Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore Advanced Materials market recorded a value of approximately USD ~ billion, supported by strong demand from semiconductor fabrication, electronics manufacturing, aerospace engineering, and biomedical technology industries. Advanced materials such as nanomaterials, specialty polymers, advanced ceramics, and electronic grade materials are widely integrated across high precision manufacturing systems. Government supported innovation programs and industrial research initiatives led by the Agency for Science Technology and Research and the Economic Development Board further strengthen materials science commercialization and industrial deployment across advanced manufacturing industries.

Singapore’s advanced materials ecosystem is concentrated within technology intensive industrial clusters such as Jurong Innovation District, one north research hub, and Tuas industrial zone where semiconductor fabrication plants and precision engineering firms operate advanced production infrastructure. These locations host research laboratories, multinational manufacturing facilities, and innovation centers focused on materials engineering and nanotechnology development. Strong logistics connectivity, highly skilled technical workforce, and strong government support for advanced manufacturing research allow these industrial clusters to function as key hubs supporting advanced materials production and technology deployment.

Market Segmentation

By Product Type

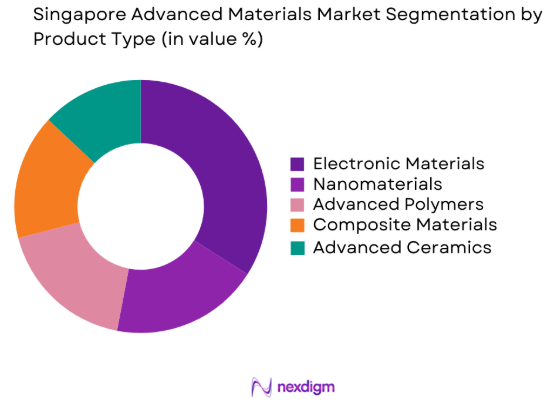

Singapore Advanced Materials market is segmented by product type into X, composite materials, and electronic materials. Recently, electronic materials has a dominant market share due to factors such as strong semiconductor manufacturing demand, advanced electronics assembly infrastructure, and increasing integration of specialized materials in chip fabrication processes. Semiconductor manufacturing requires extremely high purity materials including silicon wafers, photoresists, specialty chemicals, and deposition materials used in lithography and etching processes. Singapore’s globally recognized semiconductor manufacturing ecosystem and continuous investments in fabrication facilities have significantly strengthened demand for advanced electronic materials used across microelectronics and integrated circuit production.

By End Use Industry

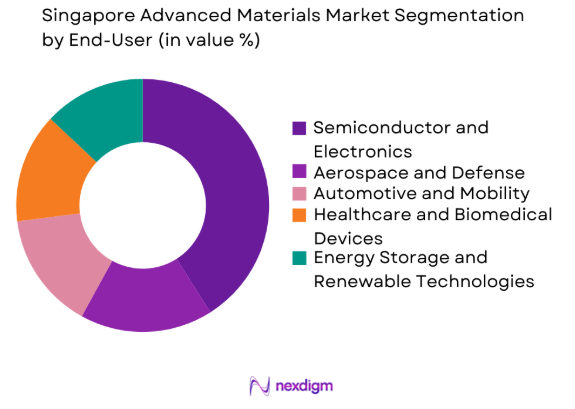

Singapore Advanced Materials market is segmented by end use industry into semiconductor and electronics, aerospace and defense, automotive and mobility, healthcare and biomedical devices, and energy storage and renewable technologies. Recently, semiconductor and electronics has a dominant market share due to factors such as large scale semiconductor fabrication facilities, advanced electronics manufacturing infrastructure, and strong export driven electronics production activities. The presence of major semiconductor manufacturers and global electronics firms operating advanced fabrication plants significantly drives demand for high performance materials used in wafer production, electronic components, and integrated circuit packaging technologies.

Competitive Landscape

The Singapore Advanced Materials market demonstrates moderate consolidation characterized by the presence of global chemical manufacturers, advanced materials innovators, and electronics material suppliers operating research and manufacturing facilities within Singapore. Major multinational companies collaborate closely with semiconductor manufacturers and advanced manufacturing firms to supply specialized materials used in electronics fabrication, aerospace engineering, and energy technologies. Continuous investment in research laboratories and material innovation partnerships has intensified competition among global suppliers competing to develop next generation materials with higher performance, durability, and precision characteristics.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Core Materials Portfolio |

| BASF SE | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| DuPont | 1802 | United States | ~ | ~ | ~ | ~ | ~ |

| Toray Industries | 1926 | Japan | ~ | ~ | ~ | ~ | ~ |

| 3M Company | 1902 | United States | ~ | ~ | ~ | ~ | ~ |

| Evonik Industries | 2007 | Germany | ~ | ~ | ~ | ~ | ~ |

Singapore Advanced Materials Market Analysis

Growth Drivers

Expansion of Semiconductor Fabrication and Microelectronics Manufacturing Ecosystem

Singapore hosts a highly advanced semiconductor manufacturing ecosystem that significantly increases demand for high performance advanced materials used in microelectronics production. Semiconductor fabrication requires specialized materials including high purity silicon wafers, photoresists, dielectric layers, deposition chemicals, and nanostructured materials used during lithography and etching processes. Major multinational semiconductor companies operate fabrication facilities producing integrated circuits for consumer electronics, telecommunications equipment, automotive electronics, and data center processors. These processes require materials with exceptional purity and precise structural characteristics. Expanding semiconductor manufacturing capacity across Singapore’s technology clusters continues strengthening demand for electronic grade materials. Collaboration between semiconductor manufacturers and research institutions also supports development of materials enabling next generation chip technologies.

Growing Investment in Nanotechnology and Advanced Materials Research Infrastructure

Singapore has developed a globally recognized research ecosystem focused on materials science innovation and nanotechnology development, supporting commercialization of advanced materials across multiple industries. Government supported organizations such as the Agency for Science Technology and Research operate laboratories dedicated to nanomaterials engineering, advanced polymers, biomedical materials, and functional material technologies. These institutions collaborate with universities and manufacturers to develop next generation materials for electronics manufacturing, healthcare technologies, energy storage systems, and aerospace applications. Continuous investment in research infrastructure attracts global materials science companies and skilled professionals. Public private partnerships accelerate commercialization of laboratory innovations. This research driven environment strengthens Singapore’s role as a regional hub for advanced materials development and industrial deployment.

Market Challenges

High Production Costs and Complex Manufacturing Processes for Advanced Materials

Advanced materials manufacturing requires sophisticated production technologies, specialized chemical processing equipment, and highly controlled environments capable of maintaining precise temperature, pressure, and purity conditions throughout production cycles. These requirements significantly increase manufacturing costs compared with conventional material production processes. Materials such as nanomaterials, electronic grade chemicals, and high performance composites require complex synthesis techniques including chemical vapor deposition, molecular engineering, and advanced polymerization. These processes demand substantial investment in specialized equipment and high precision quality control systems. Singapore’s high cost industrial environment, skilled labor requirements, and strict environmental safety regulations further increase operational expenses. Manufacturers must therefore improve production efficiency and adopt advanced technologies to reduce costs and maintain competitiveness.

Dependence on Imported Rare Elements and Specialized Raw Material Supply Chains

Many advanced materials require rare earth elements, specialty metals, and highly refined chemical compounds that are not available within Singapore’s domestic resource base. Semiconductor materials, nanomaterials, high performance magnets, and advanced battery materials depend on metals such as gallium, indium, cobalt, lithium, and other rare earth elements sourced from limited global mining regions. Singapore therefore relies heavily on international supply chains to obtain these essential inputs for advanced materials manufacturing. Geopolitical tensions, export restrictions, and mining disruptions can affect material availability and pricing. Logistics costs and transportation of high purity chemical precursors also increase production expenses. Diversifying supply partnerships and developing alternative material formulations are important strategies for maintaining stable raw material availability.

Opportunities

Development of Next Generation Semiconductor Materials for Advanced Chip Manufacturing

Semiconductor technology continues advancing toward smaller transistor nodes, faster processing capabilities, and improved energy efficiency, increasing demand for innovative materials that support these developments. Advanced materials such as high k dielectric materials, compound semiconductors, and specialized conductive layers are essential for modern semiconductor device fabrication. Singapore’s strong semiconductor manufacturing ecosystem supports development and commercialization of these materials within advanced chip production environments. Research laboratories collaborate with semiconductor manufacturers to test materials that enhance chip performance and manufacturing precision. Materials enabling three dimensional chip architectures, advanced packaging systems, and high frequency electronic devices are increasingly required worldwide. Singapore’s research infrastructure and manufacturing ecosystem therefore create strong opportunities for companies developing specialized semiconductor materials.

Growth of Advanced Materials Applications in Energy Storage and Renewable Energy Technologies

Global energy transition initiatives are increasing demand for advanced materials used in battery technologies, hydrogen fuel systems, solar photovoltaic infrastructure, and other renewable energy technologies. Materials such as lithium ion battery cathodes, solid state electrolytes, graphene conductors, and advanced composites play essential roles in energy storage systems. Singapore’s strong focus on sustainable energy innovation and clean technology development supports material research and industrial adoption. Research institutions and technology companies develop materials that improve battery energy density, charging efficiency, and durability for electric mobility and grid energy storage systems. Advanced materials also enhance photovoltaic efficiency, enabling higher electricity generation. Singapore’s research driven ecosystem therefore creates long term opportunities for advanced materials manufacturers supporting global renewable energy expansion.

Future Outlook

The Singapore Advanced Materials market is expected to experience sustained growth driven by expanding semiconductor manufacturing capacity, rising investments in nanotechnology research, and increasing adoption of advanced materials across aerospace, electronics, healthcare, and renewable energy industries. Continuous innovation in materials science will enable the development of high performance materials supporting next generation manufacturing technologies. Government support for research and advanced manufacturing infrastructure will further accelerate commercialization of new materials technologies across industrial sectors.

Major Players

- BASF SE

- DuPont

- Toray Industries

- 3M Company

- Evonik Industries

- Covestro AG

- Mitsubishi Chemical Group

- Arkema SA

- Solvay SA

- Huntsman Corporation

- Saint Gobain

- LG Chem

- Sumitomo Chemical

- Kuraray Co Ltd

- Showa Denko

Key Target Audience

- Semiconductor manufacturing companies

- Aerospace and defense equipment manufacturers

- Automotive and electric vehicle manufacturers

- Energy storage and battery manufacturers

- Healthcare and biomedical device manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Advanced materials manufacturing companies

Research Methodology

Step 1: Identification of Key Variables

The research begins with identifying core variables affecting the Singapore Advanced Materials market including technological innovation, industrial demand, advanced manufacturing capacity, and regulatory frameworks influencing material science industries.

Step 2: Market Analysis and Construction

Primary and secondary data sources including government publications, industrial databases, and manufacturing reports are analyzed to construct segmentation models and competitive mapping of the Singapore Advanced Materials market.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including materials scientists, semiconductor engineers, and manufacturing specialists are consulted to validate demand trends, technological adoption, and industry growth patterns.

Step 4: Research Synthesis and Final Output

Validated research findings are synthesized into a comprehensive report including market structure, industry drivers, challenges, competitive positioning, and future development trends shaping the Singapore Advanced Materials market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Semiconductor Manufacturing and Electronics Production

Government Supported Research and Innovation in Advanced Materials

Increasing Demand for Lightweight High Performance Materials - Market Challenges

High Production Costs of Advanced Material Manufacturing

Dependence on Imported Raw Materials and Rare Elements

Complex Manufacturing and Processing Requirements - Market Opportunities

Development of Next Generation Semiconductor Materials

Growth of Energy Storage and Battery Material Technologies

Expansion of Biomedical and Healthcare Material Applications - Trends

Rapid Adoption of Nanomaterials in Electronics Manufacturing

Growing Integration of Advanced Materials in Electric Vehicles

Expansion of Additive Manufacturing Materials and Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Polymers and High Performance Plastics

Nanomaterials and Nanostructured Materials

Composite Materials and Fiber Reinforced Structures

Electronic and Semiconductor Materials

Advanced Ceramics and Functional Materials - By Platform Type (In Value%)

Electronics and Semiconductor Manufacturing

Aerospace and Defense Systems

Automotive and Electric Mobility Platforms

Energy Storage and Renewable Energy Systems

Biomedical and Healthcare Devices - By Fitment Type (In Value%)

Embedded Material Integration

Structural Component Integration

Surface Coating and Functional Layer Integration

Additive Manufacturing Material Integration

Microelectronic Material Deposition Systems - By End User Segment (In Value%)

Semiconductor and Electronics Manufacturers

Aerospace and Defense Equipment Producers

Automotive and Electric Vehicle Manufacturers

Healthcare and Biomedical Device Manufacturers

Energy Storage and Clean Energy Technology Firms - By Procurement Channel (In Value%)

Direct Industrial Procurement

Long Term Strategic Supply Contracts

Government Research and Innovation Procurement

Technology Licensing and Material Partnerships

Specialized Advanced Materials Distributors

- Market Share Analysis

- Cross Comparison Parameters (Material Innovation Capability, Manufacturing Technology, Product Portfolio Diversity, Global Supply Chain Integration, End Industry Coverage, R&D Investment Intensity, Patent Portfolio Strength, Strategic Industry Partnerships, Production Capacity Scale, Sustainability and Environmental Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

3M Company

Dow Inc.

DuPont de Nemours Inc.

Toray Industries

Hexcel Corporation

Evonik Industries

BASF SE

Arkema SA

Covestro AG

Mitsubishi Chemical Group

Solvay SA

Hitachi Chemical Company

Showa Denko Materials

Huntsman Corporation

Saint Gobain

- Semiconductor Manufacturers Driving Demand for Electronic Materials

- Aerospace Firms Increasing Use of Lightweight Composite Materials

- Automotive Sector Integrating High Performance Materials in EV Platforms

- Healthcare Industry Expanding Biomedical Material Applications

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now