Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Singapore Hybrid Aircraft Market is valued at approximately USD ~ billion in 2024, driven by rapid advancements in hybrid propulsion technologies and the push for carbon-neutral aviation. The market’s growth is propelled by factors such as stringent environmental regulations, government incentives supporting sustainable aviation, and the increasing need for energy-efficient solutions in the aviation industry. The growth of urban air mobility (UAM) solutions and the rising demand for low-emission aircraft for regional aviation are also contributing to the market’s expansion.

Singapore, as a global aviation hub, plays a dominant role in the hybrid aircraft market due to its strategic position in Southeast Asia, its advanced aerospace infrastructure, and its commitment to becoming a leader in sustainable aviation. The city-state’s strong regulatory frameworks, government-backed sustainability initiatives, and major international airline presence create a conducive environment for hybrid aircraft adoption. Furthermore, its development as a testbed for urban air mobility (UAM) makes it a focal point for innovation in hybrid aircraft technologies.

Market Segmentation

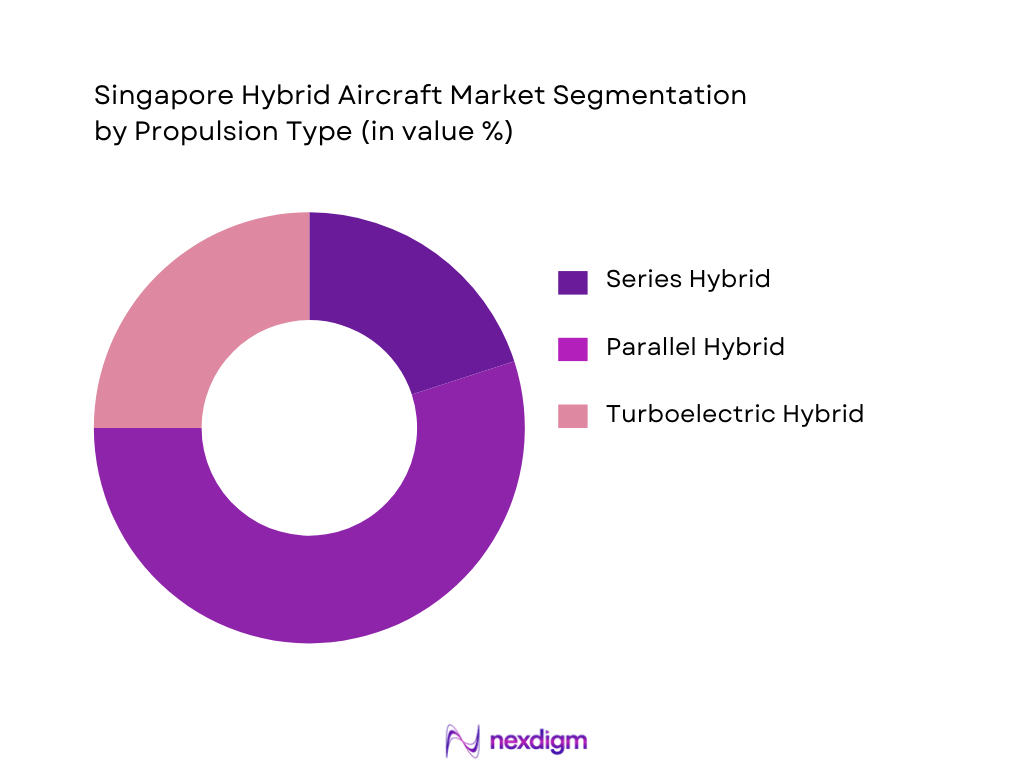

By Propulsion Type

The Singapore Hybrid Aircraft Market is segmented by propulsion type into series hybrid, parallel hybrid, and turboelectric hybrid systems. The parallel hybrid propulsion system currently dominates the market share, primarily because it offers greater flexibility and efficiency for both short and medium-haul flights. This system allows the aircraft to operate using a combination of electric and traditional engines, improving fuel efficiency while reducing carbon emissions. The development of lighter, more efficient batteries and turbofan engines has solidified the parallel hybrid system’s position in the market.

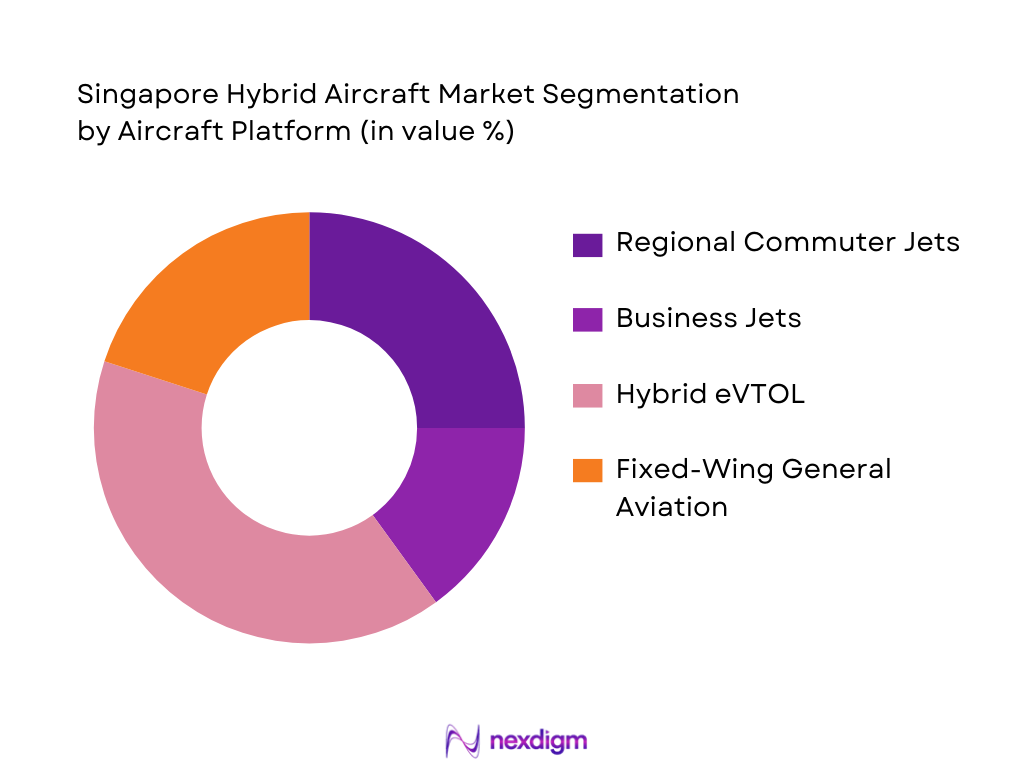

By Aircraft Platform

The market is also segmented by aircraft platform, which includes regional commuter jets, business jets, hybrid eVTOL, and fixed-wing general aviation. Among these, hybrid eVTOL platforms are witnessing the highest growth. Singapore’s emphasis on urban air mobility (UAM) and the integration of advanced air mobility solutions make hybrid eVTOL platforms a focal point. These aircraft are increasingly seen as the future of urban transportation, where quick, eco-friendly travel across short distances is essential. The regulatory support and infrastructure development in Singapore have contributed to the increasing adoption of hybrid eVTOLs.

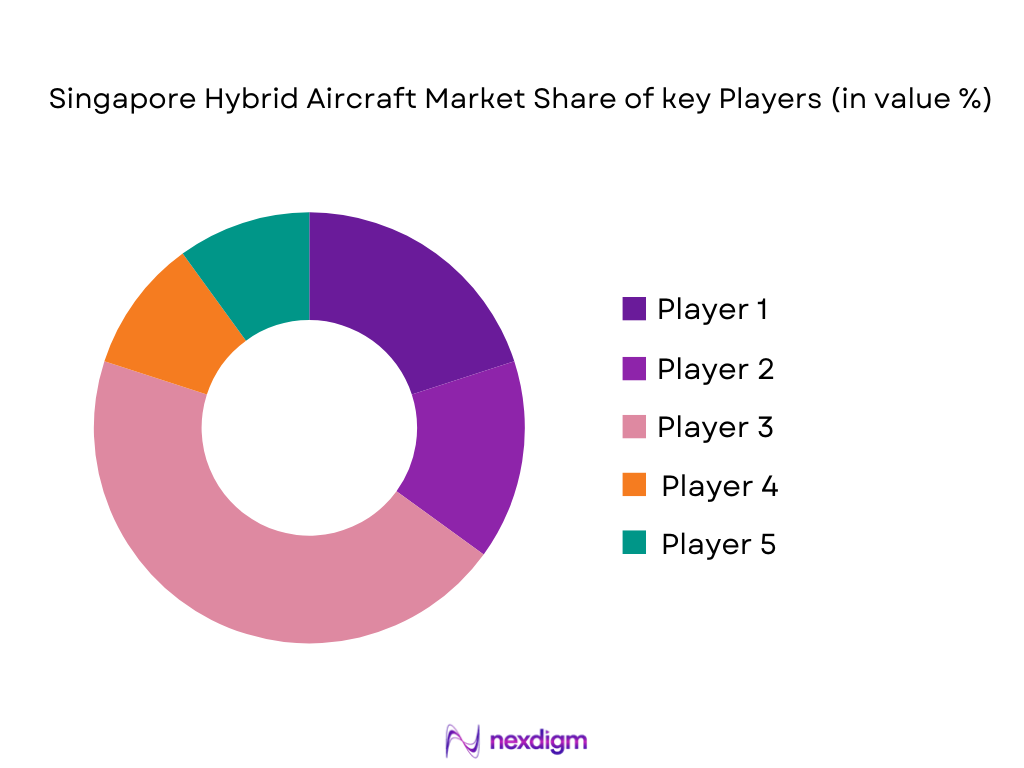

Competitive Landscape

The Singapore Hybrid Aircraft Market is highly competitive, with a mix of global aerospace giants and local companies contributing to its growth. Major players such as Airbus, Boeing, Rolls-Royce, and Embraer dominate the market due to their extensive resources, technological expertise, and ongoing investments in hybrid propulsion systems. Local firms are also gaining traction by collaborating with international players and focusing on niche solutions like hybrid eVTOL platforms for urban mobility. This competitive landscape showcases the consolidation of expertise from both local and international companies in advancing hybrid aircraft technologies.

| Company Name | Establishment Year | Headquarters | Market Share | Key Technologies | Strategic Partnerships | Annual Revenue | Number of Employees |

| Airbus | 1970 | France | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Rolls-Royce | 1906 | UK | ~ | ~ | ~ | ~ | ~ |

| Embraer | 1969 | Brazil | ~ | ~ | ~ | ~ | ~ |

| MagniX | 2009 | USA | ~ | ~ | ~ | ~ | ~ |

Singapore Hybrid Aircraft Market Analysis

Growth Drivers

Sustainability & Net-Zero Aviation Mandates

Sustainability and net-zero aviation targets are powerful growth drivers for the Singapore Hybrid Aircraft Market. The Singapore government has committed to achieving net-zero emissions , aligning with global aviation sustainability goals. This includes the development of hybrid aircraft as a key enabler for reducing carbon footprints in aviation. With stricter environmental regulations and increasing pressure on the aviation industry to decarbonize, the demand for hybrid aircraft, which combine traditional and electric propulsion systems, is rising. These aircraft help reduce fuel consumption and lower emissions, supporting both commercial and regional airlines in meeting sustainability goals. The regulatory framework in Singapore promotes such eco-friendly solutions, offering incentives for companies developing or adopting green technologies in aviation, including hybrid propulsion systems.

Carbon Emission Reduction Targets

Carbon emission reduction targets are a key driver in the growth of the hybrid aircraft market in Singapore. As part of its commitment to the Paris Agreement and international aviation standards set by ICAO (International Civil Aviation Organization), Singapore has set ambitious targets for reducing aviation carbon emissions. Hybrid aircraft provide an immediate solution by improving fuel efficiency and reducing CO2 emissions during flight. The market for these aircraft is therefore expected to grow rapidly as airlines and operators strive to meet stringent emission reduction targets set by both local authorities and international bodies.

Market Challenges

Battery Energy Density Constraints

One of the primary challenges faced by the Singapore Hybrid Aircraft Market is the limitation in battery energy density. Hybrid aircraft rely on batteries to power electric motors for a portion of their operations, but current battery technologies are not yet capable of providing sufficient energy density for longer flights, particularly in larger aircraft. This limitation restricts the practical use of hybrid aircraft to shorter regional routes, as batteries need to be light, compact, and capable of delivering high energy output. Until advancements in battery technology can provide better energy density with lower weight, hybrid aircraft will face limitations in their market adoption, particularly for long-haul flights.

Hybrid Aircraft Certification & Airworthiness Complexity

Certification and airworthiness complexity are significant barriers in the hybrid aircraft market. Given that hybrid propulsion systems combine both electric and traditional engines, they require specialized testing and certification processes to ensure they meet international safety standards. This adds complexity and lengthens the timeline for bringing these aircraft to market. In Singapore, while the Civil Aviation Authority of Singapore (CAAS) is supportive of green aviation, the regulatory requirements for hybrid aircraft are still evolving. Achieving certification for hybrid aircraft involves rigorous testing to ensure safety, reliability, and compliance with environmental standards, which increases costs and delays the widespread adoption of these aircraft.

Opportunities

Technological Advancements in Hybrid Propulsion Systems

Technological advancements in hybrid propulsion systems are creating significant opportunities in the Singapore Hybrid Aircraft Market. As hybrid propulsion technologies evolve, they are becoming more efficient and cost-effective. Developments in lightweight materials, energy management systems, and power electronics are enhancing the performance of hybrid aircraft. Improvements in battery technology, fuel cells, and electric motors are making hybrid propulsion systems more viable for a wider range of aircraft types. These advancements are particularly relevant in Singapore, which is positioning itself as a leader in sustainable aviation. The local market, supported by government initiatives and international collaborations, offers a fertile ground for the commercialization of these next-generation hybrid propulsion systems.

Urban Air Mobility (UAM) Growth

Urban air mobility (UAM) represents one of the most promising opportunities for hybrid aircraft in Singapore. The rapid development of UAM solutions, such as electric vertical takeoff and landing (eVTOL) aircraft, is driving the demand for hybrid aircraft that can efficiently operate in urban environments. Singapore’s forward-thinking approach to smart city development, along with its focus on sustainability and reducing congestion, makes it an ideal testbed for hybrid eVTOL platforms. These aircraft can serve as an alternative to ground transportation, offering quick, eco-friendly air travel solutions in dense urban areas. The government’s commitment to supporting UAM infrastructure, including charging stations and regulatory frameworks, further strengthens the growth prospects for hybrid aircraft in this segment.

Future Outlook

The Singapore Hybrid Aircraft Market is expected to experience significant growth in the coming years, driven by ongoing advancements in hybrid propulsion technologies, increased government support for sustainable aviation, and the growing demand for low-emission air travel solutions. As urban air mobility and hybrid eVTOL aircraft gain traction, Singapore is poised to lead the way in testing and adopting these innovative aircraft solutions. Furthermore, the push towards carbon-neutral aviation, combined with breakthroughs in battery technology, will likely result in accelerated market adoption, ensuring continued growth for hybrid aircraft solutions.

Major Players

- Airbus

- Boeing

- Rolls-Royce

- Embraer

- MagniX

- Honeywell Aerospace

- GE Aviation

- Safran

- Zunum Aero

- Bye Aerospace

- Joby Aviation

- Lilium

- Vertical Aerospace

- Pipistrel

- Ampaire

Key Target Audience

- Government and regulatory bodies (Civil Aviation Authority of Singapore (CAAS), International Civil Aviation Organization (ICAO))

- Investment and venture capitalist firms

- Airlines and commercial aviation companies

- Airport operators and infrastructure developers

- Aircraft manufacturers and OEMs

- Urban air mobility (UAM) startups and developers

- Aerospace technology developers and component suppliers

- Environmental and sustainability advocacy groups

Research Methodology

Step 1: Identification of Key Variables

This phase involves creating an ecosystem map for the Singapore Hybrid Aircraft Market by identifying key stakeholders such as OEMs, regulatory bodies, infrastructure providers, and UAM developers. A combination of secondary data and proprietary databases will be utilized to ensure comprehensive insights into market drivers and barriers.

Step 2: Market Analysis and Construction

We will assess historical data on hybrid aircraft adoption rates, regulatory milestones, and technological advancements. This phase will also include a deep dive into customer adoption behaviors, such as fleet modernization and sustainability initiatives by airlines.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be validated through interviews with industry experts from aerospace companies, technology developers, and government agencies. These consultations will provide qualitative insights into technological trends and regulatory challenges, aiding in refining the market data.

Step 4: Research Synthesis and Final Output

The final stage will include validation through direct engagement with key market players, such as hybrid aircraft manufacturers and airlines, to refine the understanding of market dynamics. The output will be a comprehensive report detailing trends, forecasts, and recommendations for stakeholders.

- Executive Summary

- Research Methodology

(Market Definitions & Assumptions, Abbreviations, Hybrid Propulsion Technology Taxonomy, Battery Chemistry, Energy Density & Power-to-Weight Assumptions, Emission Benchmarks & Compliance Thresholds, Singapore Aviation Policy & Sustainability Framework Assumptions, Data Sourcing & Validation Framework, Primary Interview Structure (OEMs, Regulators, Operators, MROs), Limitations, Risks & Future Research Direction)

- Definition and Scope of Hybrid & Hybrid-Electric Aircraft

- Propulsion Hybridization Levels

- Energy Source Architectures – Series Hybrid, Parallel Hybrid, Turboelectric

- Singapore Aviation Industry Genesis & Hybrid Technology Adoption Milestones

- ASEAN & Asia-Pacific Aviation Integration Impact on Singapore

- Singapore Hybrid Aircraft Value Chain Structure (OEMs, Tier-1 System

- Integrators, Airports, MRO Providers, Regulators)

- Component & Sub-System Supply Chain Mapping

- Growth Drivers

Sustainability & Net-Zero Aviation Mandates

Carbon Emission Reduction Targets

Airport Electrification & Smart Infrastructure Rollout - Market Challenges

Battery Energy Density Constraints

Hybrid Aircraft Certification & Airworthiness Complexity

Charging, Fueling & Ground Infrastructure Gaps

High Initial Capital & Retrofitting Costs - Opportunities

Technological Advancements in Hybrid Propulsion Systems

Urban Air Mobility (UAM) Growth

Emission Reduction Mandates

Regional Aviation Network Expansion

Infrastructure Development

Investment and Funding

Growing Demand for Low-Cost, Sustainable Aviation

Integration with Smart City & Mobility Solutions - Investment & Funding Landscape

Venture Capital & Strategic Investors

Government Grants & Green Aviation Incentives

Public-Private R&D Partnerships - Technology & Innovation Trends

Hybrid + Hydrogen Fuel Cell Convergence

Lightweight Materials & Structural Electrification

Advanced Thermal Management & Energy Optimization - Regulatory & Compliance Environment

CAAS Certification Framework

ICAO Emission & Noise Standards Alignment - Macro-Economic, Trade & Geopolitical Impact

- Porter’s Five Forces Analysis

- SWOT & Strategic Imperatives

- Market Value, 2020-2025

- Volume Consumption Across Subsegments, 2020-2025

- Composite Adoption Intensity, 2020-2025

- By Propulsion Type (In Value %)

Series Hybrid

Parallel Hybrid

Turboelectric Hybrid

- By Aircraft Platform (In Value %)

Regional Commuter Aircraft

Business & Corporate Jets

Hybrid eVTOL & Air Taxi Platforms

Fixed-Wing General Aviation Aircraft

Hybrid Cargo & Logistics Drones

- By Energy System Architecture (In Value %)

Battery-Dominant Hybrid Systems

Fuel Cell-Integrated Hybrid Systems

Hybrid Turbogenerator + Electric Drive Systems

- By Operational Range Profile (In Value %)

Short-Range Regional Operations

Medium-Range Commuter Operations

Extended-Range Hybrid Applications

- By Application End-Use (In Value %)

Commercial Passenger Aviation

Urban Air Mobility & Advanced Air Mobility

Defense & Government Operations

Cargo, Express & Logistics

General & Recreational Aviation

- Market Share & Competitive Positioning by Value & Aircraft Units

- Cross-Comparison Parameters (Propulsion Technology Maturity, Battery Energy Density & Power Output Metrics, Certification & Regulatory Readiness, Strategic Alliances & Ecosystem Partnerships, Revenue Mix by Aircraft Platform, Fleet Commitments & Order Backlog, Operational Range & Payload Capability, Aftermarket, MRO & Support Infrastructure, R&D Intensity & Capital Allocation)

- Detailed Company Profiles

Airbus

Boeing

Rolls-Royce

Honeywell Aerospace

GE Aviation

Safran

Embraer

MagniX

Ampaire

Zunum

Aero

Bye Aerospace

Joby Aviation

Lilium

Vertical Aerospace

Pipistrel

- Demand Elasticity & Adoption Curve Analysis

- Airlines vs Urban Air Mobility Operators

- Operating Cost & Lifecycle Economics Comparison

- Procurement Decision Framework

- Total Cost of Ownership

- ESG & Sustainability Alignment

- Route Optimization & Network Efficiency

- End-User Pain Points & Performance Expectations

- Forecast by Value & Growth Scenarios, 2026-2035

- Forecast by Volume & Composite Penetration, 2026-2035

- Future Demand by Aircraft Segment, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now