Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Singapore Courier, Express, and Parcel market recorded a market size of approximately USD ~ billion, supported by strong cross-border trade activity and high digital commerce penetration. Government data from Enterprise Singapore and the Infocomm Media Development Authority indicates that Singapore’s advanced logistics infrastructure and digital retail ecosystem continue to generate strong parcel volumes. Rapid adoption of online shopping platforms, integrated logistics hubs, and automated parcel sorting systems are major factors strengthening parcel distribution capacity across the country.

Singapore dominates CEP activity in Southeast Asia due to its strategic geographic location and advanced logistics infrastructure centered around major logistics zones such as Changi, Jurong, and Tuas. These areas host large cargo terminals, e-commerce fulfillment centers, and regional distribution hubs that support high parcel volumes moving across Southeast Asia and global trade routes. Strong air cargo connectivity through Changi Airport and efficient port logistics further reinforce Singapore’s role as a regional parcel distribution gateway.

Market Segmentation

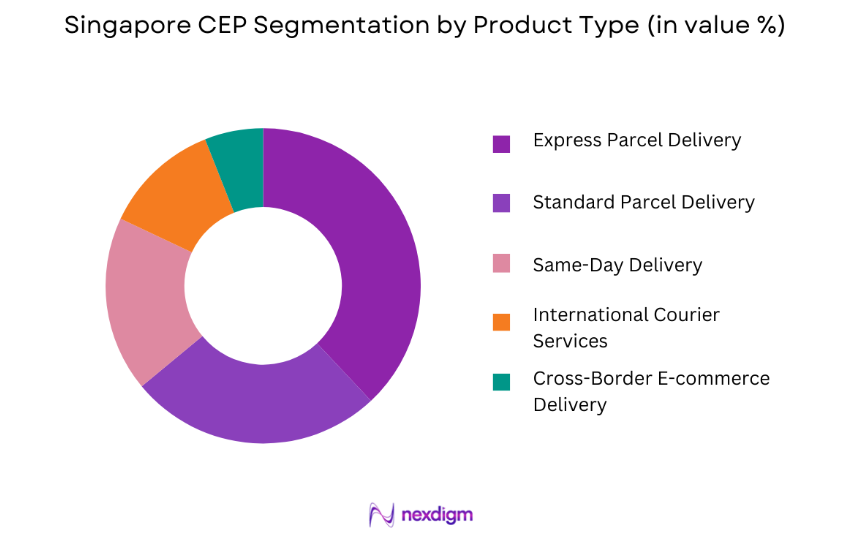

By Product Type

Singapore CEP market is segmented by product type into Express Parcel Delivery, Standard Parcel Delivery, Same-Day Delivery, International Courier Services, and Cross-Border E-commerce Delivery. Recently, Express Parcel Delivery has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Singapore’s highly urbanized geography enables rapid parcel movement, making express delivery services highly attractive for both businesses and consumers. E-commerce retailers and online marketplaces rely on express delivery services to meet customer expectations for fast order fulfillment. Logistics companies have also invested heavily in automated sorting facilities, smart lockers, and advanced parcel tracking technologies that support rapid delivery operations across the city-state. These infrastructure developments have strengthened express logistics networks and allowed courier providers to maintain fast delivery timelines across Singapore’s dense urban environment.

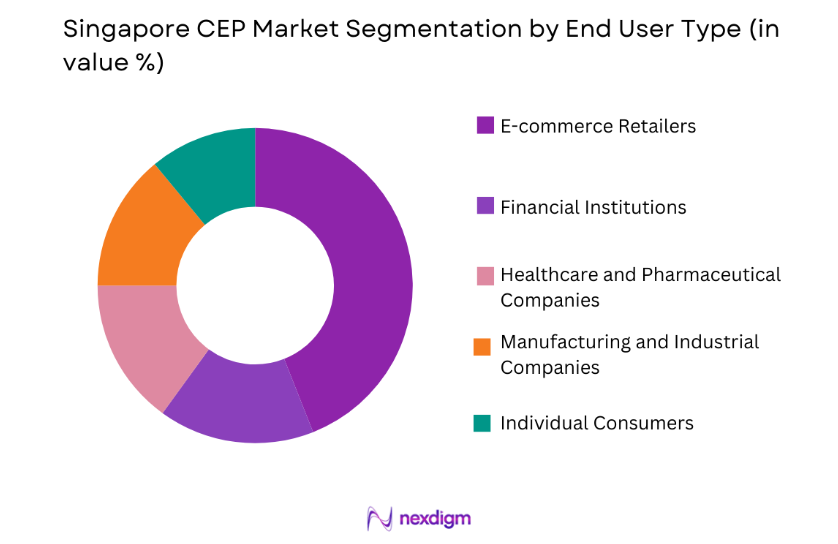

By End User

By End User

Singapore CEP market is segmented by end user into E-commerce Retailers, Financial Institutions, Healthcare and Pharmaceutical Companies, Manufacturing and Industrial Companies, and Individual Consumers. Recently, E-commerce Retailers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Singapore has one of the highest internet penetration rates globally, which has significantly accelerated digital retail activity across the country. Major online marketplaces and retail platforms generate substantial parcel shipments requiring fast and reliable delivery services. Logistics companies have responded by developing advanced last-mile delivery networks and automated parcel locker systems to support high parcel volumes. Retailers also maintain partnerships with courier providers to ensure rapid order fulfillment and efficient logistics operations across Singapore’s highly connected urban ecosystem.

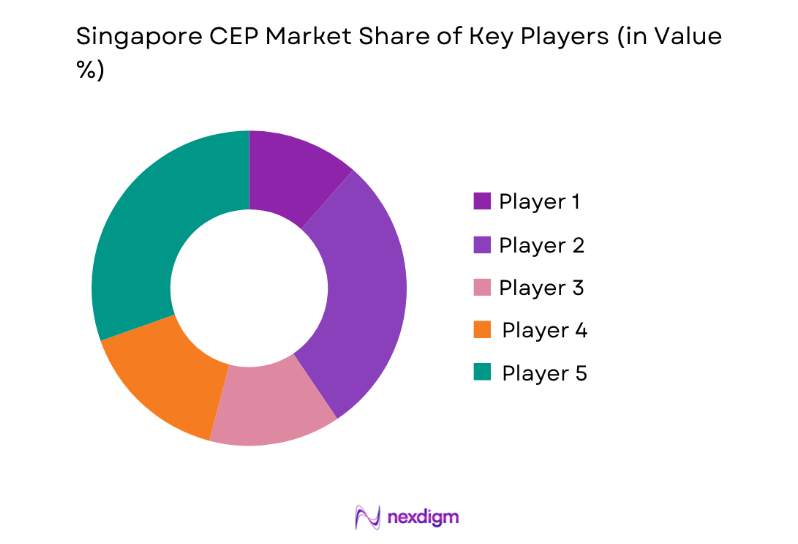

Competitive Landscape

The Singapore CEP market features a highly competitive environment characterized by strong participation from global logistics companies and regional courier providers. Major international firms operate advanced logistics hubs within Singapore due to its role as a regional trade gateway and international air cargo hub. Competitive advantage is largely driven by technology integration, cross-border logistics capability, and extensive delivery network coverage across Southeast Asia.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Logistics Hub Presence |

| DHL Express | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| SingPost | 1819 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Ninja Van | 2014 | Singapore | ~ | ~ | ~ | ~ | ~ |

Singapore CEP Market Analysis

Growth Drivers

Expansion of E-commerce Platforms and Digital Retail Logistics Demand

Singapore’s CEP market is strongly influenced by the rapid expansion of digital retail platforms that generate large parcel volumes requiring efficient logistics networks. Online marketplaces such as Lazada, Shopee, and Amazon serve millions of digital consumers and rely heavily on courier providers to ensure rapid order fulfillment. High smartphone penetration and widespread digital payment adoption have significantly increased online purchasing activity among Singaporean consumers. Logistics providers have responded by investing in automated sorting facilities and advanced parcel tracking technologies that support fast delivery operations across the city-state. Retailers depend on courier networks to maintain competitive delivery speeds and improve customer satisfaction. Singapore’s dense urban environment enables efficient parcel distribution and reduces transportation times for logistics providers. Companies are also expanding smart parcel locker networks and automated delivery hubs that improve last-mile logistics efficiency. Integration of digital commerce platforms with logistics systems further enhances shipment management and operational coordination.

Development of Regional Logistics Hub and International Trade Connectivity

Singapore’s role as a major global trade hub significantly supports the growth of the CEP market through strong cross-border logistics demand. The country’s strategic geographic location and world-class port and airport infrastructure enable efficient cargo movement across Asia and global trade routes. Changi Airport operates as a major international air cargo hub that facilitates high volumes of express shipments moving between Southeast Asia and global markets. Logistics companies utilize Singapore as a regional distribution center for parcel shipments destined for neighboring countries. Advanced customs clearance systems and streamlined trade procedures also support efficient cross-border parcel movement. Government initiatives aimed at strengthening logistics infrastructure and digital trade platforms further enhance operational efficiency for courier companies. Major logistics firms continue investing in regional distribution hubs and automated parcel handling systems within Singapore’s logistics parks.

Market Challenges

Limited Land Availability and High Logistics Infrastructure Costs

Singapore’s CEP market faces operational challenges due to limited land availability and high real estate costs associated with logistics infrastructure development. The country’s compact geography restricts the expansion of large-scale distribution centers and logistics hubs. Courier providers must operate within a limited physical footprint while managing growing parcel shipment volumes generated by digital commerce activity. High land and warehouse leasing costs increase operating expenses for logistics companies operating distribution facilities across Singapore. Logistics providers must therefore rely on advanced automation and vertical warehousing systems to maximize operational efficiency within limited space. Urban congestion and traffic regulations can also affect last-mile delivery operations within densely populated districts. Companies must optimize delivery routing and adopt smaller electric delivery vehicles to maintain efficient parcel distribution networks.

Rising Competition from Regional Logistics Providers and Delivery Platforms

The Singapore CEP market faces increasing competition from emerging logistics providers and technology-driven delivery platforms operating across Southeast Asia. Digital logistics startups and regional courier companies are entering the market with flexible delivery solutions and technology-enabled parcel distribution platforms. E-commerce marketplaces are also developing their own integrated logistics networks to improve order fulfillment efficiency. These developments intensify competition for traditional courier providers operating within Singapore. Logistics companies must invest heavily in automation, route optimization technologies, and customer service improvements to maintain competitive advantage. Competitive pricing strategies implemented by new entrants can place pressure on profit margins across the CEP sector. Courier firms must also differentiate through specialized services such as cross-border logistics and integrated supply chain management.

Opportunities

Expansion of Cross-Border E-commerce Logistics and Regional Distribution Networks

Singapore’s CEP market presents significant opportunities through the rapid expansion of cross-border e-commerce and regional logistics networks across Southeast Asia. Singapore-based logistics providers serve as key facilitators for international parcel shipments connecting Asia with global markets. Online retailers increasingly rely on courier providers to manage international order fulfillment and last-mile delivery across multiple countries. Singapore’s efficient customs clearance procedures and advanced logistics infrastructure enable fast international parcel movement. Logistics firms are investing in regional distribution hubs and cross-border fulfillment centers that allow efficient shipment consolidation and distribution. Small and medium enterprises in Singapore are also expanding into global e-commerce markets, generating additional parcel shipment demand.

Adoption of Smart Logistics Technology and Automated Delivery Infrastructure

The CEP market in Singapore offers strong opportunities through the adoption of advanced logistics technologies and automation systems that enhance operational efficiency. Courier providers are deploying artificial intelligence platforms that optimize delivery routes and forecast parcel demand patterns. Automated parcel sorting facilities equipped with robotics technology allow companies to process high shipment volumes with minimal manual intervention. Smart parcel lockers and autonomous delivery solutions are also being introduced to improve last-mile delivery efficiency in urban areas. Logistics companies are integrating digital platforms that enable real-time shipment tracking and automated order management.

Future Outlook

The Singapore CEP market is expected to experience steady expansion over the next five years as digital commerce and cross-border trade continue to grow across Southeast Asia. Investments in automated logistics hubs, smart parcel lockers, and advanced tracking technologies will significantly improve delivery efficiency and parcel handling capacity. Government initiatives supporting digital trade platforms and logistics innovation will further strengthen the country’s position as a regional logistics hub. Growing e-commerce activity and international parcel shipments will continue driving CEP demand across Singapore.

Major Players

- DHL Express

- FedEx

- UPS

- SingPost

- Ninja Van

- J&T Express

- SF Express

- Aramex

- Qxpress

- ZTO Express

- Kerry Express

- YTO Express

- Best Express

- JD Logistics

- Amazon Logistics

Key Target Audience

- E-commerce Retail Platforms

- Logistics and Supply Chain Companies

- Manufacturing and Industrial Enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail Distribution Companies

- Transportation Infrastructure Developers

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying key variables influencing the Singapore CEP market including parcel shipment volumes, digital commerce growth, cross-border logistics activity, delivery network coverage, and logistics infrastructure capacity across the country.

Step 2: Market Analysis and Construction

Extensive analysis is conducted using logistics industry databases, government trade statistics, company financial reports, and transportation infrastructure data to construct an accurate representation of market structure and operational dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, supply chain managers, and e-commerce platform operators are consulted to validate market assumptions and confirm trends affecting courier and parcel delivery networks.

Step 4: Research Synthesis and Final Output

All data collected through primary and secondary research is synthesized using structured analytical frameworks to produce a comprehensive report outlining market trends, competitive dynamics, and future opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Strong Growth of E-commerce and Cross-Border Online Retail

Advanced Logistics Infrastructure and Smart Port Ecosystem

High Demand for Fast and Reliable Urban Delivery Services - Market Challenges

High Operational and Labor Costs in Urban Logistics

Limited Urban Space for Logistics Infrastructure

Increasing Competition Among CEP Providers - Market Opportunities

Expansion of Cross-Border E-commerce Logistics Services

Adoption of Smart Parcel Lockers and Automated Delivery Solutions

Integration of AI-Based Route Optimization Systems - Trends

Increasing Use of Automated Parcel Sorting Facilities

Growth of Sustainable Delivery Fleets Using Electric Vehicles - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Courier Delivery Services

Express Parcel Delivery

Standard Parcel Delivery

Same-Day Delivery Services

International Parcel Delivery - By Platform Type (In Value%)

Road-Based Parcel Delivery Networks

Air Express Logistics Platforms

Integrated Urban Delivery Platforms

Cross-Border Parcel Logistics Platforms - By Fitment Type (In Value%)

Dedicated Courier Networks

Third-Party Logistics Parcel Services

Asset-Light Delivery Networks

Integrated E-commerce Fulfillment Services - By End User Segment (In Value%)

E-commerce and Online Retail Companies

Small and Medium Enterprises

Large Enterprises and Corporate Clients

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Parcel Handling Capacity, Technology Integration Level, Delivery Speed and Reliability, Pricing Competitiveness, Sorting Infrastructure Capacity, Cross-Border Logistics Capabilities)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

SingPost

DHL eCommerce Singapore

FedEx Express Singapore

UPS Singapore

Ninja Van

J&T Express Singapore

Qxpress

Aramex Singapore

SF Express Singapore

Janio Asia

ZTO Express Singapore

JD Logistics Singapore

Cainiao Network

Lalamove Singapore

Pickupp Singapore

- E-commerce Companies Driving High Parcel Delivery Volumes

- SMEs Leveraging Courier Networks for Regional Trade

- Large Enterprises Outsourcing Express Logistics Services

- Retailers Expanding Omnichannel Delivery Capabilities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now