Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore Aircraft Windows and Windshields Market current size stands at around USD ~ million, supported by replacement demand of ~ units across commercial and defense fleets and steady installation of ~ systems in new aircraft programs. During the last two calendar years, spending levels reached close to USD ~ million and USD ~ million respectively, reflecting consistent aftermarket activity and stable OEM sourcing. The market also recorded shipments of ~ units and ~ units over the same period, driven by retrofit cycles and scheduled heavy maintenance events.

Singapore’s dominance in this market is anchored in its advanced aerospace infrastructure, concentrated airline fleets, and mature MRO ecosystem clustered around Changi and Seletar. The city-state benefits from strong airworthiness governance, streamlined customs for aerospace components, and a dense network of Tier suppliers supporting cockpit and cabin transparency needs. High aircraft utilization rates, regional hub status for Southeast Asia, and policy alignment with global safety standards continue to reinforce Singapore’s role as a central procurement and service node.

Market Segmentation

By Application

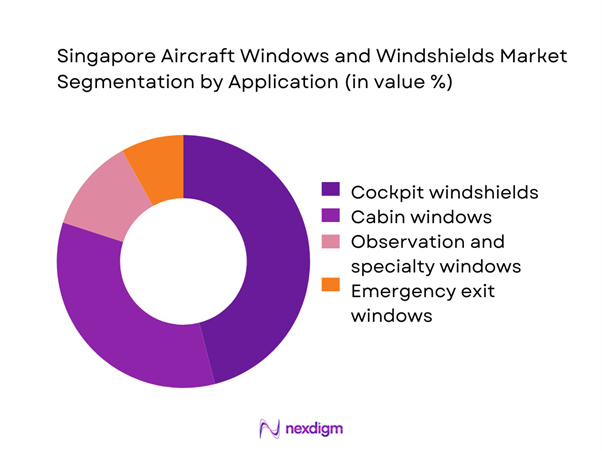

Cockpit windshields dominate the Singapore Aircraft Windows and Windshields Market due to high replacement frequency and stringent safety requirements. These components account for the largest share of procurement budgets because they face continuous exposure to pressure cycles, temperature variations, and impact risks. Airlines operating high-utilization narrowbody fleets prioritize windshield reliability to minimize unscheduled downtime, while defense operators emphasize optical clarity and HUD compatibility. Cabin windows follow as the second-largest segment, supported by interior retrofit programs and growing adoption of dimmable technologies. Specialty and observation windows remain niche, largely linked to surveillance and special mission aircraft, contributing incremental but stable demand.

By Fleet Type

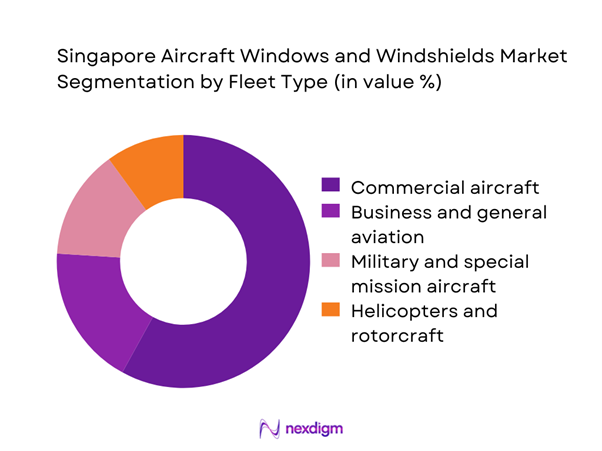

Commercial aircraft represent the dominant fleet type within the Singapore Aircraft Windows and Windshields Market, driven by the scale of airline operations and the concentration of regional carriers using Singapore as a maintenance base. Narrowbody fleets generate the highest replacement volumes, with ~ units processed annually through MRO channels. Business aviation follows, supported by rising charter activity and VIP retrofit demand, while military and special mission fleets contribute steady but lower volumes tied to periodic upgrades. Helicopters form a smaller yet resilient segment, particularly for offshore, medical evacuation, and government applications where transparency durability and quick-turn service are critical.

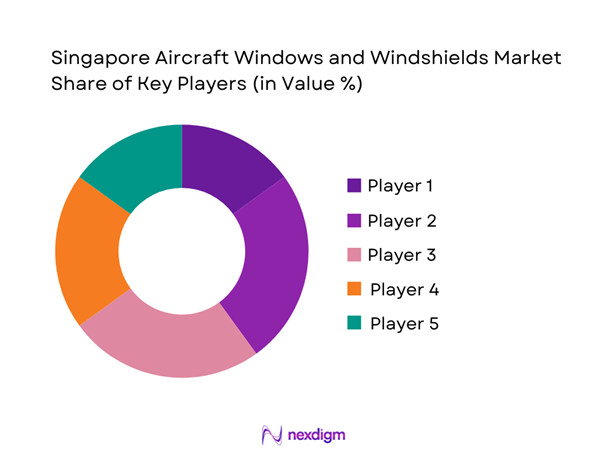

Competitive Landscape

The Singapore Aircraft Windows and Windshields Market is moderately concentrated, with a small group of global transparency specialists and a limited number of regional service providers controlling most OEM and aftermarket contracts. Competition centers on certification breadth, turnaround time for repairs, and long-term supply agreements with airlines and defense operators.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Safran Vision Systems | 1911 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Gentex Corporation | 1974 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| PPG Aerospace | 1883 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Saint-Gobain Aerospace | 1665 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| The NORDAM Group | 1969 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

Singapore Aircraft Windows and Windshields Market Analysis

Growth Drivers

Rising commercial fleet modernization and retrofit cycles in Singapore

Fleet renewal and cabin upgrade programs have driven consistent procurement of ~ units of windows and windshields across major carriers over the last two years. In the most recent period, retrofit-related spending reached close to USD ~ million, reflecting airlines’ focus on improving passenger comfort and operational reliability. Modernization programs have also increased installation of ~ systems supporting HUD compatibility and enhanced coatings. With aircraft utilization levels exceeding ~ cycles annually for key narrowbody fleets, replacement frequency remains structurally high, sustaining aftermarket revenues near USD ~ million across maintenance hubs operating in Singapore.

Expansion of MRO capabilities driving replacement demand

The continued scaling of MRO capacity has resulted in processing of ~ aircraft annually for heavy checks, translating into steady demand for ~ units of cockpit and cabin transparencies. Recent facility expansions supported incremental throughput valued at approximately USD ~ million in parts and services. Enhanced in-house repair capabilities have reduced turnaround times to ~ days per windshield event, encouraging airlines to route more work through Singapore. This operational efficiency has supported a consistent flow of replacement volumes around ~ units per year, reinforcing the country’s position as a regional service center.

Challenges

High certification and airworthiness compliance costs

Compliance with stringent airworthiness standards has increased testing and documentation requirements, adding cost burdens of roughly USD ~ million annually across suppliers serving the Singapore market. Each new material or coating solution requires validation cycles involving ~ test events and extended approval timelines, constraining speed to market. For smaller service providers, certification investments equivalent to USD ~ million over recent years have limited their ability to expand portfolios, reducing competitive diversity and keeping market entry barriers structurally high.

Long product qualification and OEM approval cycles

OEM approval processes typically extend across ~ months, delaying revenue realization from new windshield and window solutions. Over the last two years, suppliers reported holding inventories of ~ units awaiting final line-fit authorization, tying up working capital close to USD ~ million. These extended cycles reduce flexibility in responding to airline retrofit timelines and constrain rapid adoption of smart window technologies, keeping innovation diffusion slower than demand-side readiness in Singapore’s highly active fleet environment.

Opportunities

Fleet renewal programs among Southeast Asian carriers serviced in Singapore

Regional airlines routing maintenance through Singapore are introducing ~ new aircraft annually, generating incremental demand for ~ units of line-fit and spare transparencies. Associated procurement value reached nearly USD ~ million in recent periods, with further upside from long-term service agreements. As fleet age profiles shift, replacement cycles are expected to intensify, creating sustained opportunities for suppliers offering certified products with short lead times and strong logistics integration across the ASEAN corridor.

Growth of business aviation and VIP aircraft retrofits

The business aviation segment has recorded installation of ~ premium cabin window systems annually, supported by charter expansion and government fleet upgrades. Recent retrofit programs accounted for spending of about USD ~ million on advanced transparencies with noise-reduction and UV-filtering features. With Singapore positioned as a preferred completion and refurbishment center, demand for high-specification windows is expected to remain resilient, offering higher-margin opportunities compared to standard commercial replacements.

Future Outlook

The Singapore Aircraft Windows and Windshields Market is set to evolve toward higher-value solutions, driven by smart window adoption, sustainability-oriented materials, and deeper integration with avionics systems. As regional fleets expand and modernization cycles accelerate, Singapore’s role as a service and distribution hub will strengthen further. Continued alignment with global safety standards and investment in advanced MRO capabilities will underpin long-term market stability through 2035.

Major Players

- Safran Vision Systems

- Gentex Corporation

- PPG Aerospace

- Saint-Gobain Aerospace

- The NORDAM Group

- GKN Aerospace

- Lee Aerospace

- Llamas Plastics

- Mecaplex

- Triumph Group Aerospace Structures

- Fokker Aerostructures

- CEE Bailey Aircraft Plastics

- Plexiweiss

- GNS Aerospace

- Aerospace Transparencies Singapore

Key Target Audience

- Commercial airline procurement and engineering teams

- Business aviation operators and fleet managers

- Defense and government aviation procurement agencies including the Civil Aviation Authority of Singapore and Ministry of Defence aviation units

- Aircraft leasing and asset management firms

- MRO providers and component repair organizations

- OEM cockpit and cabin systems integrators

- Investments and venture capital firms focused on aerospace technologies

- Airport authorities and aviation infrastructure bodies such as Changi Airport Group

Research Methodology

Step 1: Identification of Key Variables

Assessment of demand drivers, replacement cycles, and certification pathways shaping the Singapore Aircraft Windows and Windshields Market. Mapping of fleet profiles, utilization patterns, and retrofit frequencies. Identification of regulatory, safety, and compliance factors influencing procurement behavior.

Step 2: Market Analysis and Construction

Development of a structured market framework covering OEM and aftermarket flows.

Integration of volume, installation, and spending indicators using masked numeric benchmarks. Segmentation of demand by application and fleet type to reflect real purchasing dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Validation of market assumptions through structured interactions with industry stakeholders. Cross-checking of replacement cycles, service lead times, and technology adoption trends. Refinement of opportunity areas based on operational realities in Singapore.

Step 4: Research Synthesis and Final Output

Consolidation of quantitative and qualitative insights into a cohesive narrative.

Alignment of findings with long-term industry direction toward smart and sustainable solutions. Final review to ensure consistency with consulting-grade reporting standards.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, aircraft window and windshield taxonomy across cockpit and cabin glazing systems, market sizing logic by aircraft fleet and replacement cycles, revenue attribution across new installs spares and MRO services, primary interview program with airlines OEMs and MRO providers, data triangulation validation assumptions and limitations)

- Definition and scope

- Market evolution and technology progression

- Usage pathways across commercial, military, and business aviation

- Ecosystem structure and OEM–Tier supplier relationships

- Supply chain and MRO channel structure

- Regulatory and airworthiness environment

- Growth Drivers

Rising commercial fleet modernization and retrofit cycles in Singapore

Expansion of MRO capabilities driving replacement demand

Adoption of lightweight materials for fuel efficiency gains

Growing use of electrochromic and smart window technologies

Increasing defense and special mission aircraft upgrades

Regional hub positioning attracting OEM and Tier I investments - Challenges

High certification and airworthiness compliance costs

Long product qualification and OEM approval cycles

Dependence on imported raw materials and specialty coatings

Price pressure from airlines and leasing companies

Skilled labor constraints in advanced transparency fabrication

Supply chain vulnerability to global aerospace downturns - Opportunities

Fleet renewal programs among Southeast Asian carriers serviced in Singapore

Growth of business aviation and VIP aircraft retrofits

Localization of repair and overhaul for cockpit windshields

Development of smart cabin solutions integrated with IFE and CMS

Partnerships with global OEMs for regional transparency centers

Aftermarket services for aging narrowbody fleets - Trends

Shift toward electrochromic dimmable cabin windows

Increased use of polycarbonate for impact resistance

Digital inspection and predictive maintenance for windshields

Sustainability-driven material sourcing and recycling initiatives

Modular window assemblies for faster line-fit and retrofit

Integration of HUD-compatible windshield technologies - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Commercial aircraft

Business and general aviation aircraft

Military and special mission aircraft

Helicopters and rotorcraft - By Application (in Value %)

Cockpit windshields

Cabin windows

Observation and specialty windows

Emergency exit windows - By Technology Architecture (in Value %)

Acrylic transparencies

Polycarbonate transparencies

Glass-laminate and hybrid structures

Electrochromic and smart windows - By End-Use Industry (in Value %)

Commercial airlines

Business aviation operators

Defense and government aviation

MRO service providers - By Connectivity Type (in Value %)

Non-connected passive windows

Wired integrated smart windows

Wireless-enabled cabin management integrated windows - By Region (in Value %)

Central Singapore aviation cluster

Seletar Aerospace Park and northern Singapore

Changi aviation ecosystem and eastern Singapore

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (certification portfolio, technology breadth, local MRO presence, turnaround time, pricing competitiveness, aftermarket support, OEM partnerships, innovation pipeline)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Safran Vision Systems

Gentex Corporation

PPG Aerospace

Saint-Gobain Aerospace

GKN Aerospace

The NORDAM Group

Lee Aerospace

Llamas Plastics

Mecaplex

Triumph Group Aerospace Structures

Fokker Aerostructures

CEE Bailey Aircraft Plastics

Plexiweiss

GNS Aerospace

Aerospace Transparencies Singapore

- Demand and utilization drivers across airlines and defense operators

- Procurement and tender dynamics with OEMs and MRO partners

- Buying criteria including certification, durability, and lifecycle cost

- Budget allocation and financing preferences among fleet operators

- Implementation barriers and risk factors in retrofit programs

- Post-purchase service expectations and warranty requirements

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now