logistics Demand

Adoption of Digital Freight Platforms and Data Driven Supply Chains - Trends

Integration of Artificial Intelligence in Logistics Operations

Growth of Sustainable and Green Logistics Practices

Increasing Adoption of Multimodal Freight Solutions - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Transportation Management Services

Warehousing and Distribution Services

Integrated Logistics Solutions

Cold Chain Logistics Services

Value Added Logistics Services - By Platform Type (In Value%)

Road Logistics Platforms

Air Freight Logistics Platforms

Sea Freight Logistics Platforms

Multimodal Logistics Platforms

Digital Logistics Management Platforms - By Fitment Type (In Value%)

Dedicated Contract Logistics

Shared Warehousing Solutions

On Demand Logistics Services

Integrated End to End Logistics Solutions

Hybrid Logistics Service Models - By End User Segment (In Value%)

E-commerce and Retail Companies

Manufacturing and Industrial Firms

Pharmaceutical and Healthcare Companies

Consumer Goods and FMCG Companies

Technology and Electronics Companies - By Procurement Channel (In Value%)

Direct Enterprise Logistics Contracts

Government and Public Sector Logistics Tenders

Long Term Strategic Logistics Partnerships

Third Party Logistics Brokers

Digital Freight and Logistics Platforms

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio Breadth, Warehousing Capacity, Digital Logistics Integration, Geographic Coverage, Industry Specialization)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain

DB Schenker

Kuehne + Nagel

DSV

UPS Supply Chain Solutions

FedEx Logistics

CEVA Logistics

Nippon Express

Yusen Logistics

Expeditors International

Bolloré Logistics

CJ Logistics

Agility Logistics

Maersk Logistics & Services

SATS Ltd

- E-commerce companies increasingly outsource fulfillment and delivery logistics to specialized 3PL providers

- Manufacturing firms rely on integrated warehousing and transportation services to support regional supply chains

- Healthcare and pharmaceutical companies demand temperature controlled logistics infrastructure

- Technology and electronics firms require high value cargo handling and global distribution networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now