Download PDF

Download PDFMarket Overview

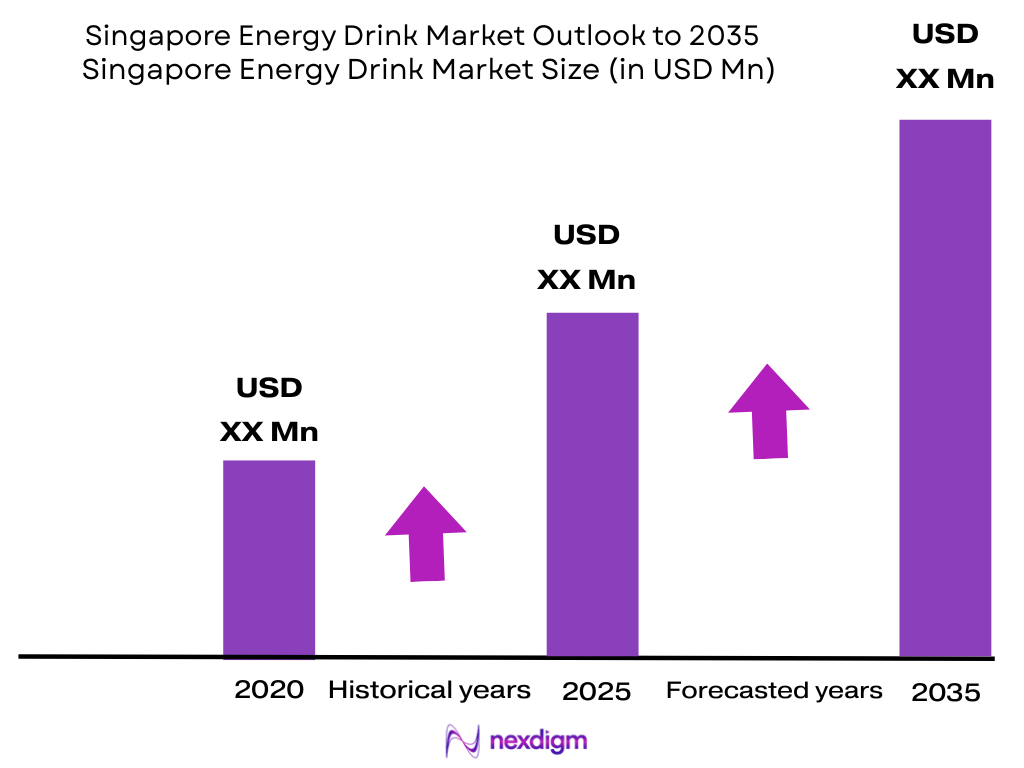

The Singapore Energy Drink Market is valued at USD ~ million, based on a five-year historical analysis, while another country-level benchmark places the market at USD 25.0 million under a narrower retail-value definition. The forecasted CAGR for the 2026–2035 period is benchmarked at 8.16%, aligned with the global long-term energy drink outlook, while Singapore-specific forecasts show 8.17% for the available country forecast window. Demand is driven by office productivity, convenience retail, fitness, gaming, tourism and zero-sugar innovation. The Singapore Energy Drink Market is concentrated across the Central Business District, Marina Bay, Orchard, Changi, Jurong, Tampines, Woodlands and Sentosa because these zones combine offices, universities, gyms, nightlife, tourist attractions, airport retail, convenience stores, vending and supermarket networks. Singapore’s GDP reached USD 547.39 billion, GDP per capita reached USD 90,674.1, and population was approximately 6 million, supporting high-value imported cans, multipacks and premium sugar-free beverages.

Market Segmentation

By Product Type

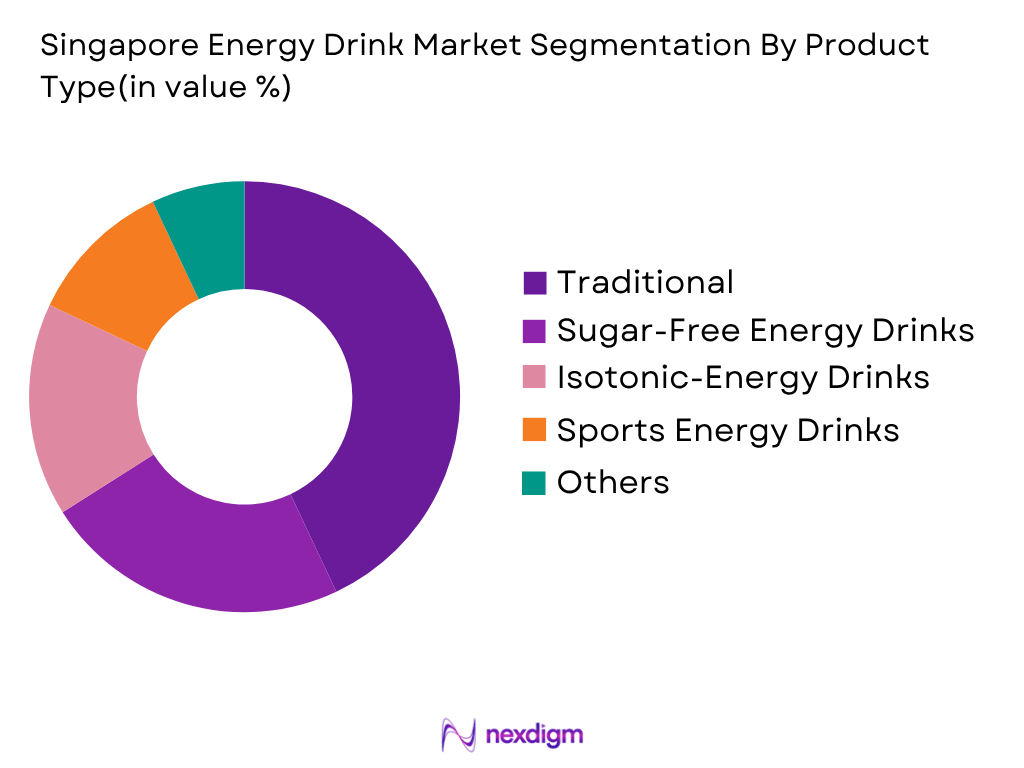

Singapore Energy Drink Market is segmented by product type into traditional or standard energy drinks, sugar-free energy drinks, isotonic-energy drinks, sports energy drinks, natural-caffeine energy drinks, and energy shots or powdered energy mixes. Recently, traditional or standard energy drinks have a dominant market share in Singapore under product type segmentation because they benefit from strong brand recall, convenience-store visibility and immediate-consumption occasions. Red Bull, Monster, Lucozade, HELL, Carabao and similar imported brands are positioned around alertness, stamina, gaming, late-night work, study, gym routines and nightlife. Singapore’s compact retail network also favours single-serve chilled cans, which are available through 7-Eleven, Cheers, FairPrice, Cold Storage, petrol stations, vending machines and e-commerce platforms. Sugar-free and low-sugar formats are expanding due to Nutri-Grade visibility, but standard energy drinks remain dominant because they retain mainstream taste familiarity and stronger legacy demand.

By Packaging Type

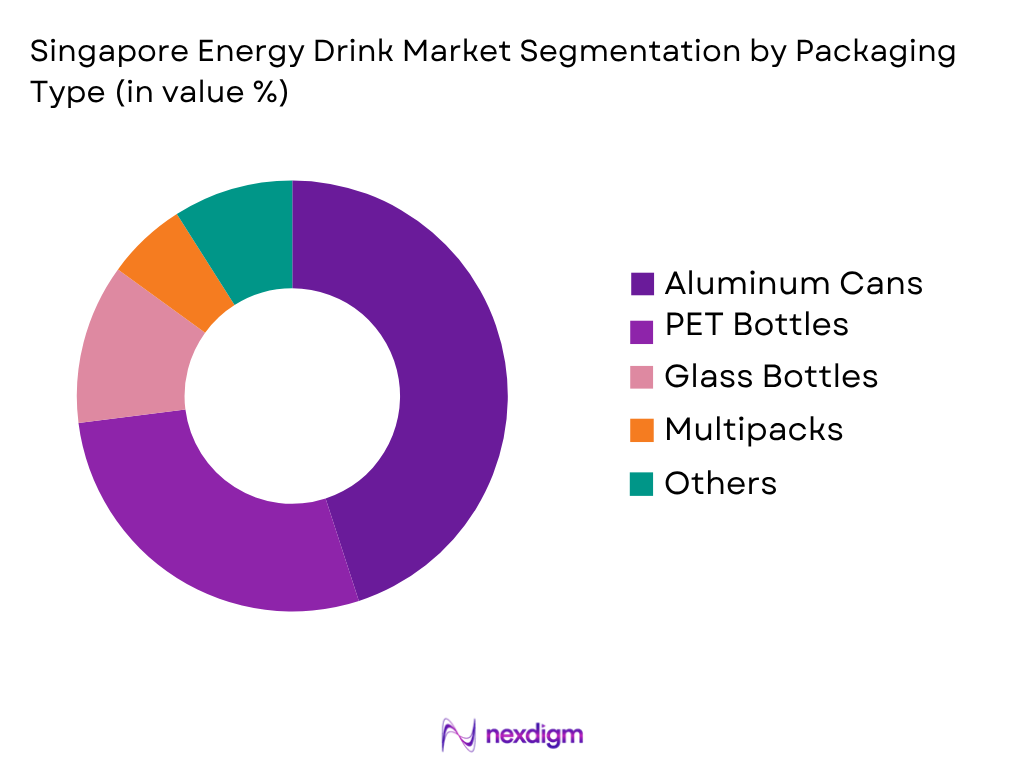

Singapore Energy Drink Market is segmented by packaging type into aluminum cans, PET bottles, multipacks, glass bottles, energy shots, and powder tubs or sachets. Recently, aluminum cans have a dominant market share under packaging type segmentation because they are the most recognised format for energy drinks across convenience stores, supermarkets, gyms, vending machines, bars and e-commerce. Cans support carbonation stability, fast chilling, strong shelf branding and single-serve impulse purchase, which fits Singapore’s dense urban routines. Red Bull’s slim-can format, Monster’s large-can portfolio, HELL’s European cans and Carabao’s mainstream can positioning reinforce this structure. PET bottles are more relevant to isotonic and sports-energy adjacency, while multipacks are mainly purchased through FairPrice, RedMart, Amazon and supermarket channels. Global energy drink benchmarks also identify cans as the largest packaging format, supporting Singapore’s can-led category structure.

Competitive Landscape

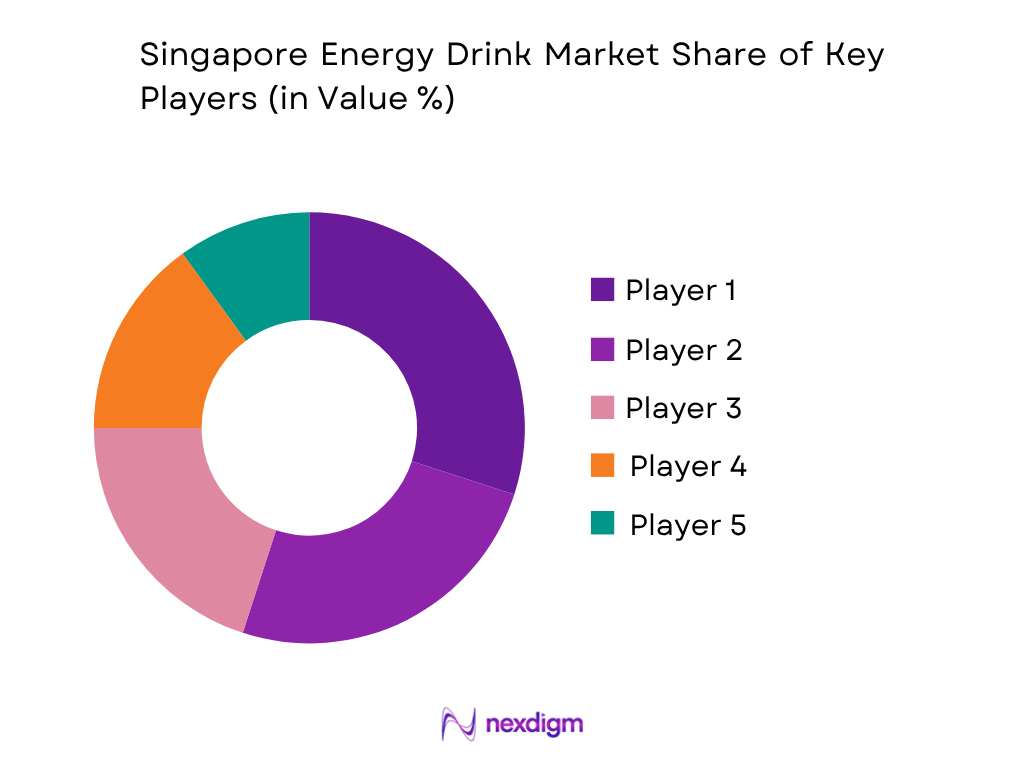

The Singapore Energy Drink Market is led by global premium energy brands, regional Southeast Asian players, isotonic-energy adjacent companies and e-commerce-led functional beverage brands. Red Bull and Monster maintain strong visibility through convenience stores, supermarkets, gyms, nightlife and imported SKU appeal, while Lucozade, Carabao, HELL, Prime, G Fuel and Celsius address sports, gaming, fitness and lifestyle-led demand. Competition is shaped by Nutri-Grade compliance, sugar-free availability, imported flavor breadth, chiller facings, vending access and multipack visibility across online grocery platforms.

| Company | Establishment Year | Headquarters | Core Energy Portfolio | Singapore Positioning | Packaging Focus | Distribution Strength | Product Innovation Focus | Market-Specific Edge |

| Red Bull GmbH | 1984 | Fuschl am See, Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| Monster Beverage Corporation | 1935 | Corona, California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| PepsiCo Singapore | 1965 | Purchase, New York, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Lucozade Ribena Suntory Singapore | 2014 | London / Singapore operations | ~ | ~ | ~ | ~ | ~ | ~ |

| Fraser and Neave Singapore | 1883 | Singapore | ~ | ~ | ~ | ~ | ~ | ~ |

Singapore Energy Drink Market Analysis

Growth Drivers

High-Income Urban Workforce and Convenience-Led Energy Consumption

Singapore Energy Drink Market is supported by a compact, high-income urban economy where energy drinks are purchased through convenience stores, supermarkets, vending machines, petrol stations, office pantries and e-commerce channels for work productivity, study, commuting, gaming and shift-based service work. World Bank reported Singapore GDP at USD 547.39 billion and GDP per capita at USD 90,674.07 in 2024, supporting premium imported cans, zero-sugar variants and functional beverage formats. Singapore’s total population stood at 6.04 million as at June 2024, creating a concentrated addressable base for chilled single-serve energy drinks in CBD, Marina Bay, Orchard, Jurong, Tampines and Changi.

Tourism, Airport Retail and Nightlife-Led Demand

Singapore Energy Drink Market benefits from travel, hospitality and nightlife consumption because energy drinks are relevant in Changi Airport, hotels, bars, clubs, Sentosa, Marina Bay, Orchard Road, event venues and late-night retail. Singapore Tourism Board reported 16.5 million international visitor arrivals in 2024, up from 2023, supporting beverage demand across tourism corridors, duty-free zones, convenience stores and HoReCa outlets. STB also reported 16.9 million international visitor arrivals in 2025, including 3.1 million from Mainland China, 2.4 million from Indonesia, 1.3 million from Malaysia, 1.3 million from Australia and 1.2 million from India, strengthening premium energy drink occasions across travel and nightlife channels.

Market Challenges

Nutri-Grade Labelling and Sugar-Reformulation Pressure

Singapore Energy Drink Market faces regulatory pressure because sugar content is visible to consumers and retail buyers under the Nutri-Grade framework. HPB states that Nutri-Grade beverage measures for pre-packaged beverages and non-customisable automated beverage dispensers came into effect on 30 December 2022, and were extended to freshly prepared beverages from 30 December 2023. MOH states that beverages must be graded A, B, C or D, beverages graded C or D must display the Nutri-Grade mark, and advertisements for Grade D beverages are prohibited. This directly pressures energy drink brands to expand zero-sugar, low-sugar and reduced-calorie SKUs.

Small-Market Shelf Saturation and Imported SKU Dependency

Singapore Energy Drink Market faces shelf-space and import-dependency pressure because the country is compact, highly urban and served by limited chiller facings across convenience stores, supermarkets, vending machines, gyms and petrol stations. Singapore’s population stood at 6.04 million in June 2024, while resident population stood at 4.18 million, making the addressable market concentrated but small compared with larger Asian beverage markets. MOM reported overall employment growth of 45,500 in 2024, compared with 78,800 in 2023, indicating a mature labour market where growth depends more on SKU rotation, channel execution and premiumisation than broad population expansion.

Market Opportunities

Zero-Sugar, Low-Sugar and Nutri-Grade-Aligned Energy Drinks

Singapore Energy Drink Market has future growth opportunity in zero-sugar, low-sugar and Nutri-Grade-aligned energy drinks because current regulation makes sugar visibility commercially important. MOH states that Nutri-Grade requirements apply to freshly prepared beverages sold at retail settings such as F&B outlets and catering establishments, and non-retail settings such as hotels, workplaces, educational institutions, healthcare institutions and childcare facilities from 30 December 2023. Non-compliance can lead to a fine of up to S$1,000 for a first offence and up to S$2,000 for second or subsequent convictions. Energy drink brands can use this environment to grow sugar-free cans, lower-sugar multipacks, office-pantry packs and gym-focused functional SKUs.

Office Pantry, Vending and E-Commerce Multipack Expansion

Singapore Energy Drink Market has future growth opportunity through office pantry, vending, campus retail, supermarket apps and e-commerce multipacks because the country combines high income, dense workplaces and strong digital retail habits. World Bank reported GDP per capita at USD 90,674.07 and GDP at USD 547.39 billion in 2024, supporting premium functional beverage purchases. Singapore’s total population reached 6.04 million, with 1.86 million non-residents, including foreign workers, dependants and international students, increasing demand around workplaces, campuses, industrial parks and convenience retail. Brands can target CBD offices, Changi Business Park, Jurong, universities, gyms and e-commerce platforms with multipacks and imported flavour ranges.

Future Outlook

The Singapore Energy Drink Market is expected to expand steadily as the category shifts from legacy stimulant beverages toward sugar-free, low-sugar, performance, focus and natural-caffeine formats. The market will remain highly urban, import-led and channel-intensive, with demand clustered around convenience stores, supermarkets, vending machines, gyms, offices, campuses, nightlife venues and e-commerce platforms.

The 2026–2035 CAGR is benchmarked at 8.16% using the global long-term energy drink forecast, while Singapore-specific sources indicate 8.17% growth across the available country forecast window. Singapore’s high GDP per capita, compact retail infrastructure and strong tourism recovery support premiumisation, while Nutri-Grade rules push companies toward better-for-you reformulation.

Over the next phase, zero-sugar energy drinks and Nutri-Grade-aligned products will gain stronger shelf visibility. Brands with reduced-sugar formulations, clear nutrition labelling and imported flavor variety can gain traction with office professionals, students, gym-goers and digitally active consumers. Natural-caffeine products using guarana, green tea, ginseng or botanical ingredients can also address wellness-oriented consumers seeking alternatives to traditional caffeine-taurine formulas.

Convenience stores, e-commerce and vending machines will remain central to consumption. Energy drinks in Singapore are often purchased as immediate-use products during work, study, commuting, gaming and late-night occasions. RedMart, Amazon, Lazada and Shopee can support multipacks, limited editions and imported SKUs, while 7-Eleven, Cheers, FairPrice, Cold Storage and petrol-station stores will continue to drive chilled single-serve purchases.

Major Players

- Red Bull Singapore

- Monster Energy Singapore

- PepsiCo Singapore

- The Coca-Cola Company Singapore

- Lucozade Ribena Suntory Singapore

- Fraser and Neave Singapore

- Yeo Hiap Seng

- Otsuka Pharmaceutical Singapore

- Taisho Pharmaceutical

- TCP Group Singapore

- HELL Energy Singapore

- Carabao Energy Drink Singapore

- Prime Hydration Singapore

- G Fuel Singapore

- Celsius Holdings Singapore

Key Target Audience

- Energy drink manufacturers and brand owners

- Functional beverage companies

- Carbonated soft drink and packaged beverage companies

- Convenience store, supermarket and hypermarket retail chains

- Vending, office pantry and e-commerce channel operators

- Gym, sports nutrition, HoReCa and nightlife channel operators

- Investments and venture capitalist firms

- Government and regulatory bodies (Singapore Food Agency, Health Promotion Board, Ministry of Health, Singapore Customs, Competition and Consumer Commission of Singapore)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map for the Singapore Energy Drink Market, covering brand owners, importers, distributors, supermarkets, convenience stores, vending operators, gyms, HoReCa outlets, e-commerce platforms and regulators. The objective is to identify key variables such as product type, sugar profile, Nutri-Grade band, caffeine positioning, pack format, imported SKU breadth and channel reach.

Step 2: Market Analysis and Construction

In this phase, historical data for the Singapore Energy Drink Market is compiled through country-level market benchmarks, company portfolios, SKU listings, retail shelf checks, e-commerce availability and channel mapping. The assessment reviews standard energy drinks, sugar-free variants, isotonic-energy adjacency, cans, PET bottles, multipacks, convenience stores, vending, supermarkets, gyms and online product availability.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through computer-assisted telephone interviews with beverage importers, supermarket category buyers, convenience-store operators, vending suppliers, gym retailers, e-commerce sellers and HoReCa distributors. These consultations provide operational insights into SKU movement, chiller placement, imported flavor rotation, Nutri-Grade impact, sugar-free adoption, promotion mechanics and channel-specific acceptance.

Step 4: Research Synthesis and Final Output

The final phase triangulates top-down market benchmarks with bottom-up brand, SKU, pack and channel evidence. Direct engagement with beverage distributors, retailers and category stakeholders helps verify product segmentation, competitive positioning, demand zones, regulatory exposure, channel economics and future opportunity areas in the Singapore Energy Drink Market.

- Executive Summary

- Research Methodology [market definitions and assumptions, RTD energy drink classification, formulated caffeinated beverage scope, non-alcoholic stimulant beverage inclusion, NAFDAC registration framework, excise-duty adjustment, top-down sizing, bottom-up sizing, retail audit checks, distributor interviews, SKU-level price-pack benchmarking]

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (youth consumers, open-market distribution, affordability, nightlife, transport corridors, work fatigue, gaming, local manufacturing)

- Market Challenges (excise duty, sugar scrutiny, NAFDAC registration, counterfeit risk, affordability pressure, cold-chain limitations)

- Market Opportunities (local energy brands, PET formats, sugar-free variants, herbal energy, open-market expansion, nightlife, transport channels, e-commerce)

- Market Trends (value energy, local challengers, sugar scrutiny, herbal energy, PET formats, nightlife activation, social media marketing)

- SWOT Analysis

- Porter’s Five Forces

- By Value (2020-2025)

- By Volume (2020-2025)

- By Unit Sales (2020-2025)

- By Product Type (In Value %)

Traditional Energy Drinks

Malt-Based Energy Drinks

Herbal Energy Drinks

Sugar-Free Energy Drinks - By Packaging Type (In Value %)

Aluminum Cans

PET Bottles

Glass Bottles

Multipacks

Large Cans - By Distribution Channel (In Value %)

Open Markets and Wholesale Depots

Kiosks and Roadside Retail

Supermarkets and Hypermarkets

Convenience Stores

Petrol Stations and Forecourts - By Region (In Value %)

Marina Bay

Orchard Road

Changi Business Park

West Region

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (caffeine mg per 100 ml, sugar grams per 100 ml, NAFDAC registration and label compliance, local manufacturing footprint, open-market and kiosk distribution depth, PET versus can portfolio, music-campus-nightlife activation intensity, affordability and pack-size architecture)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Red Bull Singapore

Monster Energy Singapore

PepsiCo Singapore

The Coca-Cola Company Singapore

Lucozade Ribena Suntory Singapore

Fraser and Neave Singapore

Yeo Hiap Seng

Otsuka Pharmaceutical Singapore

Taisho Pharmaceutical

TCP Group Singapore

HELL Energy Singapore

Carabao Energy Drink Singapore

Prime Hydration Singapore

G Fuel Singapore

Celsius Holdings Singapore

- Market Demand and Utilization

- Purchasing Power and Budget Allocation

- Regulatory and Compliance Requirements

- Needs, Desires and Pain Point Areas

- By Value (2026-2035)

- By Volume (2026-2035)

- By Unit Sales (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now