Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Singapore’s edge computing market reached approximately USD ~ million based on a recent historical assessment, driven by 5G network densification, industrial IoT adoption, and latency-sensitive digital services across manufacturing, logistics, and smart city platforms. Telecom operators and cloud providers are deploying distributed edge nodes and micro data centers to support real-time analytics and AI inference workloads. Expansion of autonomous systems, smart mobility, and digital infrastructure applications is accelerating demand for localized compute and edge networking infrastructure.

Singapore dominates Southeast Asia’s edge computing landscape due to dense 5G coverage, advanced industrial automation, and concentration of logistics and urban digital services requiring ultra-low-latency processing. Jurong and Tuas industrial zones host manufacturing and port automation edge deployments, while urban districts concentrate smart city and enterprise edge workloads. Strong telecom infrastructure, regulatory clarity, and digital innovation ecosystems position Singapore as the region’s primary edge computing deployment hub.

Market Segmentation

By Product Type

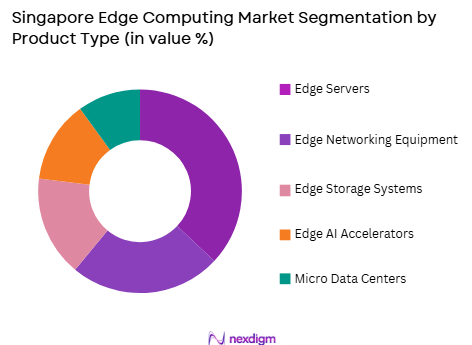

Singapore Edge Computing Market is segmented by product type into edge servers, edge networking equipment, edge storage systems, edge AI accelerators, and micro data centers. Recently, edge servers have a dominant market share due to factors such as 5G edge node deployments, industrial automation compute requirements, and real-time analytics processing across logistics and smart city applications. Telecom operators deploy ruggedized edge servers at base stations and aggregation sites to host low-latency applications. Manufacturing and port automation systems rely on localized compute nodes for robotics and control systems. Cloud providers extend distributed compute platforms through edge server installations. AI inference workloads in video analytics and autonomous operations further increase server demand. Edge infrastructure scaling across urban and industrial environments reinforces this segment’s leadership in Singapore’s distributed computing ecosystem.

By End User

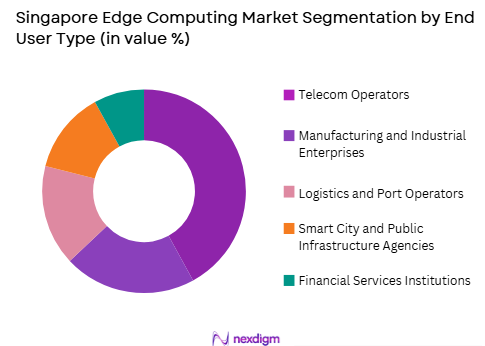

Singapore Edge Computing Market is segmented by end user into telecom operators, manufacturing and industrial enterprises, logistics and port operators, smart city and public infrastructure agencies, and financial services institutions. Recently, telecom operators have a dominant market share due to factors such as 5G multi-access edge computing deployment, distributed network infrastructure ownership, and hosting of enterprise edge applications on telecom platforms. Telecom providers deploy edge nodes across base stations and central offices enabling low-latency services. Enterprises utilize telecom-hosted edge environments instead of building private infrastructure. 5G network slicing and edge services drive telecom investment. Partnerships with cloud providers extend edge platforms. These dynamics position telecom operators as primary edge infrastructure investors and operators in Singapore.

Competitive Landscape

Singapore’s edge computing market is concentrated among telecom operators, cloud providers, and edge hardware vendors deploying distributed compute infrastructure across 5G networks and industrial environments. Market leadership is shaped by telecom edge platform scale, 5G integration capability, and industrial edge solution expertise. Partnerships between telecom operators and hyperscale cloud providers are central to edge ecosystem development in Singapore.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Singapore Edge Role |

| Singtel | 1879 | Singapore | ~ | ~ | ~ | ~ | ~ |

| StarHub | 2000 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| Huawei | 1987 | China | ~ | ~ | ~ | ~ | ~ |

Singapore Edge Computing Market Analysis

Growth Drivers

5G Multi-Access Edge Computing Deployment and Telecom Edge Platform Expansion

Singapore’s edge computing market growth is primarily driven by rapid deployment of 5G multi-access edge computing infrastructure by telecom operators enabling ultra-low-latency services across industrial, enterprise, and consumer applications. Nationwide 5G standalone networks provide dense connectivity fabric for distributed edge nodes located at base stations and aggregation sites. Telecom providers deploy edge servers and micro data centers integrated with network cores to host real-time applications. Enterprises leverage telecom edge platforms instead of building private infrastructure, accelerating adoption. Cloud providers integrate edge services with telecom networks enabling distributed cloud architectures. Smart mobility, video analytics, and augmented reality services require proximity compute enabled by 5G MEC. Industrial automation and robotics systems rely on telecom edge for control latency. Continuous 5G densification expands edge node footprint. Telecom-cloud partnerships standardize edge platforms across Singapore. These 5G MEC deployment dynamics structurally anchor sustained edge infrastructure investment.

Industrial Automation, Smart Port, and Urban Digital Infrastructure Applications

Extensive deployment of automation, robotics, and real-time monitoring systems across Singapore’s manufacturing plants, ports, and urban infrastructure is a major driver of edge computing infrastructure demand requiring localized compute and AI inference capabilities. Smart port operations in Tuas deploy edge systems for autonomous vehicles, cargo tracking, and predictive maintenance. Advanced manufacturing facilities utilize edge compute for robotics coordination and quality inspection. Urban digital infrastructure including traffic management and surveillance relies on edge analytics. Industrial IoT sensors generate high-volume data requiring local processing. Energy and utilities systems deploy edge monitoring nodes. Smart building and facility management platforms use distributed compute. Real-time safety and operational analytics depend on low-latency edge infrastructure. Integration with central cloud systems increases hybrid architectures. Singapore’s smart nation initiatives expand edge application scope. These industrial and urban digitalization dynamics significantly expand edge computing deployment across Singapore.

Market Challenges

Limited Physical Space and Infrastructure Integration Complexity

Singapore’s edge computing deployment faces constraints from limited physical space for distributed infrastructure in dense urban environments and complexity of integrating edge nodes across telecom, industrial, and urban systems. Edge nodes must be installed in space-constrained base stations, buildings, and industrial sites. Retrofitting infrastructure for edge hardware increases engineering complexity. Urban zoning and regulatory approvals affect installation. Interoperability between telecom, enterprise, and city systems is technically challenging. Network integration and orchestration across distributed nodes require advanced management. Physical security and environmental protection of edge equipment add costs. Multi-stakeholder coordination complicates deployment timelines. Maintenance access in dense environments is constrained. Standardization gaps affect integration. These spatial and integration challenges slow large-scale edge rollout.

Cybersecurity and Distributed Infrastructure Management Risks

Edge computing infrastructure in Singapore faces elevated cybersecurity and operational management risks due to highly distributed node architectures across telecom and industrial environments. Edge nodes expand attack surfaces compared with centralized data centers. Securing distributed compute across public and industrial sites is complex. Real-time edge applications require resilient protection mechanisms. Monitoring and patching large node fleets increase operational burden. Industrial control systems connected to edge raise safety risks. Telecom-cloud integration introduces multi-domain security challenges. Compliance requirements for critical infrastructure add constraints. Data privacy at edge locations must be ensured. Managing distributed infrastructure lifecycle is complex. These security and management risks challenge scalable edge deployment.

Opportunities

Autonomous Systems, Robotics, and AI Inference at the Edge

Singapore’s leadership in autonomous transport, robotics, and AI-driven urban systems creates strong opportunity for expansion of edge computing infrastructure optimized for real-time inference and control workloads across mobility, logistics, and smart infrastructure. Autonomous vehicles and drones require localized compute. Robotics coordination depends on low-latency edge processing. AI video analytics for safety and operations expands demand. Smart transport and traffic systems rely on edge nodes. Industrial automation growth increases inference workloads. Defense and security applications adopt edge AI. Integration with 5G enhances capabilities. Edge AI platforms can be exported regionally. Singapore’s innovation ecosystem supports development. These autonomous and robotics applications drive edge growth.

Edge-Cloud Hybrid Platforms and Regional Edge Service Export

Singapore can expand hybrid edge-cloud platforms and export edge computing services regionally leveraging telecom infrastructure, cloud partnerships, and digital trade connectivity. Enterprises deploy hybrid architectures across Singapore edge nodes and regional operations. Telecom providers can offer regional edge hosting. Cross-border digital services rely on Singapore edge compute. Cloud providers extend edge regions through Singapore hubs. Managed edge services create new revenue streams. Regional enterprises access Singapore edge platforms. Integration with AI and IoT ecosystems expands services. Singapore’s trusted digital environment supports exports. These hybrid and regional service opportunities expand market scope.

Future Outlook

Singapore’s edge computing market is expected to expand steadily over the next five years as 5G MEC deployment, industrial automation, and smart city applications increase demand for distributed compute. Autonomous systems and AI inference workloads will accelerate edge node deployment. Telecom-cloud partnerships will deepen hybrid edge architectures. Singapore will remain Southeast Asia’s primary edge computing innovation and deployment hub.

Major Players

- Singtel

- StarHub

- M1

- ST Engineering

- Amazon Web Services

- Microsoft

- Huawei

- Cisco

- ell Technologies

- Hewlett Packard Enterprise

- NVIDIA

- Ericsson

- Nokia

- Equinix

Key Target Audience

- Telecom operators

- Manufacturing and industrial enterprises

- Logistics and port operators

- Smart city infrastructure agencies

- Transportation authorities

- Digital platform companies

- Government and regulatory bodies

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key variables including edge node deployments, 5G coverage, industrial automation adoption, and distributed compute capacity were identified across Singapore’s edge ecosystem. Demand drivers across telecom, manufacturing, logistics, and smart infrastructure were mapped to infrastructure requirements. Supply-side variables such as telecom networks and edge hardware vendors were defined.

Step 2: Market Analysis and Construction

Primary and secondary inputs were integrated to construct the Singapore edge computing market model, incorporating MEC deployment, industrial automation projects, and smart city initiatives. Segmentation by product type and end user was applied to estimate shares. Competitive roles of telecom and cloud providers were analyzed.

Step 3: Hypothesis Validation and Expert Consultation Assumptions regarding edge a

doption growth, 5G expansion, and industrial deployment were validated through consultations with telecom engineers, industrial automation specialists, and edge computing experts. Alignment with Singapore digital infrastructure strategies was verified. Sensitivity checks were applied to deployment scenarios.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into a structured Singapore edge computing market report covering segmentation, competitive landscape, and strategic outlook. Quantitative estimates were aligned with deployment evidence and policy direction. The final output integrates drivers, constraints, and opportunities shaping edge computing growth in Singapore.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

5G network densification and ultra-low latency services demand

Smart Nation and urban digital infrastructure initiatives

Industrial automation and real-time analytics adoption - Market Challenges

Limited physical space for distributed edge infrastructure

Interoperability and lifecycle management complexity

Cybersecurity risks across distributed edge nodes - Market Opportunities

Edge AI deployment for autonomous and urban applications

Integration of edge with hyperscale cloud ecosystems

Edge infrastructure for ports, airports, and logistics hubs - Trends

Convergence of telco edge and cloud edge platforms

Adoption of modular micro data centers

Growth of AI-enabled edge analytics and inference - Government regulations

Data protection and cybersecurity compliance frameworks

Telecom and critical infrastructure regulations

Smart city and digital infrastructure policies - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Compute Servers

Edge Storage Systems

Edge Networking and Gateways

Micro Data Center Modules

Edge AI and Analytics Platforms - By Platform Type (In Value%)

On-Premise Edge Platforms

Telco Edge Platforms

Cloud-Managed Edge Platforms

Industrial Edge Platforms

AI Edge Platforms - By Fitment Type (In Value%)

Enterprise Edge Deployments

Telecom Network Edge Sites

Smart City Edge Installations

Industrial and Port Edge Nodes

Retail and Campus Edge Systems - By EndUser Segment (In Value%)

Telecom and 5G Operators

Manufacturing and Industry 4.0

Transport and Port Logistics

Retail and Smart Buildings

Government and Smart Nation Programs - By Procurement Channel (In Value%)

Telecom Operator Procurement

Direct OEM Procurement

System Integrators

Cloud and Edge Partnerships

Government Digital Programs

- Market Share Analysis

- Cross Comparison Parameters (Edge Deployment Architecture, Latency and Real-Time Performance, Edge AI and Analytics Capability, 5G and Telco Network Integration, Micro Data Center Design and Density, Hybrid Cloud and Edge Orchestration, Industry-Specific Edge Solutions, Security and Zero-Trust Edge Compliance, Lifecycle and Remote Management, Regional Edge Connectivity Ecosystem)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Cisco

Nokia

Ericsson

Huawei

Supermicro

Schneider Electric

Vertiv

Amazon Web Services

Microsoft

Google

Singtel

ST Engineering

- Telecom operators deploying 5G edge for low-latency services

- Manufacturers adopting edge for automation and vision systems

- Ports and logistics hubs using edge analytics platforms

- Government deploying edge for smart city operations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now