Download PDF

Download PDFMarket Overview

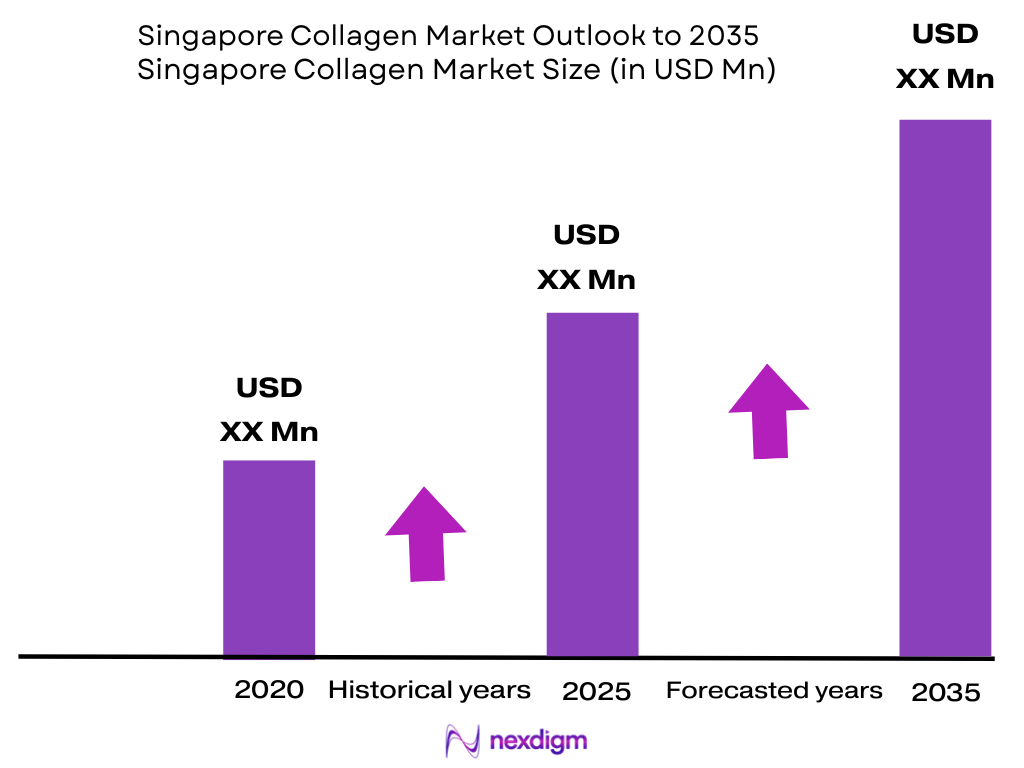

The Singapore collagen supplements market is valued at USD ~ million, based on a five-year historical analysis, and is forecast to record 3.98% CAGR from 2026 to 2034 in the available country outlook. Demand is driven by marine collagen sachets, bovine collagen powders, Japanese and Korean beauty drinks, tablets, capsules and pharmacy-led nutricosmetic purchases. Singapore’s GDP increased from USD 501.44 billion to USD 547.39 billion, supporting premium wellness consumption. Orchard, Marina Bay, CBD, Novena, Tampines, Jurong, Woodlands and major heartland malls dominate Singapore collagen demand because they combine premium beauty retail, pharmacies, aesthetic clinics, online fulfilment and higher-income wellness consumers. Singapore’s population reached nearly 6.04 million, while GDP per capita reached USD 90,674.1, supporting imported collagen powders, Japanese beauty drinks, marine sachets, gummies, tablets and active-aging supplements. Pharmacy chains and marketplaces drive demand through accessibility and product trust.

Market Segmentation

By Source

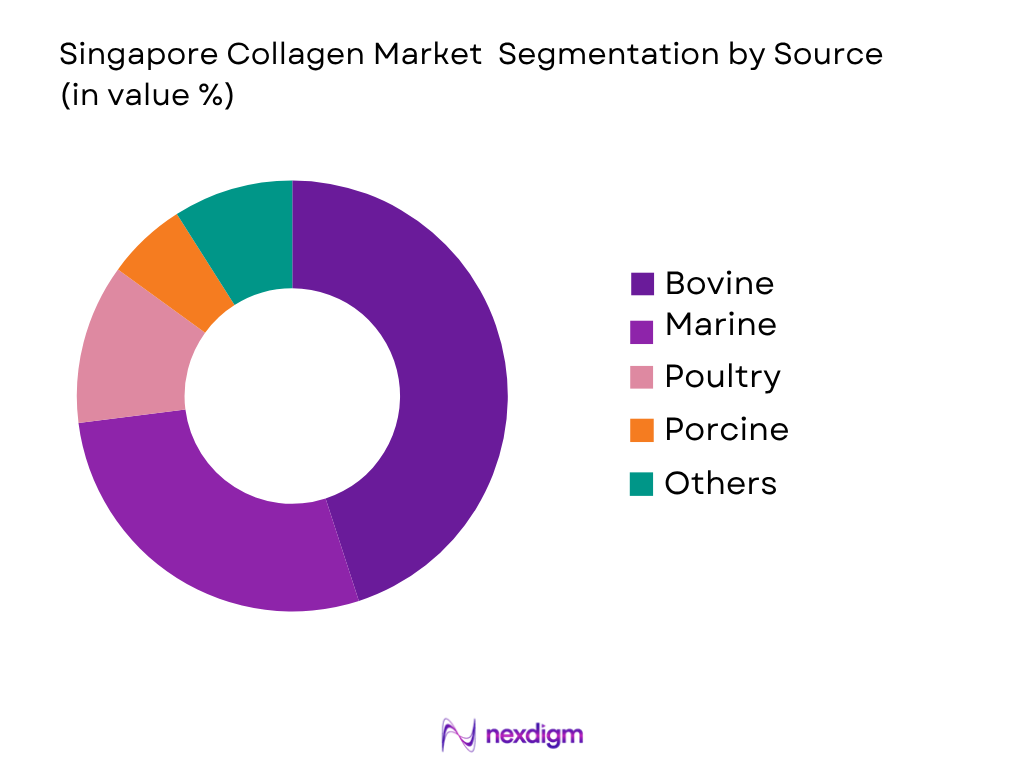

Singapore collagen market is segmented by source into bovine, marine, porcine, poultry and plant-based collagen builders. Recently, bovine collagen has a dominant market share in Singapore under source segmentation, because it is cost-efficient, scalable and widely used in powders, capsules, tablets, multi-collagen blends and sports-recovery formats. Bovine collagen provides Type I and Type III collagen, allowing brands to position products for skin, hair, nails, joints and active aging. Marine collagen is highly visible in premium beauty supplements because Singapore consumers are familiar with Japanese and Korean skin-health formats, but marine collagen usually carries a stronger premium positioning. Porcine collagen is more sensitive due to halal and dietary preferences, while poultry collagen is primarily used in Type II joint-health supplements. Country-level market intelligence identifies bovine as the leading source category in Singapore collagen supplements.

By Product Form

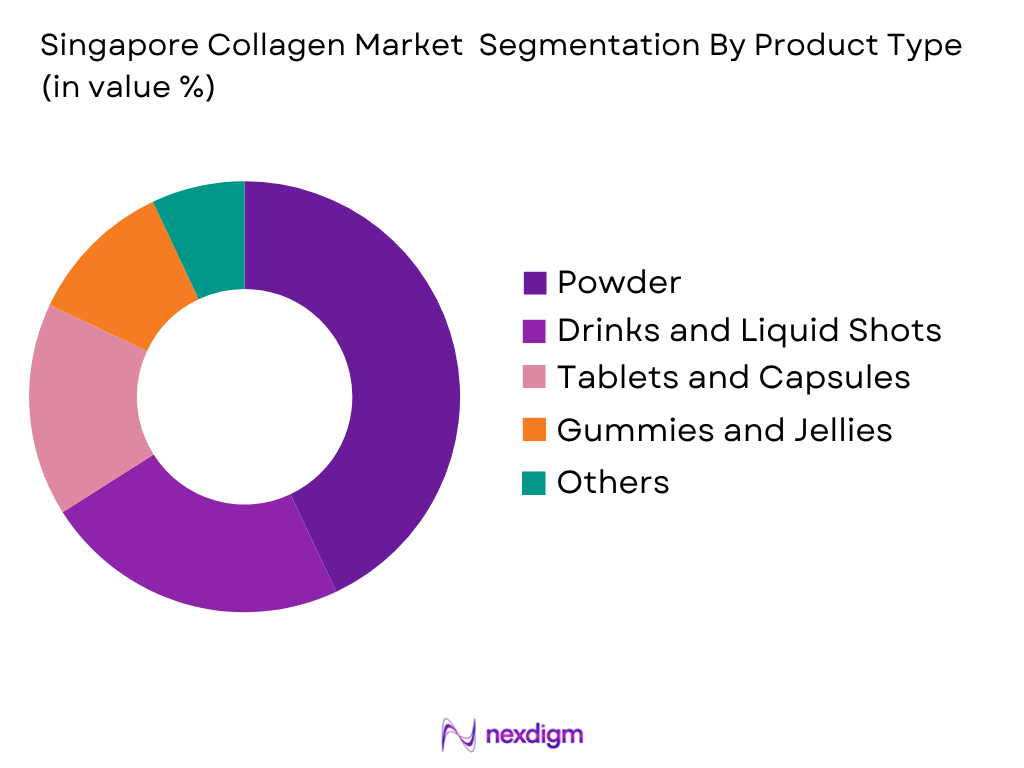

Singapore collagen market is segmented by product form into powders, drinks, tablets and capsules, gummies and jellies, and other formats. Recently, powder has a dominant market share in Singapore under product form segmentation, because it offers higher dosage flexibility, daily routine integration, mixability with coffee or water, and suitability for marine and bovine hydrolyzed collagen peptides. Powders also work well in sachets, jars and stick packs, making them convenient for office workers, active-aging consumers and beauty supplement users. Collagen drinks remain important because Japanese liquid collagen and Korean beauty beverages are familiar to Singapore consumers, but powders remain broader across beauty, joint health and sports nutrition. Global collagen supplement data indicates powder as the leading form, supporting Singapore’s premium powder-led category structure.

Competitive Landscape

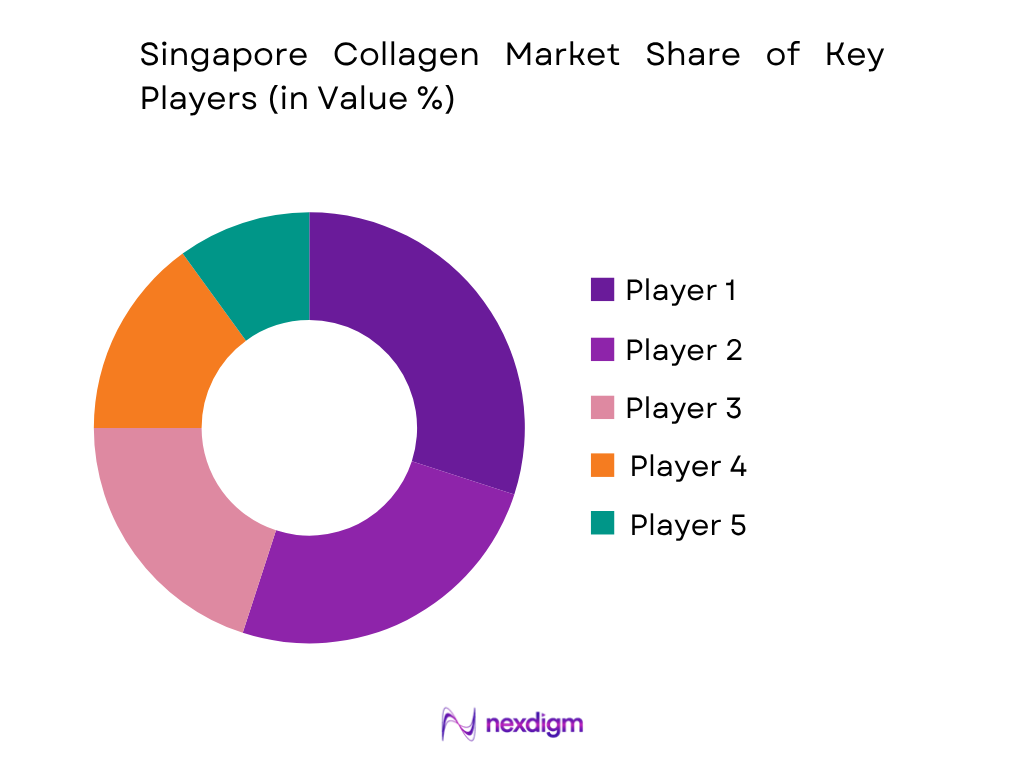

Singapore collagen market is competitive across Japanese beauty brands, Korean inner-beauty brands, local nutricosmetic companies, pharmacy supplement ranges and imported global collagen peptide players. Kinohimitsu, Shiseido, Meiji, DHC and FANCL compete strongly through liquid collagen, tablets and beauty-from-within formats, while Vital Proteins, NeoCell and Vida Glow compete through powder and marine collagen positioning. The market rewards brands with pharmacy access, HSA-compliant claims, clear source disclosure, product traceability, Japanese/Korean country-of-origin trust, e-commerce reviews and strong visibility on Watsons, Guardian, Shopee, Lazada, iHerb and Amazon Singapore. Singapore’s dietary supplements market was estimated at USD 560.9 million, giving collagen products a strong adjacent wellness category base.

| Company | Establishment Year | Headquarters | Collagen Portfolio | Main Source Focus | Application Coverage | Singapore Market Role | Distribution Model | Strategic Strength |

| Kinohimitsu | 1997 | Singapore | ~ | ~ | ~ | ~ | ~ | ~ |

| Shiseido The Collagen | 1872 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Meiji Holdings | 1917 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| DHC | 1972 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Vital Proteins / Nestlé Health Science | 2013 | Chicago, USA | ~ | ~ | ~ | ~ | ~ | ~ |

Singapore Collagen Market Analysis

Growth Drivers

Premium Consumer Economy Supporting Beauty and Active-Aging Collagen Demand

Singapore collagen market is supported by high-income consumers purchasing marine collagen sachets, bovine collagen powders, Japanese collagen drinks, Korean jelly sticks, tablets and capsules for skin hydration, hair support, nail health, joint mobility and active-aging routines. World Bank reports Singapore’s GDP per capita at USD 90,674.1 in 2024, GDP at USD 547.39 billion in 2024 and population at 6.04 million in 2024, creating a strong premium-consumption base for imported wellness products. MTI also reported full-year GDP growth of 4.4 in 2024, supporting discretionary health and beauty purchases.

Aging Population Supporting Joint, Mobility and Skin-Health Collagen Products

Singapore collagen market is driven by active-aging demand because collagen products are positioned for joint mobility, cartilage support, skin elasticity, bone support and healthy aging. Singapore’s Population in Brief reports total population increased from 5.92 million in June 2023 to 6.04 million in June 2024, while the citizen population aged 65 and above reached 19.9 in every 100 citizens in June 2024. Citizens aged 80 and above increased from 91,000 in 2015 to 145,000 in 2025, strengthening demand for Type II collagen, multi-collagen blends and pharmacy-led mobility supplements.

Market Challenges

Claims Compliance and Safety Requirements for Health Supplement Brands

Singapore collagen market faces a compliance challenge because collagen supplements are marketed for beauty, skin elasticity, joint health, recovery and active aging, but health claims must not imply medicinal treatment. HSA states that health supplements are not subject to HSA approval or licensing before import, manufacture or sale, placing responsibility on dealers to ensure product safety and quality. HSA also prohibits medicinal ingredients such as steroids and sets strict toxic heavy-metal limits. With Singapore’s population at 6.04 million and GDP per capita at USD 90,674.1 in 2024, compliant national distribution is commercially important for premium collagen brands.

Imported Product Dependency and Marketplace Authenticity Risk

Singapore collagen market faces import and authenticity challenges because Japanese, Korean, Australian, U.S. and European collagen products are commonly sold through pharmacies, beauty retailers and online marketplaces. This matters for marine collagen sachets, beauty drinks, jelly sticks, bovine powders and tablets where consumers check source, batch, distributor and country-of-origin cues. World Bank reports mobile cellular subscriptions at 171 per 100 people in 2024, while internet use reached 94.38 in every 100 people in 2024, widening marketplace access but also increasing exposure to cross-border sellers and parallel imports.

Market Opportunities

Pharmacy and Omnichannel Retail Expansion for Verified Collagen Products

Singapore collagen market has an opportunity in verified pharmacy, health-beauty and omnichannel distribution because consumers buying collagen for beauty, joint health and active aging value product authenticity, claims discipline and source disclosure. SingStat reported estimated total retail sales value of S$4.0 billion in September 2024, with online retail sales contributing 13.8 in every 100 retail-sales dollars. This supports collagen products sold through Watsons, Guardian, Shopee, Lazada, Amazon Singapore and official brand websites. World Bank also reports GDP per capita at USD 90,674.1 in 2024, supporting premium repeat purchases.

Tourism and Premium Beauty Retail Supporting Marine Collagen Formats

Singapore collagen market has an opportunity in premium marine collagen sachets, Japanese liquid collagen, Korean jelly sticks and beauty shots because tourism, airport retail and Orchard-area beauty retail expose consumers to imported nutricosmetic formats. Singapore Tourism Board reported 16.5 million visitor arrivals in 2024, with tourism receipts expected near the upper end of S$27.5 billion to S$29.0 billion. Visitor markets such as Mainland China, Indonesia and India support beauty retail discovery, while Singapore’s GDP of USD 547.39 billion in 2024 provides a strong resident premium-consumption base for collagen products.

Future Outlook

Singapore collagen market is expected to grow steadily over the next decade, supported by premium beauty supplementation, active-aging nutrition, medical aesthetic influence, pharmacy retail trust and high e-commerce penetration. The available Singapore country outlook places collagen supplements at USD 21.2 million in 2025 and estimates the category to reach USD 30.06 million by 2034. For the requested 2026–2035 period, Singapore-specific public data is available through 2034, with 3.98% CAGR from 2026 to 2034. For the additional 2035 endpoint, the report should treat the same growth track as the closest public benchmark, subject to validation through SKU-level and distributor-level primary research.

Future demand will be concentrated in marine collagen sachets, bovine collagen powders, Japanese liquid collagen, Korean jelly sticks, collagen tablets, gummies, Type II joint-health capsules and active-aging blends. Premium formulations with vitamin C, hyaluronic acid, elastin, ceramides, zinc, biotin, glutathione and coenzyme Q10 will remain important because consumers increasingly compare collagen products by ingredient stack, source and format. Singapore’s future collagen market will also be shaped by regulatory discipline. Health supplements are not subject to pre-market approval in Singapore, but dealers must ensure product safety, quality and claims compliance. Brands that use substantiated functional claims, avoid medicinal claims, disclose allergens, provide certificates of analysis and maintain traceable official distribution will be better positioned across pharmacies, marketplaces and aesthetic-clinic-linked wellness channels.

Major Players

- Kinohimitsu

- Shiseido The Collagen

- Meiji Holdings

- DHC

- FANCL

- AFC Japan

- Holistic Way

- LAC

- 21st Century HealthCare

- Nature’s Way

- Swisse

- Vital Proteins / Nestlé Health Science

- NeoCell

- Vida Glow

- InnerB / CJ Wellcare

Key Target Audience

- Collagen supplement importers

- Dietary supplement and nutraceutical brands

- Pharmacy and health-beauty retail chains

- Beauty and nutricosmetic brands

- E-commerce and marketplace wellness sellers

- Medical aesthetic and dermatology clinic groups

- Investments and venture capitalist firms

- Government and regulatory bodies, Health Sciences Authority, Singapore Food Agency, Health Promotion Board, Enterprise Singapore

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of Singapore collagen market, covering imported supplement brands, pharmacies, beauty retailers, e-commerce platforms, health supplement distributors, aesthetic clinics, functional food brands and regulators. The primary objective is to define critical variables such as source, form factor, product type, channel, claim positioning, ingredient stack and consumer use case.

Step 2: Market Analysis and Construction

In this phase, historical and current data is compiled across collagen supplement revenue, imported product activity, pharmacy listings, marketplace SKUs, Japanese and Korean beauty formats, active-aging products and source mix. The analysis evaluates marine, bovine, porcine, poultry and plant-based collagen-builder products across beauty, joint health, sports nutrition, functional foods and medical-aesthetic adjacent uses.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with supplement importers, pharmacy buyers, beauty retailers, e-commerce sellers, aesthetic clinics, dermatology practices and functional food manufacturers. These consultations help validate assumptions around bovine source leadership, marine premiumization, powder-format dominance, Japanese/Korean influence, pharmacy trust and marketplace competition.

Step 4: Research Synthesis and Final Output

The final phase combines top-down macroeconomic and category indicators with bottom-up SKU, channel and company-level checks. This approach validates Singapore collagen market size, segmentation, competitive structure, regulatory risk, demand outlook and growth opportunities for manufacturers, importers, retailers, investors and consumer-health companies.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Validation, Bottom-Up Validation, Import Mapping, SKU Benchmarking, Primary Interviews, Regulatory Review, Competitive Mapping, Forecast Model, Limitations)

- Definition and Scope

- Market Genesis and Evolution

- Timeline of Major Players

- Business Cycle and Beauty Supplement Seasonality

- Growth Drivers (Premium Beauty Consumption, Japanese and Korean Inner Beauty Influence, Active Aging Demand, E-Commerce Penetration, Pharmacy Channel Trust, Medical Aesthetics Growth, Functional Food Innovation)

- Market Challenges (Imported Product Dependency, Claim Substantiation, Non-Pre-Market Approval Perception, Grey Imports, Counterfeit Risk, Source Disclosure, Fish Allergen Risk)

- Market Opportunities (Premium Marine Collagen, Collagen Drinks, Japanese and Korean Inspired Beauty Jellies, Active Aging Joint Formulas, Medical Aesthetic Bundles, Halal-Certified Collagen, Functional Beverages, Pet Collagen)

- Market Trends (Marine Collagen Sachets, Japanese Liquid Collagen, Korean Jelly Sticks, Collagen Coffee, Hyaluronic Acid Pairing, QR Authentication, Clean Label, TikTok Shop Education)

- SWOT Analysis

- Porter’s Five Forces

- PESTLE Analysis

- By Value (2020-2025)

- By Volume (2020-2025)

- By Average Selling Price (2020-2025)

- By Source (In Value %)

Marine Collagen

Bovine Collagen

Porcine Collagen

Poultry Collagen

Eggshell Membrane Collagen - By Product Type (In Value %)

Hydrolyzed Collagen Peptides

Gelatin

Native Collagen

Undenatured Type II Collagen

Collagen Beauty Foods

Multi-Collagen Blends - By Distribution Channel (In Value %)

Pharmacies and Drugstores

Health and Beauty Retailers

E-Commerce Marketplaces

Supermarkets and Hypermarkets

Direct-to-Consumer - By Consumer Cluster (In Value %)

Central Business District and Marina Bay

Orchard and Premium Retail Belt

Heartland Residential Towns

Jurong and Western Cluster

Tampines and Eastern Cluster

Woodlands and Northern Cluster

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (Collagen Source Portfolio, Product Format Portfolio, Country-of-Origin Positioning, HSA Claims Compliance Readiness, Pharmacy and E-Commerce Reach, QR Authentication and Traceability, Ingredient Stacking Capability, Influencer and Clinic Partnership Strength)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Kinohimitsu

Shiseido The Collagen

Meiji Holdings

DHC

FANCL

AFC Japan

Holistic Way

LAC

21st Century HealthCare

Nature’s Way

Swisse

Vital Proteins / Nestlé Health Science

NeoCell

Vida Glow

InnerB / CJ Wellcare

- Supplement Brand and Importer Demand

- Beauty and Nutricosmetic Brand Demand

- Pharmacy and Drugstore Buyer Demand

- E-Commerce Seller Demand

- Medical Aesthetic Clinic Buyer Demand

- By Value (2026-2035)

- By Volume (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now