Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore Diagnostic Labs Market demonstrates strong expansion supported by advanced healthcare infrastructure, high diagnostic testing demand, and government investment in biomedical sciences. Based on a recent historical assessment, the Singapore diagnostic laboratories sector generated approximately USD ~ billion, supported by increasing chronic disease screening, preventive healthcare adoption, and strong public healthcare spending reported by the Ministry of Health Singapore and healthcare industry financial disclosures.

Singapore’s diagnostic laboratory ecosystem is concentrated around advanced healthcare clusters such as Singapore General Hospital campus, the Novena Health City medical district, and the Bio polis biomedical research hub. These locations dominate due to integrated hospital networks, biotechnology companies, and research institutions operating in close proximity. Strong laboratory automation capabilities, high clinical testing standards, and strategic investments in genomic medicine programs further strengthen the dominance of these healthcare innovation districts.

Market Segmentation

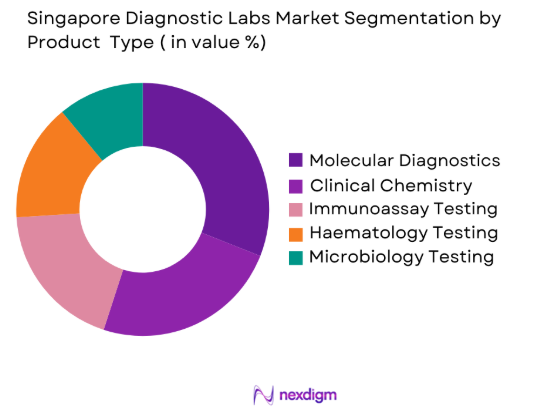

By Product Type

Singapore Diagnostic Labs market is segmented by product type into clinical chemistry testing, molecular diagnostics, haematology testing, immunoassay testing, and microbiology testing. Recently, molecular diagnostics testing has a dominant market share due to factors such as increasing infectious disease surveillance programs, expanding genomic medicine initiatives, and the presence of advanced diagnostic laboratories across Singapore’s healthcare system. Government-backed biomedical research initiatives and strong biotechnology sector collaboration have accelerated adoption of high-throughput PCR, sequencing, and genomic testing technologies. Molecular diagnostics laboratories support clinical decision making across oncology, infectious disease management, and precision medicine programs implemented by major hospital systems. The presence of advanced laboratory automation systems, strong regulatory oversight from the Health Sciences Authority, and rising patient demand for rapid and highly accurate diagnostic testing further reinforce the dominance of molecular diagnostic testing services across the Singapore diagnostic laboratory ecosystem.

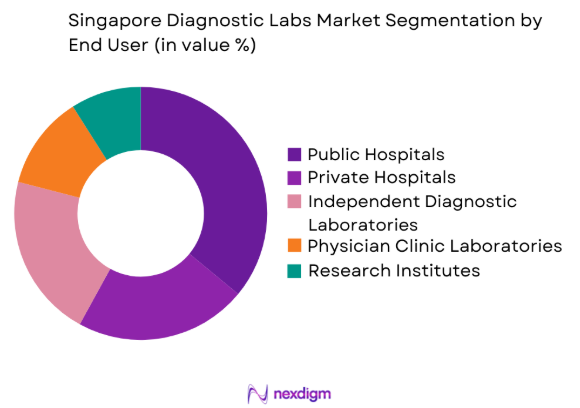

By End User

Singapore Diagnostic Labs market is segmented by end users into public hospitals, private hospitals, independent diagnostic laboratories, research institutes, and physician clinic laboratories. Recently, public hospitals have a dominant market share due to factors such as centralized healthcare delivery systems, integrated diagnostic laboratories within large hospital campuses, and strong government funding for healthcare infrastructure. Singapore’s public healthcare clusters including Sing Health, National Healthcare Group, and National University Health System operate large laboratory networks that process high volumes of diagnostic tests daily. These hospitals also support national disease surveillance programs and precision medicine research initiatives, requiring advanced laboratory capabilities and high throughput diagnostic platforms. The presence of specialized medical centres, oncology diagnostic programs, and infectious disease laboratories within public healthcare institutions further strengthens their role as the primary diagnostic testing providers across Singapore’s healthcare ecosystem.

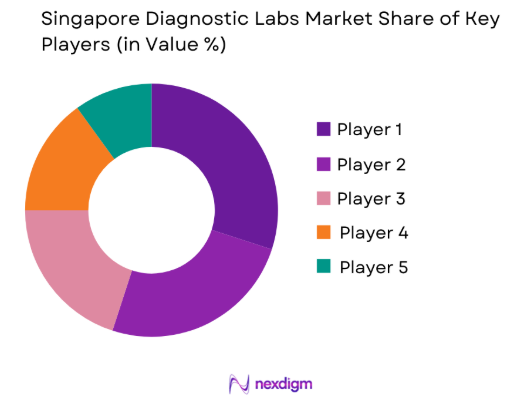

Competitive Landscape

The Singapore Diagnostic Labs Market is characterized by a moderately consolidated structure dominated by integrated healthcare providers and multinational diagnostic technology companies. Major hospital laboratory networks maintain strong diagnostic capacity through advanced automation platforms and centralized laboratory infrastructure. Global diagnostic equipment manufacturers collaborate with healthcare institutions to deploy molecular diagnostics, immunoassay analysers, and high-throughput laboratory systems. Strategic partnerships between hospitals, biotechnology firms, and research institutes continue to strengthen the competitive landscape while supporting innovation in precision diagnostics.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Parkway Laboratories | 1996 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Raffles Medical Group | 1976 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Innoquest Diagnostics | 2001 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Switzerland | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Germany | ~ | ~ | ~ | ~ | ~ |

Singapore Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Precision Medicine and Genomic Testing Programs

Expansion of precision medicine and genomic testing programs drives growth in the Singapore Diagnostic Labs Market as healthcare strategies increasingly prioritize personalized diagnostics and targeted therapies. Hospitals integrate genomic sequencing technologies into diagnostic workflows to analyze patient genetic profiles and guide treatment decisions. Government supported biomedical research initiatives encourage laboratories to adopt high throughput sequencing platforms for complex genomic analysis. Genomic diagnostics are widely used in oncology testing to identify mutations linked to cancer development. Diagnostic laboratories therefore invest in bioinformatics systems and advanced molecular testing infrastructure. Collaboration between biotechnology companies and healthcare institutions further accelerates innovation in clinical genomic diagnostics.

Growing Burden of Chronic Diseases and Preventive Healthcare Screening Programs

Growing prevalence of chronic diseases and preventive healthcare screening programs significantly drives the Singapore Diagnostic Labs Market because increasing health awareness encourages early disease detection and routine diagnostic testing. Conditions such as diabetes, cardiovascular disorders, and cancer require continuous laboratory monitoring for effective treatment management. Healthcare providers conduct blood tests, biomarker analysis, and pathology examinations to track disease progression. National health screening initiatives further increase diagnostic testing volumes across hospitals and clinics. Corporate wellness programs and expanding preventive health packages also contribute to higher laboratory utilization. As the aging population grows, diagnostic laboratories expand automated testing capacity to support rising healthcare demand.

Market Challenges

High Cost of Advanced Diagnostic Technologies and Laboratory Automation Systems

High Cost of Advanced Diagnostic Technologies and Laboratory Automation Systems: High costs of advanced diagnostic technologies and laboratory automation systems pose a significant challenge for the Singapore Diagnostic Labs Market because modern laboratories rely on sophisticated equipment, specialized infrastructure, and trained professionals to operate complex testing platforms. Molecular diagnostic analyzers, genomic sequencing instruments, and automated laboratory robotics require large capital investments for acquisition and installation. Ongoing maintenance, calibration, and software updates further raise operational costs. Smaller diagnostic laboratories often face financial limitations that restrict technology adoption. In addition, expensive reagents and specialized consumables used in advanced testing procedures increase procurement expenses, creating financial pressure for laboratories seeking to expand services.

Regulatory Compliance and Quality Assurance Requirements for Diagnostic Laboratories

Regulatory compliance and quality assurance requirements create operational complexities for the Singapore Diagnostic Labs Market because laboratories must follow strict regulations governing testing accuracy, safety standards, and patient data protection. Authorities such as the Health Sciences Authority enforce guidelines for laboratory accreditation, diagnostic device approval, and clinical testing procedures. Laboratories implement quality management systems to monitor equipment calibration, sample handling, and testing workflows. Regular inspections and certification audits ensure adherence to international laboratory standards. Compliance also requires investment in secure digital systems for managing patient diagnostic data. These regulatory obligations increase operational costs and administrative responsibilities for diagnostic laboratory operators.

Opportunities

Expansion of Artificial Intelligence and Digital Pathology in Diagnostic Laboratories

Expansion of artificial intelligence and digital pathology in diagnostic laboratories creates strong opportunities for the Singapore Diagnostic Labs Market as healthcare providers adopt advanced computational tools to enhance diagnostic accuracy and laboratory efficiency. Artificial intelligence algorithms analyze pathology slides, medical images, and laboratory data to detect disease patterns quickly. Digital pathology converts microscope slides into high-resolution images for machine learning analysis. Hospitals invest in integrated AI diagnostic systems and laboratory information platforms. These technologies support faster interpretation, higher testing volumes, and improved diagnostic consistency. Remote pathology consultations through digital platforms also expand access to specialized diagnostic expertise across healthcare networks.

Growth of Home-Based Diagnostic Testing and Remote Sample Collection Services

Growth of home-based diagnostic testing and remote sample collection services creates emerging opportunities in the Singapore Diagnostic Labs Market because healthcare consumers increasingly prefer convenient diagnostic services that reduce hospital visits while maintaining access to reliable laboratory testing. Patients can schedule sample collection at home for routine screening and disease monitoring. Diagnostic laboratories deploy trained phlebotomists to collect blood and other specimens at residences. Digital healthcare platforms allow online booking and electronic report delivery. Telemedicine integration enables physicians to review diagnostic results remotely and guide patients. This service model improves accessibility for elderly populations, busy professionals, and individuals seeking preventive healthcare screening.

Future Outlook

The Singapore Diagnostic Labs Market is expected to witness sustained growth driven by increasing demand for precision diagnostics, rising preventive healthcare adoption, and continued investment in biomedical innovation. Expansion of genomic medicine programs, artificial intelligence integration in pathology, and automation of laboratory workflows will enhance diagnostic capabilities. Government healthcare initiatives supporting early disease detection and digital healthcare transformation will further strengthen the diagnostic ecosystem. Growing healthcare demand and technological advancement will continue shaping laboratory diagnostics across Singapore.

Major Players

- Parkway Laboratories

- Raffles Medical Group

- InnoquestDiagnostics

- Pathology Asia Holdings

- Roche Diagnostics

- Siemens Healthineers

- Abbott Laboratories

- Bio-Rad Laboratories

- ThermoFisher Scientific

- SYNLAB International

- Quest Diagnostics

- Fullerton Health Diagnostics

- LifeStrandsGenomics

- A*STAR Diagnostics Development Hub

- Clinical Reference Laboratory

Key Target Audience

- Hospital networks and healthcare providers

- Pharmaceutical and biotechnology companies

- Diagnostic equipment manufacturers

- Healthcare technology companies

- Insurance and healthcare financing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Private healthcare investors

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying core market variables influencing the Singapore Diagnostic Labs Market including healthcare infrastructure expansion, laboratory technology adoption, diagnostic testing demand, and regulatory frameworks affecting clinical laboratories.

Step 2: Market Analysis and Construction

Comprehensive analysis is conducted using healthcare industry databases, financial disclosures from diagnostic companies, and public health data from government healthcare authorities to construct accurate market size and segmentation insights.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including laboratory professionals, healthcare administrators, and biomedical technology specialists validate market assumptions and technology trends affecting the diagnostic laboratory ecosystem.

Step 4: Research Synthesis and Final Output

Validated research findings are synthesized into structured market insights that evaluate diagnostic technology adoption, healthcare infrastructure development, and strategic trends shaping the Singapore Diagnostic Labs Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Precision Medicine and Genomic Testing Programs

Rising Demand for Early Disease Detection and Preventive Diagnostics

Strong Healthcare Infrastructure and Public Health Investment - Market Challenges

High Capital Cost of Advanced Diagnostic Equipment

Stringent Regulatory Approval and Laboratory Accreditation Requirements

Shortage of Skilled Laboratory Technologists and Specialists - Market Opportunities

Integration of Artificial Intelligence in Clinical Diagnostics

Growth of Home Based and Remote Diagnostic Services

Expansion of Genomic Sequencing and Personalized Medicine - Trends

Adoption of Automation and Robotics in Diagnostic Laboratories

Growth of Digital Pathology and Remote Diagnostic Platforms

Increasing Use of Data Analytics in Clinical Diagnostics - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Analyzers

Hematology Diagnostic Systems

Molecular Diagnostic Platforms

Immunoassay Diagnostic Systems

Point of Care Diagnostic Systems - By Platform Type (In Value%)

Hospital Based Diagnostic Laboratories

Independent Diagnostic Laboratory Networks

Academic and Research Diagnostic Laboratories

Private Physician Office Laboratories

Mobile and Home Diagnostic Service Platforms - By Fitment Type (In Value%)

Centralized Laboratory Diagnostic Systems

Decentralized Point of Care Systems

Integrated Hospital Information Systems

Standalone Diagnostic Equipment

Cloud Connected Diagnostic Platforms - By End User Segment (In Value%)

Public Hospitals and Healthcare Institutions

Private Hospitals and Specialist Clinics

Diagnostic Laboratory Chains

Academic and Research Institutes

Pharmaceutical and Biotechnology Companies - By Procurement Channel (In Value%)

Direct Procurement from Diagnostic Equipment Manufacturers

Government Healthcare Procurement Programs

Hospital Group Procurement Networks

Third Party Medical Equipment Distributors

Public Healthcare Tender Contracts

- Market Share Analysis

- Cross Comparison Parameters (Technology Portfolio, Test Menu Breadth, Laboratory Network Size, Automation Capability, Strategic Partnerships, Test Turnaround Time, Sample Collection Network, Digital Health Integration, Quality Accreditation & Compliance, Diagnostic Accuracy & Sensitivity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Parkway Laboratories

Raffles Medical Group

Quest Laboratories Singapore

Pathology Asia Holdings

Clinical Reference Laboratory Singapore

IHH Healthcare Diagnostics

SYNLAB International

Fullerton Health Diagnostics

Innoquest Diagnostics

LifeStrands Genomics

A*STAR Diagnostics Development Hub

Roche Diagnostics Asia Pacific

Abbott Diagnostics Singapore

Siemens Healthineers Singapore

Bio Rad Laboratories Asia Pacific

- Hospitals Increasingly Integrating Advanced Molecular Diagnostic Platforms

- Private Clinics Expanding Preventive Health Screening Services

- Diagnostic Chains Investing in Automation and High Throughput Systems

- Research Institutes Expanding Genomic and Translational Medicine Programs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now