Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Singapore home finance market reached approximately USD ~ billion in outstanding residential mortgage balances based on Monetary Authority of Singapore housing loan statistics and central bank financial stability disclosures. The market is driven by sustained housing demand across public and private segments, high household income stability, and strong banking sector liquidity enabling long-tenor mortgage issuance. Government-linked housing financing schemes and regulated lending frameworks further support consistent credit flow, while digital mortgage origination and refinancing platforms accelerate borrower access and loan processing efficiency across financial institutions.

Within Singapore, mortgage demand is concentrated in major residential corridors such as Tampines, Woodlands, Jurong, and central region districts where housing supply and employment hubs are closely aligned. Dominance arises from integrated transport infrastructure, proximity to business zones, and large public housing estates financed through concessional loan structures. Private condominium financing activity is concentrated in central and eastern coastal districts due to expatriate housing demand and premium property development clusters, reinforcing geographic concentration of home finance origination and refinancing activity across urban zones.

Market Segmentation

By Product Type

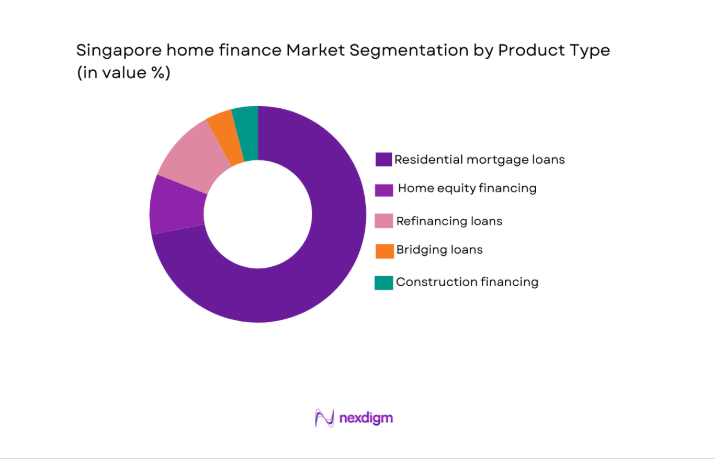

Singapore home finance market is segmented by product type into residential mortgage loans, home equity financing, refinancing loans, bridging loans, and construction financing. Recently, residential mortgage loans has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. High homeownership prevalence supported by public housing policies ensures continuous primary mortgage demand, while banks prioritize standardized residential lending due to lower credit risk and collateral security. Refinancing and equity products remain secondary as they depend on existing ownership cycles rather than new housing formation. Regulatory loan-to-value frameworks and concessional public housing financing further reinforce residential mortgages as the core lending product across lenders.

By Platform Type

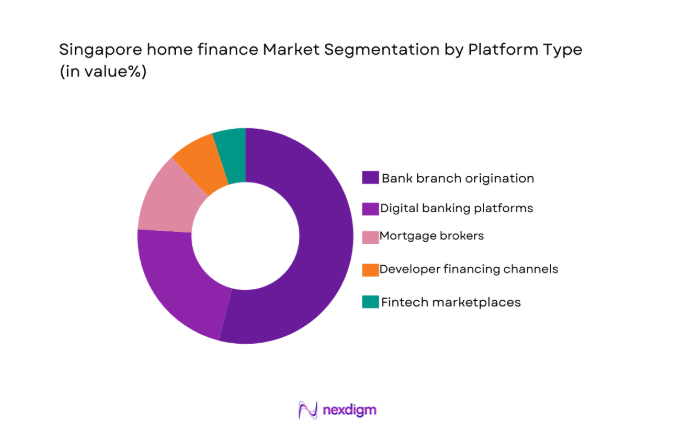

Singapore home finance market is segmented by platform type into bank branch origination, digital banking platforms, mortgage brokers, developer financing channels, and fintech marketplaces. Recently, bank branch origination has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Major banks maintain extensive physical advisory networks trusted for high-value mortgage decisions and regulatory documentation requirements. Borrowers prefer in-person consultation for complex loan structuring and property financing eligibility checks. While digital platforms are expanding, mortgage advisory and approval workflows remain relationship-driven, sustaining branch-led origination dominance across primary and refinancing housing finance transactions.

Competitive Landscape

Singapore home finance market is highly consolidated with three domestic banking groups dominating mortgage origination due to deposit strength, regulatory trust, and nationwide distribution networks. International banks and finance companies compete in niche expatriate and premium segments, while fintech comparison platforms influence pricing transparency and refinancing switching behavior.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Focus |

| DBS Bank | 1968 | Singapore | ~ | ~ | ~ | ~ | ~ |

| OCBC Bank | 1932 | Singapore | ~ | ~ | ~ | ~ | ~ |

| United Overseas Bank | 1935 | Singapore | ~ | ~ | ~ | ~ | ~ |

| Standard Chartered | 1969 (SG) | Singapore | ~ | ~ | ~ | ~ | ~ |

| HSBC Singapore | 1877 (SG) | Singapore | ~ | ~ | ~ | ~ | ~ |

Singapore home finance Market Analysis

Growth Drivers

Public Housing-Led Mortgage Demand Stability

Public housing-led mortgage demand stability forms the structural backbone of Singapore home finance expansion because the majority of households purchase subsidized or regulated housing units financed through institutional lending frameworks that integrate housing policy with banking credit delivery. The state-supported housing development system continuously releases new housing supply aligned with demographic formation and household upgrading cycles, ensuring a predictable pipeline of mortgage borrowers entering the financial system each year. Mortgage providers benefit from standardized property valuation, regulated pricing bands, and clear eligibility criteria that significantly reduce underwriting uncertainty and credit volatility compared with private housing markets in other countries. Concessional financing schemes and structured repayment models for public housing buyers enable borrowers with moderate incomes to access long-tenor housing loans while maintaining strong repayment performance, reinforcing lender confidence and portfolio expansion capacity. The integration of public housing allocation, mortgage approval, and ownership transfer through centralized administrative platforms accelerates loan origination cycles and reduces processing friction across the housing finance ecosystem. High owner-occupation rates supported by housing policy create sustained baseline demand for primary mortgages rather than speculative lending, stabilizing credit growth across economic cycles. As households progress through life stages and upgrade from smaller to larger public or private units, refinancing and new mortgage issuance activity expands proportionally, maintaining consistent portfolio turnover within banks. Mortgage markets therefore remain structurally anchored to housing policy design rather than purely market-driven property cycles, reducing volatility and supporting long-term credit expansion. Financial institutions align product structures, pricing strategies, and capital allocation with predictable public housing demand flows, ensuring continued scale and stability in Singapore home finance origination and outstanding loan balances.

High Income Stability and Banking Liquidity Supporting Long-Tenor Lending

High income stability and banking liquidity supporting long-tenor lending drives Singapore home finance growth because the country maintains one of the world’s strongest household income profiles and banking sector capitalization levels, enabling lenders to extend large mortgage volumes with controlled credit risk exposure. Stable employment structures across advanced services, technology, and government sectors provide borrowers with reliable repayment capacity, allowing financial institutions to offer extended loan tenures that reduce monthly servicing burdens while increasing loan eligibility thresholds. Domestic banks maintain strong deposit bases and regulatory capital adequacy ratios, ensuring sufficient liquidity to fund long-duration mortgage assets without funding mismatches or interest rate risk pressures that constrain lending in less stable financial systems. Predictable income growth trajectories allow borrowers to upgrade housing over time, generating repeat mortgage demand and refinancing cycles that expand overall credit portfolios within the banking sector. Low default rates and high asset recovery values in Singapore’s regulated property market reinforce lender confidence to scale mortgage lending without excessive provisioning costs. Monetary policy transmission and interest rate pass-through mechanisms remain efficient, enabling lenders to adjust mortgage pricing while maintaining borrower affordability within regulated debt servicing thresholds. Strong financial system supervision ensures mortgage underwriting standards remain prudent, preventing speculative excesses while sustaining credit expansion aligned with economic fundamentals. Cross-selling opportunities between mortgages and wealth management, insurance, and transaction banking further incentivize banks to prioritize housing finance growth as a core retail banking strategy. Combined income stability and liquidity strength therefore sustain long-term expansion of Singapore home finance through secure borrower capacity and institutional lending resilience.

Market Challenges

Macroprudential Lending Restrictions Limiting Borrowing Capacity

Macroprudential lending restrictions limiting borrowing capacity represent a structural constraint in Singapore home finance because regulatory authorities impose strict loan-to-value limits, total debt servicing ratio thresholds, and borrower eligibility controls designed to prevent housing speculation and systemic financial risk accumulation. These prudential safeguards reduce the maximum mortgage size accessible to borrowers relative to property value, particularly for investment properties and second-home purchases, thereby constraining credit expansion potential despite strong housing demand. Borrowers with adequate income and savings may still face reduced loan eligibility under debt servicing caps that aggregate all outstanding obligations, limiting financing accessibility especially for middle-income households seeking housing upgrades. Financial institutions must allocate significant compliance resources to monitor borrower liabilities, income verification, and property ownership status under evolving regulatory frameworks, increasing origination costs and processing complexity. Policy tightening cycles introduced to cool housing markets can abruptly reduce transaction volumes and mortgage approvals, generating volatility in lending pipelines and bank revenue forecasts. Investors and expatriate buyers face additional restrictions and taxes that suppress leveraged property acquisition financed through mortgages, narrowing growth segments for lenders. The regulatory environment also limits product innovation such as high loan-to-value mortgages or flexible repayment structures that might otherwise expand borrower inclusion. Mortgage demand therefore remains structurally capped by prudential policy objectives prioritizing financial stability over credit growth. While these regulations maintain systemic resilience and low default risk, they simultaneously constrain the scale and elasticity of Singapore home finance expansion across borrower categories and property segments.

High Property Prices Constraining First-Time Buyer Entry

High property prices constraining first-time buyer entry challenge Singapore home finance growth because housing affordability relative to income levels determines the volume of new mortgage borrowers entering the market each year, and sustained price appreciation raises the financial barrier to ownership despite stable economic conditions. Elevated land scarcity and controlled housing supply in a dense urban environment drive property valuation upward across both public and private segments, requiring larger down-payments and higher loan amounts that exceed affordability thresholds for younger households. Even with concessional financing schemes, borrowers must accumulate substantial savings to meet equity requirements and transaction costs before accessing mortgage financing, delaying entry into homeownership and reducing loan origination volumes. Rising property values also increase debt servicing burdens relative to income under regulatory caps, further restricting loan eligibility despite borrower willingness. Financial institutions face limited ability to mitigate affordability constraints because lending ratios and underwriting criteria remain tightly regulated to prevent over-leveraging. Housing upgrades become more financially demanding, reducing repeat mortgage activity and slowing refinancing cycles that typically sustain portfolio growth. Investor participation financed through mortgages declines when property prices compress rental yields relative to financing costs, reducing demand from leveraged buyers. Geographic concentration of affordable housing in specific districts can also limit borrower choice and transaction volume in preferred employment locations. Consequently, elevated property prices act as a structural ceiling on borrower expansion and mortgage penetration, constraining long-term growth potential in Singapore home finance despite strong economic fundamentals and banking sector capacity.

Opportunities

Green and Energy-Efficient Housing Finance Expansion

Green and energy-efficient housing finance expansion presents a significant opportunity in Singapore home finance because national sustainability targets and building efficiency standards are driving demand for environmentally certified residential properties that require specialized mortgage products aligned with green financing frameworks. Financial institutions are increasingly integrating sustainability criteria into mortgage underwriting by offering preferential interest rates or incentives for properties meeting energy efficiency or environmental certification benchmarks, encouraging borrowers to select green housing developments. Developers are simultaneously expanding supply of energy-efficient residential projects incorporating smart energy systems, sustainable materials, and low-carbon construction standards that align with regulatory climate objectives. Government support for green finance initiatives and sustainable urban development strengthens policy alignment between housing finance and environmental goals, enabling banks to access green funding channels and sustainability-linked capital markets to finance qualifying mortgage portfolios. Borrowers benefit from lower utility costs and long-term asset value resilience associated with energy-efficient properties, enhancing repayment capacity and collateral quality for lenders. Institutional investors and global funding providers increasingly prioritize green mortgage-backed assets, expanding liquidity and securitization potential for sustainable housing finance portfolios. Digital property valuation and certification verification systems further enable lenders to identify eligible green properties and streamline approval processes. As environmental awareness and regulatory incentives intensify, green housing finance adoption is expected to scale across both public and private housing segments. The convergence of sustainability policy, developer supply, borrower preference, and financial innovation therefore positions green mortgages as a major growth avenue within Singapore home finance markets.

Digital Mortgage Ecosystem and Platform Integration

Digital mortgage ecosystem and platform integration offers a transformative opportunity in Singapore home finance because technological integration across property search, credit assessment, documentation, and loan servicing can significantly reduce friction, cost, and processing time in mortgage origination and refinancing cycles. Financial institutions are investing in end-to-end digital mortgage journeys enabling borrowers to compare rates, submit applications, verify income data, and receive approvals through online platforms without physical branch interaction, expanding accessibility and operational efficiency. Integration between real estate portals, valuation databases, and banking systems allows seamless transfer of property and borrower data into underwriting workflows, accelerating decision timelines and improving customer experience. Automated credit scoring and income verification through open banking data sources enhance risk assessment accuracy while reducing manual documentation requirements that traditionally slow mortgage approvals. Digital refinancing platforms enable borrowers to switch lenders more easily in response to interest rate changes, increasing competitive dynamics and transaction volumes within the mortgage market. Lenders benefit from lower acquisition costs and scalable distribution channels capable of reaching digitally native borrowers and expatriate clients remotely. Regulatory acceptance of electronic documentation and digital identity verification further legitimizes fully digital mortgage processes. Fintech partnerships and marketplace ecosystems are expanding cross-institution loan comparison and origination channels, increasing transparency and borrower choice. As digital adoption accelerates across financial services and property transactions, integrated mortgage ecosystems are expected to expand origination efficiency and overall Singapore home finance market activity.

Future Outlook

Singapore home finance is expected to expand steadily over the next five years supported by stable housing demand, sustained household income strength, and continued banking sector liquidity. Digital mortgage platforms and refinancing ecosystems will enhance accessibility and processing efficiency across lenders. Sustainability-linked housing finance and green property development will create new lending segments aligned with national climate objectives. Regulatory frameworks will continue balancing financial stability with housing affordability, sustaining long-term mortgage market resilience and moderate credit growth.

Major Players

- DBS Bank

- OCBC Bank

- United Overseas Bank

- Standard Chartered Singapore

- HSBC Singapore

- Maybank Singapore

- Citibank Singapore

- Bank of China Singapore

- Hong Leong Finance

- Singapura Finance

- RHB Bank Singapore

- CIMB Bank Singapore

- ANZ Singapore

- Credit Suisse Singapore

- Deutsche Bank Singapore

Key Target Audience

- Retail banks

- Housing finance companies

- Property developers

- Real estate investment trusts

- Institutional investors

- Government and regulatory bodies

- Investment and venture capitalist firms

- Mortgage technology providers

Research Methodology

Step 1: Identification of Key Variables

Key variables influencing Singapore home finance including housing supply, mortgage rates, regulatory lending caps, borrower income profiles, and banking liquidity conditions are identified through policy review and financial statistics mapping. Market structure boundaries and segmentation definitions are established to ensure consistent data interpretation across housing finance categories.

Step 2: Market Analysis and Construction

Mortgage outstanding volumes, origination flows, property transaction activity, and lending channel distribution are analyzed to construct the Singapore home finance market model. Data triangulation across banking disclosures, housing authority statistics, and property transaction datasets ensures reliable estimation of segmentation and competitive structure.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings regarding demand drivers, regulatory constraints, and competitive positioning are validated through consultation with mortgage advisors, banking professionals, and housing policy analysts. Expert inputs refine assumptions on borrower behavior, refinancing cycles, and digital adoption trends shaping the market outlook.

Step 4: Research Synthesis and Final Output

Validated data and insights are synthesized into structured analysis covering segmentation, competitive dynamics, growth drivers, challenges, and opportunities in Singapore home finance. Final outputs integrate quantitative estimates with qualitative interpretation to provide decision-ready market intelligence aligned with industry and policy realities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Sustained housing demand supported by population growth and household formation

Low unemployment and high income stability enabling mortgage affordability

Strong banking sector liquidity supporting long-tenor mortgage lending

Government housing schemes encouraging home ownership financing uptake

Digital mortgage origination improving customer access and processing speed - Market Challenges

Property cooling measures limiting loan-to-value ratios and borrowing capacity

Interest rate volatility impacting mortgage affordability and refinancing activity

High property prices constraining entry of first-time buyers

Tight macroprudential regulations increasing lender compliance burden

Limited land supply restricting housing stock expansion - Market Opportunities

Green mortgage products linked to energy-efficient housing

Digital refinancing and mortgage switching platforms

Cross-border financing for overseas property acquisition - Trends

Shift toward fixed-rate and hybrid mortgage packages

Expansion of digital end-to-end mortgage journeys

Integration of property search and financing platforms

Rising refinancing cycles driven by rate movements

Growth of sustainability-linked housing finance - Government Regulations & Defense Policy

Loan-to-value and total debt servicing ratio regulations

Stamp duty and property ownership eligibility policies

Public housing financing eligibility frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential mortgage loans

Home equity financing

Refinancing and repricing facilities

Construction and bridging loans

Islamic and Sharia-compliant home financing - By Platform Type (In Value%)

Bank branch origination

Digital banking platforms

Mortgage broker channels

Property developer tie-ups

Fintech mortgage marketplaces - By Fitment Type (In Value%)

Public housing (HDB) financing

Private condominium financing

Landed property financing

Executive condominium financing

Overseas property financing - By End User Segment (In Value%)

First-time homebuyers

Upgraders and repeat buyers

Property investors

Expatriate buyers

Corporate and trust buyers

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Interest rate structure, Loan tenure flexibility, Digital origination capability, Approval turnaround time, LTV policy flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DBS Bank

OCBC Bank

United Overseas Bank

Standard Chartered Singapore

HSBC Singapore

Maybank Singapore

Citibank Singapore

Bank of China Singapore

Hong Leong Finance

Singapura Finance

RHB Bank Singapore

CIMB Bank Singapore

ANZ Singapore

Credit Suisse Singapore

Deutsche Bank Singapore

- First-time buyers rely heavily on public housing financing schemes and concessional mortgage structures

- Upgraders drive refinancing and larger ticket private property loans

- Investors focus on rental yield optimization and leverage strategies

- Expatriate buyers require cross-border compliance and foreign ownership financing solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now