Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore Aerospace and Defense market is valued at approximately USD ~ billion based on a recent historical assessment. The market is primarily driven by increasing government expenditure on national security, technological advancements in defense systems, and a growing demand for air travel infrastructure. In addition, regional geopolitical tensions and the rising demand for defense electronics and autonomous military systems are also contributing to market growth. Furthermore, the strategic location of Singapore as a key player in the Asia-Pacific region enhances its aerospace and defense prominence.

Singapore’s aerospace and defense sector benefits from its strategic geographic location, making it an essential hub for both commercial and defense industries. The country’s proximity to major shipping lanes and its modern infrastructure have fostered a robust defense sector. Singapore has successfully positioned itself as a key player in the Asia-Pacific market due to its strong technological capabilities and government-driven investments in defense modernization. The country also plays a vital role in regional collaborations with major global defense and aerospace contractors.

Market Segmentation

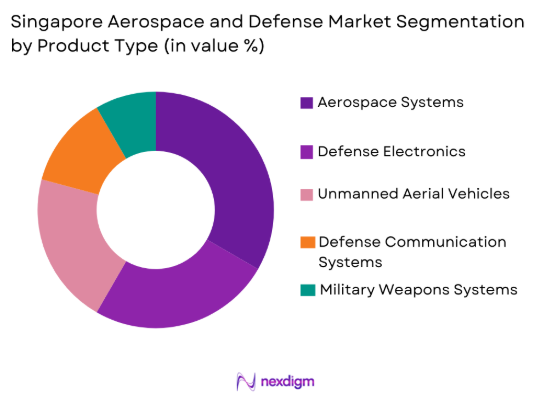

By Product Type

The Singapore Aerospace and Defense market is segmented by product type into aerospace systems, defense electronics, unmanned aerial vehicles, defense communication systems, and military weapons systems. Recently, aerospace systems have dominated the market share due to factors such as increasing air travel demand, government investments in national security, and advancements in commercial aircraft technology. The availability of sophisticated manufacturing facilities and established infrastructure for aerospace production has further contributed to this dominance.

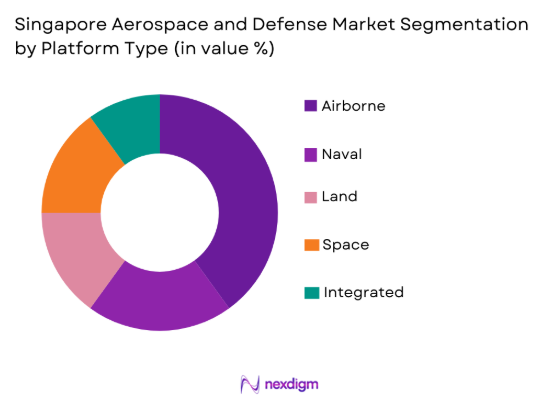

By Platform Type

The Singapore Aerospace and Defense market is segmented by platform type into airborne platforms, naval platforms, land-based platforms, space-based platforms, and integrated platforms. Airborne platforms dominate the market share due to the country’s strong air force presence, continuous airspace monitoring needs, and an expanding commercial aviation sector. Singapore’s commitment to upgrading its air defense systems has led to robust demand for advanced airborne platforms, including fighter jets, drones, and surveillance aircraft.

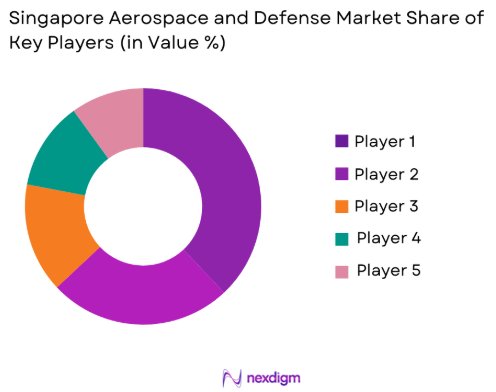

Competitive Landscape

The competitive landscape of the Singapore Aerospace and Defense market is dominated by both local and international players. The market has seen consolidation with large defense and aerospace companies such as ST Engineering and Lockheed Martin, which significantly influence the supply of advanced defense technologies. The competitive environment is marked by high R&D investments, innovation in aerospace technologies, and strategic government partnerships that ensure a steady demand pipeline.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| ST Engineering | 1967 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | USA | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | France | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 1922 | USA | ~ | ~ | ~ | ~ | ~ |

Singapore Aerospace and Defense Market Analysis

Growth Drivers

Increased government expenditure on national security

As Singapore faces growing regional security concerns, its government has significantly increased defense spending. The government’s commitment to enhancing national security is reflected in various defense contracts and the modernization of military infrastructure. This has led to a steady increase in demand for defense technologies, including advanced weapons systems, cybersecurity solutions, and surveillance platforms. Furthermore, the government’s investment in aerospace infrastructure, such as Changi Airport, has spurred growth in aerospace technology development, boosting the economy and the defense sector simultaneously.

Technological advancements in military systems

Technological advancements in areas such as drones, surveillance systems, and autonomous defense technologies are contributing to market growth. The integration of artificial intelligence (AI) and machine learning in military operations has improved strategic capabilities, offering enhanced surveillance, reconnaissance, and cybersecurity features. With increasing demand for unmanned aerial systems (UAS) and precision-guided weapons, these innovations are expected to drive long-term growth in the aerospace and defense sector.

Market Challenges

High capital expenditure in defense projects

The high capital expenditure required for defense projects, particularly in upgrading air and land defense systems, remains a significant challenge in Singapore’s aerospace and defense market. While the government has been supportive of funding, the large initial investments in infrastructure and technology can deter private sector participation. Moreover, long-term contract durations and high operational costs may limit smaller companies from entering the market, increasing reliance on larger, well-established players for defense procurement.

Cybersecurity threats and vulnerabilities

As defense systems become increasingly connected to global networks and reliant on digital technologies, cybersecurity threats present a growing challenge. Vulnerabilities in defense communication systems, unmanned platforms, and weapon systems create significant security risks. Protecting critical national infrastructure from cyberattacks is essential to maintaining defense capabilities, necessitating substantial investments in cybersecurity technologies. Additionally, these cybersecurity concerns add complexity to the integration of newer defense technologies, impeding market growth in the short term.

Opportunities

Expansion of artificial intelligence (AI)-driven defense solutions

As AI technology advances, it presents new opportunities for the Singapore aerospace and defense market. AI can enhance defense systems by improving decision-making processes, automating operations, and optimizing resource allocation. The growing integration of AI in military technologies such as autonomous drones and surveillance systems opens up new market avenues. Additionally, AI-based solutions can help defense organizations streamline operations, improve efficiency, and reduce costs, all contributing to market growth.

Partnerships with private tech firms for enhanced cybersecurity:

As cybersecurity threats intensify, there is a rising need for partnerships between defense organizations and private technology firms specializing in cybersecurity solutions. Such partnerships can enable the adoption of cutting-edge technologies, such as encryption, intrusion detection systems, and threat intelligence tools. The collaboration between government entities and tech companies can lead to the development of robust defense platforms that offer advanced protection against cyberattacks, enhancing national security and promoting long-term market growth.

Future Outlook

The Singapore Aerospace and Defense market is expected to witness steady growth in the next five years, driven by ongoing investments in military modernization, technological advancements, and regional security dynamics. There is increasing demand for high-tech aerospace solutions, with emphasis on unmanned systems, AI-powered defense technologies, and cybersecurity infrastructure. Regulatory support, strategic defense partnerships, and government funding will further foster innovation in defense systems, positioning Singapore as a leading market for aerospace and defense solutions in the Asia-Pacific region.

Major Players

- ST Engineering

- Lockheed Martin

- Boeing

- Thales Group

- Raytheon Technologies

- General Dynamics

- Northrop Grumman

- Airbus

- BAE Systems

- Leonardo

- Elbit Systems

- L3 Technologies

- Saab Group

- Mitsubishi Heavy Industries

- Rockwell Collins

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Military forces

- Aerospace contractors

- Defense system manufacturers

- Aerospace technology developers

- Unmanned aerial system (UAS) developers

- Private defense contractors

Research Methodology

Step 1: Identification of Key Variables

Key market drivers, challenges, and trends are identified by analyzing primary and secondary data sources, including government reports, industry publications, and expert interviews.

Step 2: Market Analysis and Construction

Data is collected and analyzed to estimate market size, segmentation, and future forecasts, using reliable sources like financial reports and industry analysis to ensure accurate modeling.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts and key stakeholders are consulted to validate findings, ensure market assumptions are realistic, and refine forecasts.

Step 4: Research Synthesis and Final Output

Data from all research phases are synthesized into a comprehensive report, ensuring that conclusions and recommendations are both insightful and actionable.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased government investments in national defense

Technological advancements in AI and robotics

Growing geopolitical tensions in the Asia-Pacific

Military modernization programs in Southeast Asia

Integration of commercial technologies into defense systems - Market Challenges

High capital expenditure in defense projects

Cybersecurity threats and vulnerabilities

Regulatory and compliance barriers

Technological integration and interoperability issues

Political and social resistance to military expansion - Market Opportunities

Expansion in AI-driven defense solutions

Partnerships with private tech firms for enhanced cybersecurity

Emerging demand for autonomous systems and robotics - Trends

Increase in use of autonomous and unmanned systems

Integration of AI and machine learning in battlefield operations

Surge in cybersecurity investments for defense systems

Growing interest in space-based defense capabilities

Development of hybrid defense platforms - Government Regulations & Defense Policy

Data protection and privacy regulations

Export control and compliance policies

Government funding and grants for defense technologies

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Aircraft Systems

Defense Electronics

Military Communication Systems

Unmanned Aerial Systems (UAS)

Weapon Systems - By Platform Type (In Value%)

Land Platforms

Airborne Platforms

Naval Platforms

Space Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (in Value%)

Metal Alloys

Composite Materials

Electronics & Sensors

Advanced Propulsion Technologies

Software Solutions

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

ST Engineering

Singapore Technologies Aerospace

Lockheed Martin

BAE Systems

Thales Group

General Dynamics

Northrop Grumman

Raytheon Technologies

L3 Technologies

Leonardo

Harris Corporation

Saab Group

Rheinmetall AG

Elbit Systems

Hewlett Packard Enterprise

- Military Forces’ increasing demand for digital systems

- Government agencies’ role in regulating and procuring defense systems

- Defense contractors’ shift towards innovation and integration

- Private sector’s growing interest in cybersecurity solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now