Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore Aviation Manufacturing Market is valued at USD ~ billion. This market is driven by strong aviation industry growth, particularly in commercial and defense aviation. Government-backed initiatives, robust infrastructure, and increasing air traffic have supported this expansion. The demand for aircraft components, maintenance services, and the rise in military aviation contribute to its current size. Technological advancements in aircraft systems and materials also play a role in the growing value.

Singapore’s strategic location and advanced manufacturing capabilities make it a dominant player in the aviation manufacturing sector. The country benefits from its well-established aerospace infrastructure and access to regional and global markets. Key drivers of this dominance include a well-developed transport network, skilled workforce, and strong governmental support for the aerospace industry. Singapore also boasts strong collaboration between aviation manufacturers and research institutes, further enhancing its competitive position. This has positioned the country as a regional hub for aircraft and component manufacturing.

Market Segmentation

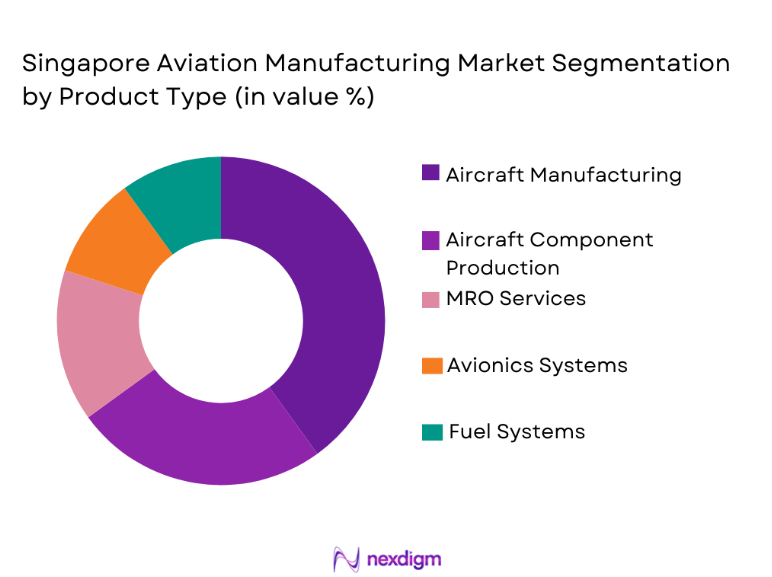

By Product Type

The Singapore Aviation Manufacturing Market is segmented by product type into aircraft manufacturing, aircraft component production, MRO services, avionics systems, and fuel systems. Recently, aircraft manufacturing has dominated the market share due to its substantial demand driven by global air traffic growth and the increasing need for new aircraft. Singapore’s well-developed infrastructure, skilled workforce, and strategic government investments in the aviation industry further support this sub-segment’s dominance. Leading companies in the region have also invested heavily in aircraft assembly lines, making this the largest market segment. Demand for high-tech, fuel-efficient, and environmentally friendly aircraft has propelled the continued growth of this sub-segment. Additionally, the rise in long-haul flights and air cargo transport has increased the need for more aircraft, reinforcing its market dominance.

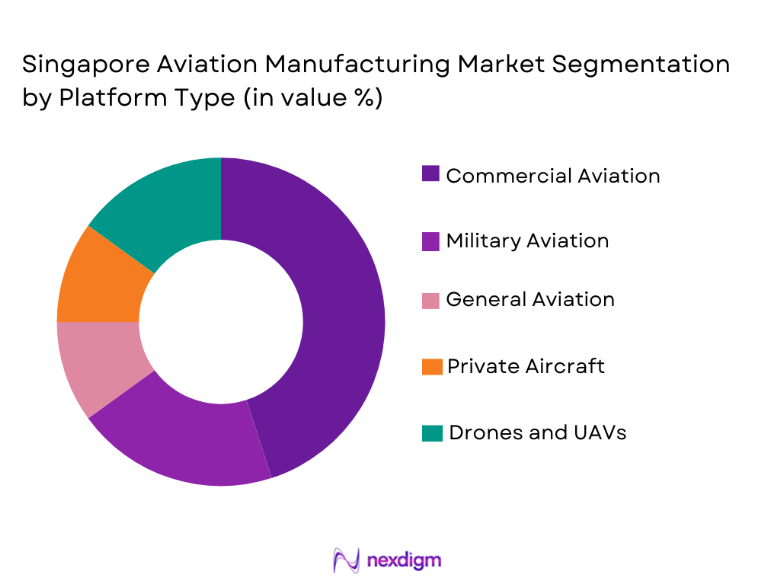

By Platform Type

The Singapore Aviation Manufacturing Market is segmented by platform type into commercial aviation, military aviation, general aviation, private aircraft, and drones and UAVs. Recently, commercial aviation has dominated the market share due to the rising demand for air travel and the continuous expansion of international flight routes. As Singapore serves as a global aviation hub with strong airline carriers, the demand for aircraft across all levels, from short to long-haul flights, continues to grow. Additionally, Singapore’s robust infrastructure and airline fleet support this sub-segment’s growth, with airlines increasingly seeking more efficient, technologically advanced aircraft. Military aviation and UAVs are also seeing a rise in demand, driven by defense spending and technological advancements. This diverse platform base ensures that the market maintains its broad growth trajectory.

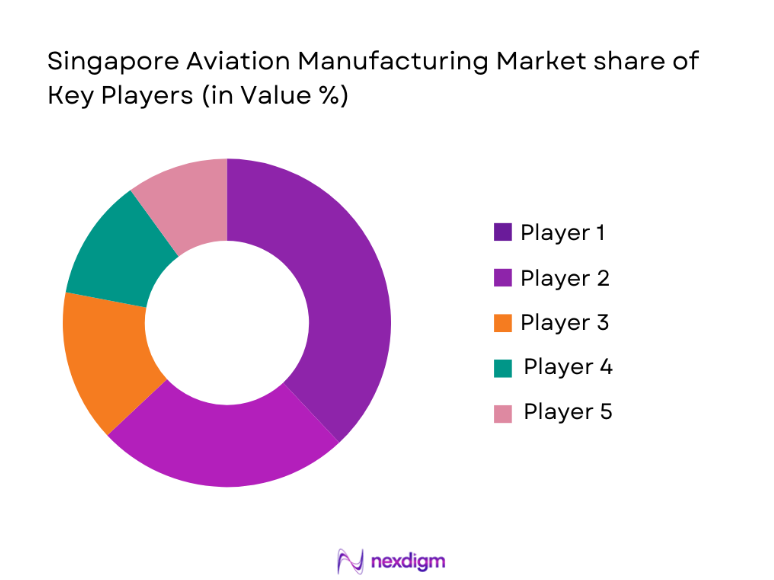

Competitive Landscape

The Singapore Aviation Manufacturing Market is characterized by a highly competitive landscape, with consolidation occurring among large industry players. Many global aerospace companies have established a presence in Singapore, attracted by its robust infrastructure, skilled workforce, and strategic location in Southeast Asia. The influence of major players, particularly in aircraft manufacturing, is significant. These companies focus on technological advancements and strategic partnerships to expand their market reach. The competition is intensified by both established firms and emerging players offering innovative solutions for commercial and military aviation manufacturing.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| ST Engineering | 1967 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Rolls-Royce Singapore | 1950 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Boeing Singapore | 1990 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Airbus Singapore | 1997 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Honeywell Aerospace | 1885 | USA | ~ | ~ | ~ | ~ | ~ |

Singapore Aviation Manufacturing Market Analysis

Growth Drivers

Government Investments in Aviation Infrastructure

The expansion of the Singapore Aviation Manufacturing Market is significantly driven by continued government investments in aviation infrastructure. Singapore’s government has long recognized the strategic importance of the aerospace industry, committing substantial resources to its growth. These investments include the development of world-class aviation hubs like Changi Airport and advanced aerospace parks, which attract international companies to set up manufacturing and maintenance facilities in the region. Furthermore, the government supports aerospace research and development, positioning Singapore as a leader in innovative aviation technologies. This not only strengthens the local aviation manufacturing sector but also attracts foreign investment and enhances export opportunities. In addition to infrastructure, the government’s policies also focus on creating a conducive business environment for aerospace companies, from tax incentives to financing support. This has accelerated the development of manufacturing capabilities and enhanced Singapore’s position as a global aviation manufacturing hub.

Technological Advancements in Aircraft Manufacturing

Another key growth driver for the Singapore Aviation Manufacturing Market is the continuous advancements in aircraft manufacturing technologies. These innovations are primarily focused on improving fuel efficiency, reducing emissions, and enhancing aircraft performance. The demand for more sustainable, high-performance aircraft is driving the need for cutting-edge technologies such as lightweight materials, improved avionics, and advanced manufacturing techniques like additive manufacturing. Singapore’s aerospace sector has increasingly embraced these technologies, positioning itself as a leader in next-generation aircraft manufacturing. The integration of these advanced technologies has led to the production of more efficient, cost-effective, and environmentally friendly aircraft. In addition, the rise of electric and hybrid aircraft further strengthens the market, as Singapore seeks to be at the forefront of these developments. Investments in Research & Development (R&D) from both private and government sectors continue to fuel technological innovation, ensuring sustained market growth.

Market Challenges

High Manufacturing Costs

The Singapore Aviation Manufacturing Market faces significant challenges related to high manufacturing costs. Aircraft manufacturing, particularly the production of advanced, high-performance aircraft, requires substantial capital investment in materials, machinery, and skilled labor. The costs of research, development, and quality assurance are also significant factors. These high production costs can lead to price pressures, especially when competitors from regions with lower labor and operational costs enter the market. This challenge is compounded by the need for constant innovation in manufacturing processes to meet the growing demand for fuel-efficient and environmentally friendly aircraft. These factors can lead to a competitive disadvantage for smaller players or companies with limited resources. Despite these challenges, Singapore’s government incentives and strong infrastructure have helped mitigate some of the financial pressures, but the high cost of manufacturing remains a key issue.

Geopolitical Risks and Supply Chain Vulnerabilities

The Singapore Aviation Manufacturing Market is also affected by geopolitical risks and supply chain vulnerabilities. As the market is heavily reliant on international suppliers for components and materials, disruptions in the global supply chain can lead to delays and increased costs. Geopolitical tensions in key aerospace production regions, such as the U.S., Europe, and China, can exacerbate these supply chain risks. Trade restrictions, tariffs, and export control regulations may also disrupt the smooth flow of essential materials and components needed for aircraft manufacturing. Additionally, the market is susceptible to fluctuations in raw material prices, particularly metals like aluminum and titanium, which are essential for aircraft production. These challenges make it crucial for manufacturers to diversify their supply chains and establish resilient procurement strategies. The geopolitical uncertainty and potential for disruptions add complexity to the operations of aviation manufacturers in Singapore.

Opportunities

Expansion into Emerging Markets

A significant opportunity for the Singapore Aviation Manufacturing Market lies in expanding into emerging markets, particularly in Southeast Asia and Africa. As global air traffic grows, there is an increasing need for new aircraft, components, and maintenance services in developing economies. Many of these regions have seen rapid economic growth, leading to higher disposable incomes and an increasing demand for air travel. Singapore’s aviation manufacturing sector, with its advanced infrastructure and expertise, is well-positioned to meet the growing demands of these regions. In addition, expanding into emerging markets presents opportunities for partnerships, joint ventures, and collaborations with local manufacturers and airlines. These partnerships can help Singaporean manufacturers secure a foothold in new markets, increase their revenue streams, and diversify their customer base. Moreover, governments in these regions are investing heavily in aviation infrastructure, creating a conducive environment for aviation manufacturing companies.

Integration of Electric and Hybrid Aircraft Technologies

The integration of electric and hybrid aircraft technologies presents a significant growth opportunity for the Singapore Aviation Manufacturing Market. With increasing concerns over environmental sustainability and the desire to reduce carbon emissions, the aviation industry is focusing on the development of electric and hybrid propulsion systems. Singapore has already made strides in positioning itself as a leader in this area, with several initiatives aimed at developing green aviation technologies. As governments around the world introduce stricter environmental regulations, the demand for sustainable aircraft will continue to rise. Singapore’s strong research and development capabilities, combined with its established aerospace manufacturing infrastructure, give it a competitive advantage in the development of electric and hybrid aircraft. This opens up a new market segment for local manufacturers, offering the potential for global leadership in the production of eco-friendly aircraft solutions.

Future Outlook

Over the next five years, the Singapore Aviation Manufacturing Market is expected to continue its growth trajectory, driven by technological advancements and strong government support. The increasing demand for commercial and defense aviation, coupled with innovations in electric and hybrid aircraft technologies, will shape the market. The government’s focus on building a green aerospace ecosystem will boost sustainability efforts in aircraft manufacturing. Furthermore, Singapore’s strategic position as a global aviation hub will continue to attract investment, enhancing the region’s competitive edge in the international market.

Major Players

- ST Engineering

- Rolls-Royce Singapore

- Boeing Singapore

- Airbus Singapore

- Honeywell Aerospace

- Safran

- UTC Aerospace Systems

- General Electric Aviation

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- Thales Group

- Collins Aerospace

- Leonardo DRS

- BAE Systems

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aircraft manufacturers

- Aerospace suppliers

- Defense contractors

- Airlines and aviation operators

- Commercial aircraft leasing firms

- Aviation technology firms

Research Methodology

Step 1: Identification of Key Variables

We identify critical market variables such as demand drivers, technological advancements, and regulatory factors.

Step 2: Market Analysis and Construction

We construct the market model using data collected from primary and secondary sources to ensure a comprehensive market landscape.

Step 3: Hypothesis Validation and Expert Consultation

We validate hypotheses through interviews with industry experts, stakeholders, and executives in the aviation sector.

Step 4: Research Synthesis and Final Output

We synthesize data and insights to create the final report, ensuring high accuracy and relevance to market participants.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Growth in global aviation demand

Technological advancements in manufacturing processes

Government investments in aviation infrastructure

Rise in defense spending in the Asia-Pacific

Increase in air traffic and aircraft fleet size - Market Challenges

High manufacturing costs

Stringent regulatory and compliance requirements

Supply chain disruptions

Rising competition from low-cost manufacturers

Environmental sustainability concerns - Market Opportunities

Expansion of defense manufacturing capabilities

Increased demand for UAV production

Collaborations with international aerospace companies - Trends

Automation in production processes

Shift towards electric and hybrid aircraft

Increased use of AI and machine learning in aviation

Sustainability efforts in aviation manufacturing

Adoption of Industry 4.0 technologies - Government Regulations & Defense Policy

Aviation safety standards

Environmental regulations in manufacturing

Government subsidies and incentives for aerospace growth - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Aircraft manufacturing

Aircraft component production

MRO services

Avionics systems

Fuel systems - By Platform Type (In Value%)

Commercial aviation

Military aviation

General aviation

Private aircraft

Drones and UAVs - By Fitment Type (In Value%)

OEM production

Aftermarket services

Integrated systems

Customized solutions

Maintenance & repair - By EndUser Segment (In Value%)

Airlines

Military forces

Private owners

Government defense

Cargo operators - By Procurement Channel (In Value%)

Direct procurement

Third-party suppliers

Online marketplaces

OEM sales

Government contracts - By Material / Technology (In Value%)

Carbon fiber composites

Titanium alloys

Aluminum alloys

Smart materials

Additive manufacturing

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Market Value, Installed Units, Average System Price, System Complexity, Procurement Channels, Technology Adoption, Regulatory Compliance, Market Share, Geographical Presence, R&D Investments)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

ST Engineering

SIA Engineering Company

Singapore Technologies Aerospace

Boeing Singapore

Rolls-Royce Singapore

Honeywell Aerospace

UTC Aerospace Systems

Airbus Singapore

Boeing

Northrop Grumman

General Electric Aviation

Lockheed Martin

Safran

Raytheon Technologies

Thales Group

- Increased demand for commercial aircraft

- Military demand for advanced systems and technologies

- Private aviation growth in Southeast Asia

- Demand for UAVs in defense and logistics sectors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now