Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore Aircraft Flight Recorder market is valued at approximately USD ~million. This market is primarily driven by increasing demand for flight safety compliance in the aviation sector. The Civil Aviation Authority of Singapore (CAAS) mandates the use of flight data recorders (FDR) and cockpit voice recorders (CVR) in all commercial aircraft, which has led to widespread adoption across various airline fleets. Additionally, the expansion of Singapore Airlines, which has continued to grow its fleet and global reach, has contributed significantly to the market’s growth. The aviation safety industry in Singapore is also bolstered by regional growth in air traffic, particularly within Southeast Asia, which creates a robust demand for advanced flight recorder systems. The demand is further supported by regulatory standards that align with ICAO (International Civil Aviation Organization) requirements.

Singapore is a major hub for aviation in Southeast Asia and plays a crucial role in the aircraft flight recorder market. The country’s strategic location as a global transit point, combined with the growing importance of Singapore Airlines, positions it as a key player in the market. Singapore’s highly developed aviation infrastructure and its compliance with strict ICAO safety standards have made it a leader in the deployment of modern flight safety technologies, including flight recorders. The government’s commitment to maintaining and enhancing aviation safety, along with investments in air traffic control and regulatory compliance, ensures the country remains at the forefront of the region’s aircraft flight recorder market.

Market Segmentation

By Product Type

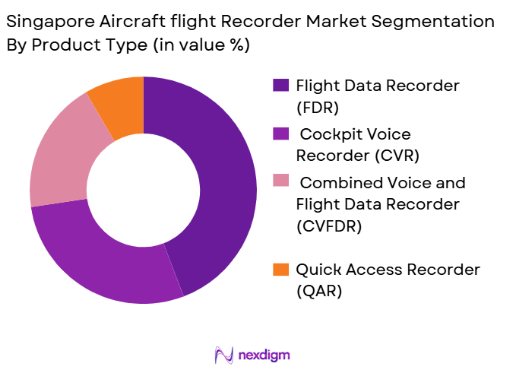

The Singapore Aircraft Flight Recorder market is segmented by product type into Flight Data Recorders (FDR), Cockpit Voice Recorders (CVR), Combined Voice and Flight Data Recorders (CVFDR), and Quick Access Recorders (QAR). The FDR segment is the most dominant in the market due to its critical role in capturing flight parameters essential for accident investigations and safety monitoring. With Singapore’s strong airline infrastructure and fleet composition, particularly in the wide-body aircraft sector, the demand for FDR systems has been substantial. FDRs are integral to meeting the mandatory regulatory requirements set by Singapore’s Civil Aviation Authority and ICAO. The FDR segment is expected to continue holding the largest share due to its entrenched presence in the aviation sector and its regulatory importance.

By Aircraft Type

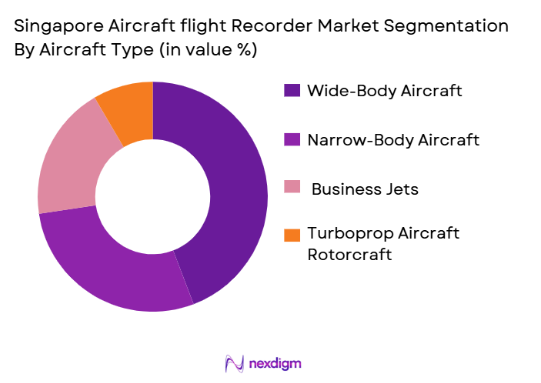

The market is also segmented by aircraft type, which includes narrow-body aircraft, wide-body aircraft, business jets, turboprop aircraft, and rotorcraft. The wide-body aircraft segment dominates the market in Singapore due to the significant presence of large international carriers such as Singapore Airlines, which operates a large number of wide-body aircraft for long-haul flights. Wide-body aircraft require advanced flight recorder systems for their increased complexity, including extended flight durations and higher passenger volumes, which necessitate detailed data recording for safety and regulatory compliance. The wide-body segment will continue to dominate in terms of the number of flight recorders required, given the strategic focus of Singapore Airlines and the strong growth of air travel in the region.

Competitive Landscape

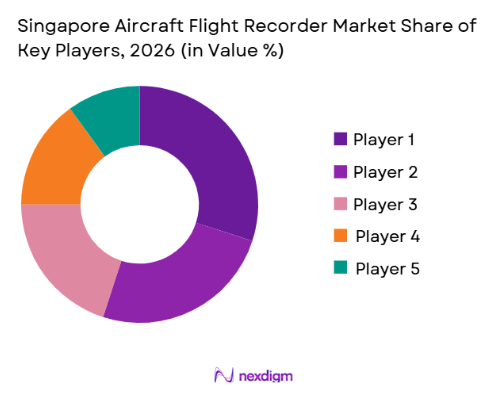

The Singapore Aircraft Flight Recorder market is dominated by several major players that have a strong global presence and technological capabilities. Companies like Honeywell Aerospace, L3Harris Technologies, and Collins Aerospace lead the market due to their comprehensive product portfolios, advanced technologies, and established relationships with airlines and regulatory bodies. The competition in the market highlights the influence of both global and regional players that provide flight recorder systems that comply with stringent safety and data security standards.

| Company | Establishment Year | Headquarters | Revenue (2023) | Product Portfolio | Key Market | Technology Focus |

| Honeywell Aerospace | 1906 | USA | ~ | ~ | ~ | ~ |

| L3Harris Technologies | 2019 | USA | ~ | ~ | ~ | ~ |

| Collins Aerospace (Raytheon) | 2018 | USA | ~ | ~ | ~ | ~ |

| Safran Electronics & Defense | 2005 | France | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | France | ~ | ~ | ~ | ~ |

Singapore Aircraft Flight Recorder Market Analysis

Growth Drivers

Mandatory Flight Safety Recording Compliance

Singapore’s aviation sector operates under stringent safety mandates enforced by the Civil Aviation Authority of Singapore (CAAS) and aligned with International Civil Aviation Organization (ICAO) regulations that require flight data and cockpit voice recorders on all commercial aircraft. Changi Airport, one of the world’s busiest hubs, recorded ~ passenger movements and ~ aircraft movements in 2025, indicating high flight activity that necessitates enhanced safety systems such as flight recorders. These movements reflect robust operations where compliance with recorder standards ensures accurate incident investigation and continuous safety monitoring. CAAS’s annual report highlights the aviation workforce returning to pre pandemic levels across ~ personnel, further solidifying safety compliance infrastructure. This mandatory compliance under regulatory frameworks drives consistent deployment and upgrades of flight recorder systems across Singapore’s airline fleets.

Expansion of Singapore Airlines Fleet & International Routes

Singapore Airlines remains a key driver of demand for flight recorder systems due to its sizeable and expanding fleet. As per the Singapore Airlines Group operating statistics, the airline operated ~ aircraft as of early 2026, including long haul widebody jets that require advanced recorder systems to support safety and operational oversight. Singapore’s aviation traffic, evidenced by over ~ passenger movements at Changi Airport in 2025, underscores extensive flight operations that push airlines to maintain compliance and capability in flight data systems. Furthermore, Singapore Airlines continues to commit to aircraft enhancements and retrofit programs, such as a USD ~ billion investment into its Airbus A350 retrofit program, which implies upgrades to onboard systems including flight recorders to support fleet modernization. The airline’s global network and diverse aircraft operations reinforce the need for advanced flight data capture and monitoring systems integral to compliance and safety oversight within Singapore’s aviation ecosystem.

Challenges

Cost of Installation & Certification of Advanced Recorders

The installation and certification of advanced flight recorder systems pose a substantial operational challenge for airlines and MRO providers in Singapore’s aviation market. Singapore’s aviation throughput, with ~ aircraft movements in 2025, underscores heavy utilization of aircraft where retrofits must be coordinated with operational schedules, increasing resource allocation. Although specific recorder installation costs are not detailed in government macro statistics, the Civil Aviation Authority of Singapore’s workforce data ~ aviation professionals — suggests substantial human resource investment in certification and maintenance procedures. CAAS compliance standards require exhaustive validation and integration testing for any new flight recorder installation, which extends downtime for aircraft and adds to maintenance planning complexity. The necessity for specialized engineers, compliance audits, and CAAS approved certification processes places financial and logistical strain on operators, particularly when coordinating upgrades across fleets with different aircraft types. These certification and installation complexities remain a significant challenge in scaling adoption of next generation flight recorder technologies within Singapore’s aviation operations.

Supply Chain Disruptions for High Tech Components

Modern flight recorder systems rely on advanced electronics and solid-state components, which have faced supply chain pressures in recent years. Singapore’s aviation manufacturing and maintenance ecosystem contributes notably to global MRO output, supported by more than ~ aerospace companies in the region, yet the broader global semiconductor shortages and logistics delays have impacted delivery timelines for critical avionics components. While Singapore’s macroeconomic datasets do not publish specific electronics delivery statistics, the aviation throughput reported at ~ passenger movements and increased aircraft activity in 2025 highlights the scale of operations requiring uninterrupted access to high tech parts. Supply chain constraints for memory modules, processors, and avionics connectors challenge timely production and maintenance of flight recorder systems, occasionally leading to extended aircraft grounding or reliance on legacy systems. These disruptions strain operators and MRO providers tasked with maintaining regulatory compliance while coping with global logistics delays and manufacturing bottlenecks for avionicsgrade components.

Opportunities

Integration of Predictive Safety Analytics in Flight Recorders

The integration of predictive safety analytics within flight recorder systems offers significant operational advantages for Singapore’s airlines and maintenance providers. Singapore’s air transport metrics, including ~ passenger movements and ~ aircraft movements at Changi in 2025, generate extensive flight data that can be analyzed to forecast maintenance needs and identify potential system failures before they occur. Advanced analytics built into modern flight recorders can assist airlines in optimizing aircraft utilization, reducing unscheduled downtimes, and enhancing overall safety insights. Although macroeconomic data does not report adoption figures for predictive analytics, the volume of flight data produced supports strong analytical use cases. Singapore’s sophisticated aviation infrastructure and the presence of robust MRO capabilities create an environment where predictive analytics can be integrated into flight data workflows, significantly elevating safety, reliability, and operational efficiency across airline fleets.

Growth in the Adoption of Wireless Quick Access Recorders

Wireless Quick Access Recorders (QARs) present an opportunity to streamline flight data retrieval in Singapore’s high traffic aviation environment. With ~ aircraft movements recorded at Changi Airport in 2025, airlines operating out of Singapore benefit from technology that enables rapid and automated data transfers, reducing ground time traditionally spent on manual data downloads. Although specific adoption statistics are not provided in macroeconomic sources, the lion’s share of flight operations through Singapore’s main hub suggests elevated demand for efficient data systems. Wireless QARs facilitate near realtime access to flight parameters, enabling faster maintenance decision support and operational planning. As datacentric operations become standard in aviation maintenance and safety oversight, QAR adoption aligns with Singapore’s focus on advanced operational efficiency, making it a promising growth avenue for flight recorder technology providers in the regional market.

Future Outlook

Over the next few years, the Singapore Aircraft Flight Recorder market is expected to experience significant growth, driven by technological advancements and continuous government support for aviation safety. The adoption of digital and solid-state flight recorders, alongside the integration of predictive maintenance tools and real-time data monitoring, is anticipated to lead the market forward. The growing fleet of Singapore Airlines and the expansion of air traffic across Southeast Asia will further increase the demand for advanced flight recorder systems. With regulatory bodies pushing for even stricter compliance, the market will see increased investment in upgrading existing systems and ensuring that new aircraft come equipped with cutting-edge flight data recording technology. The rise in long-haul and wide-body flights will continue to be a key driver for the market, as these aircraft types require advanced flight recorder capabilities for enhanced data capture and operational efficiency.

Major Players

- Honeywell Aerospace

- L3Harris Technologies

- Collins Aerospace

- Safran Electronics & Defense

- Thales Group

- Acron Aviation

- CurtissWright Controls

- Esterline/TE Connectivity

- Universal Avionics Systems

- Universal Flight Services

- AVIONICA Corp

- Panasonic Avionics

- Boeing Avionics Division

- Northrop Grumman

- Liebherr Aerospace

Key Target Audience

- Commercial Airlines and Airline Operators

- Aircraft Original Equipment Manufacturers

- Military and Defense Aviation Agencies

- MRO and Retrofit Service Providers

- Aviation Safety Regulatory Authorities

- Investments and Venture Capital Firms

- Aviation Data Analytics and Technology Providers

- Aerospace and Defense Contractors

Research Methodology

Step 1: Identification of Key Variables

This phase involves gathering data on the key factors that influence the aircraft flight recorder market in Singapore. Secondary research will be conducted using industry reports, government publications, and regulatory frameworks to identify the key drivers, challenges, and opportunities. The aim is to map out the regulatory and technological landscape shaping the market.

Step 2: Market Analysis and Construction

This phase will focus on analyzing historical data regarding the adoption of flight recorders in Singapore’s aviation sector. We will look at trends in fleet growth, regulatory compliance, and the technological adoption rate of advanced flight data and cockpit voice recorders.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and validated through interviews with key stakeholders in the aviation industry, including airline operators, regulatory bodies, and technology providers. Insights from these consultations will help refine the initial hypotheses and validate the market dynamics.

Step 4: Research Synthesis and Final Output

In the final phase, data from primary and secondary research will be synthesized to provide a comprehensive market analysis. This will include detailed insights on market segmentation, competitive landscape, and future trends. Interviews with industry experts and feedback from key players will ensure the accuracy and reliability of the report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Overview Genesis.

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers

Mandatory Flight Safety Recording Compliance

Expansion of Singapore Airlines Fleet & International Routes

Technological Advancements in Digital Flight Recorders - Market Challenges

Cost of Installation & Certification of Advanced Recorders

Supply Chain Disruptions for High-Tech Components - Opportunities

Integration of Predictive Safety Analytics in Flight Recorders

Growth in the Adoption of Wireless Quick Access Recorders (QARs) - Trends

Shift to Advanced Digital Flight Data Recorders

Integration with Real-Time Flight Monitoring Systems

- Market Size, 2020-2025

- By Value, 2020-2025

- By Volume, 2020-2025

- By Average Price, 2020-2025

- By Product Type, (In Value %)

Flight Data Recorder

Cockpit Voice Recorder

Combined Voice & Flight Data Recorder

Quick Access Recorder - By Aircraft Type, (In Value %)

Narrow Body Aircraft

Wide Body Aircraft

Business Jets

Turboprop Aircraft

Rotorcraft - By Component (In Value %)

Memory Modules

Electronic Control Boards

Input Devices

Power Supply Systems

Software Modules - By End-User (In Value %)

Commercial Airlines

Military Aircraft

Business Aviation

MRO & Retrofit Services - By Region (In Value %)

Singapore

Southeast Asia

Other International Markets

- Market Share of Major Players by Product Type

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strength & Weakness, Organizational Structure, Revenues, Production Plant, Capacity, Distribution Channels, Number of Dealers and Distributors)

- SWOT analysis of key players

- Pricing analysis of major players

- Porter’s Five Forces

- Detailed Profile

Honeywell Aerospace

L3Harris Technologies

Collins Aerospace

Safran Electronics & Defense

Thales Group

Acron Aviation

Curtiss-Wright Controls

Esterline/TE Connectivity

Universal Avionics Systems

Universal Flight Services

AVIONICA Corp

Panasonic Avionics

Boeing Avionics Division

Northrop Grumman

Liebherr Aerospace

- Commercial airline fleet safety and compliance requirements

- Defense aviation mission analysis and training needs

- Business aviation demand for enhanced operational monitoring

- Government special mission aircraft data recording requirements

- By Value, 2026-2035

- By Volume, 2026-2035

- By Average Price, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now