Download PDF

Download PDFMarket Overview

The Singapore Dairy Alternatives Market is supported by increasing consumer preference for plant-based nutrition and rising awareness regarding lactose intolerance and sustainable food consumption. The market generated nearly USD ~ million in retail sales, while plant-based milk products accounted for the majority of category consumption across supermarkets, cafés, and online retail channels. Soy milk, oat milk, and almond milk continue to dominate retail shelves due to broader product availability and innovation in barista-style, flavored, and fortified formulations. Increasing health consciousness and expansion of premium café culture continue to strengthen dairy alternative penetration across urban consumer groups.

Singapore’s Central Region dominates the Singapore Dairy Alternatives Market due to its concentration of premium supermarkets, specialty cafés, affluent households, and health-conscious consumers. Areas such as Orchard, Marina Bay, and the Central Business District remain major consumption hubs because of strong café density and high adoption of oat milk beverages across premium coffee chains. Singapore also benefits from strong import connectivity with Australia, Europe, and the United States for plant-based beverage sourcing. Expanding food innovation initiatives and sustainability-focused consumption trends are further strengthening dairy alternatives demand across retail and foodservice channels.

Market Segmentation

By Product Type

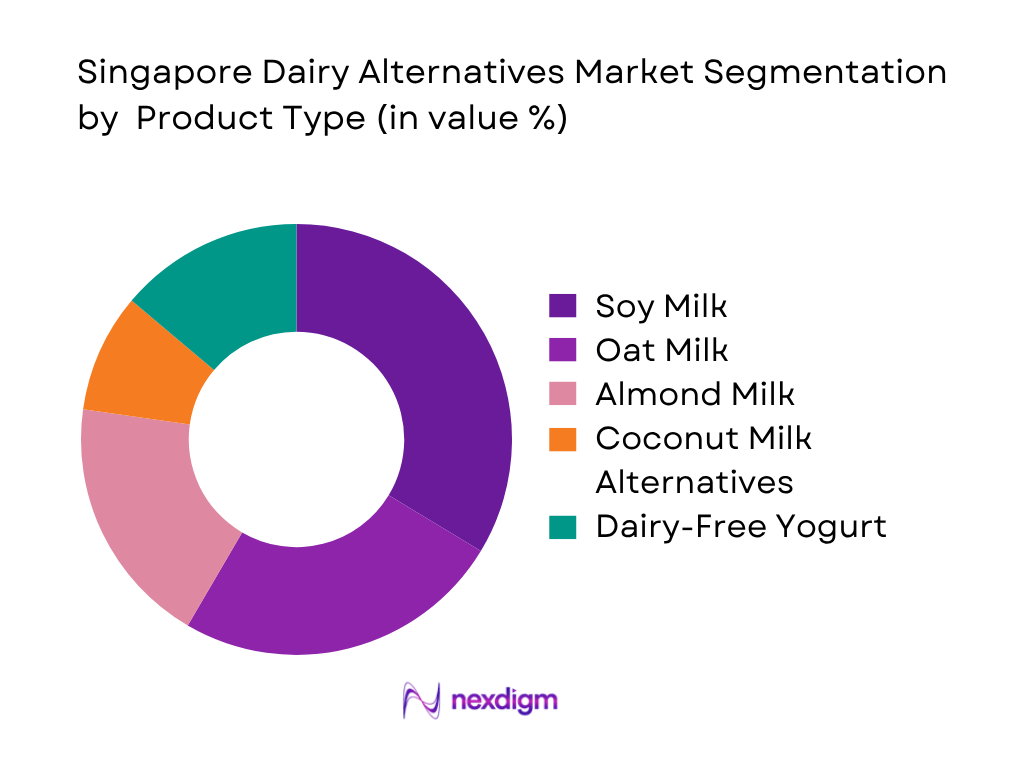

The Singapore Dairy Alternatives Market is segmented by product type into soy milk, oat milk, almond milk, coconut milk alternatives, rice milk, pea protein milk, dairy-free yogurt, dairy-free cheese, and dairy-free ice cream. Soy milk dominates the Singapore Dairy Alternatives Market under the product type segmentation due to its strong cultural familiarity, affordability, and extensive availability across supermarkets, convenience stores, and traditional beverage outlets. Consumers perceive soy milk as a nutritionally balanced and protein-rich dairy substitute, supporting higher household penetration across multiple age groups. The category also benefits from long-established consumption patterns across Asian diets and widespread integration into ready-to-drink formats. Oat milk is witnessing rapid expansion due to increasing café adoption and premium positioning; however, soy milk continues to lead because of stronger consumer familiarity, lower retail pricing, and broader retail accessibility throughout Singapore.

By Distribution Channel

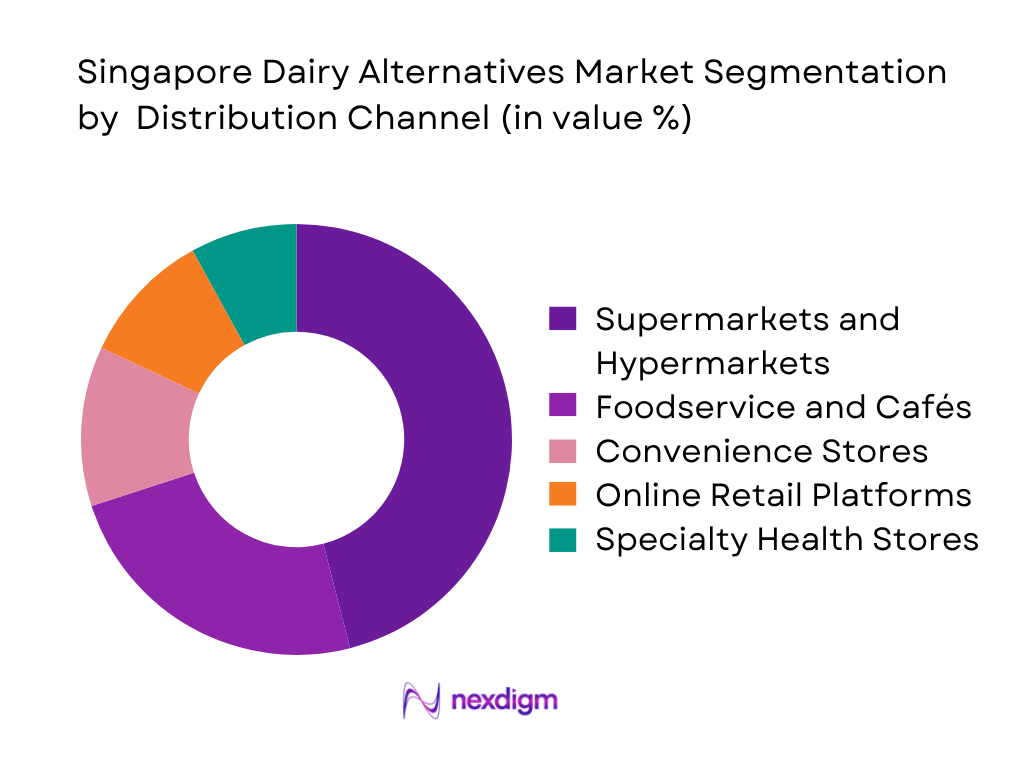

The Singapore Dairy Alternatives Market is segmented by distribution channel into supermarkets and hypermarkets, convenience stores, specialty health stores, online retail platforms, foodservice and cafés, and institutional sales. Supermarkets and hypermarkets dominate the Singapore Dairy Alternatives Market because they provide wider product assortments, premium shelf visibility, and greater accessibility to imported plant-based beverage brands. Retail chains have expanded dedicated plant-based food sections to address increasing consumer demand for dairy-free products and functional beverages. These stores offer consumers access to multiple packaging sizes, promotional campaigns, and premium imported dairy alternatives, supporting higher purchase frequency. The dominance of supermarkets is also supported by Singapore’s advanced cold-chain infrastructure and strong organized retail ecosystem. While online retail platforms continue gaining traction among younger consumers through convenience-based shopping and subscription grocery services, physical retail channels remain dominant due to stronger consumer preference for evaluating nutritional labels and product freshness before purchase.

Competitive Landscape

The Singapore Dairy Alternatives Market is moderately consolidated, with international plant-based beverage manufacturers and regional dairy alternative companies competing across retail and foodservice channels. Market participants are strengthening their positioning through product innovation, protein fortification, sustainability initiatives, and café partnerships. Increasing demand for premium oat milk and functional dairy alternatives is encouraging manufacturers to introduce barista-style formulations, sugar-free variants, and clean-label products. The market is also witnessing rising competition from emerging regional brands focused on sustainable sourcing and localized flavor innovation.

| Company | Establishment Year | Headquarters | Key Product Focus | Distribution Strength | Manufacturing Capability | Sustainability Initiatives | Foodservice Presence | Innovation Focus |

| Oatly | 1994 | Malmö, Sweden | ~ | ~ | ~ | ~ | ~ | ~ |

| Vitasoy | 1940 | Hong Kong | ~ | ~ | ~ | ~ | ~ | ~ |

| Oatside | 2020 | Singapore | ~ | ~ | ~ | ~ | ~ | ~ |

| Califia Farms | 2010 | California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Danone | 1919 | Paris, France | ~ | ~ | ~ | ~ | ~ | ~ |

Singapore Dairy Alternatives Market Analysis

Growth Drivers

Rising Lactose Intolerance Population

The increasing prevalence of lactose intolerance across Asian populations is significantly supporting demand for dairy alternatives in Singapore. Healthcare institutions in Singapore have highlighted that lactose malabsorption affects a substantial share of Asian consumers, increasing preference for soy, oat, and almond-based beverages. Singapore’s resident population exceeded 4 million in 2024, strengthening the consumer base for lactose-free and digestive-health-oriented products. Rising healthcare expenditure and increasing nutritional awareness are encouraging consumers to shift toward plant-based diets and dairy-free nutrition. Furthermore, higher urbanization levels and growing preventive healthcare spending continue to support long-term demand for plant-based dairy substitutes across retail and foodservice channels.

Increasing Vegan and Flexitarian Adoption

The growing adoption of vegan and flexitarian diets is accelerating dairy alternatives consumption across Singapore. Rising disposable income levels and premium food spending are supporting demand for wellness-oriented and environmentally sustainable food products. Singapore’s food innovation ecosystem and sustainability-focused food security initiatives continue encouraging adoption of plant-based nutrition categories. In addition, the country’s strong café culture and international foodservice presence are increasing availability of plant-based milk products across coffee chains, restaurants, and quick-service outlets. Expanding awareness regarding climate-conscious consumption and healthier dietary patterns among younger urban consumers is also contributing to stronger adoption of oat milk, almond milk, and protein-enriched dairy alternatives.

Market Challenges

High Retail Pricing Compared to Conventional Dairy

High retail pricing remains a major challenge affecting dairy alternatives adoption in Singapore. The country imports more than 90% of its food supply, increasing dependency on imported raw materials and finished plant-based beverages. Logistics costs, import duties, cold-chain requirements, and premium retail shelf positioning continue to elevate product prices compared to conventional dairy products. Inflationary pressure across packaged food categories and rising operational costs within premium retail locations also contribute to higher shelf prices for oat milk, almond milk, and specialty dairy alternatives. These pricing differences can limit penetration among price-sensitive consumers despite increasing awareness regarding plant-based nutrition and sustainability-focused consumption habits.

Dependence on Imported Raw Materials

Singapore’s dairy alternatives market remains highly dependent on imported oats, almonds, soybeans, and specialty ingredients because of limited domestic agricultural production capacity. The country has minimal agricultural land availability, restricting local cultivation of plant-based beverage ingredients and increasing reliance on international sourcing markets. Supply chain disruptions, global shipping volatility, and fluctuations in agricultural commodity availability continue affecting ingredient sourcing consistency. Dependence on imports also exposes manufacturers and retailers to currency fluctuations and geopolitical uncertainties impacting food trade routes. These factors create operational complexity for dairy alternative brands seeking stable supply chains and cost-efficient sourcing strategies within Singapore’s premium food retail ecosystem.

Market Opportunities

Expansion of Barista and Café Partnerships

Singapore’s expanding specialty café ecosystem provides strong opportunities for dairy alternative manufacturers through barista partnerships and premium coffee integration. The country’s high urban density and increasing café penetration are supporting greater adoption of oat milk and almond milk across foodservice menus. Specialty coffee operators are increasingly offering plant-based milk customization options to address evolving consumer dietary preferences and premium beverage trends. Singapore’s tourism and hospitality sectors further support café expansion and visibility for dairy-free beverages across airports, hotels, and commercial districts. Strong café culture and premium coffee consumption patterns continue creating favorable conditions for growth in barista-style dairy alternatives and specialty beverage formulations.

Development of High-Protein Dairy Alternatives

Increasing consumer focus on fitness, wellness, and protein consumption is creating opportunities for high-protein dairy alternatives in Singapore. Rising participation in fitness activities and preventive healthcare adoption are encouraging demand for functional beverages with enhanced nutritional profiles. Protein-fortified oat milk, soy milk, and pea-protein beverages are gaining attention among younger professionals, gym-going consumers, and aging populations seeking healthier dietary substitutes. Manufacturers are expanding innovation in functional dairy alternatives through protein enrichment, calcium fortification, and reduced sugar formulations. Growing health consciousness and premium nutrition spending continue supporting demand for plant-based beverages positioned around muscle maintenance, wellness, and active lifestyle consumption.

Future Outlook

The Singapore Dairy Alternatives Market is expected to witness sustained growth over the coming years due to increasing consumer preference for plant-based nutrition, rising lactose intolerance awareness, and growing sustainability-focused consumption behavior. Expansion of premium café culture and increasing adoption of flexitarian diets are expected to strengthen long-term demand for oat milk, soy milk, and protein-enriched dairy alternatives. Manufacturers are expected to focus heavily on clean-label ingredients, functional beverage fortification, and sugar-free product innovation to attract health-conscious consumers. Increasing integration of plant-based beverages into retail and foodservice channels is likely to improve consumer accessibility and product penetration across Singapore. Technological advancements in plant-protein processing and sustainable packaging solutions are also expected to strengthen future market expansion.

Major Players

- Oatly

- Alpro

- Vitasoy

- Oatside

- Minor Figures

- Califia Farms

- Silk

- Pacific Foods

- Sanitarium

- So Good

- Pureharvest

- Nestlé

- Danone

- F&N Magnolia

- Happy Happy Soy Boy

Key Target Audience

- Plant-Based Beverage Manufacturers

- Dairy-Free Yogurt and Cheese Producers

- Retail Supermarket Chains

- Foodservice and Café Operators

- Ingredient and Plant Protein Suppliers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Packaging and Sustainable Material Providers

Research Methodology

Step 1: Identification of Key Variables

The initial stage involved identifying critical variables influencing the Singapore Dairy Alternatives Market, including consumer dietary trends, lactose intolerance prevalence, retail penetration, café adoption, and product innovation. Extensive secondary research was conducted using government publications, trade statistics, food industry databases, and company disclosures to understand market dynamics and stakeholder ecosystems.

Step 2: Market Analysis and Construction

Historical market analysis was conducted using retail sales data, import-export statistics, product launch trends, and foodservice consumption patterns related to dairy alternatives. Market estimations were derived using bottom-up calculations based on product categories, retail channel performance, and consumption analysis across Singapore’s organized retail ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary findings were validated through interviews with dairy alternative manufacturers, distributors, retail category managers, café operators, and foodservice participants. These consultations provided insights regarding pricing trends, shelf expansion strategies, consumer preferences, and product innovation pipelines within the Singapore Dairy Alternatives Market.

Step 4: Research Synthesis and Final Output

The final stage involved consolidating quantitative and qualitative findings to generate a comprehensive assessment of the Singapore Dairy Alternatives Market. Cross-validation was conducted using trade data, manufacturer disclosures, and retail intelligence statistics to ensure consistency and reliability of market estimates, segmentation analysis, and future growth projections.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Research Framework, Bottom-Up Market Estimation, Top-Down Validation, Consumption Mapping, Retail Audit Analysis, Import Dependency Assessment, Primary Interviews with Manufacturers and Retailers, Forecasting Model, Limitations and Assumptions)

- Definition and Scope

- Evolution of Plant-Based Dairy Consumption in Singapore

- Industry Ecosystem and Stakeholder Mapping

- Supply Chain and Value Chain Analysis

- Raw Material Procurement Landscape

- Growth Drivers

Rising Lactose Intolerance Population

Increasing Vegan and Flexitarian Adoption

Expansion of Functional and Fortified Dairy Alternatives

Rapid Growth of Café and Coffee Chains Using Plant-Based Milk

Growth in Sustainable Food Consumption - Market Challenges

High Retail Pricing Compared to Conventional Dairy

Dependence on Imported Raw Materials

Taste and Texture Acceptance Barriers

Limited Local Manufacturing Capacity - Market Opportunities

Expansion of Barista and Café Partnerships

Development of High-Protein Dairy Alternatives

Growth in Sustainable Packaging Solutions

Expansion of Functional and Protein-Enriched Plant Beverages - Market Trends

Oat Milk Premiumization

Barista-Style Plant Milk Innovation

Sugar-Free and Organic Product Launches

Sustainable Packaging Adoption

Functional Beverage Fortification - Government Regulations

Singapore Food Agency Labeling Guidelines

Import and Food Safety Compliance Standards

Nutritional Fortification Standards

Packaging Sustainability Regulations - Porter’s Five Forces Analysis

- PESTLE Analysis

- Pricing Analysis

- Competition Ecosystem

- By Value, 2020-2025

- By Volume, 2020-2025

- By Average Selling Price, 2020-2025

- By Per Capita Consumption, 2020-2025

- By Product Type (in Value %)

Soy Milk

Oat Milk

Almond Milk

Coconut Milk Alternatives

Rice Milk - By Source Type (in Value %)

Protein Content

Raw Material Availability

Processing Efficiency

Nutritional Profile - By Distribution Channel (in Value %)

Shelf Share

Store Penetration

Online Conversion Rate

Basket Size

Supermarkets and Hypermarkets - By Consumer Demographics (in Value %)

Age Group Consumption

Lactose Intolerance Prevalence

Income-Based Spending

Health and Wellness Adoption

Vegan Consumers - By Packaging Type (in Value %)

Shelf Life

Recyclability Rate

Packaging Cost

Retail Visibility

Cartons - By Region (in Value %)

Central Region

East Region

North Region

North-East Region

West Region

- Market Share Analysis of Major Players on the Basis of Revenue and Volume

- Cross Comparison Parameters (Company Overview, Product Portfolio Breadth, Plant-Based Milk SKU Count, Fortification Strategy, Distribution Reach, Retail Shelf Presence, Manufacturing Capability, Sustainability Commitments, Ingredient Sourcing Strategy, Café Partnerships, Online Penetration, Pricing Positioning, Innovation Pipeline, Packaging Innovation, Strategic Collaborations, Revenue Performance)

- Competitive Benchmarking Matrix

- SWOT Analysis of Major Players

- Pricing Analysis by Product Category and SKU

- Detailed Profiles of Major Companies

Oatly

Alpro

Vitasoy

Oatside

Minor Figures

Califia Farms

Silk

Pacific Foods

Sanitarium

So Good

Pureharvest

Nestlé

Danone

F&N Magnolia

Happy Happy Soy Boy

- Consumption Frequency Analysis

- Consumer Spending and Basket Analysis

- Brand Loyalty and Switching Behavior

- Purchase Decision Parameters

- Health and Wellness Preference Mapping

- By Value, 2026-2030

- By Volume, 2026-2030

- By Average Selling Price, 2026-2030

- By Per Capita Consumption, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now